By Christina Leung and Kirdan Lees*

But the economic environment is changing. No longer does the Reserve Bank need to lift rates to reduce demand.

Today the Reserve Bank needs to deal with supply shocks that rapidly change how New Zealand firms organise activity.

Increasingly that makes inflation targeting no longer fit-for-purpose. Instead, targeting income growth – the sum of inflation and economic growth – looks the best bet to deal with new economic conditions.

Inflation targeting has worked but the economic environment is changing

But the global economic environment is changing. The Reserve Bank used to have to raise rates when demand for goods was sufficiently strong that it threatened to bring about higher inflation. Today, the battle is not so much demand, but negotiating a myriad of shocks to the way firms supply goods. These shocks include improvements in logistics that make it easier and faster to deliver goods to consumers, new technologies like fracking which make extracting oil cheaper, and new devices that place product information at consumers’ fingertips. Globalisation and the internet have greatly increased competitive pressures across the globe. New Zealand is no exception.

Targeting income growth deals with the new economic environment better than inflation targeting

High time to reassess the monetary policy framework

We could tweak the existing system…

Before leaping in to wholesale framework changes it is worth considering tweaks to the status quo that might improve how the economy deals with supply shocks while preserving inflation targeting. We see two possible tweaks that would help:

♦ Taxing and contracting in real not nominal terms – Many of the costs associated with inflation come from taxing nominal rather than real incomes. If feasible, taxing real incomes would help mitigate some of the costs and uncertainty from indexing taxation to nominal incomes. Likewise, contracting over real wages that take into account changes in inflation, rather than nominal wages that don’t would reduce the costs of inflation.

♦ Broadening the Policy Targets Agreement – Rewriting the Policy Targets Agreement to place more weight on asset prices and output rather than inflation could help on the margin, allowing the Reserve Bank to focus more on output rather than inflation. But the Policy Targets Agreement has been tweaked pretty hard. Pushing further risks disconnecting with the nominal anchor, that is, the variable a central bank uses to set household and firm expectations about how where interest rates need to be.

…but benefits are likely to come from more fundamental changes.

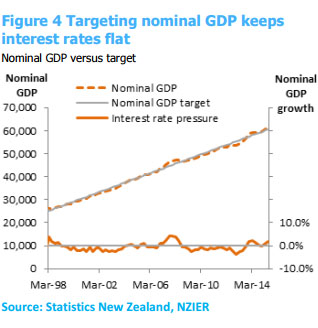

If supply shocks that lower inflation but don’t affect growth keep hitting the economy there are alternatives. Rather than targeting inflation, targeting growth in nominal incomes produces good outcomes by allowing a central bank to respond more rapidly to supply shocks. Nominal GDP targeting requires raising interest rates when nominal GDP is above trend and lowering rates when nominal GDP is weak.

Many economists test how nominal inflation targeting performs relative to inflation targeting in stylised economic models. These models suggest less volatile inflation, output and interest that make people about 22 percent better off.5 This relates to the responsiveness of monetary policy and Sumner (2014) argues that had the Federal Reserve followed a nominal GDP target, monetary policy would have responded more rapidly, mitigating the extent of the recession after the GFC.6 Models that include asset prices are likely to exacerbate these differences.

A good monetary policy regime needs to do two things:

♦ Define a nominal anchor – that is, a target variable the central bank uses to align expectations of households and firms on the future path of interest rates

♦ Help stabilise the economy against shocks that buffet the economy.

A monetary policy regime also needs to be feasible for a central bank to implement. A central bank cannot simultaneously fix the exchange rate and move the interest rate to achieve an inflation target since capital flows will look to take advantage of interest rates differentials and shift the demand for Kiwi dollars and the exchange rate.

