The demand for credit, or debt, is unlikely to bounceback as strong after Auckland's current lockdown as it did after the first one earlier in the year, the managing director of credit bureau Centrix suggests.

Centrix's Keith McLaughlin said when the nationwide lockdown ended, and the economy was freed up in May, there was a massive bounceback in credit demand.

"We got to about 96%, 97% of pre-COVID credit demand," McLaughlin told interest.co.nz.

"I'm interpreting the numbers that are in front of us at the moment where a material component of the drop is clearly identified as being uncertainty in the market. My suspicion is that we won't see the same recovery this time around. I think the first time around there was a feeling that we'd beaten it, we're okay, back to level 1 life goes on as per normal, close the borders and the New Zealand economy would be fine."

"Certainly it still hit the tourism market, but the rest of the economy got a lot of business. I don't think there's the same level of confidence that that's going to happen this time. So I'm not expecting a similar bounce to what we had with the first lockdown," McLaughlin said.

"I think it has been a wake up call and my read of it is that it'll be a slow recovery. It's going to be compounded by the increasing unemployment as it occurs. So I think this is probably not very good timing and I don't think the bounceback is going to be nearly as complete this time."

In terms of consumer credit, McLaughlin said as soon as Auckland moved into COVID-19 Alert Level 3 last week there was a 25% drop in credit demand in the city. That did not surprise him.

"But what really did surprise me was across the rest of the country there was a 6% drop in credit demand. And yet the [Level 2] restrictions placed on the rest of the country were not that material that it should've affected the ability to obtain credit or buy things on credit. So I think that really comes down more to uncertainty, lack of confidence in the market. People have pulled back from buying things, particularly non-essential items," said McLaughlin.

Centrix, which receives data from all the major banks on a monthly basis, says 11.9% of mortgages in Queenstown and 8.9% of mortgages in Rotorua are registered as being on mortgage deferral. Away from those two tourism hotspots other cities with a significant percentage of mortgages on deferral include Whangarei with 8.7%, Taupo with 8.4%, and Tauranga at 7.6%. In the major centres Wellington's at 3.8%, Auckland 6.8%, and Christchurch 6.3 %.

Surprised by volume of borrowers in arrears not seeking a deferral

McLaughlin said what's surprising Centrix is the number of people going into mortgage arrears who are not seeking a mortgage deferral.

"That has climbed a bit and at the moment shows about 13,500 mortgages that are currently in arrears where there has been no application for a deferral. And that's quite sad because the facility is there, the banks have done what they can to promote it, and we'd encourage consumers to approach their lenders if they are having any difficulties whatsoever to seek a deferral. If they're not doing that then it [their loan] just slips into arrears and that has a long term impact on their credit score. Whereas a deferral has no impact on a credit score," said McLaughlin.

The 13,500 total had probably doubled since the onset of the COVID-19 crisis, McLaughlin said, and is equivalent to about 1% of all mortgages.

McLaughlin said if somebody applies for a mortgage deferral it comes through to Centrix with a specific flag and it does not impact the borrower's credit score.

"We've put that [system] in place and it should be taken advantage of. If it [the loan] just goes into arrears and people don't respond to phone calls, or as sometimes tend to do just ignore it and hope it'll go away, then it does go into arrears and it does become an issue for them further down the track."

The mortgage deferral scheme, put in place at the onset of the COVID crisis in March by banks, the Reserve Bank and the Government, was this week extended by six months to March 31 next year.

'The envy of Australia'

On August 6 illion, another credit bureau, described New Zealand’s economic recovery as the envy of the Australian financial sector, with demand for most types of credit products quickly returning to near normal levels following the easing of lockdown restrictions.

"Since Level 3 restrictions were lifted on 27 April, NZ credit enquiries have quickly recovered to 93% of pre-COVID volumes (against an 18 January benchmark). Australia has seen a much more gradual return to credit application levels however: utility enquiries, for example, are now at 100% in New Zealand and only 75% in Australia. Credit enquiries are an important indicator of economic recovery and consumer confidence,” illion CEO Simon Bligh said.

“Effectively what we have seen in New Zealand is a U-shaped economic recovery, compared with something more like a swoosh in Australia – it’s a lot flatter,” said Bligh.

On August 14 illion said Kiwis were avoiding new debt, with applications for personal loans that fund major purchases such as cars and holidays, down to 70% of pre-COVID volumes.

Auckland was moved from COVID-19 Alert Level 1 to Level 3, and the rest of NZ to Level 2 from Level 1, on August 12 after four members of an Auckland family tested positive for the virus.

