This Top 5 COVID-19 Alert Level 3 special comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

As I write this we in Auckland have been in COVID-19 Alert Level 3 lockdown for a week. Disappointing as it is to be back in Level 3, it feels like most of us are battling on, familiar with the territory as we are from our experiences earlier in the year. Hopefully those of you in Level 2 are enjoying your greater freedoms and we'll be rejoining you soon.

Accurate pic.twitter.com/080v3xV496

— ian bremmer (@ianbremmer) August 13, 2020

1) 'No evidence of a positive impact of QE through the bank lending channel.'

A working paper from the Bank of England (BOE) asks:

How do banks adjust their balance sheets in response to unconventional monetary policies, and what are the implications for the real economy?

The paper's title is; Does quantitative easing boost bank lending to the real economy or cause other bank asset reallocation? The case of the UK. The authors are Simone Giansante, Mahmoud Fatouh and Steven Ongena.

The authors note the Bank of England's Monetary Policy Committee (MPC) didn’t expect "strong transmission" of its asset purchase program (APP) through the bank lending channel. Nonetheless given the Reserve Bank of New Zealand (RBNZ) is now pursuing quantitative easing (QE), the report's findings are of interest here.

We analysed the reaction of the balance sheets of UK banks to the APP of the BOE. The comparison of lending behaviour of treated or QE banks with a control group that is unaffected by the QE treatment helps uncover the mechanisms by which monetary policy operates and its potential real economy implications.

We used a unique confidential dataset of APP that identifies QE treated banks, i.e., those which received reserves injections through APP. The MPC didn’t anticipate strong transmission of APP impact through the bank lending channel. In line with that, our difference-in-differences exercise finds no evidence of a positive impact of QE through the bank lending channel.

Treated banks appear to have reacted to QE reserves injections by reallocating their assets towards those asset categories with low risk weights (government securities), promoting carry trade activity. These results are robust even when controlling for demand-side changes using loan level data and borrower firm fixed effects.

The combination of lower gilts yields, resulting at least partly from QE and risk-based capital requirements might have given capital-constrained banks the incentives to shift their portfolios into high-yielding assets with the low risk weights in an attempt to optimise the use of regulatory capital. Thus, the presence of risk-weighted capital requirements could limit the direct QE impact via the bank lending channel, as they may induce inadequately capitalised banks to substitute away from lending to the real economy.

These requirements may have reinforced the concentration of investment in sovereign debt, contributing to the decline of market values of many EU banks involved in carry trade operations right before the EU sovereign debt crisis (Acharya and Steffen, 2015). As it treats symmetrically, the introduction of a regulatory leverage ratio is likely to reduce banks’ incentives to invest in assets with low-risk weights, such as sovereign bonds.

If the policy objective is to provide an additional boost to the economy through supporting bank lending in a time of stress and uncertainty, it might be valuable consider using alternative credit easing tools. This may include programs such as Funding for Lending Scheme (FLS), Term Funding Scheme (TFS) and Term Funding Scheme with additional incentives for SMEs (TFSME). Other alternatives include guaranteed lending to small businesses, with no access to capital markets, or allow access to central bank balance sheet, maybe through a central bank digital currency.

Our findings also encourage policy makers to pay attention to the type of asset purchased via the QE programs in relation with banks’ exposures (Rodnyansky and Darmouni, 2015). This is key to achieve an effective transmission of QE impact to the real economy via bank lending.

Announcing its large scale asset purchase program, or QE, in March, to be worth up to $30 billion over 12 months, the RBNZ said: "The negative economic implications of the coronavirus outbreak have continued to intensify. The [Monetary Policy] Committee agreed that further monetary stimulus is needed to meet its inflation and employment objectives." Announcing the latest increase in its QE program last week, the RBNZ said it was being increased to up to $100 billion by June 2022 "so as to further lower retail interest rates in order to achieve its [the RBNZ's] remit." (Emphasis mine).

The RBNZ also said: "Monetary policy will continue to provide important economic support in the period ahead. Its effectiveness is evidenced by retail banks’ lower funding costs and lending rates, which are benefiting businesses and households. It remains in the long-term interest of banks to fully pass on the benefits of lower funding costs to their customers." (Emphasis mine).

2) 'Everything is going to be repriced' after 'the greatest demand destruction of our lifetimes.'