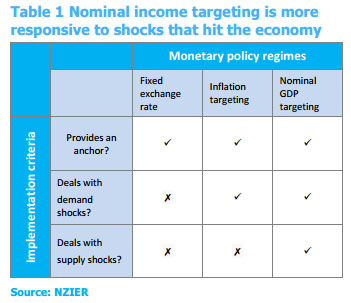

The Reserve Bank of New Zealand has tried basically two monetary policy regimes – fixing the exchange rate which was tried until the Kiwi was floated on 4 March, 1985 and then inflation targeting from the early 1990s. Each regime tries to minimise the impact of shocks on the economy. In the case of a fixed exchange rate, mitigating volatility by fixing export and import prices or under inflation targeting, moving interest rates in response to shocks. Similar to inflation targeting, under nominal income targeting a central bank responds to economic shocks by moving interest rates up or down.

And nominal income targeting would deal with demand shocks equally as well as inflation targeting, for example, by reducing rates quickly during the GFC. Since demand and supply shocks are the key shocks that hit the economy, it is critical any regime can deal with these shocks. Table 1 assesses nominal income targeting inflation targeting against current and previous monetary policy regimes using our key criteria.7

Right now the gap between inflation and nominal income growth is pretty big and growing, yielding materially different interest rates settings depending on the underlying framework.

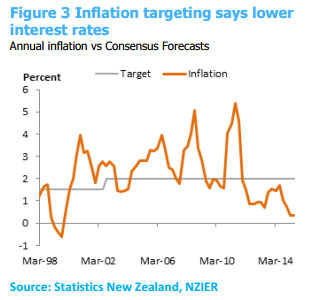

Our current inflation targeting framework says lower interest rates are required to hit a two percent target while a nominal GDP target would suggest interest rates are about right.

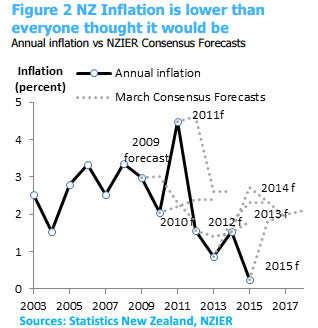

If the current low inflation environment persists for much longer it is difficult to justify the extended period of inflation away from target as temporary factors. Either rates need to be lower or the inflation target is undermined.

In contrast, nominal GDP targeting seems like an increasingly sensible framework for setting monetary policy delivering a better mix of inflation and GDP growth.

At the very least, there are appealing options should inflation targeting run out of steam.

Notes:

1. Ehrman (2015) describes the current period as “targeting inflation from below”.

2. Japan has recently set a target for nominal GDP.

3. Sometimes nominal income growth targeting is criticized as being difficult to implement because GDP is subject to revisions. But nominal income growth targeting requires setting interest rates so future income growth is close to target. Interest rates would not be buffeted by revisions to GDP. Revisions to GDP also affect the output gap, a crucial driver of inflation in most Reserve Bank models. These models apply under both frameworks so from a modelling perspective revisions are equally problematic.

4. For some countries with a large amount of debt after the Global Financial Crisis, targeting nominal GDP is appealing since it allows for some inflation and nominal GDP growth that help inflate debt away, keeping nominal debt at levels that the economy can manage. Tight monetary policy that aims to keep a lid on inflation works against repaying debt. This rationale doesn’t apply to New Zealand with government debt at relatively low levels.

5. See Jensen (2002) while McCallum and Nelson (1998) find nominal income targeting dominates inflation targeting in a stylised open economy model.

6. McCallum and Nelson (1999) and Jensen (2002) provide model-based insights and see Sumner (2014) for an overview of recent US debates.

7. Mann and Hooper (1993) provide several examples of evaluating monetary policy regimes based on the response to demand and supply shocks.

References

Ehrmann, Michael (2015), “Targeting Inflation from Below - How Do Inflation Expectations Behave?,” International Journal of Central Banking, Vol. 11 No. S1, September.

Frankel, Jeffrey (2014), “Nominal GDP Targeting for Middle Income Countries”, Working Paper Series rwp14-033, Harvard University, John F. Kennedy School of Government.

