Is it kind to bequeath debt to your children?

The theme of New Zealand’s approach to the pandemic Covid-19 is “be kind”.

It motivated a prolonged lockdown requiring $22 bln of government spending commitments and a further contingency of $39.3 bln. Since borrowing is a core part of this policy, it is reasonable to ask if kindness will determine how we deal with the debts the policy creates?

Living in interesting times

The government approach to the Covid-19 pandemic prioritised the lives of the elderly over economic activity. To do this they required most people in work to go on leave and offered them an advance on future wages funded through additional government debt. An academic industry is undoubtedly forming to understand if this and other responses were optimal.

Currently all we can say with confidence is that the New Zealand government’s approach appears to have worked on its own terms. The cost was that it left the country with substantial extra debts.

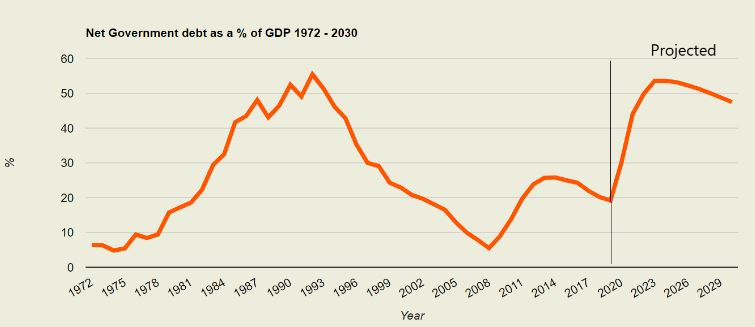

Graph 1

Source: Politik using NZIER and Treasury data.

Debt is just a tool of government policy. The tool can be used badly of which Robert Muldoon’s fight to maintain New Zealand’s as a colonial economy that drove the increase in the 1970s and 80s being a good example.

It is hard to think of a better reason for taking on debt than tackling a once in a hundred years global pandemic.

Does the government debt matter?

Sometimes personal intuitions do not work well when thinking about government finances. (If the government prints money it’s called quantitative easing, if you do it’s called forgery.)

Government debt is more intuitive. Debt matters to governments because after the initial capital is spent, the debt limits what they can do.

In the short term this means diverting income to finance the debt. Thus, even in what now seems like the good old days of 2019, debt financing cost $4.3 bln, or more than triple the $1.2 bln spent on Oranga Tamariki, the child protection agency.

As with individual borrowing, if government debts are not repaid they accumulate and lenders tend to charge more.

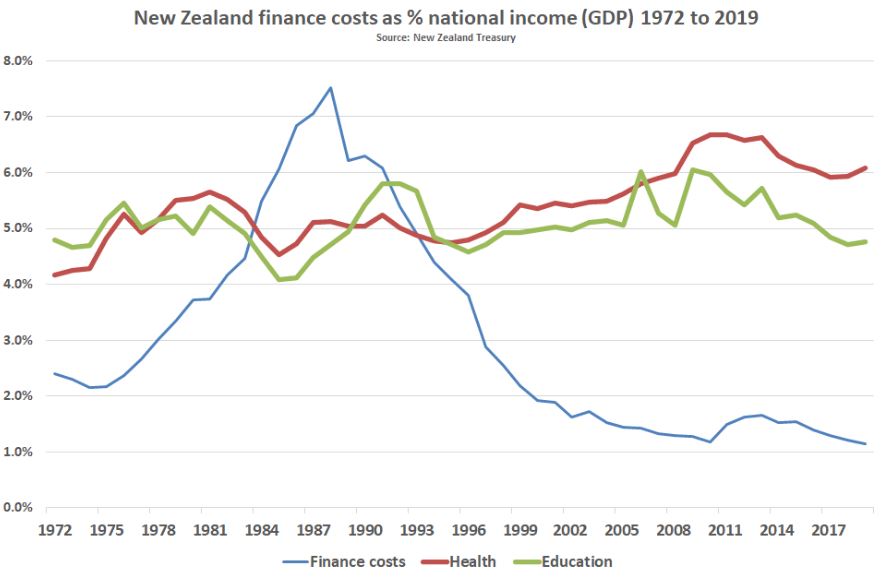

While these lenders do not threaten to break our fingers, the price they charge can be extortionary. The graph below shows the proportion of national income the New Zealand government spent on debt financing and compares it with spending on education and health. You are not reading it wrong. Between 1984 and 1991, New Zealand spent more on financing government debt, basically bonds the relatively wealthy use to improve their savings and pensions portfolios, than it was spending on either health or education. Debt can be useful, but lenders are rarely kind.

Graph 2

Source: https://treasury.govt.nz/publications/information-release/data-fiscal-t…

What can we learn from the last time we flattened a curve?

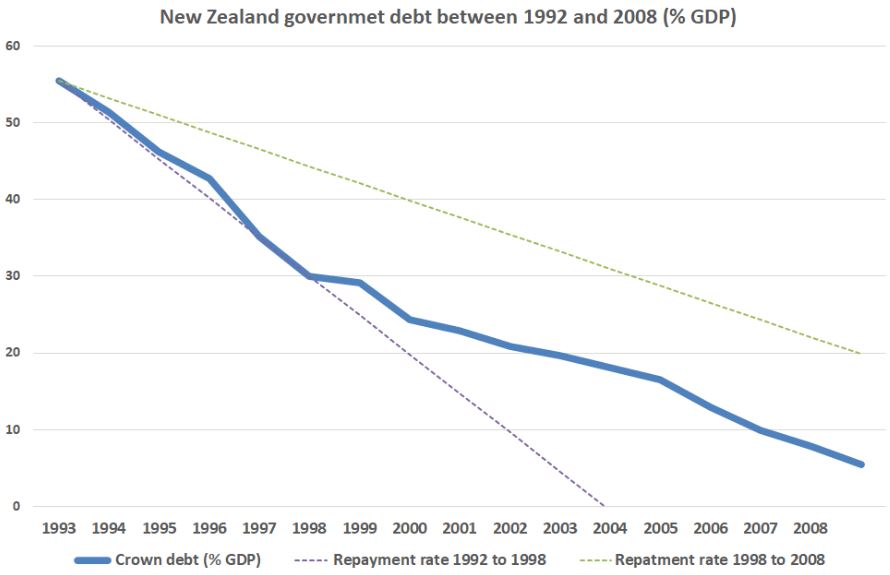

One of the few silver linings in the long grey cloud of Muldoon’s premiership is we learned how to reduce debt from over 50% of national income to around 5%.

The reduction had two components: running a balanced budget while the nominal value of the economy grew and directly repaying the debt. From 1992 until 1998 the government did both, leading to an average annual reduction of more than 5.1% per year. If we had continued at that rate we would have reached the minimal debt achieved just before the GFC by 2002/3 and had the entire debt paid off by 2004.

Graph 3

Source:NZIER ( https://data1850.nz/) with calculations by the author

This did not happen because policy softened and balancing the budget became the main instrument. Reductions in debt as a proportion of income between 1999 and 2008 were at 2.2% per year, less than half those in the first phase. Had this been the policy from 1992, the debt level when the GFC struck in 2008 would have been around 20% of GDP, or close to its peak after the GFC. The Covid-19 response would have taken New Zealand government debt to more than 70% of GDP. It is unlikely our current leaders want to hear this, but the ease with which they could be kind in 2020 is largely due to Ruth Richardson’s budgeting in the early 90s.

