This Top 5 COVID-19 Alert Level 2, or 2.5, special comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

Cartoon: Mike Luckovich, The Atlanta Journal-Constitution.

Neel Kashkari is president and CEO of the Federal Reserve Bank of Minneapolis and a member of the Federal Open Market Committee. He doesn't have a typical central banker's background having started his career as an aerospace engineer. In this Bloomberg Odd Lots podcast Kashkari, among other things, unleashes on economists' obsession with what they call the natural rate of unemployment. He also admits the Fed got it wrong by raising interest rates from 2015.

The tightening cycle that began in 2015 was a mistake. It was predicated on a misreading of the labour market. We thought we were at full employment and in some cases beyond it, and we needed to hurry up and raise rates before inflation came. And obviously inflation didn't come. So we have to learn from that. And we have to recognise that the vast majority of people want to work. One of the big frustrations I have in the economics profession is every time there's a recession the economists immediately ratchet up this thing called the natural rate of unemployment.

All these people have been dislocated, now the natural rate of unemployment is 5[%] or 6[%], and if you get below that it's going to lead to inflation and it's just bunk. It's total bunk. And so the first thing we should do is stop doing that. The vast majority of Americans want to work and if given the chance and decent wages they will surprise us and re-enter the labour market. That's one of the things I hope we've learned, I've learned, in the last recovery that that is profoundly true. So we have to learn from that and not raise rates ahead of inflation. If you look at our inflation target it was officially adopted in 2012 at 2%. We basically undershot 2% the entire time. I mean we blew it and so lets not raise rates this time until we actually get inflation sustainably back at our target or even above it to make up for prior shortfalls.

Mainstream economists' thinking around a natural rate of unemployment does seem somewhat dogmatic. And it certainly frustrates Kashkari.

Why is it that economists always assume when there's a recession the natural rate of unemployment ratchets up, and it only falls down gradually over time? And they come up with all sorts of dislocations, fancy words, skills mis-matched, skills diminished. Boy this is an enormously costly error that we keep making. People want to work and that's one of the things that we've learned. And if we just allow the economy to recover I think they will continue to surprise us. And so yes, I do think that me not being an economist has helped me to see that, but that's not to say an economist can't see that too.

This image sums up the Pandemic economy of 2020 pic.twitter.com/vdDNpBtx03

— Lindsay David (@linzcom) August 31, 2020

2) Justifying equity bull markets.

Writing for Project Syndicate, Michael Spence who is a Nobel laureate in economics, argues that whilst it's true that bullish equity markets are out of step with the historic contraction in the real economy, to say they are disconnected from it misses the point. Rather the lofty valuations of companies with high intangible capital per employee makes perfect sense in today's world, Spence suggests.

He says the pandemic economy has accelerated a pre-existing trend favoring intangible-asset value creation through companies with fewer employees.

Many have concluded that the market is unmoored from economic reality. But, viewed another way, today’s equity markets may be partly reflecting powerful underlying trends amplified by the “pandemic economy.” Equity prices and market indices are measures of value creation for the owners of capital, which is not the same thing as value creation in the economy more broadly, where labor and tangible and intangible capital all play a role.

Moreover, markets reflect the future expected real returns to capital. When it comes to measuring the present value of labor income, there simply is no comparable forward-looking index. In principal, then, if there is a significant anticipated economic rebound, the outlooks for capital and labor income could be similar, but only capital’s expected future would be reflected in the present.

But there is more to the story. Market valuations are increasingly based on intangible assets, not least the ownership and control of data, which confers its own means of value creation and monetization. According to one recent study of the S&P 500, stocks in companies with high levels of intangible capital per employee have recorded the biggest gains this year, and the less intangible capital per employee companies have, the worse their stocks have performed.

In other words, incremental value creation in markets and employment are diverging. And while this was true even before the pandemic, the trend has now accelerated. There are at least two reasons for this. One is the rapid adoption of digital technologies as part of the response to lockdown measures. The second is that many labor-intensive sectors (which normally add value mainly with labor and tangible capital) have been partly or totally shut down as a result of lockdowns, social distancing, and consumer risk aversion.