Jensen, Henrik (2002), “Targeting Nominal Income Growth or Inflation?,” American Economic Review, American Economic Association, vol. 92(4), pages 928-956, September.

Mann and Hooper (1993), Evaluating Policy Regimes: New Research in Empirical Macroeconomics, Brookings Institute, Brookings Institution Press,

McCallum, Bennett T. and Edward Nelson (1999), “Nominal income targeting in an open-economy optimizing model,” Journal of Monetary Economics, Elsevier, vol. 43(3), pages 553-578, June.

Sumner, Scott B. (2014), “Nominal GDP Targeting: A Simple Rule to Improve Fed Performance”, Cato Journal, Vol. 34, No. 2 Spring/Summer.

Christina Leung is a senior economist and Kirdan Lees is a principal economist at the NZIER. The original version of this article is here.

41 Comments

"new technologies like fracking which make extracting oil cheaper" this is not correct. a) fracking is not new, it has been around since the 1980s b) it only makes extracting shale oil cheaper and that is a maybe, ie shale oil is only economic to extract in sweet spots in the shale plays when the price is high and finance cheap.

Sure must be a lot of sweet spots out there for your theory to be correct. Also, surely you must have noticed the oil price is no longer high and much to the Saudi's chagrin the shale wells are still pumpin'.

It was the coupling of fracking with horizontal drilling that made all the difference - you are missing half of the story here. Also productivity is getting better and better. So have agree with the statement "new technologies like fracking which make extracting oil cheaper". Poor hand wringing peak oilers.

Note no mention of "sweet spots".

"Growth in U.S. hydrocarbon production from shale resources driven by drilling efficiency. DPR data show that each drilling rig in the Eagle Ford Shale will contribute over 400 barrels of oil per day (bbl/d) more in April 2014 than it would have in the same formation in January 2007."

"Capital efficiency gains from drilling longer laterals, cost savings from multi - well pad drilling and potential EUR uplift can generate well economics in this commodity price environment that rival the returns from a higher oil price environment"

http://www.eia.gov/todayinenergy/detail.cfm?id=15351

http://www.laredopetro.com/media/28968/corporate-presentation-november-…

Only 1% Of The Bakken Play Breaks Even At Current Oil Prices

All Bakken producers in this study can break even at $60-70 per barrel wellhead oil prices at current low drilling and completion costs. At $30 realized prices, they are all in serious trouble. Their investor presentations give little sense of how perilous their situation is in this price environment.

http://www.forbes.com/sites/arthurberman/2015/11/03/only-1-of-the-bakke…

The Biggest Red Herring In US Shale

"Rig productivity and drilling efficiency are red herrings.

A red herring is something that takes attention away from a more important subject. Rig productivity and drilling efficiency distract from the truth that tight oil producers are losing money at low oil prices.

Pad drilling allows many wells to be drilled from the same location by a single rig. Rig productivity reflects the increased volume of oil and gas thus produced by each of a decreasing number of rigs. It does not account for the number of producing wells that continues to increase in all tight oil plays.

In other words, although the barrels produced per rig is increasing, the barrels per average producing well is decreasing"

Rig productivity and drilling efficiency measurements do not account for declining average well productivity. They will only become useful if they can be related to the marginal cost of producing a barrel of oil. For now, they are distractions from the more important subject of tight oil profitability.

http://oilprice.com/Energy/Crude-Oil/The-Biggest-Red-Herring-In-US-Shal…

It would be interesting to see what happens when the hedges expire. I guess the USA is the land of ZIRP so money ain't what it used to be and tight oil needs all the subsidizing it can get to stay afloat at current prices.

"In other words, although the barrels produced per rig is increasing, the barrels per average producing well is decreasing".

Production per well data. Also improving over time. red Herring alright.

The History of Fracking can be traced back to 1862.

"Modern day fracking didn’t begin until the 1990s. This originated when George P. Mitchell created a new technique, which took hydraulic fracturing, and combined it with horizontal drilling."