Westpac's update

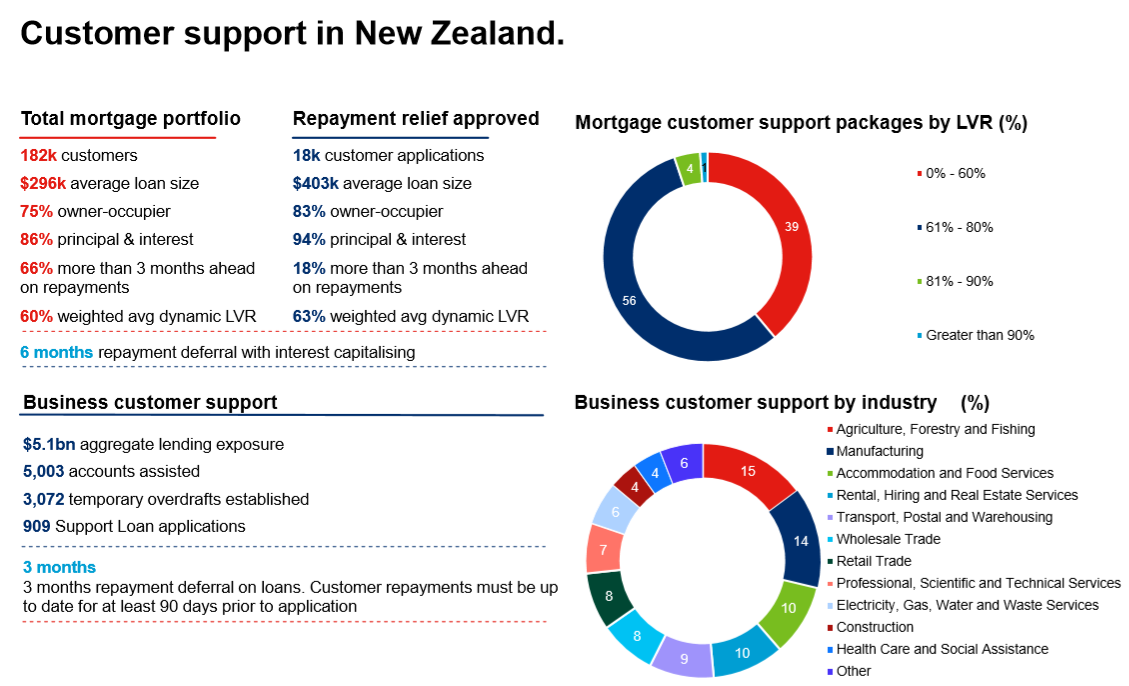

In its third quarter trading update, released on Tuesday, the Westpac Banking Corporation provided figures for COVID-19 related customer support from Westpac NZ. The figures in the diagram below are as of July 31, and in NZ dollars.

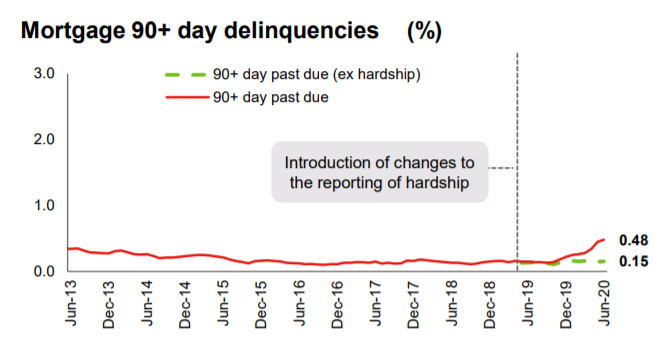

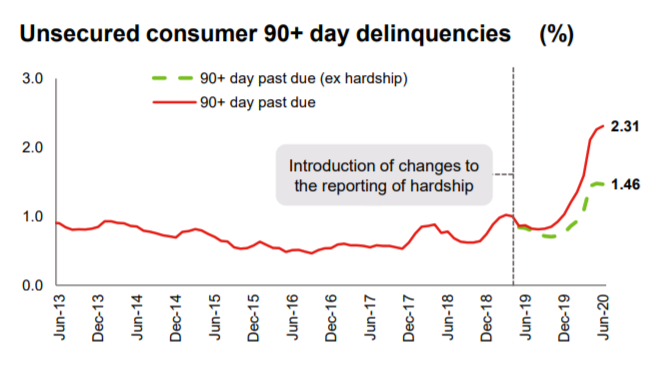

The Westpac charts below are on NZ asset quality.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

20 Comments

Fear is basic human psychology.

Credit driven by confidence

People don’t feel good and less optimistic. So, they are not going to borrow more

And much of prev bounce was prob people remortgaging at lower rates, which should be separated out but I do no think it is?

It shows that people only have confidence in housing market as are going beyond maximum limit to borrow to buy house by paying premium in this uncertain times.

People don’t feel good and less optimistic. So, they are not going to borrow more

Which means less money spent into the consumer economy, which means less revenue and lower margins. The NZ economy is designed so the typical consumer is spending as much as possible. Disrupt that any way and the whole economy gets whacked.

I think this is an interesting piece from Sharon Zoellner, ANZ clearly recognise some of the risks associated with unconventional monetary policies. I hope some of you will read it without preconceived, anti-banks, opinions.

https://push.bigtincan.com.au/downloads/ddd76ddb46f0720a85cf47bef6660c5…

{kind=link}

A good read, summed up best by her comments:

"New Zealand is still only at the beginning of the economic impacts of ...the virus.....Into the Twilight Zone we go"

There's also the bit about all of us being wiser in 30 years time, but it's how we are all prepared today that is all that matters.

