By Bernard Hickey

New Zealand has changed an awful lot over the last 30 years, and mostly for the good, but not for everyone.

Anyone born since 1985 has seen their incomes grow much slower than their elders over the last decade, and have missed out on the massive capital gains that landed on anyone owning property over that period. They grew up during New Zealand's worst recession since the Depression (1990-1992) and graduated into the recession in and around the Global Financial Crisis. The percentage of children living in poverty has almost doubled from 15% in 1984 to 29% in 2014, according to the Child Poverty Monitor run by the Children's Commissioner and Otago University.

Meanwhile, those who owned or bought property, particularly since 2000, have done extraordinarily well, and their incomes have risen much faster than those that followed. Household assets rose by over NZ$800 billion to over NZ$1.1 trillion over that period, driven largely by a NZ$700 billion rise in the value of houses, but the vast bulk of it went to those aged over 35.

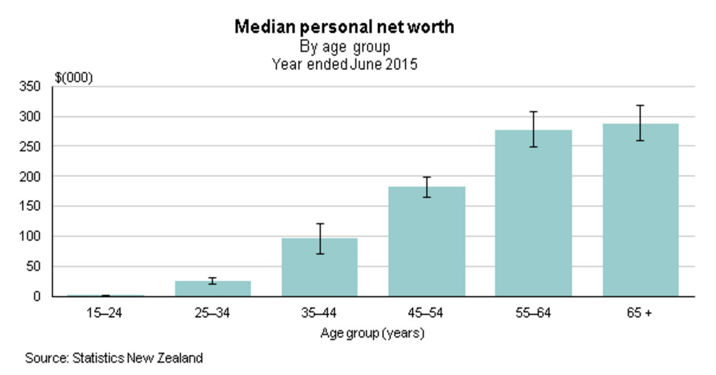

Statistics New Zealand reports the median net worth of people between the age of 25 to 34 was NZ$26,000 in the year to June 30, 2015, and this cohort of 576,000 people had a total net worth of NZ$55.1 billion. By contrast those over the age of 35 had a net worth of NZ$993.4 billion at the end of June 2015. Statistics NZ doesn't have figures for the last year, but house prices have risen 15% and the stock market has risen 20% over the last year, suggesting that group is now worth well over NZ$1.1 trillion. That means the over 35s, the generations born before the 1980s, are worth more than 20 times that of the youth of today.

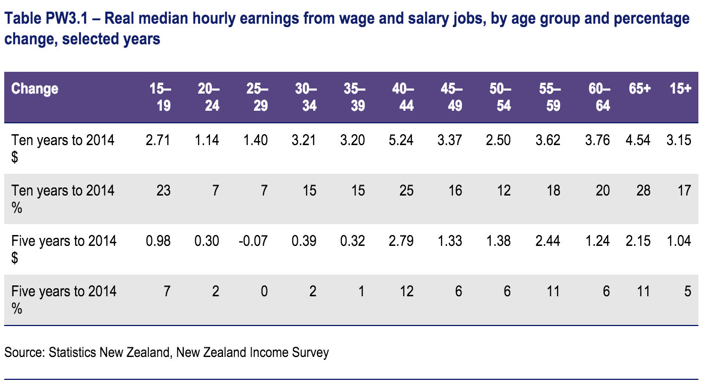

That's the wealth story. The income story isn't quite as unequal, but those over the age of 35 have also fared much better than the young, particularly over the last 10 years. Statistics New Zealand figures show real median hourly earnings from wages and salaries rose an average of 3.7% per year over the 10 years to 2014 for those over the age of 35, while those under 35 saw their wages rise by 2.1% over the same period. That means wages for those over 35 rose 76% faster than those under 35, and that growth has accumulated. Average weekly incomes for those over 35 rose by between a third and 55% over the last 10 years, while those under 35 saw their incomes rise by less than a third.

Some of the faster growth for older incomes and the massive rise in wealth for the over 35s was accidental. The over 35s grew up in the relatively prosperous 1960s, 1970s and early 1980s when unemployment was low and there were much stronger social safety nets from which to start their lives and families. They were well established in their jobs when the recessions hit so were less likely to lose their jobs. The new entrants to the workforce had it much tougher over the last 10 years than those already locked in with career paths and well-stocked Linked In profiles. Those owning property were also the accidental beneficiaries of a doubling in house prices because of high net migration, falling interest rates and restrictions on land supply for housing -- none of which could be blamed on policy-makers at the time.

But there have been some deliberate policy choices that are blowing apart the gaps in income and wealth between the generations, starting with New Zealand Superannuation. In many ways it is a fantastic system. It is simple, fair for those over 65 and encourages many to keep working, unlike those of many other countries. But it does have a couple of in-built expanders of inequality between the generations. The payment is adjusted in line with average wage growth, which is much faster than inflation and faster than wage growth for younger New Zealanders. It's also much, much faster than those on other benefits. Average weekly incomes for those over 65 rose 55% over the last 10 years because of that adjustment and because more are working beyond 65, while those aged 20-29 saw their incomes rise 30% because they are more likely to be unemployed or working on the minimum wage.