So 25 years ago both techniques were combined, like I said it isnt new technology.

"In conclusion, what enabled the oil and gas industry to extract oil from shale rock over the past 7 years was higher prices. If it weren’t for higher oil prices, the capital investment needed in the oil and gas sector, wouldn’t have occurred, and US oil production would have continued to decline"

http://oilprice.com/Energy/Crude-Oil/The-Real-History-Of-Fracking.html

Wells pumping, but they have a few short years, 3 or so for a reasonable production. The important thing is the degree of rigs actually drilling and that has significantly dropped. Sure barrels per well will improve in the short term the drillers are going for the best spots that isnt unexpected.

Yeah but the better the initial production the quicker you can get your money back - especially in the current market! And as you can see from that chart they are getting more out of each well contrary to what Pluto's man was stating.

A fracking operation today is nothing like even five years ago. Yes high oil prices pushed innovation but that is hardly unusual, the genie is now out of the bottle. Ironic how frackers shelved drilling in the Arctic rather than Greenpeace.

"Thanks to new sensing capabilities, the volume of data produced by a modern unconventional drilling operation is immense—up to one megabyte per foot drilled, according to Mills’s “Shale 2.0” report, or between one and 15 terabytes per well, depending on the length of the underground pipes. That flood of data can be used to optimize drill bit location, enhance subterranean mapping, improve overall production and transportation efficiencies—and predict where the next promising formation lies. Many oil companies are now investing as much in information technology and data analytics as in old-school exploration and production."

Thank goodness for those IT boys eh?

http://www.technologyreview.com/news/537876/big-data-will-keep-the-shal…

Except that old wells could produce for 10, 20 years per well, these wells produce for 3~5. So you have to drill 4 complex wells instead of one simple well. If you make the well more complex and stretch further it is no surprise you can get more out. The thing is the output per $ or per metre long term, ie in the beginning its expected the output will rise, after peak it will drop.

High prices didnt push innovation as such the high price, low funding and hedgeing made it appear economic. Interesting that the oil drillers are drilling mainly because they have hedged ie are getting more for their oil than the market price. Despite that the rig count has collapsed, one wonders where the numbers would be in an un-hedged market.

Sure IT will help, well the sensors will to create the maps, so we'll see a bit more oil than traditional methods the field will still peak and decline.

The "old" can't extract oil out of shale so why are you even bothering to compare. Yes the initial burst in shale is 3-5 years. Then there is refracking - which makes your comment about rig count redundant.

"A study by Bloomberg Intelligence of about 80 wells that were originally tapped in North Dakota’s Bakken formation in 2008 or 2009 and then refracked again years later shows a clear pickup in output. The wells on average produced more than 30 percent more oil in the month after the refrack than they did after the original completion, according to analysts William Foiles and Peter Pulikkan."

"Halliburton reports seeing up to an 80 percent increase in (estimated ultimate recovery) EUR per well, up to 25 percent increase oil recovery factor of unconventional asset with a balanced portfolio, and up to 66 percent reduced cost per barrel of oil equivalent (BOE) compared to new drills. The company reports seeing a 300 percent improvement in EUR in natural gas wells in the Haynesville and Eagle Ford plays. In the oil window of the Eagle Ford, Halliburton’s technology has increased the average EUR of wells by 121 percent.

http://www.rigzone.com/news/oil_gas/a/140694/Refracking_Service_Could_C…

http://www.bloomberg.com/news/articles/2015-07-06/refracking-fever-swee…

"old" that should be obvious, as stated you need 4 times (if not 6) the shale oil wells which cost considerably more than one vertical well of the "old type".

re-fracking" is a bit of a could, maybe as yet, not without issues either. "Refracked well’s IP rates are mixed when compared to the original rates, IHS said. Of the refracked wells studied by IHS, most have have lower IP rates except for the Bakken."

"Pioneer COO Timothy L. Dove said refracking in the Permian Basin doesn’t make a lot of sense, according to a Seeking Alpha transcript of the company’s first-quarter earnings call.