Hi bw, I've asked you on previous threads for your opinion but you may have missed it, so here it is again, you've been calling for deflation and a liquidity crisis for well over a year now, WHEN do you see this finally happening given the RB & Government's endless attempts at delaying such a crisis?

It's probably already underway!

Every man and their soothsayer dog sees interest rates going to 0% and below. That view is now very lopsided. (NB: I've been suggesting for more than a few weeks now that getting long term funds on the book, 5 years etc, may be a good idea - price may get better, but so what?!) Regardless....

The determinant of liquidity on the World ultimately rests with the issuer of the Reserve Currency; the USA and the US$. As others have noted that there is already a shortage of US$ in The System; most of the 'printing' having floated to the surface and being tied up in bank reserves etc. and what's left is, and will continue to be, in short supply. It's not the price of money that's important, but access to/availability of it. And I reckon it's getting tougher by the day to get hold of debt.

Long story short = Watch what happens to availability of credit. After that comes price action; interest rates start rising as scarcity emerges and Central Banks won't be able to stop commercial interest rates rising.

That, of course, triggers (further) Deflation as those with anything to sell ( especially if it's backed by unpayable debt) HAVE to sell.

But we have Novermbers USA circus to get through yet, and that may determine just how quickly 'things' get going.

Thanks for your reply bw, I appreciate it. Do you mean liquidity contraction and deflation are already starting in the US? Because it certainly doesn't seem the case here in NZ. Also I understand that scarcity of credit should lead to interest rates rises for new loans anyway but I really doubt that interest rates on existing loans can rise much at all because it will precipitate bad loans to such an extent that banks will become insolvent. Is this not expired theoretical economic thinking? (not trying to argue, just having a counterpoint)

Your view bw?

PS: For what it's worth I ran across this in the arvos reading and it may give you an alternative view of mine above.

Pushing rates negative and flooding the global economy with USD is a sure way to reduce scarcity and demand, so those are not going to happen.

Rather, U.S. yields will start rising--maybe in fits and starts, but they will start moving up longer term. And the Fed isn't going to over-supply the global economy with dollars; they're going to start limiting the excess issuance, not publicly but behind closed doors.

Scarcity and demand will both rise, dragging the dollar higher. Don't bother asking why or how just watch the yields click higher despite every financial pundit pounding the table for zero or even negative yields. Yields may dip and weave from month to month, but watch the trend.

https://charleshughsmith.blogspot.com/2020/08/the-empire-will-strike-ba…

Don't bother asking why or how...

That about sums it. A bunch of reckons from a futurist who says to ask no questions, and he'll tell no lies. I prefer looking back to look forward though (and this is certainly in line with your first comment bw).

Diminishing cross-border trade and the shock of the coronavirus have fundamentally undermined demand for dollars. This is not to be confused with demand for dollar liquidity, which some say will support the dollar. Liquidity is required in all currencies, which will be satisfied by liquidation of financial assets. The ensuing collapse of financial asset values and foreign liquidation of dollars is increasingly likely because all classes of foreign investors have, until now, enjoyed the security of investing in the world’s reserve currency, while Americans have generally avoided owning foreign currencies. It is only a matter of time before this imbalance begins to undermine the dollar, and then consequences will follow.

https://www.goldmoney.com/research/goldmoney-insights/anatomy-of-a-fiat…

There's also the bit about all of us being wiser in 30 years time, but it's how we are all prepared today that is all that matters.

Zollner is part of the problem, not the solution. She's a product of the system and has internalized it so well that she's on top of the pile. Not a role I would particularly enjoy. I think you'd have to be sociopathic to head an Australasian retail bank.

I read this yesterday and thought it was a jolly good assessment of the situation. I absolutely agree that there is no way we can know the outcome of any of this.

We're entering twilight. After twilight, it usually just gets darker for some time, whilst all the torches will be available 30 years from now.

I don't think it's a stretch to say MMT is the Emporer's New Clothes and the vacuum of logic can't continue indefinitely as people start seeing the nakedness. We live in a finite system, but are currently expecting infinite returns and growth. Therefore, the logical outcome is a collapse/reset of our current financial system as we know it as it is unsustainable. The only unknown is how long we can prolong our avoidance of discomfort at all costs.

GN, what's your view about the thread re credit crunch and deflation above? Thanks

That is some admirable transparency from Zollner.

It's fascinating that the banks, and Adrian Orr, have now both acknowledged that super-low rates encourage asset bubbles, and in turn worsen inequality, and that they are concerned about this. As Zollner says, the RB doesn't have any mandate to worry about inequality -- Orr might personally be concerned about the prospect of us turning into Brazil but he can't justify his decisions thus.

Are they counting on Gov't policy to counteract this?

That is some admirable transparency from Zollner.

Disagree. It was part waffle, part dogma, part propaganda.

Certainly if Labour and Greens were to get in as government without Winston First they would have a moral mandate for massively increasing house building activity with no requirement at all to make a profit.

"...May bouceback" Proofreader missed that.

Where?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.