Then there's the issue of who will pay the New Zealand Superannuation bill for the baby-boomers. Over 500,000 people will turn 65 and start receiving the state-funded pension over the next 20 years. Those payments will come from taxes paid by people working over the next 20 years, which will predominantly be those aged under 35 now. Sir Michael Cullen knew this and so set up both Kiwisaver and the New Zealand Superannuation Fund to help 'pre-fund' the retirement burden so that when big payments started being made there was some money to help today's young pay that bill.

Unfortunately, the Government decided progressively over the last 7 years to reduce the incentives for KiwiSaver and to stop making contributions to the New Zealand Super Fund. The fund quietly reported this week that had the Government kept making contributions since 2009 the fund would now be worth NZ$50.6 billion, which is NZ$20.5 billion larger than it is now. The Government chose not to borrow NZ$14.7 billion over those seven years and hand it on to the fund to reinvest. That meant today's under 35s are missing out on at least NZ$5 billion of money that would have earned over and above the debt incurred if the Government had continued borrowing to invest. That loss will compound in the years to come, further increasing the burden of New Zealand Superannuation.

The Government has also chosen not to tax the gains on the hundreds of billions of housing wealth that fell into the laps of those aged over the age of 35, which is helping to fuel a further widening of that gap between the generations.

Those aged under 35 face a future of very expensive housing, mostly likely as renters, much lower net wealth as they approach retirement and having potentially to pay higher taxes to keep paying the pensions of those retiring with well over NZ$1 trillion in assets.

It's not fair and no one is doing anything much about it.

A version of this article also appears in the Herald on Sunday. It is here with permission.

58 Comments

Mist migrants come with senior peple - parents and tax payers have to pay for their retirement. What is their contribution to NZ to get tax payer money.

Statistics?

I don't think that's true. I possibly know more than 60 immigrants in NZ. Only one Korean brought his mother here.

Quelle Surprise

During the past week, we reflected on recent comments about John Key's 2007 pre-election campaign announcement how housing and house prices were in a state of crisis, and if elected he would fix it. Then in 2016, as Auckland house prices passed the magic $1 million mark, John Key waves it away with "that's not a crisis", that's called success

Now, one would expect a hungry news-media to rip into that and pillory the prime minister and relentlessly beat him over the head with it

If this was Australia, their news-media would be having a field day, and dining out for a month on it

But, reliably, almost predictably, Bernard Hickey pulls out the hoary old perenial "Bash the Baby Boomers"

Great comment iconoclast. Nz media are scared to upset key...they are as useless as the opposition

Timelines :

Key 2007: At 1/2million auckland house prices were at crisis level

Under his watch prices have increased by 500k...more than all other PMs combined

Key 2016: Now at 1m auckland prices are a sign of success.

Lets remind everyone

http://www.scoop.co.nz/stories/PA0708/S00336.htm

John Key MP

Leader of the National Party

20 August 2007

Speech to Auckland branch

New Zealand Contractors Federation

Conclusion

Over the past few years a consensus has developed in New Zealand. We are facing a severe home affordability and ownership crisis. The crisis has reached dangerous levels in recent years and looks set to get worse.

This is an issue that should concern all New Zealanders. It threatens a fundamental part of our culture, it threatens our communities and, ultimately, it threatens our economy.

The good news is that we can turn the situation around. We can deal with the fundamental issues driving the home affordability crisis. Not just with rinky-dink schemes, but with sound long-term solutions to an issue that has long-term implications for New Zealand’s economy and society.

National has a plan for doing this and we will be resolute in our commitment to the goal of ensuring more young Kiwis can aspire to buy their own home.

It’s a worthy goal and one I hope you will support us in achieving. Thank-you.

It is not just John Key who has failed but also Rodney Hide and ACT. They had the opportunity to do something good by re-orientating our economy from wasteful investment in pumping up existing house prices to investing in actual productivity. Instead Rodney just says inconsequential things on that rentier excusing rag the NZ Herald.

Rodney's biggest opportunity to change our economy was to reform Auckland to make it a better and more affordable city. His Super City reform completely failed in this. It wasted years arguing over planning alignment to create the Unitary Plan. Time Auckland didn’t have -now the city is plagued with equity problems -some of the most unaffordable houses in relation to workers incomes in the world, a homelessness problem we have not seen for almost 100 years and an economy teetering over a huge property bubble.