However, Dove sees a handful of refracking candidates in the Eagle Ford."

So some wells maybe suitable, many possibly not.

http://www.oilandgasinvestor.com/refracking-remains-boutique-technique-…

Even if it can boost production and that isnt a given. "Then there’s the concern that some industry analysts have that a refrack only accelerates the flow without increasing the actual total output over the life of the well. EOG is among the drillers that remain reluctant to start using the procedure." it pushes Shale's peak out a few years, not a game changer.

hedging, so for now someone else is wearing their pain.

Also if I remember correctly the comments by the likes of David Hughes? was that the EIA had not even considered that there are sweet spots in the fields but taken a blanket approach when in fact significant parts of the field are un-economic.

interesting pod cast on the hype,

http://www.peakprosperity.com/podcast/89793/shocking-data-proving-shale…

"Let’s just take a play like the Bakken.: 45% annual field decline, sweet spots are getting to be drilled out. We know that they need to drill 1,500 wells a year just to keep production flat. But as you go into lower quality rock, the well quality in most of the play's extent is only about half of what it is in the sweet spot. If you have to rely on the lower quality part of the play you need 3,000 wells per year instead of 1,500 to offset the field decline. "

Current inflation adjusted oil price is not looking peaky in fact it looks completely boring - a whole 5 cents off the 1946-2015 inflation adjusted average. Who would have though that possible in 2008 or 1979.

"The average for the entire period from 1946 to present is $41.70" (April 2015).

http://inflationdata.com/Inflation/Inflation_Rate/Historical_Oil_Prices…

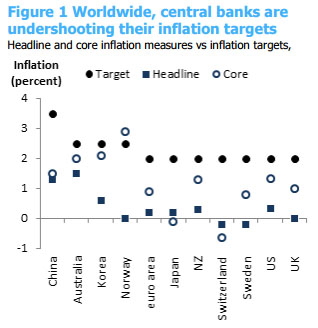

"These supply shocks are becoming more prevalent. That means inflation is low globally"

The shocks you mention are not impacting inflation significantly, debt, lack of wage increases, expensive energy and non-tradeable inflation are far more important. The items you mention would in effect reduce overheads on the input side, except they are countered by the last two I mention.

Yet more dont lower interest rates, So the argument goes that GDP is strong so we dont need to lower rates, utterly missing that critical sectors are suffering and deflating and if they tip over we will cause a recession. On top of that I suspect that GDP is actually make believe, I just cannot prove it yet.

"away from target as temporary factors" it isnt, its permanent, that is peak oil for you.

Excellent, back to effectively targeting full employment, instead of 6% unemployment, which is just pathetic and cruel.

They just need to figure out how to stop the tendency of unproductive debt to expand to the limit the population can afford and she'll be sweet. Hopefully they have heard that nearly all debt in NZ is unproductive and only serves to push up the prices of houses so more and more can be lent against them, thus enriching overseas lenders and impoverishing kiwis. Er, they do know that, don't they?

LOL, nice one.

If you keep targeting something long enough, & keep shooting it as it struggles to its shaky feet, eventually.... It dies dead.

Demand Inflation is now dead.

Apart from major city houses. And rates. And insurance.

... and fruit & vegetables (+4.9%), cigarettes (+12.6%), rates (+5.2%), package holidays (+6.7%), primary & secondary education (+4.7%), real estate services (+6.1%), "electrical appliances for personal care" (+8.5%), newspapers & magazines (+4.4%), postal services (+3.3%), bicycles (+5.5%), furniture & furnishings (+6.1%), along with 23 other items with rises between 2% and 3.99%.

Really? So how is inflation at only 0.4%? Must be some massive decreases in other goods & services.

Petrol Down, dairy down, overseas airfares down, ACC levies down, Car rego down, telecomms down, etc

Gotta laugh.

If 10 yr bond yields move higher by just 25 basis points, the income received is wiped out by capital losses. Read more

and CPI is? so for all these there must be significant price drops elsewhere to see 0.4% inflation overall.