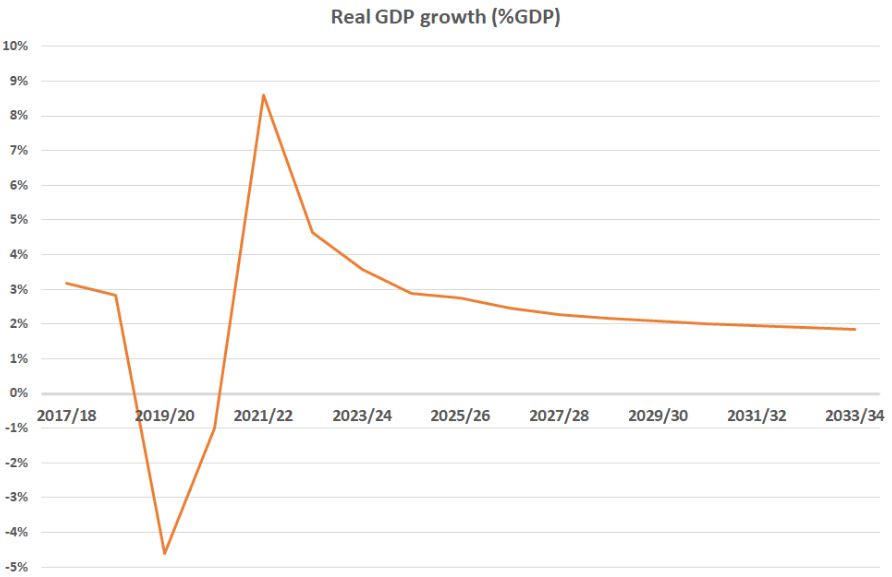

One important difference between now and the 1980s is that finances costs worldwide are considerably lower and falling. This means we are in the counterintuitive position that short run finance costs will fall as the amount of debt triples. The Treasury budget modelling predicts this happy coincidence will unwind over the next fifteen years, with costs increasing from the current 1.3% of GDP to 3.2% by the mid-2030s.

A less benign difference is greater uncertainty about New Zealand’s economic growth. The Treasury predicts two years of contraction followed by a, frankly, non-credible real GDP growth of 8.6% in 2021/22. (This is not far short of China’s growth during its boom years.) In fairness, the speed at which the once in a century pandemic emerged gave no realistic chance to improve the model in time for the budget. Their model is one for normal times, based on the economy suffering a shock and going “back to normal”. The BEFU is very clear about the uncertainty.

Graph 4

Source: https://treasury.govt.nz/sites/default/files/2020-05/fsm-befu20.xlsx

The most important lesson from previous experience is that debts from the Covid-19 response can be repaid before a new crisis. This time we will have less immediate financial pressure, but we will probably have to rely more on politically difficult direct debt repayment.

How are we going to prepare for the next crisis?

My daughter is in the latter years of primary school. Assuming she gets a tertiary education and does the traditional kiwi OE, she will be starting her career in around 15 years. How fast we repay the debt from this crisis is a decision on how much we want her and other primary school children to carry the financial risks associated with Covid-19 when the next crises come along. The 2020 Budget had nothing to say on this.

Like any other debt, the weight of government debt can be reduced by some combination of minimising the debt to be repaid, increasing income and decreasing expenditure. These are considered below.

Minimising the debt

In the 2020 budget the government set aside a contingency of $39.3bn. That would let them deal with one new national outbreak and several local outbreaks. In itself this seems completely sensible. However it will be a test of will to remain sensible in the face of pressures to spend that money if those contingencies do not arise. Virtue will have one reward: it is unlikely the government will muster the close to 90% support they had for their Covid-19 strategy for any other approach to debt reduction.

One more unpopular strategy has a potentially greater impact. The New Zealand Superannuation Fund (NZSF) is a government owned fund intended to make New Zealand Superannuation (NZS) more affordable when population aging increases the cost of NZS later this century. Those people it is meant to help are also those currently in the workforce at risk from the current economic downturn. Contributions are continuing and by 2023 this fund is projected to be worth around $60bn. It is frankly bizarre the government is still budgeting to contribute to the scheme over the next few years. This feels a little like saving money while not paying off your credit card bills.

More ambitiously, funds already saved could be used to pay for the Covid-19 response. Clearly this is a different use for the fund, but used in this way it is helping the individuals it was designed to help, just earlier than was foreseen when the fund was set up. Spending in the spirit of an initiative’s intent rather than following the bureaucracy of its setting up would seem a kind thing to do.

Increasing government income and decreasing expenditure

In an ideal world, the one where lions lie with lambs and all dog owners clean up the mess their pets make on the pavement, even in a crisis we would protect spending on the poor, the sick and children. The crisis response would be funded by removing palpably bad spending, such as abolishing sinecures like the State Services Commission, or ending subsidies to multinational corporations that use so much electricity to smelt aluminium they inflate the power costs of household consumers. Our next priority would be to consider cutting nice-to-have budgets, such as the culture and heritage spend. Only if this was insufficient would we decrease other spending or increase taxes.

It is difficult to imagine the Covid-19 crisis being a better opportunity than the GFC for us to see this ideal world. Kindness will probably go the way of austerity as a means to change the power of vested interest over government spending. With the honourable exception of the 1984-90 Labour government, governments that wish to cover new costs tend to increase taxes, have across the board sub-inflation increases in spending, or cut transfer payments.

The suggestions below are a compromise. They avoid the core welfare system but are biased to putting the cost on those with greater resources. The point of the suggestions is to provide a sense of the scale of initiative needed if politicians, of whatever political beliefs, are to replicate the stable financial base to deal with future crises created by their predecessors.

To start, the table below uses an adapted version of the Treasury Fiscal Strategy Model to assess the impact on the current government debt of previous approaches applied consistently. All assume that repayments do not start until 2023/24:

| Direct debt repayment (% GDP per year) |

Year debt <10% GDP | Year debt is zero | |

| Balanced budgets alone | 0 | Indefinite | Indefinite |

| Clark / Cullen approach | 1% | 2040 | 2045 |

| Historical average | 1.5% | 2037 | 2041 |

| Richardson approach | 2.5% | 2033 | 2036 |

Source: Treasury Fiscal Strategy Model adapted by the author

Note that these estimates do not include the incentive impacts on economic behaviour so should be treated as underestimates.

To make this more concrete, an initial assessment was made of the impact of the follow policies and compared to the goals of three approaches requiring additional policies:

-

Capital Gains Tax proposed by the Tax Working Group chaired by Michael Cullen (page 67 of the final report). The group assumed a ten year year implementation period and more prosperous economy than is likely while we recover from Covid-19.

-

Income Tax rises are targeted at middle and upper incomes ( those currently paying 30% tax over $48 000 and 33% over $70 000, respectively), with an equal percentage increase in both bands. (Treasury tax reckoner, % of GDP in 2019/20)

-

Goods and Services Tax uniform increase (Treasury reckoner as previous).

-

Increasing the age of eligibility New Zealand Superannuation from 65 to 67 modelled by Treasury for the 2013 Long Term Fiscal statement, averaging 2% of GDP annual saving when implemented.

-

Convert student loans into a grant targeted at those from low income households and the remainder used to pay the government debt. (Figures adapted from 2020 BEFU)

| Increase government income | Decrease government spending | ||||

| Capital Gains Tax | Income tax | Goods and Service Tax | Convert student loans to targeted grants |

Increase eligibility age for NZS |

|

| Clark / Cullen approach | Requires other policy for 8 years. After 8 years would cover the cost. | 36% tax on incomes over $48 000 and 39% tax on incomes over $70 000 | 2% rise in GST | Average of 50% of loaned value converted to grants and 50% for debt repayment | Phase in increased eligibility age to 67 over 10 years would cover the cost. |

| Historical average | Requires other policy. After 10 years a CGT would cover four fifths of the cost | 38% tax on incomes over $48 000 and 41% tax on incomes over $70 000 | 2.5% rise in GST | Average of 30% of loaned value converted to grants and 70% for debt repayment | Increase in eligibility age to 67 would need to be phased over 5 to 10 years to cover the cost. |

| Richardson approach | Requires other policy. After 10 years would cover a half of the cost. | 44% tax on incomes over $48 000 and 47% tax on incomes over $70 000 | 4% rise in GST | All the loaned value used for debt repayment | Unphased increase in eligibility age to 70 would cover the cost. |

Who will be asked to pay for the Covid-19 response?

There is little that is kind about repaying debt. It is what has to be done for kindness to be more than a gesture.

The approach to repaying the debt will involve many seemingly small and technical decisions so the analysis above provides a benchmark for testing the seriousness of decision makers. The particulars will be different, but the scale of any strategy needs to be similar to the ones outlined above.

If nothing is done it means whoever is in New Zealand when the next crisis strikes will be dealing with the consequences of Covid-19 and the new crisis.

That does not sound particularly kind.

