Bad things inevitably happen when the Reserve Bank governor has a distorted view of house price prospects, as Governor Wheeler currently has.

This is particularly the case in terms of house price prospects outside of Auckland that are in the process of improving dramatically at the very time the governor is focusing on the lack of upside. Ironically, the fall in dairy product prices, that is playing a key part in the OCR cuts the governor is in the process of delivering, significantly improve house price prospects, including in dairy intensive regions like the Waikato.

In the first instance, the warning bells I am ringing are about upside prospects for house prices, especially in the Upper North Island (e.g. Waikato, Northland and Bay of Plenty). But in time the much greater upside in house prices than Governor Wheeler expects will pose threats, especially to borrowers, as covered in our monthly Mortgage Strategy reports.

These are interesting and dynamic times, with the potential to deliver a range of surprises, including some positive surprises relative to the gloom suggested by the latest ANZ business confidence survey.

Governor Wheeler's rear-view-mirror focus in house prices outside of Auckland

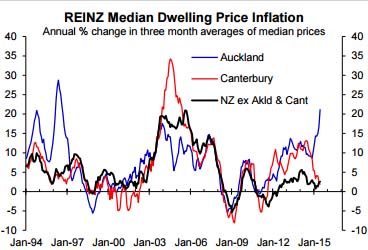

In the 23 July Policy Assessment that accompanied the announcement the OCR would be cut to 3%, Governor Wheeler stated: "House prices in Auckland continue to increase rapidly, but, outside Auckland, house price inflation generally remains low."

The governor was more specific about house price inflation outside of Auckland in a speech on 29 July, with the following being an extract from the Reserve Bank's news release regarding the speech: "Lower interest rates risked exacerbating the already extensive housing pressures in Auckland by stimulating housing demand, although, outside of Auckland, nationwide house price inflation is currently running at an annual rate of around 2 percent."

Canterbury should be considered a special case because of the impact of the earthquakes. For the three months end June, house price inflation in the rest of the country was 2.5% (i.e. only a bit above 2%).

But in making OCR decisions the governor should focus in future prospects for things like house prices outside of Auckland and Canterbury, not focus on what has happened over the last year.

Making OCR decisions based on a rearview-mirror perspective reflects the reactionary approach to monetary policy that has been used too much in NZ (and overseas) in the past. It is a route to monetary policy exacerbating economic and housing market cycles (i.e. excessive OCR cuts followed by excessive hikes, just as Governor Bollard did in the 2000s).

The governor's rear-view mirror approach goes well beyond house price prospects, as covered in our monthly economic reports and the six weekly reports we produce critiquing the governor's OCR decisions and the Reserve Bank's forecasts. But the focus here is just on house prices, in part because of the pivotal role housing plays in economic cycles (i.e. if the governor is wrong about house price prospects, he will most likely be wrong about economic growth and inflation prospects.

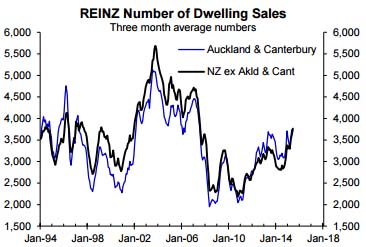

What happens to house sales is a prelude to what house prices will do. The adjacent chart shows a sharp increase in the number of house sales for NZ excluding Auckland and Canterbury over the last nine months. Rolling three month averages of the seasonally adjusted numbers of sales are used to smooth the volatility in the monthly numbers and remove the seasonal behaviour of sales. In the three months to June 2015, the number of sales for Auckland and Canterbury was up 20% from the three months ended September 2014, while for the rest of the country the increase was 31%. The level of sales in the rest of the country has gone from underperforming the level for Auckland and Canterbury combined to starting to marginally outperform. The upturn has been most impressive in the regions near to Auckland: Northland sales up 53%; Waikato sales up 60% and Bay of Plenty sales up 39%.

The fact the housing boom is spreading well beyond Auckland shouldn't be news to the governor. On 4 June an article in the Herald reported a surge in Aucklanders searching for properties in the Upper North Island (see the link below). The following is an extract from that article:

Realestate.co.nz data shows Aucklanders are more interested in homes outside their region compared with the same time last year. Last month more than 12,600 searched for homes in the Hawkes Bay, up by 152 per cent from the same time last year. The figure accounted for 36 per cent of all searches or views in the regions. Other regions that saw a jump in interest from Aucklanders included Manawatu and Wanganui, up 123 per cent; Waikato, up 114 per cent; Northland, up 86 per cent; and the Bay of Plenty, up 84 per cent. "This is a dramatic change in online searching behaviour, which could well be driven by record high property prices in Auckland," said chief executive Brendon Skipper.