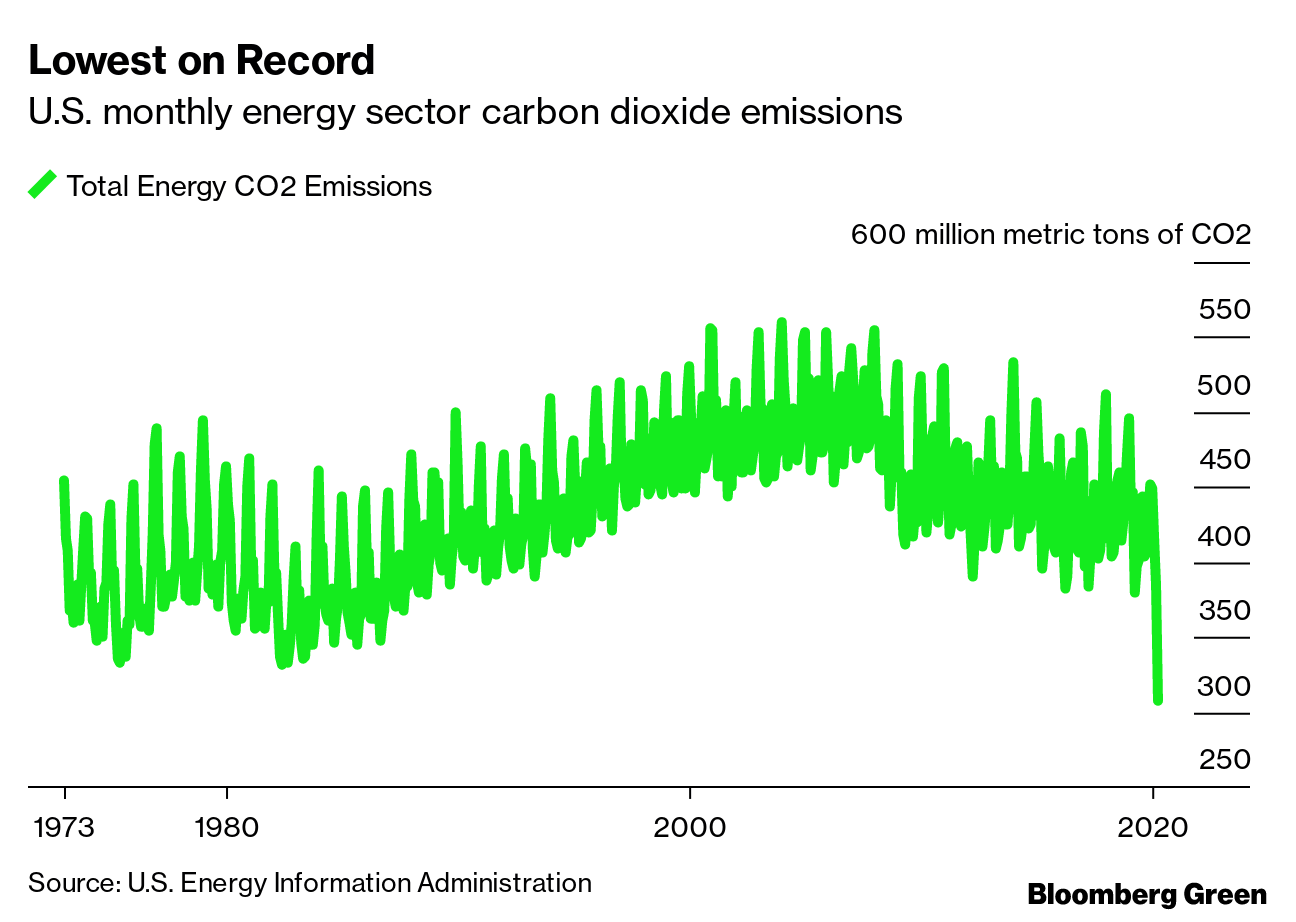

As Bloomberg puts it about the chart below, nothing in recent history has so thoroughly disrupted the act of burning fuels and emitting carbon dioxide in the US, the world's biggest economy, as COVID-19 has.

Melbourne has been embroiled in a tough battle with COVID-19 over the past couple of months but does appear to be slowly getting on top of the virus. Here the ABC analyses postcode data released by Victoria's Department of Health and Human Services.

Just nine Melbourne postcodes now have more than 50 active coronavirus cases, with numbers continuing to decline across Metropolitan Melbourne's hotspot suburbs.

Of those, only two have more than 100 active COVID-19 cases.

Still holding the unenviable honour of top hotspot postcode is 3029 for the sixth week running.