Dr Tony Burton was formerly Treasury Deputy Chief Economist and is now is an independent economist and writer. He can be contacted through: www.linkedin.com/in/Tony-

211 Comments

The beneficiaries of our society and economic structure, the landholders and the capitalists should bear the societal burden. Land value tax; and capital gains tax at the same rate as income tax.

Look at the way various factors have combined over the years to inflate land values in Auckland. Giving Governments a vested interest in them continuing to inflate won't do much for housing affordability.

Ocelot

Here we go again . . . . . "Everyone else but me".

However, as I have often posted, I do agree with you that a capital gains tax is required.

As long as the CGT has zero exceptions or loopholes, I wholeheartedly agree!

Yes - just having the govt print money is not enough ; they need to be able to tax the resulting inflation as well . I am sure that will solve all the problems , once and for all .

"Everyone else but me".

It's actually trying to move past that status quo.

I side with Milton Friedman on this one. Drop income tax a bit, increase a bit of land tax to balance. At least it is one tax that cannot be avoided, and it reflects the betterment land receives from society around it.

You pay your rates? Last time I checked Council rates were a land value tax assessed on land values. Pretty pricey stuff that apparently has been mismanaged by Councils, considering now they are broke.

The few of us who are still contributing to the state coffers may just opt out. You can't rob us forever with your delusional society building. Someone's got to foot the bill, and it'll never be you.

That's really the message here. Land value taxes have already been in place, as well as money supply growth being basically 1:1 with nominal GDP growth, and closely correlated to property price inflation.

The Government has allowed / become dependent on increased money supply growth, and funded welfare with the proceeds from tax revenue (which increases as nominal money increases).

The issue here is that it has been the private sector that holds the debt and pays the bill, i.e business and property owners, that the Government uses to fund its programs.

It has allowed (via loose regulations), private sector debt to expand to very large levels, in order to fund a large welfare state. Now that a crisis has occurred, Government & local body revenues have collapsed, as the private sector is struggling to support the dependent Government.

For anyone who says they want a land value tax. It's already there, and its been mismanaged beyond belief, and used to buy votes, which is an enormous failure of Government at the highest and most pervasive level, enough that it will undermine the trust in the currency (relative to today's levels). The reason there has been no capital gains tax, is with one, property prices & money supply growth, never would have risen at a high enough rate to fund Government revenue. I suspect that is what Ardern found when she investigated it, a nice bureaucratic note on her desk explaining the subsequent falls in growth of tax revenue, and fiscal austerity that would be imposed should a capital gains tax be in place.

When you engage in welfare spending, instead of growing the productive economy, you force a dependency on more debt. In the short term, there is a large, (dependent on welfare spending) voter base, that the Government chooses, due to it's bureaucratic structure and size (this includes both National and Labour, but each party dresses things differently).

If you spend on welfare without drawing from a productive sector to fund it, you need to bring more purchasing power forward from the future (credit), house prices are simply a symptom of those increases in credit. It's been a system that works for the Government as a single entity overall, as there has been a lack of significant crisis to destabilize real economic activity. The result has seen Government and private sector debt explode, and house prices explode upwards as a symptom.

Now that one is here, there isn't a large enough productive base, due to failure over 30 years of Government policy, to support or draw down on savings in times of crisis. The result is collapsed revenue for all, and possibly a banking crisis; as saddled with debt for 30 years, the middle and upper class will find the real bill of that debt too high, thus the banks take the hit, then the deposit base, or the Government if if finds it cannot bear a bank failure.

There will be new laws written once the effects of this 30 year policy failure, and end cycle/crisis are truly seen. The Government will find that welfare spending, and productivity failures, are absolutely extraordinarily expensive in the end. I cannot emphasize enough how much of a drop in purchasing power there will be in order to pay it all off.

Drop in purchasing power... your last comment is powerful, are you indicating hyper inflation?

I don't think it would become that bad, but I think the inflation rate will be high, and it is largely dependent on global deflation too. At a guess purchasing power would need to be around a third of what it is today.

Some real food for thought. How would you position yourself with that expectation?

Have to find a hedge for CPI

We traded our jobs for debt that's what free trade was about. China got the jobs we got the debt.

I don't disagree with you there. A lot of the issues are just global factors that nobody can do much at all about.

There are perverse incentives.

For example, when Govt. policy allowed land banking monopolies and council consenting and infrastructure monologues to happen, this increased the price of the sections by tens of thousands (even a hundred thousand plus) of dollars without adding any extra value.

As new land housing costs, especially on the city fringe set the price of all homes, including existing houses going back into the centre. The increase in fringe section prices automatically gives a free windfall gain up to the same amount for any existing property. They receive this money for doing nothing.

BUT rather than calling to tax these windfall gains, what we should be doing is putting in law changes that stop them from being created in the first place.

CV19 might just reduce prices enough so this distortion of non value-added pricing is removed. This would be the perfect time to enact legislation to remove rentier monopoly incentives.

This would mean all that money that was going to pay for overinflated housing costs, in a boom going forward, which is mainly the debt you carry in your mortgage and interest costs, is now free to be used in other more productive ways, ranging from retirement savings, education and health costs, AND yes some of it to pay more tax, or fairer user charges to help pay back the cost of covid.

Between 1984 and 1991, New Zealand spent more on financing government debt, basically bonds the relatively wealthy use to improve their savings and pensions portfolios, than it was spending on either health or education. Debt can be useful, but lenders are rarely kind..

Hmmmm... obliging the bond owning, minority rentier class. We certainly know how QE improves the immediate value of these assets while undeniably raising the present value costs of the tax paying underwriters' future liabilities, who as it happens are the majority and generally asset deficient.

Wealth effect or wealth illusion? The other therapeutic effect of lower-for-longer interest rates is the wealth effect. By driving up the value of future cash flows with lower rates of interest, all manner of assets – stock, bonds, and houses – increase in value and, thereby, can stimulate our marginal propensity to consume. More simply put, the imperative was to make rich people richer so as to encourage their consumption. It is not so hard to imagine negative side effects.

There are the obvious distributional effects between those who have assets and those who do not. Returning house prices in California to their 2005 levels may be good for those who own them, but what of those who don’t?

There are also harder-to-observe distributional consequences that flow from the impact of lower-for-longer interest rates on the value of our liabilities. This is most easily observed in pension funds.

Consider two pension funds, one with a positive funding ratio and one with a negative funding ratio. When we create a wealth effect on the asset side of their balance sheets we also drive up the value of their liabilities. Lower long-term interest rates increase the value of all future cash flows – both positive and negative. Other things being equal, each pension fund will end up approximately where they started, only more so.

The same is true for households but is much more ominous, given the inequality of wealth with which we began the experiment. Consider two households: one with savings and one without savings. Consider also not just their legally-defined liabilities, like mortgages and auto-loans, but also their future consumption expenditures, their liability to feed and clothe themselves in the future.

When the Fed engineered its experiment to promote the wealth effect, the family with savings experienced an increase in the present value of their assets and also an increase in the present value of their liabilities. Because our financial assets are traded in markets and because we receive mutual fund and retirement account statements, we promptly saw the change in the value of our assets. We are much slower to appreciate the change in the present value of our liabilities, particularly the value of our future consumption expenditures.

But just because we don’t trade our future consumption expenditures on the stock exchange does not mean that the conventions of finance do not apply. The family with savings likely ends up where they started, once we consider the necessity of revaluing their liabilities. They may more readily perceive a wealth effect but, ultimately, there is only a wealth illusion.

But what happened to the family without savings? There were no assets to go up in the value, so there is no wealth effect – real or perceived. But the value of their future consumption expenditures did go up in value. The present value of their current and expected standard of living went up but without a corresponding and

offsetting increase in assets, because they don’t have any. There was no wealth effect, not even a wealth illusion, just a cruel hoax. Link-pdf

I thought Venice did something similar forcing the citizens to buy their bonds when they were a city state. It could work to a point.

There is no subtler, no surer means of overturning the existing basis of society than to debauch the currency. The process engages all the hidden forces of economic law on the side of destruction and does it in a manner which not one man in a million is able to diagnose.