So care to explain how those sectors seeing < 0% are doing just fine? and that unemployment is creeping up but thats OK?

Not since pre WW2 have we seen global tensions like this rising, economic ( money printing), political (climate changers), religious ,growing wealth gap,privately owned media propoganda, corruption, globilization. A perfect storm.

Indeed this year so far there have been 31 hurricanes, a record I believe.

Buy me a Tui.

"no major hurricanes, defined as Category 3 or above, have struck the continental U.S. in a record-breaking 119 months, according to hurricane data kept by the National Oceanic & Atmospheric Administration’s (NOAA) Hurricane Research Division (HRC) dating back to 1851."

http://www.cnsnews.com/news/article/barbara-hollingsworth/119-months-hi…

Indeed however you cherry pick again....ie when we talk about global warming / climate change its global, not an area.

Hurricanes striking the US are easy to measure/record and the record goes back to 1851 so it is good measure of the state of play. Just because you can now pick up hurricanes that never hit land with a satellite doesn't mean there are more hurricanes around. But no doubt green ideologues will milk it for all its worth - there is a gravy train to support after all.

" based on careful examination of the Atlantic tropical storm database (HURDAT) and on estimates of how many storms were likely missed in the past, it is likely that the increase in Atlantic tropical storm and hurricane frequency in HURDAT since the late-1800s is primarily due to improved monitoring."

http://www.gfdl.noaa.gov/historical-atlantic-hurricane-and-tropical-sto…

Except you can profile the amount and size of events for some decades and more accurately. From that you get a trend. On top of that since you are only considering the US you are ignoring hits on other countries which have been devastating. So at the very least you should be considering all landfall events globally. However the more area you consider the more noise is removed and the better trends are indicated.

Aren't we going to need large inflation in the future to manage the Auckland house prices? Inflation and wage growth should be around the same amount, but when house inflation in Auckland has risen so much, something is going to break. Or you are going to get 10-20 years of no house price rises in Auckland, or worse, prices drops.

The tools also should be looked at. Interest rates are at best a blunt and indirect tool, with all the wrong incentives on saving and asset bubbles alluded to in the article. There are other more direct monetary and fiscal tools that could easily be used, with constraints on which tools and how much still controlled by an independent central bank.

The thinking is rather deficient. Inflation is a part of GDP in the first instance, so it is getting counted twice. No understanding of the link between resources and growth either. The suggestions no better than the current regime. All that is controlled is the peaks and troughs, but the trend lies beyond central control.

Agree, in fact worse...

In terms of shocks whats suggested seems to be a slower but bigger response? which suggests less stability and not more. So if inflation is an early indicator it allows RB's to move in a reasonable timeframe, this "new" method suggests not. Also GDP seems to be "false" so as an example you would need to extract the debt component to get a NET GDP, this seems a lot of effort for no real gain.

I do agree inflation targetting is now probably somewhat pointless, mostly because it is done with such large blinkers and the wrong target, ie CPI when we should be using core which takes out energy.

Why do right wingers want to collapse the economy?

Seems what ever the outlook the far right wingers want the OCR to go up, I cannot fathom why myself except to collapse the economy into a mega recession and cause huge losses, a very strange wish.

Really...??? Right wingers want to crash the economy...

There is no such thing as a free lunch....

In an economic world that runs on Credit...the Business cycle is a "natural" thing..

Recessions are actually healthy.... they clean out the excesses of the previous boom..

In your world you could well manage things to avoid a recession.... and then the next recession...and maybe the next....

BUT.... what you are doing is kicking the can down the road..... You are creating the scene , the recipe, for a much bigger shock and maybe a depression.... much greater pain..

How would you manage things Steven...??? Would u try to do away with recessions..???

By setting interest rates too high, yes the evidence is it will crash the economy. What we do see is as banking regulation has been removed the finance sector has created a monster, this is the issue.