The postcode in Melbourne's west, which includes the suburbs of Hoppers Crossing, Tarneit and Truganina, has 126 active cases, down from 177 active cases a week ago, and recording a major decline in active infections since its peak of 463 on August 13.

The other postcode yet to get under the 100 mark is 3030, home to Point Cook and Werribee which has 121 active cases this week, down from 131 last week and 210 a fortnight ago.

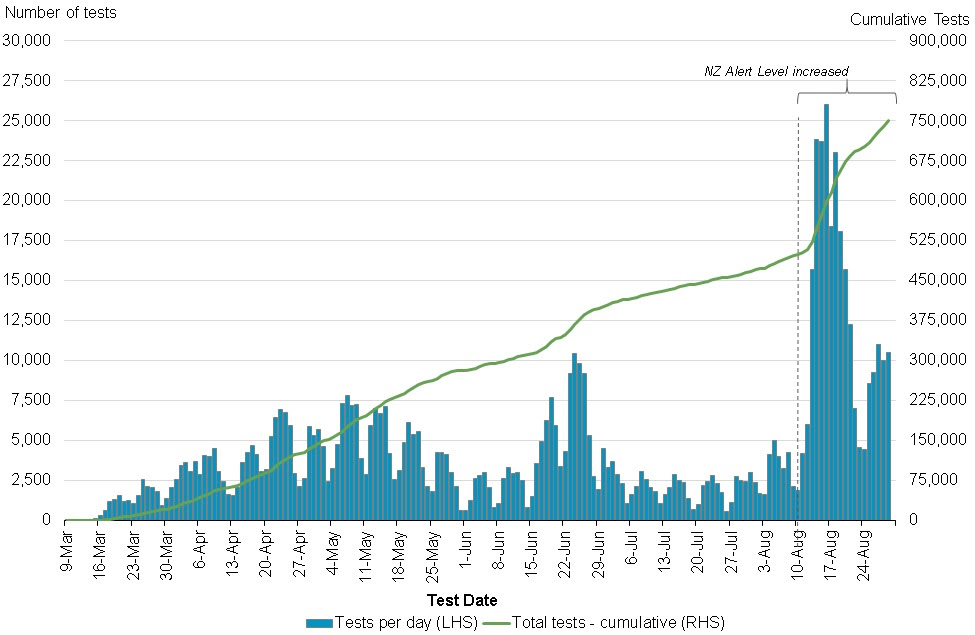

This chart is useful for putting the second wage subsidy extension in context (and indeed the second lockdown - though one has to bear in mind that the bar for qualifying for the two extensions was raised from 30% to a 40% revenue hit ). pic.twitter.com/R1cT447MRK

— Sharon Zollner (@sharon_zollner) September 3, 2020

4) What do you do when COVID-19 kills your tourism business? Why, start a nappy factory of course.

Like their counterparts in New Zealand, those working in tourism in the Argenitne province of Salta have been hard hit by the loss of overseas tourists. Here the Buenos Aires Times looks at new business ideas some of the tourism workers are turning to. Food, wine and carpentry feature, along with nappies. Argentines, the article points out, have plenty of experience with economic crises.

One of the more leftfield ideas is the brainchild of a local celebrity, Francisco Siciliano, always a pioneer. Originally from Santa Fe, “Pancho”, as everyone in Salta knows him, came to work in the northwest 15 years ago, after studying tourism in Buenos Aires.

“I loved the area, I used to come every year,” he recalled.

His agency, Argentina Trails, specialises in intrepid mountaineering and hiking expeditions. “Our clientele is 100 percent foreign, mainly from Switzerland, UK and France, but also Austria and Japan,” he says.

Pancho is currently converting an old building close to the international airport, in the town of Cerrillos, into a nappy factory. The plan is to employ locals as door-to-door salespeople.

“There’s a terrible embarrassment about adult nappies, so we’re going to produce those as well as for babies, and even nappies for pets,” he explained.

“I’ve gone five months without work, and was investigating areas, different sectors, looking at what might work. I enjoy producing something new, setting a new venture up, and we’ll be making things that people are always going to need.”

COVID-19 Tests per day

Source: Ministry of Health

5) What's the worst thing that could happen?

The November US presidential election is inching closer against the backdrop of COVID-19 and Black Lives Matter protests. Writing in The Washington Post, Georgetown University law professor Rosa Brooks asks the question; What's the worst thing that could happen?