"Lenin is said to have declared that the best way to destroy the capitalist system was to debauch the currency. By a continuing process of inflation, governments can confiscate, secretly and unobserved, an important part of the wealth of their citizens. By this method they not only confiscate, but they confiscate arbitrarily; and, while the process impoverishes many, it actually enriches some. The sight of this arbitrary rearrangement of riches strikes not only at security but [also] at confidence in the equity of the existing distribution of wealth.

Those to whom the system brings windfalls, beyond their deserts and even beyond their expectations or desires, become "profiteers," who are the object of the hatred of the bourgeoisie, whom the inflationism has impoverished, not less than of the proletariat. As the inflation proceeds and the real value of the currency fluctuate wildly from month to month, all permanent relations between debtors and creditors, which form the ultimate foundation of capitalism, become so utterly disordered as to be almost meaningless; and the process of wealth-getting degenerates into a gamble and a lottery."

If you feel that the wealthy are accumulating too much of the money that the government creates through its spending then the fairest way to remedy that is through taxation. Having the government reduce its spending and thereby inflicting austerity on the poor and increasing inequality as is mostly done around the world at present is not a just way to solve the problem.

Whilst the repayment of debt is admirable, we shouldn't be in a position that this is required.

We were too slow to move and went too far in our lockdown. If we had implemented a quarantine in mid-February, we wouldn't be in the hole for >40b government spending. But we are where are, so time to solve the problem.

This debt repayment approach isn't addressing our actual problem. We need to grow our GDP per captia, not take a larger part of it in tax revenue. I just don't understand how this is such a complex thing to understand.

There are very real consequences if you tax incomes, 10 - 20% more, even in this base scenario (27% to 36% @ 48k+ PA). There is a reason New Zealand has the second highest citizen diaspora globally at 16% (behind Ireland). We will force our talented people away from New Zealand to create a better future for themselves.

We must change our economic thinking. We need to either be the best place in the world to create a business or operate business in. We are already doing well in aspects of this. We must go further to grow our tax revenue pool, not just tax the existing base more.

A key part of this is keeping our best talent and attracting the best talent in the World. Those income tax rates wont do it when peoples OTE is very low versus the rest of the World, particularly once FX is factored in.

Attract talent, create value added business and attract further business investment. Grow the pie, dont cut it into more pieces.

"We need to grow our GDP per capita"

Sounds about right. And the best way to do that?

Keep the 'capita' bit constant - use the people we already have here, first and foremost, and import only those crucial to the development of the country.

It's time for us to press Pause on the General Immigration button for a while until we have the 'GDP per..." bit adjusted.

The alternative; and most favoured historical answer to repaying Debt is mass immigration - more taxpayers to pay off the debt at the current PAYE brackets.

That may work on a nominal basis, but the necessary " GDP per capita" you write of - will become just another forgotten, good idea.

I agree wholeheartedly, but keeping the capita broadly stagnant is only one element. We need to shift mix of immigration, while greatly reducing overall levels. We shift that mix through incentive, hard to incentivise high capability with low wages and rapidly increasing cost of living.

We have great reference points to view in close allies, Singapore and Ireland. There is no reason whatsoever we can steal with pride from their models. Lower tax environments for individuals and businesses alike. Progressively move income tax rates lower, while target being tax neutral with CGT, the numbers can be adapted to meet that neutral tax amount.

We then need to build a business environment that is highly desirable. Look at business tax relief for startup business (no tax first five years as an example) and investment into small, medium and large capitalisation businesses that are willing to commit to either a global or regional hub in New Zealand. This could be funded via PPP model or NZ Super Fund (think Boeing in USA or Renault in France).

The above seems like a lot of work for very little net gain in tax revenue at face value. But what it does do is significantly shift the health of our overall tax system. It provides more incentive for high capability individuals in all tax thresholds to stay in New Zealand. We can then grow the demand side for this talent to grow existing business or create new businesses through a Government investment vehicle.

This model of course isn't perfect. It is infinitely more progressive than where we stand of more bodies in the door. It is also a future New Zealand I'd want to live in, where people can create better futures for themselves. One can dream.

Boeing has just laid off 12000 workers, Renault 15000.

Do we really need foreign capital, is this not the same kind of juice as immigration? Selling out for a quick buck on the promise of some imaginary expertise that we supposedly don't have..

No we don't need foreign capital, but it would be good to have more foreign business establish big businesses here. We have low to zero corruption in a relatively strong OECD economy, if we get the operating environment for business right we could entice a number of 'anchor tenants'. More of the recently announced Microsoft Datacentre investment.

It would be great to see Callaghan Innovation create a strong business incubator setup, using New Zealand capital. Investing 100M NZD in globally scalable businesses would drive strong outcomes for us. It isn't like we aren't dabbling in this either, Callaghan Innovation is currently funding significant R&D investments, it just needs to go further to grow businesses faster in a sustainable way.

Your point that Kiwis go overseas due to taxation doesn’t stack up. Otherwise, why are there so many Kiwis in Australia or the UK? Could it be the lack of job opportunities and the low-wages?

Did you read my original comment when I mentioned "OTE (opportunity to earn) is very low, particularly when FX is factored in"? You are making my point for me.

We can't reasonably compete on opportunity to earn, so we have to compete on net income. This is where we can overcome those markets due their 48.5% and 45% top tax rates respectively. If we get to a top tax bracket of 25%, plus our purported high living standards we can establish a pretty amazing economic environment for the best talent and business globally.

I think you'll find that some ridiculously small percentage of kiwis bear the brunt of net taxation. The gross rate is meaningless in isolation of Working for families, Independent earner tax credit, in work tax credit, best start child payment, etc.

Can't remember the numbers exactly but its something like 50% of the country pays no net tax at all, and the top 10-20% pay the majority

I suspect you are remembering these Treasury figures quoted by Bill English in 2014:

"The Treasury estimates that this year households earning over $150,000 a year – the top 15 per cent of households by income – will pay 49 per cent of income tax."

"But when benefit payments, Working for Families, paid parental leave and accommodation support are taken into account, these 15 per cent of households are expected to pay 74 per cent of the net income tax."

"And that is before New Zealand Superannuation payments are counted."

"It also excludes the impact of other aspects of the tax changes in 2010, including tightening property tax rules and compliance, and increasing GST.

By contrast, households earning under $60,000 a year – which is just under half of all households – are expected to pay 9 per cent of income tax."

Yes that is most likely it.

Incredible how dependent the entire country is on a productive few

And how hated working people have become.

Don't want to wade into the emotional debate. The numbers are interesting though.

I.m not productive, but I am a net taxpayer.

That's disarmingly honest of you.

Horrific, really.

Meanwhile, $150k per annum is not that significant a salary vs. house prices and house price rises...and National as property investors thought nothing of central sponsorship of that tax-free income to property investors while leaving those $150k productive households to pick up the bill. How appropriate that English's first name is Bill, as that is truly the "sign of our success" his legacy has left upon the country.

Mlennial,

"we need to grow our GDP per capita". Well yes, but the problem has been around for decades, so you need to explain in some detail just what needs to be done to solve it. You state that we force our talented people away(because of high taxation), but what actual evidence do you have to back that up? I suspect that the answer is none.

How about a reference article from interest.co.nz as the first link from Google? https://www.interest.co.nz/news/98882/expat-community-over-one-million-…

Never did I mention that income tax was the sole reason. I even mentioned OTE in the original comment. Something isn't working when 20% of New Zealand citizens live overseas at any one time.

NZ didn't implement a quarantine untl we were already mid way through level 4 lockdown, when it caould have, and should have been done lot sooner. But what other countries did it quicker than NZ? IT is more a case that there weren't coordinated global systems in place to deal with this sort of traveling bio hazzard

If the NZ governement hadn't cut healthcare costs over the years, and our contact traceing systems were gold standard originally, we also may not have had to go into a level 4 lockdown, as per what one of NZ top Epidemiologists said,. Australia didn't have the same strict lockdown, but then again Australia still have community transmission occurring, and are today still under a more locked down country than NZ. Also Oz have far from eliminated it , and they expect cases to continue over there until a vaccine comes along, which may never happen. So much for a travel bubble with them.. NZ is one of only a few countries that may actually eliminate the virus, and will should be able to have travel bubbles with pacific islands that are virus free. The last thing NZ wants to do is risk the pacific islands countries getting the virus, which is a risk if we open a travel bubble with any country that hasn't eliminated the virus. .