We sometimes run articles by John Mauldin of Mauldin Economics. We didn't run this one but it's well worth a read. Mauldin's primarily writing about the US economy. But given it's the world's biggest, what happens there remains of interest and importance to us. And the outlook's not good.

Here's one thing I think we can all agree on…

This recession/depression is unlike anything we have experienced in the history of the US.

I am at a loss to find anything like it in world history. That is because we have never experienced an economic disaster—and that’s the correct phrase—like we are witnessing today.

As this type of article tends to do, he eventually gets onto what economic recovery may look like.

I frankly think it is misleading to draw a graph and say this is what the economic recovery will look like.

Talk about a V- or U-shaped recovery is simply silly. Every one of the “bodies” I mentioned above will have a significant recovery impact. We don’t know how they will interact.

My guess is that we are going to see several different economies. Heather Long (a fellow Camp Kotok regular) illustrates this for The Washington Post.

This dichotomy is evident in many facets of the economy, especially in employment. Jobs are fully back for the highest wage earners, but fewer than half the jobs lost this spring have returned for those making less than $20 an hour, according to a new labor data analysis by John Friedman, an economics professor at Brown University and co-director of Opportunity Insights.

If we have to choose a letter for the economic recovery, maybe it should be a “K.” Some go up and others go down.

He goes onto argue that this crisis is going to change the way we live. I'm sure he's right about this. But I'm not convinced all the changes we're experiencing will be permanent, not clear on which ones will be temporary, and which changes are yet to emerge. Being adaptable and flexible is now more important than ever.

This is going to change the way we live. We have already seen savings increase, not unlike our parents and grandparents during the Great Depression. It is going to change spending and saving habits. It is going to force businesses and entrepreneurs to adjust in ways that they never dreamed they would need to.

I think it is fair to say that many of us have looked at our lives and decided we don’t need quite as much “stuff” as we did before. We are not going to hunker down in caves, but we may pack them with less paraphernalia.

Each one of those choices represents a buying decision that impacts some entrepreneur who provided that product.

This crisis is simply the greatest demand destruction of our lifetimes. It will come back, but it is not going to come back to what it looked like in 2019. Our future economic buying decisions are going to be different.

Everything, I mean everything, is going to be repriced and thought through. You can’t take anything for granted. Inflation numbers and measures are going to be warped for at least a few years. We are using old tools to measure a new economy. We are going to have to develop new models to appropriately analyze the world we now live in.

How do we value the price of a home or apartment? I don’t think it is unreasonable to expect 10% unemployment, or something close to it, in the middle of 2021. That is going to affect prices up and down the housing value chain.

How do you value retail and office space? If your tenants are gone, do you pay the mortgage? Hotels will come back, eventually, but who is going to own them? The old private-equity owners or the new ones? At what price? We already knew we had too many retail stores. What is the correct number in the future? How will malls and commercial space be repurposed?

Hundreds, if not thousands of planes are sitting on the tarmac. Who is going to own them?

There are thousands of scenarios playing out in thousands of industries all over the world. What they have in common is that…

Everything is going to be repriced.

That makes me very uncomfortable.