QV released two reports in the first half of July focused on the upside in house prices spreading especially to the Upper North Island (see the links here and here). The following is an extract from the 14 July report:

It appears that many Aucklanders are looking to capitalise on their equity by either selling up and moving to Hamilton, Tauranga and the Hawkes Bay or using their equity to purchase rental properties there. “There are reports of large numbers of Aucklanders are flocking to buy property in Tauranga, Hamilton and the Western Bay of Plenty resulting in rising values in these centres,” said QV National spokesperson Andrea Rush.

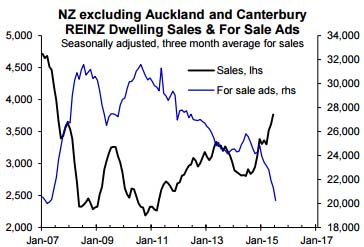

Quality economic analysis is supposed to be based on analysing demand and supply in the market under consideration. The chart above shows the dramatic improvement or tightening in the demand-supply balance in the housing market for the rest of NZ this year (i.e. surging sales and a tumbling stock of property for sale). A forward-looking focus on house price prospects outside of Auckland and Canterbury should conclude that prospects are in the process of improving dramatically from the minor increase experienced over the last year that Governor Wheeler keeps focusing on. The demand-supply balance indicated by the chart above suggests that house price inflation outside of Auckland and Canterbury could reach 10% or so by the end of the year, with more upside in sales and downside in the stock of property for sales likely over the next several months in response to the continued fall in mortgage interest rates.

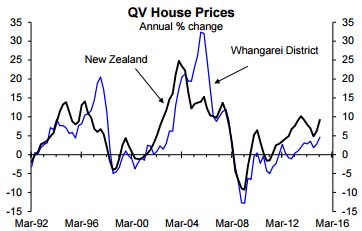

In my assessment Whangarei, where I have the most direct experience, is about to experience a mid-late cycle surge in house prices of the sort experienced in the 1990s and 2000s (see the spikes in Whangarei house price inflation in 1997- 98 and 2004-05 in the adjacent chart).

Denise and I have seen clear evidence of the Whangarei market heating up significantly over the few months while searching for Northland rental properties to buy. There is strong evidence of increased buying by investors and first home buyers, and a switch to selling via auctions or sell by dates that are prevalent in Auckland and reflective of a hot market. For the right sorts of properties, multi-offers have become common (i.e. tidy three bedroom houses and especially those sort after by first home buyers and investors).

The more dairy product prices fall the more house market prospects will improve

Governor Wheeler is focused quite a bit on the fall in diary product prices in justifying OCR cuts, while in my assessment the business sector has seized the opportunity offered by the ANZ business survey to provide the governor with the evidence of slower growth he is seeking to justify further cuts. This issue was the focus of the last Raving, but it warrants revisiting given the further tumble in business confidence in the just released ANZ July survey. Use the link below to access the latest ANZ survey results and to read the lack of critical assessment of the survey results by the ANZ economists. Of note are the comments about downside risk for building activity because lots more of the building respondents to the survey have ticked the negative box. In the case of residential building, the downside risk signalled by the ANZ survey runs counter to what other much more reliable leading indicators are predicting (i.e. the surge in existing house sales reported by REINZ).

The most topical local economic issue at the moment is the tumble in diary product prices. Some people may connect tumbling dairy farm incomes to falling business confidence and downside risk for residential building. Some link to the fall in business confidence is justified, but rather than representing a threat to the housing market, the fall in dairy farm incomes increases the upside potential, including in the likes of the Waikato and Taranaki where lots of dairy cows live.

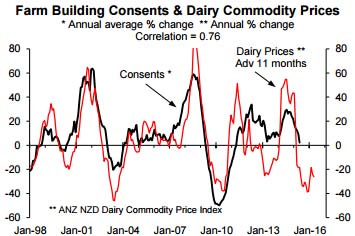

As an aside, the fall in farm building consents will reflect fewer conversions to dairy farms, which is part of the process that will slow local and global milk production and contribute to the next upturn in dairy product prices, but that is another story (and one we cover in our monthly economic reports).