Having one of the best responses in the world isn’t enough for some people!

In hindsight we could have shut down our border and a big chunk of our economy (tourism) sooner and put ourself into recession just because the Italians got it bad, but likewise we could have also done that with SARS, MERs, Ebola, etc too and in hindsight those would have been wrong.

"Having one of the best responses in the world isn’t enough for some people!"

That might be because now that the costs of the response are hitting home it is undermining the claim that it was the best we could do.

Very well said

You seem to forget that exporters of logs and meat and others were shut down prior to any lockdown. I dont believe, no matter how it was handled, there was any chance of a differing economic outcome, covid was a catalyst that sped up the balls that were already on play.

When people's livelihood is concerned I think scale matters. There was going to be some kind of impact for sure.

Who pays for Covid 19 Kindness.....Who cares in Election Year !

Need Votes by hook or by crook.

I am surprised NZ has not erupted like the USA. It probably will one day. The youth should really wake up and see how they are being walked all over and being kept down by greedy landlords, usually boomers. NZ needs a reset.

Kiwis, unfortunately, are too polite and wouldn't want to upset their masters.

FB, it is attitudes like yours that is the reason there is the chaos in America!

Your thoughts should be kept to yourself as you sound like an ungrateful person and should feel privileged to live in NZ.

Landlords are not greedy at all and are hardworking genuine people who are providing accommodation to people that need it and that the government is not able to supply.

The crap state houses that are provided is a disgrace but then a lot of the the tenants we wouldn’t being accommodating in property!

NZ does need a reset. It is called get rid of the socialism that is going to be the root of much trouble going forward.

People should be responsible for themselves more rather than relying on everyone else to support them!

So you're a landlord purely to help others have a good roof over their head? You're so kind to give those struggling people a home without making any profit or capital gain. A true hero

Dumbandbroke, yes thank you for appreciating us for providing accommodation to people.

Yes we run it as a business, however our tenants seem to appreciate what we do for them by putting a roof over their heads!

Yes we make a profit, would you be far happier if we made a big loss?

If it makes you feel better, then I will say that we make a huge loss each and every week!

It'd make my generation happier if we didn't have to compete with speculators to buy a home. Maybe try and invest in something that isn't parasitic and productive for the country?

The economic illiteracy in this thread has come to a head with this comment. You get rid of landlords, you get rid of housing investment. Your desired world is one in which few houses get built, and to a low standard. Look to Europe for the results of what you want: everyone crammed into a tiny apartment which they don't own, but is instead owned by some housing collective which never improves the property without state coercion.

If you want a scapegoat, look to the Reserve Bank, not the people who provide you housing.

Yes it has.

But remember that the illiteracy is based on 'economics'.

Everyone could own a house, sans landlordery. They are merely parasites on tenant income (and I am neither, btw). The house would exist without the landlord, but he would have to tap into the resource/energy stream some other way.

No you don't get rid of housing investment actually. People will invest in their own house because it provides a fundamental need that all humans require. NZ housing standards are poor so property investment hasn't improved rentals either. I don't mind people investing in property as it has been profitable. What I absolutely loath is the ones who bleat on about how much good they're doing for the tenants and how they should be grateful they have priced them out of the market.

All generations have had to compete with speculators.

The internet changed the game significantly. OS investors, buying up all over the country.it didnt used to have the worldwide visibility.

Yes, that's a fair point.

Speculators will be active in any market that they perceive to be rising. In the commodities market they provide the important function of liquidity. Interest rates are a main component of housing values, so when interest rates fell after the GFC it became obvious that housing values would rise - enter speculators. If all first home buyers and tenants refused to meet the associated higher costs those costs would have to fall but unfortunately most don't, and the market takes no notice of the minority who do.

Other generations have fortunately had government invested in making housing affordable, not unaffordable while celebrating it as "a good problem to have". Big part of why NZ reached such highs of home ownership in the past.

He is actually an agent with a tiny bit of slumlording on the side.

Fritz, which part of I am not a real estate salesperson now don’t you understand?

I am a professional providing quality accommodation to people who require it!

TM2, landlords are not greedy, excuse me as I wipe my cornflakes off the floor after throwing up with, laughter actually. If you aren't greedy, I assume you let all your properties out at well below market rates, in line only with what your tenants can comfortably afford.

Your definition of greed seems to be anybody who is not a charity.

And TM2's definition of chivalry seems to be greed

Reference your last line there TM2 - 'People should be responsible for themselves more rather than relying on everyone else to support them!'

Just remind me that it is the government paying tenants accommodation supplements and tenants paying you rent.

So everyone is supporting you right (tax payers and tenants)? Yet you tell others they should be responsible for themselves instead of others?

Any hypocrisy in your views by chance?

IO, couldn’t tell you how many of our tenants get an accommodation supplement at all!

We thoroughly check out all our tenants prior to accepting any of them, this way we reduce the risk rent loss.

Can confirm that we have only had to go to the Tenancy Tribunal once for rent arrears and of course they didn’t turn up.

Of course we won and the debt collectors are collecting the arrears plus being on their record will affect their chances of getting future rentals, providing landlords do the proper checks!

TM2, truthfully, do you feel a bit superior to your renters?

The obvious answer is, most definitely.

Do I feel superior to my tenants?

Not sure what you mean exactly!

Superior in what way?

If you mean am I better off financially than any of my tenants, then of course I am!

If you mean because I am financially better off so I can pick and choose what I what to do? Then of course I am!

Does not mean that I am superior to any of them, because at the end of the day we all can make choices!

Who do you feel superior too?

Be truthful, do you feel a bit superior to landlords for example?

From a moral and ethical perspective, yes I do in many instances. Especially if an individual or couple who pay minimal taxes (or in the past have been offsetting loses), owns 5, 10, 15 rentals and is receiving welfare payments from struggling NZ'ers in the form of rent. Who then come onto websites like this to gloat about how wealthy they are, while people sleep in cars.

There are exceptions of course, for example a property that has been received as an inheritance that people don't want to let go of and turn into a rental. But if a person/s decide to buy multiple properties and make $$ from landlording, while turning their fellow NZ'ers into serfs and the social and economic ramifications of those decisions, well we can each decide where our moral compass falls on that - but for many I think we've lost our signal and willingness to say where north might be on our moral compasses.

The good lady wife got an ird statement for last tax year and no bull, IRD paid her over 4500 for WFF. I have no idea why. So I made a note to call IRD tomorrow to let them know they have paid in error. Unless they pay WFF for our 4 puppies then maybe she has an extra child even she didnt know about.

Should rename it from WFF to WTF.

"and make $$ from landlording, while turning their fellow NZ'ers into serfs"

I can't really see how 'land lording' any different from any business being paid by anybody for anything (dentistry/meat/petrol/shoes/wood).

what if instead of land/housing, it was water that was the investment dream of kiwis.

So everyone who is financially stable could buy a share of water infrastructure, maintain or it not (to the government enforced standards), sell those litres-per-day to the young or unlucky or dumb who need water but can't get themselves on the water-ownership 'ladder', to pay back our bank loan.

Water doesn't grow on trees, and maintenance is not free, so we would put prices up inch by inch matching incomes. The government might increase the water subsidy $50 a week so we would bump the price up to absorb that. As a ponzi scheme we make it a far fetched dream of the young to own their own water supply some day.

The point is, maybe just maybe it makes a difference that housing is something people need, and the ability to shop around for a fair deal is severely limited as there is not enough of it in desirable places. Government (and RBNZ) policy has quietly fed this culture to the detriment of everyone with 0 housing in their name, to the massive benefit of anyone with >1 housing in their name.

Its not wrong to want to make $$, it is perhaps wrong to not see how much more damage this landlording business can potentially do, compared to building your dentristry/meat cartel.

Yeah, I don't see much of an argument there.

People need meat, you can die from dentistry germs if you do nothing when your tooth breaks.

The answer to a lack of housing is (and has always been) to build more houses. The regulatory mess that makes that impossible (even for the government itself) is the core of the problem here. So I think we agree government policies have fed the mess. But I don't see the point in blaming landlords in particular.

The day you see any government tackle local government reform will be the day someone actually has a real interest in fixing things.