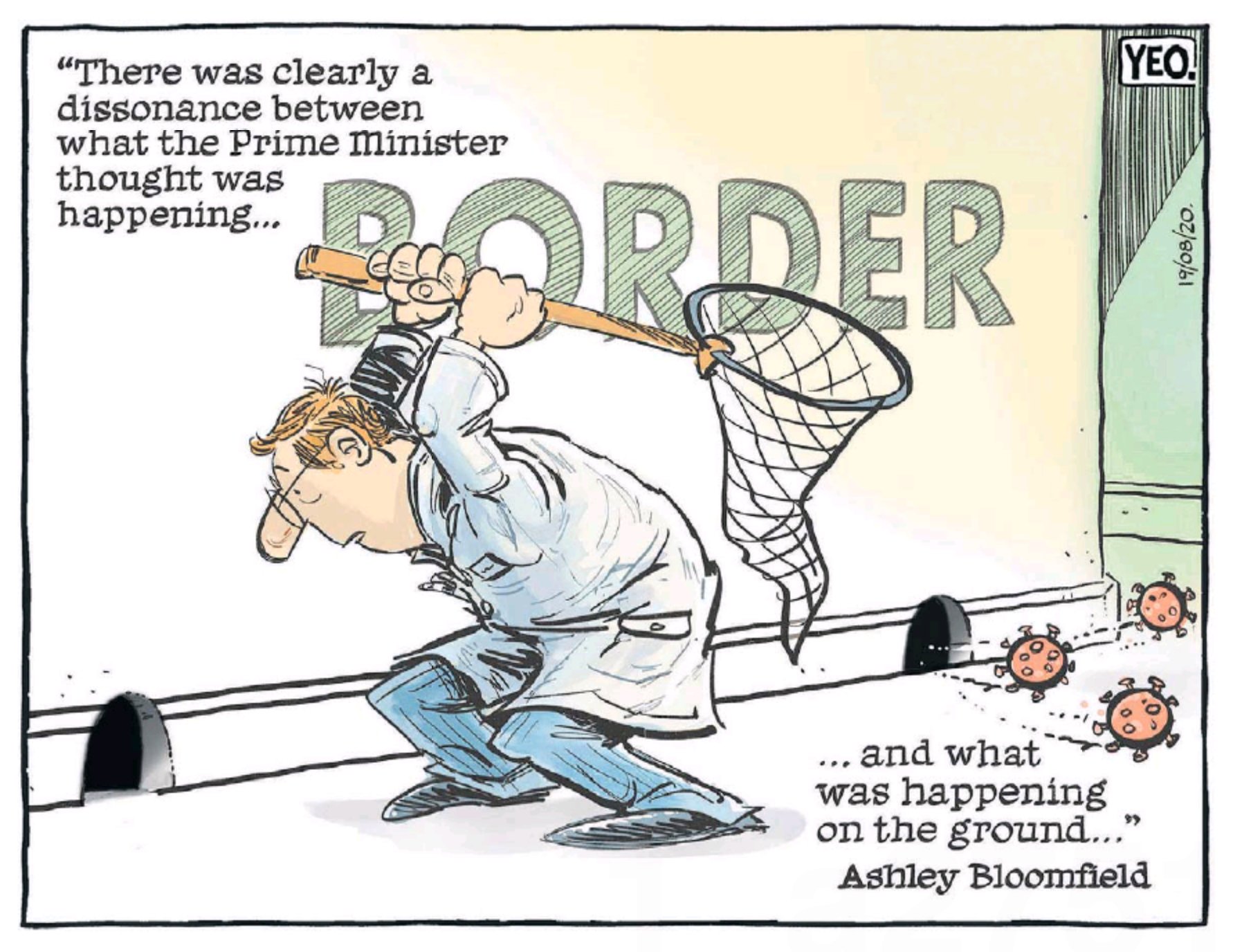

Cartoon: Shaun Yeo, Otago Daily Times.

3) What we’ve stolen from our kids.

Writing in The Atlantic Chavi Eve Karkowsky, a doctor and mother of four school-age kids, delves into the impact on them of not going to school for months on end. I recently spoke to a friend in New Jersey whose kids haven't been to school since March. The breaks here obviously hasn't been as long. But as a parent, I hear where Karkowsky's coming from. If we hadn't moved from Level 3 to Level 2 in May I was ready to ask David C for some time off. I felt my eight year-old needed some attention as lockdown dragged on with his parents busy working from home and striving to home school him and his older brother.

But even for children whose needs are less physical, school is often their entire external world. It is a place where their relationships are not dependent on their parents, where they try and fail and then try and succeed. School is where they make friends and mortal enemies and friends again. School is where my children are not my daughter or son; they are themselves, figuring out who that is every day.

I am not a developmental psychologist; I’m just a mom. But it has always seemed to me that headlong, unstoppable forward development is the normal state of a growing child. In the same way that a shark that is alive must swim, a child who is alive needs to be in a constant state of movement and change. When the forward motion stops, something is very wrong.

With no school, much of that progression, that learning, that schoolyard negotiation—in short, much of a kid’s life outside their house—disappears.

Meanwhile elsewhere in America...

Just heard from a teacher friend prepping for the school year: they've been told they can't leave classroom doors open to promote better air circulation, because that would circumvent the school's automatic locking system that's in place for active shooter situations.

— Gabriel Debenedetti (@gdebenedetti) August 17, 2020

4) The degrowth movement, - is less really more?