"clean out" actually there is little evidence? that it is excesses that are cleaned out but simply otherwise good businesses can go tot he wall due to external factors principally financial misdemeanour's.

"next and the next" in a grow for ever model that may indeed be possible or at least mitigate the worst. of course we are on a finite planet and have past peak oil so now we shrink. The can kicking is that we are ignoring expensive energy causing recessions, a fact we cannot avoid by substituting debt (which is a call on future energy that isnt there)

In an infinite world yes I would attempt to mitigate recessions and regulate excesses. The thing is the financial excesses is what is really multiplying teh damage of expensive energy and its going to kill us and fast.

--edit-- I dont know that they want to crash the economy (though that is possible), however the actions that they want to undertake ie basically raise the OCR will have that effect IMHO.

It's not really about right and left, that's a distraction to fool us all. It's about creditors (finance) and debtors (industry). The financiers hold that all debt is equal and must be repaid. In fact, most of it is predatory lending to us gullible types and serves no useful purpose. To maintain a veneer of respectability the financiers do lend some to viable productive projects.

I don't think finance is bad, it's just a technology that has become widely misused as a wealth transfer mechanism from the poorer 99.99% to the very richest 0.01%. I read somewhere that maybe 40 individuals worldwide control 50% of the world's wealth (eg King of Saudi, Putin), unfortunately the link escapes me. The Saudi King is estimated to be worth $1.5 trillion. It would be interesting to know exactly whose pockets those interest payments on the mortgage actually end up in.

Yes you are more accurate, the financiers seem to be invariably hard right wingers and the left plays no part really but its probably a better distinction.

Last para, yes very much, I think if we on main street could see how this works and understand it we'd have a revolution tomorrow.

Seems to me that income targeting as a monetary policy framework is just "tweaking" the monetary system.... a flawed monetary system...

They are doing this because of the obvious disconnect between inflation and Monetary policy..

( ie. the forces of deflation are global and beyond the Reserve Banks power to influence)

Basically they are advocating for nominal growth thru Credit growth... growing by debt.... which is how the western world has had such incredible growth since WWII.... and which resulted in the GFC., (which is essentially a Global Debt crisis..)

We still end up in the same place as with inflation targeting.... with some kind of debt crisis and some kind of 0% interest rate ( zirp ) and our own version of QE..

The model of economic growth thru credit growth has within it , as Ray Dalio shows, a larger debt cycle which ends in a deleveraging phase which , if it goes badly, becomes a depression..

Yep. Well written up.

The main thing putting it together is it strikes me as yet more smoke and mirrors from the right deluding themselves and us that all is well a little longer. However in the real world main street is suffering which is why we are in this mess. All this does is is make yet another excuse for the suffering and contraction to continue which will make the coming depression all the more certain and bigger IMHO.

At last, some questioning in NZ of inflation targeting. Others have been doing so for quite some time. Thus,the Nobel Laureate Paul Krugman gave a speech to an ECB conference in May '14 entitled,"Inflation Targets Reconsidered." Karl Whelan of University College Dublin wrote a paper: "A Broader Mandate:Why Inflation Targeting is Inadequate".

To be fair,there was an article inMay this year from David Hargeaves,the first sentenceof which was "Is it time for a comprehensive overhaul of the RBNZ Act 1989?

Even rank amateurs like myself have been questioning the orthodox line on inflation targeting for quite some time.

Interestingly Singapore has always targeted the exchange rate via a currency board - not interest rates which would be a mistake as lectured to by a Singaporean taxi driver recently.

They run a current account surplus of US $ 70 Billion - we after 45 consecutive years of C/A deficits

run a deficit of ~ US $ 5 B and as a consequence are moving to a sharecropper society as tenants in our own land.

Investing more than you save for long periods of time is not without consequences.

This can only be financed by borrowing or assets sales given we have forgone the QE route which may have made good sense when the NZ $ was at 0.88.

Occasionally it pays to reflects as to which is the better outcome.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.