Disagree - you can build houses until your blue in the face, but if landlords and speculators show up to the auction and buy the house out under the FHB's feet because they've got equity and income in their favour, it just makes the ponzi worse (exhibit the last 15 years in NZ).

I dunno. Its unrealistic perhaps but - picture 5 new townhouse/apartment mix developments popping up in wellington and the hutt. 1000 units appear, at yep high prices 400K for a tiny one, 800K for compact luxury.

Tell everyone who is buying that there is no capital gain beyond inflation, based on the current government policies and plans to build a small number like it every year.

Couples and wellington above-median folk will get in no problem at 4% mortgages. Single folk will need to flat, big deal.

If landlords take them all, well... build another 1000. Now we have 1000 empty rentals. Are landlords still going to push FHB aside?

(Please dont attack my numbers, but the idea is worth proposing... more housing should block the ability for landlords to take-it-all.. shouldnt it?)

My concept is that landlords/speculators should be treated like Foreign Buyers and can only turn new builds into rentals (exception being an inherited title).

Agree with the overall take you have.

Through local government reform land prices could be halved. And if I then built one million houses the supply side shock would reset the entire investment class and your current rules would no longer apply.

P.S. Governments created the current price problem, not landlords.

Who votes for the government?

Yep. I may end becoming a landlord one day too. Blaming landlords is pointless. Blame people who want to block change or deny there is a problem I think. As an optimist I believe there has to be a way to gradually bring the problem under control.

Maybe encouraging investors to build rental housing instead of buying family homes and renting them out, might help.

Spot on!

So housing is simply a commodity like anything else?

New Zealand is not a socialist country so I suspect you don’t know what socialism is.

It still amazes me that there are people on this forum who believe 'socialist' is a dirty word. What is so wrong with 'each according to their needs, according to their ability'?

Ok, so that's communism, but close enough.. And collectivism is fairly common here anyway..

Well, we went to war against it quite a bit so it can't be that great - the Malayan Emergency, The Korean War, the Viet Nam war to name a few.

Do you have an example so we can see where it works?

The military.

Not really, it's possible to progress in the military through hard work and study. Sure, they crush individualism and independent thought, I'll give you that as socialist

Maybe he is referring to the method of taxpayer commitment demanded by oligarch type owners of private US defense manufacturing companies. They seem to be price indifferent because of powerful political forces underwriting preferred place sitters on the right committees of power in Washington?

I'm pretty sure that's not what he was referring to. You know how I know that? Because not a single one of the 8bn plus inhabitants of Earth thinks like you.

Such a perspicacious observation.

There's nothing wrong with neuro-diversity, very under-rated.

Kibbutz work well. And yea I've been to a few.

People like to believe that what they have accomplished is through their own hard work and luck had nothing to do with it and therefore they don’t owe anything, i.e., taxes, to the society that gave them the opportunities that made their success possible.

Successful people seem to find that the harder they worked, the luckier they got.

Most people that I know who are very rich either inherited it, got a good investment job through their parents connections or they got lucky as their house price went up exponentially under JK. Very few truly hardworking blue collar workers get rich. The system is set up to keep the elites at the top. The system needs to be reset.

With a few exceptions, all the people I know who did well came from nothing. That might be confronting for you.

Don't tell me.... they were all born at the right time to buy a house for peanuts, then they got a loan off the bank for a rental, both houses went up 500% so they got another couple rentals with the equity and became big-time landlords. Not really the same as working hard sorry, but you just go ahead and and believe you are a genius. It sounds better than accepting the fact you was just born early enough.

No, they took risk and didn't feel sorry for themselves.

I really can't work you out. You tell everyone who will listen not to buy property, but then complain relentlessly that it keeps going up.

Te Kooti, the risk that they took is still there.

As long as those leveraged landlords have not taken their chips off the table, and converted them into a safer foreign currency, the power of leverage will now start hitting them in reverse.

Correct, so if they end up doing well let's pat them on the back and not be resentful. It wasn't a one-way bet.

I believe that everyone should get a chance at owning their own home at an affordable price. Investment properties should be banned immediately. Let investors invest in businesses instead. Lets see how genius they really are.

If property investors are "businesses" then make them take out business loans at 8 - 10% +

I've been saying this for years - they're only businesses when it suits them and when it doesn't, they're not.

Your displaying your total lack of awareness about banking and pricing for risk. A business will pay 8%-10% unsecured however if they put up a property as security they will be paying not much above mortgage rates.

Yes depends whether you've been indoctrinated or not I guess eh. History suggests that there is no risk for residential housing (yeah right!)

We know there is risk because mortgage rates are some way above the risk free rate.

Shouldn't mortgages rates be rising signifincatly right now to reflect the higher risk of default by customers? e.g. pay cuts, unemployment etc. A higher risk premium for residential and commercial property lending.

Just because the risk free rate is falling, doesn't mean that the actual risk isn't rising. Probably the most risk on the mortgage market now of mass debt defaults - perhaps more so than ever, yet rates are falling. Makes sense...until it doesn't. Its a rigged game and the theory of risk right now is bull shit.

Each mortgage is assessed on it's individual merits. Let's just assume they know more about what they're doing than you and I.

Ok, having lived through the mortgage crisis in the US, you can do that if you want. I'll keep my views.

It's a bullshit set up. I have over 1m in physical saleable stock sitting on my shelves in my business - that's at cost, so converted to trade let's say its 1.5m. I have no debt against it. Guess what interest rate I can get on a loan secured against that ???? 8.5%. Its not like I have no equity, we have stellar financials.

The whole system is geared to property, it is a huge problem in my opinion.

The govt sponsored loan came through at 2.5%, I used this so I dont have to use the other facility through the winter. Thank god for covid.

The US government had the exact same policy. Better still, they put their money where their mouth was and funded the scheme through Fannie Mae and Freddie Mac.

It created an enormous housing bubble and economic crash we called the GFC.

On the other hand, NZ's history of government involvement played a big part in helping achieve a high rate of home ownership, such that none who are now enriched through the reversal can with any self-awareness claim to have done it all "on their own two feet".

FB, it is clear that you do have little experience with wealth generation, or the people that have generated wealth. Yes, some do inherit wealth. The usual rule is that it takes three generations to erase wealth. One generation earns it, the next generation inherits it, and attempts to keep it, and the following generation eliminates the wealth via spending.

The primary path to wealth is simply to spend beneath ones means. This is most important when one is young, small savings made when one is young ends up being large when one is old due to the magic of compound interest. Until three years ago, I had never bought a television. Three decades ago, I did have a hand-me-down TV (that had actual vacuum tubes) that I used for almost two decades. I bought one new car per decade, and drove each one around 400k km before replacing.

What needs to be reset is the work and saving ethic. Work so that your effort provides a benefit to your employer. Spend less than you earn so that you have something set aside so as to make it through challenging times, or better for your retirement.

The system is set up to make spendthrifts beholden to lenders for their life time. Save for the future, don't spend for the present.

That you think that some got very rich via their house price increasing is somewhat amusing. For the last few decades, housing has been a rather peestrian investment return as compared to investing in other areas such as the share market. As for housing price increases vs government, the median house percentage price increase was higher during the HK government that was prior to JK. Housing price increases are associated with both Labour and National, sadly neither party has done anything material in regards to reducing house prices, despite the usual campaign promises prior to election.

Unsure under which ROCK you have been living Yankiwi, but compound interest is no more.

Decades of deflation ahead + negative interest rates.

As long as the interest rate keeps above the inflation rate, compound interest still applies... even if there is a minus sign on both.

The concept of fiscal prudence still applies, regardless of whether one has corrugated steel or a rock as a roof.

I'm blue collar and have worked hard 7 days a week most weeks for near on 10 years.

Would've been easier to go on benefits though.

Personally I feel all working people should be given the utmost respect.

It's an unpopular view these days it seems.

That is complete rubbish and you know it. Do you think someone who works 16hr days in a ruby mine in Burma gets 'lucky' regularly.

What a ridiculous example, and you know it. We're talking about NZ.

Do you think someone who works 16hr days in a ruby mine in New Zealand gets 'lucky' regularly?

a NZ ruby mine .. lol

We're against mining in all its forms don't you know.

free the ruby's

Chunks of capital are ever so helpful.