Okay, strictly speaking this isn't a COVID-19 related story. But following on from the massive changes we're facing according to John Mauldin, it fits. Bloomberg's Akshat Rathi talks to Jason Hickel, an economic anthropologist at Goldsmiths University of London, about the degrowth movement. Hickel has a book called Less in More: How Degrowth Will Save the World.

Rathi explains what Hickel and other scholars who share his views want.

These scholars first want the world to reconsider the value of gross domestic product as a metric for progress, as GDP may still be rising even as inequality worsens and overall well-being falls. Second, they contend that a sustainable planet must find a way to live within certain limits for things like climate change, ocean acidification, and biodiversity loss, called “planetary boundaries”—and that rich countries are abusing these boundaries by consuming too many resources. And third, they question the wisdom—and even the morality—of most climate models looking to keep temperature increases below 1.5°C, which require the use of negative-emissions technologies that draw down carbon dioxide from the air and are still in early stages of development.

But suggests there are plenty of gaps in the theory.

Some economists have shown that well-being does keep rising along with GDP. Technologists have shown that we are eking out more economic gains from less material use. Others say that the idea of degrowth goes against the deep-seated human desire to have it at least as good as one’s neighbors—an impulse that has geopolitical consequences, as well.

Rathi starts by asking Hickel what people get wrong about degrowth.

When people first encounter the idea, they think this sounds like a recession. In fact, degrowth is the opposite of recession in some key respects. A recession is what happens when a growth-oriented economy stops growing. Everything falls apart. People lose their jobs. It’s a human disaster.

But degrowth is building an economy that does not require growth in the first place, which can deliver high levels of human flourishing without growth. In a recession you see inequality rise, you see joblessness rise. In degrowth, you have a reduction of inequality. You have full employment, which you achieve through a shorter working week and a job guarantee.

A lot of people when they initially encounter the concept of degrowth, they think that sounds bad because we have so much poverty in the world. I have to point out this is just for high income countries that are exceeding planetary boundaries and need to reduce excess material and energy throughput.

5) Reported COVID-19 deaths vs the likely real number.

The Financial Times has a COVID-19 section that's not behind its paywall, with this page particularly useful. Among other things the FT undertakes the grim task of tallying the COVID-19 death toll. The FT says whilst more than 766,000 people are known to have died from the virus globally, the real number is likely much higher.

There are concerns, however, that reported Covid-19 deaths are not capturing the true impact of coronavirus on mortality around the world. The FT has gathered and analysed data on excess mortality — the numbers of deaths over and above the historical average — across the globe, and has found that numbers of deaths in some countries are more than 50 per cent higher than usual. In many countries, these excess deaths exceed reported numbers of Covid-19 deaths by large margins.

The picture is even starker in the hardest-hit cities and regions. In Ecuador’s Guayas province, there have been 10,000 more deaths than normal since the start of March, an increase of more than 300 per cent. London has seen overall deaths more than double, and New York City’s total death numbers since mid-March are more than four times the norm.There are several different ways of comparing excess deaths figures between countries. In absolute numbers, more people than would usually be expected have died in the in the US than in any of the other countries for which recent all-cause mortality data is available.

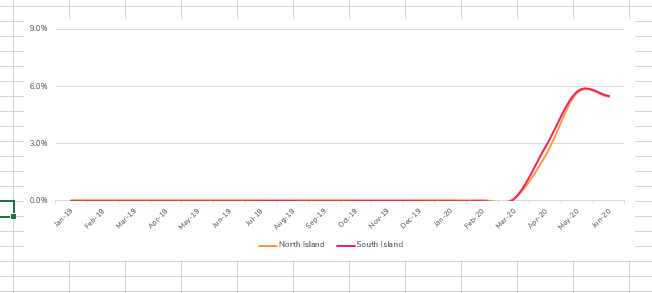

6) Mortgage deferral volumes similar in the North and South islands.

On Wednesday I published a story in which figures from credit bureau Centrix put 11.9% of mortgages in Queenstown and 8.9% of mortgages in Rotorua on deferral. Other cities Centrix highlighted were Whangarei with 8.7% of mortgages registered as being on deferral, Taupo with 8.4%, and Tauranga at 7.6%. In the major centres 3.8% of Wellington mortgages are registered as being on deferral, 6.8% in Auckland, and 6.3% in Christchurch.