Involved with a group called the Transition Integrity Project, Brooks says a series of war games were cooked up, with Republicans, Democrats, civil servants, media experts, pollsters and strategists' views sought on a range of election and transition scenarios.

A landslide for Joe Biden resulted in a relatively orderly transfer of power. Every other scenario we looked at involved street-level violence and political crisis.

It certainly feels like the Divided States of America is a tinderbox at the moment. This perception was reinforced to me when Zooming with my cousin and his wife in Chicago last weekend. Brooks has some advice for the military and law enforcement, the media and citizens.

Meanwhile, military and law enforcement leaders can prepare for the possibility that politicians will seek to manipulate or misuse their coercive powers. Partisans, including Trump, may try to deploy law enforcement, National Guard troops and, potentially, active-duty military personnel to “restore order” in a manner that primarily benefits one party, or involve troops and law enforcement in efforts to interrupt the ballot-counting process. The federal response to this summer’s protests in D.C.’s Lafayette Square and Portland, Ore., suggests that this is not purely speculative. To avoid becoming unwitting pawns in a partisan battle, military and law enforcement leaders can issue clear advance statements about what they will and won’t do. They can train troops and police officers on de-escalation techniques and on the vital need to remain nonpartisan and respectful of civil liberties.

The media also has an important role. Responsible outlets can help educate the public about the possibility — indeed, the likelihood — that there won’t be a clear winner on election night because an accurate count may take weeks, given the large number of mail-in ballots expected in this unprecedented mid-pandemic election. Journalists can also help people understand that voter fraud is extraordinarily rare, and, in particular, that there’s nothing nefarious about voting by mail. Social media platforms can commit to protecting the democratic process, by rapidly removing or correcting false statements spread by foreign or domestic disinformation campaigns and by ensuring that their platforms aren’t used to incite or plan violence.

Finally, ordinary citizens can help, too — perhaps most of all. As the jurist Learned Hand said in 1944, “Liberty lies in the hearts of men and women; when it dies there, no constitution, no law, no court can save it . . . while it lies there, it needs no constitution, no law, no court to save it.” This is as true now as it was then: When people unite to demand democracy and the rule of law, even repressive regimes can be stopped in their tracks. Mass mobilization is no guarantee that our democracy will survive — but if things go as badly as our exercises suggest they might, a sustained, nonviolent protest movement may be America’s best and final hope.

7 Comments

Stephanie Kelton in her book on MMT also identifies that the 'natural rate of unemployment' is not a valid measure, and that literal 'full' employment can be gained. My view is that there are natural constraints, not around if it can be achieved, but in doing what? Full, meaningful employment is an important requirement, and indeed should be an expectation. But things like 'productivity' take on a different perspective in some areas.

Completely agree. Sometimes this arguments lack substance. As you so correctly say, you can achieve full employment if there is no regard to meaningfulness of employment. I know from first hand experience where manufacturing companies that were government owned employed way more than they needed so the government can claim employment in their area. But not only the cost of employment meant that the factor was not viable, the actual physical output of the factory reduced.

The Supreme Court will be getting ready soon in Washington, rehashing the Gore-Bush case of 2000.

The Military will stay on the sidelines, unless street riots erupt on election night and after and get out of control.

The Constitution will prevail in the end.

And the Markets will rebound after the Inauguaration, as usual.

This is what my crystal ball says. No guarantee though.

It’s easy to see a scenario where trump calls on his supporters and incites these riots once he realises he’s likely lost. This is where the Republican Party needs to take some responsibility and insure this doesn’t happen.

The US election has the potential for serious civil unrest IMO, the US feels like it's ready to explode. My expectation is that it would be worse if Trump get's up, we've had a taste of that in Portland.

The Economist's article on #5 ;

https://www.economist.com/leaders/2020/09/03/americas-ugly-election

1) Central banker admits mistakes and hits out at economists' obsessing over the natural rate of unemployment.

Wait, wait, wait. Hold up. The Federal Reserve just concluded its near two-year long Grand Strategy Review. The purpose, in its most basic component, was to figure out why inflation hadn’t shown up in the manner everyone at the Federal Reserve spent years promising even though the unemployment tumbled to 50-year lows.

The labor market was so tight, inflation was guaranteed. Then it didn’t happen. Link

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.