Chunks of capital are indeed helpful. Big chunks come from small chunks, and the small chunks come from spending smaller than income.

"Micawber Principle" Google it.

Any honest historian must conclude socialism is a dirty word.

Doesn't seem to prevent them wanting it for themselves coupled with capitalism for others.

dp

What is wrong with "from each according to his ability, to each according to his needs" - is that it creates incentives to conceal one's ability, so as not to have so much taken from one, and to exaggerate one's needs, so as to get given more. Everybody is actively disincentivised from doing their best.

It also totally ignores the reality of the human heart.

It lives in a fantasy world where jealousy, greed, envy and laziness do not exist and in doing so makes itself almost entirely irrelevant to the most important issues of human existence.

Go live in them for a while. You will soon see what is wrong with Socialism.

How many people have been commie-joe then escaped to west and written an “uncensored” piece praising the virtues of the system?

Argentina, Greece, Venezuela are all pretty stark illustrations of the dangers it represents as the number of grasping hands starts to exceed the number of net contributors. In short the demand for a thing (govt largess) will expand without check when the price for it (loss of sufficient votes to lose electoral ascendancy) is zero.

So what would you call the Labour Party currently?

Certainly is not democratic as we have been dictated to over the last few months!

Please spare us the whining MAN - be a MAN

NZ is heavily socialist. Big secret of NZ property is that it goes up due to welfare spending.

Yes, I'm sure we'll see these pseudo-capitalists volunteer up their landlord subsidies and non-means-tested pensions any moment now. Until then, it's a little hard to take them seriously while they live up large off the wealth of preceding and succeeding generations.

Lay off the whiskey.

You speak as if to be 'socialist' is like turning on and off a light in a room, all or nothing.

There are people on these pages who have said they would like to see collective/state ownership of various assets in NZ. Many have said they support central plans for the economy. These are both tenets of socialist economic theory.

NZ has a law that states the police can smash down the front door of your home without any warrant. That's what the Stasi did in East Germany for several decades as an example.

We’ve also been developing our narking abilities as well as movement tracing. The full skill set.

I don't think its a bad thing, in the mild to extreme it is. But when I speak of socialism as a positive, its in reference to a Government that is around a third its current size

One trouble with socialism is it pretends to be able to dictate morality through politics. Which is very dangerous and people tend to die a to as a result.

Another is the consistent historical pattern of bankrupting countries, which is no fun to be a part of. And if they can bankrupt an oil rich nation like Venezuela then they won't have any problems with little NZ.

You know what they say, "socialism is fun until you have to eat your pets"

New Zealanders are paying for it by not being able to afford to leave the island again. Not saying that is a bad thing per se. Just a bit boring imho?

Get used to it, the lockdown is a preview of life as carbon neutral.

Yes, we're living the Green Nude Eel....

And we used to laugh at North Korea.

On the plus side, my kids who are indoctrinated with this stuff at school have seen the future and are no-longer onside with it.

'If you are not a socialist before age 25 you have no heart, if you are still a socialist after age 25 you have no brain.'

A bit out of date, but fairly good nonetheless.

Family in OZ can't visit, but hey no worries. A historic flight from LA to Wellington was able to land and bring in vital medical supplies essential medical personnel stranded Kiwis a few folk from hollywood to make a movie.

Got to work all lockdown with no handouts for me or my employer, and emplyment forecast to remain well over 70%. Phew... thank goodness we gave handouts to over 60% of the population.

By staying at home, Good job, that meant we were able to sneak an extra few thousand in from overseas before the qurantine was activated at the border.

Mass panic due to the wuflu making it to NZ. She'll be right. In NZ you can't catch it

- If you go outside and walk around the neighbourhood, beach, or park 476,329 times a day .

- Congregate at the letterbox and talk about how "none of us" have it so fine to share a bevvy.

- Show a temperature, cough, and have a headache, but it's the weekend.

- Go to the supermarket with 100 other people, as opposed to those dastardly butchers with 2.

- You are the health minister.

Deadliest virus since the Bubonic Plague. Yep, that's the one. 0.32 per 1,000 chance of dying from it if under 65 and no underlying conditions. 0.02 per 1,000 if under 20.

As a net tax payer under 40 with a young family. I am so glad we were able to keep all the elderly and sick safe. In fact I am so glad, me and my kids will pick up the bill. Drinks are on us NZ - you deserve it!

We are all equal, ask SIR Key.... yuck!

What do you mean net taxpayer? Are you getting working for families or some other support?

No WFF here. No ACC, No benefits, No pension, no wage subsidy, no student allowance. No income support of any kind.

We provide the Govt with PAYE on income, RWT on savings and investments, and GST on purchases. We are not rich, we are just smart with our money.

Therefore we are a net taxpayer.

Way to go

No need to donate to WorldVision this year Noncents.

If you feel peoples private income and taxation are everybody else's business why don't you post your own details before asking it of others?

Great article

RE this comment: "It is frankly bizarre the government is still budgeting to contribute to the scheme (NZSF) over the next few years. This feels a little like saving money while not paying off your credit card bills" Why is it bizarre? The Fund has a higher rate of return on investments than the cost of Government borrowing. Financial planners advise people to start paying into their personal super funds as soon as possible and to keep paying into it even if they have a mortgage. With the ever increasing cost of National Super and the reluctance to adjust the scheme to lower future costs to NZ, the NZSF seems like a good investment to me at least.

Financial planners have vested interest. Ask an rea if you should be selling your house and the answer will always be yes so long as they get to list it for you

Thank you for reading the article. I gave credit cards as an example because it is closer to the choice the government is making than having a mortgage. If you stop paying your mortgage, you do not stop paying for accommodation because you need leave somewhere. Even Hotel Mum and Dad eventually ejects non-paying children in work! It means the opportunity costs of not having a mortgage are very different from other debts.

On the other hand credit card debt has generally been built up paying for a good that, for whatever reason, we want or need immediately. In my case, it is usually something more frivolous than than protecting the country from a killer pandemic... Financial advisors invariably suggest that the best way to save money is, first, get out of debt, no matter how right it was to get into debt in the first place. One exception would be student loans while you are not paying interest, but that is exceptional.

I hope that answers your question

Tony

Thanks for dropping by.

So what is government debt? it is actually defined as the money that the government has created through its spending but hasn't taxed back and cancelled. it becomes our savings and our net money supply.

The only other source of money is that which banks create when we borrow from them and they then charge us interest on it. Government money is free of charge for us to use until we return it in taxation, and the government actually pays us interest for holding it.

What about this guy's version (page 21-22 of 45 pdf), referenced by Paul Krugman?

In terms of taxation and spending the US Treasury must settle all transactions in its account at the Federal Reserve (which settles in outside money or bank reserves). In this regard, the Fed is the banker to the US government. But the US Treasury can only settle funds in its reserve account by first procuring funds from the private sector (taxing) in the form of inside money (the US Treasury cannot legally run an overdraft in its Fed account). It is best to think of this process whereby the government can only spend from its account at the Fed if it has already obtained credits via inside money transactions involving taxes or bond sales. This procurement of funds allows the government to then redistribute pre-existing inside money back into the banking system completing the flow of funds that starts with the banking system’s creation of inside money (in the form of loans which create deposits) and ending in a private bank account user being credit with the government’s spending.

Said differently, when the US government taxes Paul, Paul pays with bank deposits or inside money. This inside money provides a credit to the Treasury’s Treasury Tax & Loan account at a commercial bank. The Treasury will settle this payment by having the Fed credit its account in what is called the Treasury General Account (the Treasury’s account at the Fed). This flow of funds from Paul allows the Treasury to then spend a bank deposit into Peter’s account. From start to finish, this process results in inside money in (taxation) and inside money out (government spending).

Paul Krugman was discredited as an economist long ago. Read here what economist Prof Bill Mitchell has to say about him.

http://bilbo.economicoutlook.net/blog/?p=35148

Read the article and critique the content, not the guy who referenced it.