Now illion, another credit bureau, has provided me with the chart below. It shows a very similar rate of mortgage deferrals in the South Island as the North Island.

45 Comments

#1 Let me get this straight - the BOE gave some private banks (it is interesting that it was not ALL) wheelbarrows full of money for their reserves as their implementation of QE, in the expectation that it will save the economy, but without specific direction as to how it will be used, and they are surprised there was no positive effect from this????! Actually there would be a positive effect - the shareholders will heave benefited HUGELY! Seriously? where do we get these central bank governors from? Even Orr has admitted here it is more important to prop up the property market, a part of the economy that is not even half of it, at the expense of the rest of the economy. Have we all fallen down the rabbit hole?

Is this intentional? Is it a way to ensure the government is the only buyer when things go pop? The nation state is the only economic player with the ability to enter into a proper jubilee arrangement with another, and what better way to recapitalise the state than by being able to buy critical assets at pennies in the dollar? Have Reserve Banks printed a bunch phoney money in the knowledge that when judgement day comes, there's a plan to let states seize control of the assets lost to MNCs and just forget about the debt that pushed us over the edge?

It's borderline conspiracy stuff, but there's no actual rational explanation for the situation we're in either. Either way, I don't expect it to work out for John Q. Mortgageholder.

#2 - I hope this means fishing boats!

A couple of things. In my own experience, a small loan to develop a freehold property was to incur a 12-14% interest rate due to "the risk". Earlier this year. Banks just laugh at Reserve Bank rates and just fleece their customers as usual.

The Covid deaths have just as much chance of being overstated as understated. From memory one Kiwi Covid death was not even tested, but the patient had the symptoms so it was written in as cause of death. All over the world people with multiple health issues get Covid as their cause of death. My suspicion is that the true number will be never known, and will be argued about for many decades.

That would have been the 96 year old who had dementia, who tested negative, but because they were in a rest home with covid patients, they were counted as a "probable" and recorded as a Covid death.

Re:1)'No evidence of a positive impact of QE through the bank lending channel.'

Treated banks appear to have reacted to QE reserves injections by reallocating their assets towards those asset categories with low risk weights (government securities), promoting carry trade activity. These results are robust even when controlling for demand-side changes using loan level data and borrower firm fixed effects.

The combination of lower gilts yields, resulting at least partly from QE and risk-based capital requirements might have given capital-constrained banks the incentives to shift their portfolios into high-yielding assets with the low risk weights in an attempt to optimise the use of regulatory capital. Thus, the presence of risk-weighted capital requirements could limit the direct QE impact via the bank lending channel, as they may induce inadequately capitalised banks to substitute away from lending to the real economy.

Hardly a revelation for Kiwis.

Prior to QE our building societies masquerading as banks took advantage of the low capital risk weighting assigned to residential property mortgages to direct 60 % of their lending to this asset class for one third of creditworthy households to speculate.

{kind=link}

Now we have the prospect of banks being in receipt of around $100 billion of OCR earning excess settlement cash locked up at the RBNZ until the QE bonds are sold or redeemed.

Furthermore, they may decide to keep a significant proportion of the zero weighted government debt they monetise for the government to build fortress balance sheets against pending deflation.and illiquidity associated with that. Witness the actions of large US banks.

{kind=link}

This article, and in particular the reaction of banks to QE, confirm what you have been saying all along, Audaxes.

Nice piece Gareth and you add some good points.

Many people seem to rubbish the impact of all of this on kids. If you have school age ones then you know the challenges and the disturbance it has created for them. For some it will have lasting effects.

I had a few days of looking after grandchildren during lockdown - trying to get them to participate in home-schooling. The materials provided by the school were amazing, and the remote support (daily Zoom meetings and online class work posting sites) from teachers was great too.

Despite all the adults best efforts however, it was all a bit of a waste of time. What I think happened was that in their family unit of brothers and sisters there is no collective 'peer pressure' - they aren't 'wired' to comply in the company of their siblings. Home is too familiar and they don't worry about 'standing out' in the crowd for non-compliance.

Yes 100% agree. Despite all the good and best efforts, it's nowhere near the same for the kids.

And the more lockdowns we keep having, the more their education will suffer in the longer term. Not to mention extra curricular activities.

+1. The teachers are doing their best but online school is rubbish.