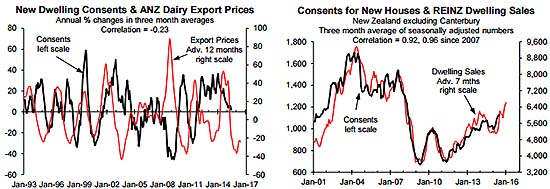

It is a very different story when it comes to any link between residential building and dairy product prices and quality analysis should point this out. The left chart below shows a mildly negative correlation (-0.23) rather than significant positive one between the annual % change in diary product prices advanced by 12 months and the annual % change in new dwelling consents. It is more often the case that downturns in dairy product prices are followed by upturn in new dwelling consents than downturns. This is also the case for new dwelling consents in dairying provinces like the Waikato.

The fall in dairy farm incomes will have a minor negative impact on the housing market via the impacts on the number of investment properties brought and/or sold by dairy farmers and employment growth; although even in the Waikato there is no clear link between dairy product prices and employment growth. The real story is that the fall in interest rates, aided by the fall in dairy product prices, population growth approaching 2% as a result of much higher net external migration and a range of government initiatives (e.g. increased first home buyer grants, Housing Accords, changes to social housing) are providing a major boost to residential building; helped in the case of the Waikato by flight from expensive Auckland housing. And this is why consents to build new houses for NZ excluding Canterbury have started to follow the earlier increase in dwelling sales reported by REINZ. The right chart below shows an extremely high correlation between the number of dwelling sales advanced or leading by seven months and the number of consents for new houses. Dwelling/house sales should head higher over the rest of the year as a lagged response to the unfolding fall in mortgage interest rates that are by far the key cyclical driver of the housing market.

The upside in new house consents outside of Canterbury should more than make up for any more downside in Canterbury rebuilding activity, as discussed in our monthly Building Barometer reports. The surprise over the next year should be upside in residential building rather than the downside suggested by the latest ANZ survey of residential builders' expectations. Maybe the world has turned topsy-turvy, but I think the most reasonable explanation is that an increasing number of respondents to the ANZ survey are realising they can manipulate OCR decisions by ticking the negative box, with this game made much easier by Governor Wheeler's predisposition to cut the OCR because of his crusade to talk the NZD down, which he tries to do at every opportunity (see the links here and here).

So why am I ringing warning bells?

Rather than ring warning bells, this Raving presents positive outlooks for house prices and residential building, especially for the Upper North Island. But the games Governor Wheeler, the bank economists and some respondents to the ANZ survey appear to be playing do ring warning bells as well as present opportunities to make money from the housing upturn. These games should be viewed in the context of the poorly justified OCR cuts delivered by Governor Bollard in 2003 that were followed by 13 OCR hikes between 2004 and 2015. For more about the risks I refer readers to our pay to view reports, including the newish Mortgage Strategy reports.

----------------------------------------------

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

2 Comments

But the games Governor Wheeler, the bank economists and some respondents to the ANZ survey appear to be playing do ring warning bells as well as present opportunities to make money from the housing upturn. These games should be viewed in the context of the poorly justified OCR cuts delivered by Governor Bollard in 2003 that were followed by 13 OCR hikes between 2004 and 2015.

An RBNZ governor denied integrity is a governor about to be denied tenure. No?

Real estate insight from the San Francisco Fed as seen through the eyes of another.

This Economic Letter investigates the link between interest rates, mortgage lending, and house prices. Quantifying this link is important in assessing whether or not interest rate policy can be used to guard against leveraged asset price booms in practice. Housing plays perhaps the most important role among asset classes because purchases are typically leveraged through mortgages. Many consider the 2002–06 housing bubble an important trigger of the subsequent financial crisis. However, economists disagree about the role that low interest rates played in fueling the house price boom. Our goal in this Letter is different. We instead ask how much interest rates would have had to rise to keep housing prices under control. Our rough figures suggest interest rates would have needed to rise around 8 percentage points to completely avoid the boom-bust cycle. However, such a boost also could have caused significant damage to the Fed’s main objectives of full employment and price stability. Read more

For a number of reasons Christchurch is heading for a period of flat to falling prices (dependent on which sector of the market) and rents and rental demand are both in free fall.

On that basis I can not see regional South Island price increases at all, bar maybe Queenstown due to continued foreign influence - however it is still suffering a mass oversupply of vacant land and low land prices which will constrain any potential growth.

Maybe the upper North Island will grow due to the Auckland effect and foreign cash pushing local money to the nearby regions, but any sustained boom while the economic doldrums approach is probably unlikely.

It is interesting that markets where there is an absolute oversupply situation can take decades to recover. One example is Te Anau, where massive developments went in during the early 2000s boom. Sections were offered at what seemed like bargain prices from around $79,000. 10 years on you can pick up those same sections at or under $50,000 any day of the week. And at the current rate of building it would take almost until the end of the century (ie 2100) for all of the current sites available to be built on.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.