It is rather a long read. I believe that there are errors in his understanding of how government finances operate. He suggests that taxation and borrowing comes first, (tab)s and spending then follows, rather than spending coming first s(tab). I prefer to gain my understanding through the lens of Modern Monetary Theory which I believe gives a truer understanding. Currency must first be created through spending before taxation and borrowing can take place. He doesn't recognise government money creation apart from supplying reserves for the banking system. MMT economist Stephanie Kelton is one of the best at explaining things I think. Listen to her here on YouTube.

https://www.youtube.com/watch?v=WS9nP-BKa3M&t=2s

Nice response, well done.

Currency must first be created through spending before taxation and borrowing can take place.

Does the term "currency" mean notes and coins?

Notes and coins are certainly currency but the government doesn't use them for its own spending and we can't use them to pay our taxes either. They are considered part of the governments debt though.

So what are you referring to when you employ the term "currency" must first be created?

When the government makes a payment the treasury directs the reserve bank to credit the account of the recipient, this is done simply by typing numbers from a computer keyboard into the account, the money never existed before this point, it was created out of thin air just as when a bank loans money and it creates it. The government though creates currency, (NZ Dollars) while banks can only create credit a different hierarchy of money. MMT describes it as vertical money and horizontal money and it has different abilities within the economy, for private savings for instance.

The RBNZ can only create reserves and currency. Reserves are not fungible with the private sector banking credit creation activities associated with citizen bank accounts. Reserves are freely traded between banks, the RBNZ and Treasury to facilitate private bank account transaction settlement.

It seems that you are agreeing with me? All government spending creates bank reserves as the money resides within the banking system until it is taxed away or drained through bond sales.The RBNZ can also create reserves and lend them directly to the banks if they fall short for the operation of their exchange settlement accounts.

I don't agree - banks create credit which the government taps with taxation and bond sales to recycle to beneficiary accounts lodged within the private bank system. The government, RBNZ or Treasury generally are not in the reserve creation business.

Study MMT. Didn't you listen to Stephanie Keltons YouTube lecture. She has just written a book called The Deficit Myth. https://stephaniekelton.com/

Another useful site for information here. http://neweconomicperspectives.org/

Yes, but is the argument correct or not?

There is a time differnetial. Inside money in from Paul pays today pays for inside money out by Paul spent upto 30 years ago. Seems like the money go around can go on forever just because it apparently has.

Thank you for your comment.

Other people know a great deal more about monetary economics than me, but one thing I do know is that the money government uses is most certainly not free of charge. In a democratic society, government is usually meant to be looking after money voters have donated through taxation. I am aware the word donation here may offend some people (!), but my point is that even if you pay tax with alacrity, government is still a cost to you when pay the tax.

Yes, one of the defining roles of a sovereign government is printing money. Adding money has a cost to those who already own assets or have an income, including recipients of benefit payments. Monetary experts like Michael Reddell, who writes the Croaking Cassandra blog, have written extensively on how we might do this. I am not sure he is right but, regardless, that is not what has happened in New Zealand. In New Zealand, the government has borrowed money in way that is similar to taking on a personal debt.

There are real opportunity costs to governments holding debt. In less jargon, the interest on debt goes to people who have enough assets that their money can be lent to the government, usually with a bank or financial intermediary. Therefore money paid in interest is not being used on other activities, like supporting the poor, the ill, etc. Obviously New Zealand government took on the debt to help vulnerable people. But once that money has been used it is not so clear we should be indefinitely paying an income, through interest payments, to people who are not so obviously in need.

I hope that answers your question.

Tony Burton

"In New Zealand, the government has borrowed money"

Correct me if I am wrong, but we've done that borrowing in NZD have we not, so that the potential of an inflationary spiral to wipe down the debt still exists does it not (ignoring the costs of such a spiral)?

Government borrowing is a policy choice and it doesn't actually fund the governments spending, economist Prof Bill Mitchell calls it corporate welfare, he suggests just leaving the money in the banking system and paying zero interest on it.

Taxation doesn't fund the government either it controls the money supply by returning money back to the government to be cancelled, but only when the government runs deficits are net financial assets created to finance our savings. Listen here to a short video by economist Randall Wray explaining how it works.

https://www.youtube.com/watch?v=zxDVRISfsls

I tend to think about it this way - imagine if we implement $60bn of QE and nothing bad happens, does that tell us taxation and fiscal prudence are not necessary? So, in my opinion there just has to be consequences, firstly a weaker NZ$ and following that domestic and imported inflation. I don't see asset prices falling at all.

I would be following inflation break-evens very closely.

If debt is free abolish taxation now!

A rough on the back of an envelope calculation using RBNZ QE purchase yields suggests the NZ 5-year/5-year forward inflation rate is ~0.35%.

...the 5-year/5-year forward inflation rate. This is derived from the difference between the other two, the 5-year TIPS breakeven and the 10-year. It tells us about longer run inflation expectations that are especially relevant and revealing, as I wrote three years ago:

The 5-year/5-year forward inflation rate, a calculation derived from the inflation breakevens of TIPS securities, is one prominent means for demonstrating this monetary stability. By measuring the differences of inflation expectations in a second five-year period above the first, it essentially captures market expectations for whether short- and intermediate-term concerns or trends embedded in breakevens are believed to have an effect on the long run. Prior to late 2008, no matter which direction the PCE Deflator went, the 5-year/5-year forward rate was remarkably stable, indicating that no matter what bond market investors largely believed the Fed had it covered in the short run so as to maintain the same stable long-term economic prospects. Link

I'm pretty sure you are confusing break-evens with real yields. The 10yr US zero-coupon cpi swap is 1.35%, and the curve is positive,

https://ycharts.com/indicators/5year_5year_forward_inflation_expectatio…

But my arithmetic is suspect, possibly a revised NZ calculation might be around 1.04% - off the cuff calculations are always dangerous.

That is a good data source, I haven't seen that before. It looks spot on for the 5y/5y US.

QE is just the opposite operation of selling bonds, bonds reduce bank reserves and QE returns the reserves back to the banks again. As banks never lend out their reserves nothing much happens except interest rates will fall and make bank lending cheaper.

There is an option of indefinite rollover of government bonds till economy improves. One hopes the spend partly provides a return to NZ inc.

In a recent study using the Heritage Foundation’s Economic Freedom Index, New Zealand economist, Bryce Wilkinson, found that in 2018, individuals living in 135 out of 180 countries had a lower tax average than New Zealand. By count of population, that amounted to 94% of the world’s population living in a lower tax environment than we do!

Yes our taxation rates start too early and then don't go high enough. There is too much taxation on wages and not enough on investments and capital. There is too much poverty and inequality in NZ and also high levels of household debt.

I find it interesting that all comments focus on how to repay the debt but non question wether it was right to create the debt in the first place. I think there is a significant number of people who benefit from the government's handouts that don't really need it

A significant number benefit from RE speculation too - maybe we should outlaw anything not actually productive.

Along with outlawing anything our offspring will object to.

And theirs.

And theirs....

I assume you have the same sentiment when it comes to private debt borrowed against housing and government handouts in the form of accommodation supplements and WFF

That would not make any sense.

Private debt is accountable, public debt is loaded up on tax payers to the next generation without almost any accountability. They are completely different things with completely different rules.

Yvil's question was "is it right?". In the context of a property bubble, this question still holds validity.

But given they are totally separate types of debt it still makes little sense that we would expect them to be judged equally.

To state it another way, the 'rightness' depends on the accountability.

I don't think they have any options except to spend at some high level.

Being an idealogical based government their dearth of experience in practical business or economics has led them to spend way more than was required and being so badly organised and rushed I expect enormous amounts to be wasted six ways to Sunday.

Until they realise that business people are not the devil incarnate they will struggle to create the environment required to create really good jobs in the volumes needed.

The money will find its way to best return eventually - if we maintain property rights, freedom of contract, export focus economy

Read the National Policy Statement on indigenous vegetation - this Labour led government does not recognise property rights at all.

Does the government debt matter?

Yes, government debt needs to be enough to achieve public policy aims. What are Tony Burton's public policy aims? Sounds to me like he is stuck in a neoliberal "public debt bad" mindset without understanding that this implies a "private debt good"mindset. Growth in GDP = a growth in money, and the license to create money is only delegated to the RBNZ and registered banks. To get growth, it's either government debt, or household+business debt. And governments have completely different financial capabilities to either of the latter groups.

after the initial capital is spent, the debt limits what they can do