Not all kids had parents or grandparents willing and able to homeschool them. Think of all the kids with parents who didn't care, or couldn't be bothered, who couldn't understand the school work, don't speak English, used older children to babysit the younger ones, don't know how to use a computer, or who didn't want to appear dumb in front of their kids so avoided it ....

Great collection, Gareth, thanks.

#3 Couldn't agree more. The absolute worst thing about COVID management for children is closed schools. It is the primary reason I support the elimination strategy for NZ.

#4 It's where we are headed willingly or not. I find it interesting how few people see de-growth as a positive turn for future generations. I also agree with them about the temperature limiting targets. I still see climate pragmatism as the way forward; "accelerate energy innovation, build resilience to extreme weather, and pursue no regrets pollution reduction measures".

"I find it interesting how few people see de-growth as a positive turn for future generations."

Simply because

1) it collapses Debt (which is the same as collapsing wealth or the value of fiat) and consequently ownership ... if everythings valueless, who owns your house?

2) it collapses the job market (as we are seeing, without massive Govt debt issuance the majority have no job or income)

3) it collapses levels of consumption and standards of living

But its all coming regardless

1) A 'Great Reset' whatever form it takes will have to happen. https://www.weforum.org/press/2020/06/the-great-reset-a-unique-twin-sum…

2) We will always need to build, make, repair and re-purpose things - it's just that less of these things will be 'nice to haves'.

3) You mistake consumption for consumerism - and yes, the latter will become a thing of the past. I suspect standards of living (and health) will improve. Think of a world without junk food, for example.

#1 Kate I'm just a little cynical of a 'great reset' planned and executed by economists and banks. These groups are likely lobbied to death by the rich and powerful, so their 'social contract' is not likely to do what they say they want, or the Governments and law makers will just ignore it anyway. David Mahon said in his article on China; "In crises, the West is often trapped by assumptions derived from laissez-faire capitalist ideology, leaving markets to correct anomalies that government interventions are often better able to repair." Governments are essentially trapped by the capitalist free market model and are too afraid to regulate away from it because they are bombarded by people with too much to lose that it will be too damaging. They don't realise that decent regulation can limit any damage.

Yes, me too. The WEF is really the last place I'd expect any reform to happen, however, we are at that 'the last place' stage. The 'Davos crowd' can no longer fail to address the certainty of collapse unless systemic change is implemented.

No argument there. Just wonder how long the talk will go on?

Venezuela has done 'degrowth' very well. We should be holding the Venezuelans up as prime examples of a successful degrowth story. Another one is Zimbabwe, their degrowth experience has been both profound and long lasting, successfully degrowing for decades now for the enduring happiness of their children.

I think you are confusing degrowth with hyperinflation.

They run concurrently, and satisfy the demands of both the growth to infinity proponents and the degrowthers. Believe me. Hyperinflation is what you're looking for.

Seems to me you are looking at this from yesterday's playbook - orthodox economics which suggests that the principle cause of hyperinflation is excess money supply; i.e.,

..if the increase in money supply is not supported by economic growth as measured by gross domestic product (GDP), the result can lead to hyperinflation. If GDP, which is a measure of the production of goods and services in an economy, isn't growing, businesses raise prices to boost profits and stay afloat. Since consumers have more money, they pay the higher prices, which leads to inflation. As the economy deteriorates further, companies charge more, consumers pay more, and the central bank prints more money—leading to a vicious cycle and hyperinflation.

Surely you have seen enough evidence of late that that isn't happening? GDP (growth measurement), CPI (inflation targeting) and OCR (monetary policy) are all archaic, ineffectual metrics.

What will cause hyperinflation in certain economies in future is loss of confidence (not in the 'economy' or monetary system) but in social cohesion, the rule of law, and equity/fairness in the institutions of governance. We'd be better measuring trust (in institutions) and safety/wellness (of citizenry) if we want to measure function/success of different economies.

Hickel has been on-point for some time.

Degrowth is indeed what we will experience; it's what happens when you have $1,000 in the bank and spend $1, $2, $4, $8, $16, $32, $64, $128, $256 - at which point you have one doubling-time left (in other words, if you were attempting 3% growth you'd have 24 years to 'all gone'. Of course, if your 'growth' relies on the 500 items left - substitute fossil energy for $ in the scenario - you won't maintain it towards the end.....)

But what happens to the collection of forward bets, made on the assumption that we progress through $512, $1,024, $2,048 etc, if the open question. They cannot all be honoured, and the must-be-dishonoured portion must be increasing exponentially in reverse. Do we forgive debt? In if so, what is anything 'worth'? And if we doný forgive debt, same question; what is anything worth?

Which is where Mauldin comes in. But not completely. Hickel's 'high levels of human flourishing without growth' reminds me of the of the addenda to the Brundtland definition of 'Sustainable Growth' that our RMA parroted; “What is needed now is a new era of economic growth - growth that is forceful and at the same time socially and environmentally sustainable”. (p. xii)

(the oxymoron of all time)

#2 spending and saving habits don't seem to be changing in the US. They have lower incomes and are still spending the same amount on credit cards.

Look at 2007/8 and I helped a lot of people in the US unravel their debt problems. Typically 9-12 credit cards with around $100k USD for a balance. Most I helped change habits partially or fully, and there was one that had dug the debt hole too deep to avoid bankruptcy. Give it a year and I have no doubt I'll see the same thing again in the US.

For habits to change the credit card companies and car loans will have to tighten so as to not feed addiction.

Surely the Federal Reserve can just print another week...

The 'basket' used (as a measure to retain ones place in the middle class) in the Cost of Thriving Index (COTI) are:

a three-bedroom house at the 40th percentile of a local market’s prices, a family health-insurance premium, a semester of public

college, and the operation of a vehicle.

And it is health and higher education costs that are most eroding/impacting on that middle class status over time.

https://media4.manhattan-institute.org/sites/default/files/the-cost-of-…

Like the US pieces you shared Gareth, this one has NZ relevance due to similar policies (QE, wage subsidies) and likely similar effects...

"The Rich Got Richer During the Pandemic, Bailed Out by the Fed. How That Happened and Why That’s Bad for the Economy"

https://wolfstreet.com/2020/08/19/the-fed-made-sure-the-rich-got-richer…

if the NZX50 is anything to go by, NZ is enjoying a level of prosperity unparalleled in it's history - only I can't understand why "I" can't see it? Can you see see it?

What is prosperity? I am probably considered wealthy, and I think what I expect to see when I see prosperity is

1) I'm doing OK and more or less optimistic about my stash, but that's not crucial.

2) I look around and see less people struggling, or real opportunities for strugglers to improve their lot

I am pretty confident that prosperity is not evident if the rich are getting richer. (2) is an absolute requirement for prosperity.

So I guess that means that the stock exchange is not really an indicator.

It would be awesome if there was an indicator for (2), found on your financial markets page.

Yes, indeed. Society works well when we all do well. There is no fundamental conflict between capital and labour. Things get out of whack when special interest groups, such as banks and government workers, get more than their fair share. A civilised society is built up from SMEs, not down from over entitled corporations and bureaucracies.

Careful on the Government workers though Roger. Yes there are a lot earning very good money, and many IMO not worth it, but equally there are an awful lot not earning good money, doing difficult thankless jobs, and getting abused for their trouble. Agree with the banks, moneyed individuals at the top of private organisations, and wealthy investors, but most of the rest are struggling to survive.

Yes, indeed, no problem with the government employees who actually do useful things and are good at their jobs. There just seem to be too many of the other sort, who just produce endless reports and hot air and waffle and obfuscation and poor, poor, poor policy and hopeless, dispiriting regulations that sap the lifeblood of the country.

Don't blame the government workers, many of whom work hard. But they (including councils) are stuck in Zombie organisations and their hard work does not produce much at all. Most or much of it is just internally interactive.

But it gets worse, those organisations impede and cripple the productive ones.

Poor people don't play the stock market. Those that do have made out like bandits, working from home on full pay, saving money, investing their growing cash hoard. They are feeling very prosperous.

FYI on COVID-19 testing. This is pretty impressive even given our small population compared to some of the other countries. Lots of hard work being done by our health workers, and great compliance from the NZ public - https://ourworldindata.org/grapher/number-of-covid-19-tests-per-confirmed-case

Here, "per confirmed case" is key. NZ's confirmed cases have always been artificially low, because for months and months we assiduously tested only symptomatic. Thus, far fewer confirmed cases when we're actively not looking for all cases. Even when NZ's first so-called surveillance testing was done (not properly random to qualify scientifically as such, but that's another matter), it was 4 weeks into lockdown. Hurrah, no new cases found and no community transmission hyped. It would have been very different if done in week 1 of that first lockdown, and the real state of community transmission known, and more cases would have been added to our tally. So, even when we did some wider testing, its timing meant case numbers stayed artificially low.

Germany by contrast went all out, months ago doing 1m tests a week, actively searching for and finding asymptomatic cases, thus increasing their 'case' numbers. So they look 'lower' on this stat (unlike NZ which studiously didn't test for asymptomatic), but they wanted to find cases, thus achieving better outcomes for their citizens than UK which didn't ramp up testing till long after, and still did it poorly.

Another issue with this stat (as you imply) is that small countries always rate more highly. This chart months ago had even tinier states way on top, for no other reason than they were tiny.

Ron, I am thinking/commenting mainly on testing volume here since the current community outbreak was discovered which has been impressive. Also there have been some asymptomatic people tested here. I was just talking to my sister-in-law earlier. She is a doctor and has now been tested three times in total, twice whilst asymptomatic.

Yes, much has been made in media of recent 'huge' increase in testing. Indeed, it is good, as you say. But, the (then) claimed 'huge' increase to 1000 tests, woohoo, then (very recently), 10k+ likewise woohoo, misses the bigger picture. The testing level remains derisory. The new minister has ramped it up, but seems still captive to MoH thinking (apparently even now we have only 100k or so testing kits, so couldn't even do fast all-population regional testing even at this late stage in the game).

The current situation demands a different response, but for context if we'd done all-population fast-cycle testing for our wee 'team of 5m' back in March (backed by proper contact tracing), we'd have found all symptomatic and asymptomatic cases, isolated just those (and paid their wage subsidy, not everyone), and might have avoided lockdown (although realistically, probably gone into it and come out early). We would have also created the world's first GPS of how Covid spreads, handed it to every country and vaccine maker as the first all population study of how the virus transmits, and NZ might now be 2nd on the list for just about every vaccine. As here: https://medium.com/illumination/dear-jacinda-ardern-prime-minister-of-n….

The problem isn't testing, but testing based on incremental thinking rather than outcomes science. Thus, we accept what was claimed 'gold standard' without referencing intended outcomes. Then when faults are found, we improve it by ramping up what we've been doing, and doing it better, yet without standing back and asking what do we want to achieve and how can we make it happen. That sometimes requires different thinking, and in this case (in my view at least) multiple complementary, diverse disciplines, not just more of the same uni-science and unidirectional policy.

#4. Degrowth. The way to think of this is like big big organisations that are barely profitable, and the little ones who do very well.

I think we should look at the small approach. eg Tourism. We should be looking at sustainable activity that pays us well, and does not mess up citizens enjoyment of our wonderful country.

Reduce the numbers (with an effect of reducing GDP) and have well paid happy citizens doing the work.

Excess deaths will need to be averaged out over time, not just extrapolated over the few months of the pandemic. Considering the vast majority of deaths are in the elderly, all of whom had co-morbidities and were already on their way out, then arguably all Covid has done is pull forward upcoming deaths into 2020. I would expect that in the absence of Covid that deaths in 2021 and 2022 will be significantly less than normal as a result.

Indeed. Fewer deaths during lockdowns (eg work injuries, car crashes, etc) must be counted, as well as additional deaths caused by lockdowns, some of which may only be known long afterwards (eg from tens of thousands of delayed cancer tests, cardiac, suicides, etc). Ditto, public health impact from economic recession caused by lockdowns etc in response to Covid. And tracking across age groups as you say, with incremental effects very different for elderly, children, 30-something cancer patient diagnosed as stage 4 (terminal) rather than 2, etc.

Bank behaviour is strongly driven by an aversion to credit risk. Unless banks can be persuaded change criteria, like the test rates for loans, it's unlikely that there will be sudden credit growth in a period of economic decline.

Reserve banks would be better served by finding a way to get consumers spending instead of inflating asset bubbles. While many know this their intuitive response has been to reach for rates because they are also risk averse and there is an established historic precedence to using rates.

In short everyone is doing what they're doing because that's the way things have always been done.

Non-recourse mortgages?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.