There was a simple supply side reform (because that is all National/ACT believe in) -a housing affordability national policy statement for the RMA. This could have been implemented at any time in the last 8 years to make the housing market work more equitably. Even now the right refuse to implement this -voting against it in parliament. Julie Anne Genter explains the conditions which the Green Party would accept this policy proposal and David Parker explains the policy.

Julie Anne Genter http://www.inthehouse.co.nz/video/45200

David Parker http://www.inthehouse.co.nz/video/45201

For John Key/National and ACT/Seymour this exposes their lack of principles. They do not want market reforms which would increase equity. For ACT and National market tools are only useful if it benefits the wealthy elite.

The fact that Rodney refuses to talk about this -shows how malleable his principles are.

Also - during the past month - another foot-in-mouth blooper

Remember, often said, and repeated ad-nauseum, Foreign Buyers comprising only 3% of buyers are not the cause of Auckland house price increases

When the $1 million mark was passed, the drum beats began clamouring for a 15% Canadian Tax on foreign buyers John Key squashed that, saying such a tax on foreign buyers would have a catastrophic effect on Auckland house prices and we can't do that

Both statements cannot possibly be true

Lot of foot-in-mouth bloopers coming back to haunt JK

Quick - get on the phones, pull out the old "Bash Baby Boomers" press releases

An in depth NY Times report claims:

In Australia, China’s

Appetite Shifts From

Rocks to Real Estate

China’s breakneck growth fueled an iron ore boom in Western Australia. Now,

Chinese investors are fleeing a cooling economy by investing in Australian homes. Read more

essential reading - the NY Times article is dated 24 Sept 2016 - yesterday

The bust happened 3 years ago - that's why you have to see what's happening on the ground at the time - you only get to read about it 3 years later

Yet house prices have fallen nearly 10% in Perth.

All of various National governments' constant faffing around with superannuation schemes, which were mainly instigated by Labour, has brought these particular chickens home to roost.

Lets also not forget the 100 billion of debt foisted on us by the sound economic managers of the National party over the last eight years.

It's a disgrace people still vote for these clowns.

And the Left leaning Mayor Brown of Auckland.

I don't understand your comment. Are you claiming Len Brown also bears responsibility for the massive government debt?

Any chance that over 35s could have more wealth in general because some of them have had over 10 times as many years of working life ( years over 21 )? Also note that the later years are the ones when they are worth the most due to experience.

Many many thousands of young people will be waiting for their inheritance as we speak, which if Mr Hickey had his way, would be much reduced by taxation.

Think you might find the likes of Ryman, Bupa etc first in line these days

Thats if their money isn't tied up in trusts etc.

They are a cunning bunch these oldies,took everything and want to hold onto it.

That's what I told my old Dad - you can't take it with you.

He said "if I can't take it with me I'm not going to go".

Didn't work out like that; he's gone and the finance company spivs got the money.

That's a shame, I am sure you would rather have seen his will read "Haha I spent it all" than that outcome.

I'm in my early sixities and waiting. I built my own working life instead and retired early from it when social engineering undertaken by the few on behalf of the not so fortunate many overwhelmed my sense of justice. The appointment of the Blair UK government in 1998 consolidated my thinking. Today's national government is hardly different in it's execution of outcomes.

What needs to happen is exceedingly simple; we must allow truly free markets or pull down the curtain and render unto full socialism. We cannot hide it any longer, and though there is much to legitimately fear over the latter I am still at this point confident enough that showing the full face of monetary socialism will be enough to finally tip the scales back toward the former (and sufficiently so) by first setting straight a great about what has been wrong all this time. History is not linear but cyclical, and the pendulum has swung very far in the direction of monetary socialism, a fact easily demonstrated just this week in both what one central bank did and what another did not. Read more

It is noticeable, in an election year, the entitled in the US have drawn upon the resources of the state to fool the people prosperity awaits them, given the right choice.

Leading the Credit charge – once again - was the federal government. Federal borrowing jumped SAAR $751bn, down from Q1’s $852 but still the strongest Q2 borrowings since 2012. Federal expenditures rose to a record SAAR $4.137 TN, up 41% compared to pre-crisis Q2 2007. At SAAR $3.470 TN, Q2 federal receipts were up 30% compared to Q2 2007. Deficits have this year been running at the fastest pace since 2012.

Also keeping quite occupied in Washington, GSE holdings jumped SAAR $348bn. This was up sharply from Q1’s $9.9bn growth and Q2 2015’s $70.9bn. GSE holdings enjoyed their strongest quarterly expansion since Q2 2008. The second quarter saw FHLB (Federal Home Loan Banks) Loans increase SAAR $168bn (up from Q1’s $51bn), the biggest quarterly growth since Q3 2008. (Worth noting from FHLB financial statements, Advances to Member Banks expanded almost 9% in the year’s first half to $690bn). Again, Like Old Times.

Total Agency- and GSE-backed Securities expanded SAAR $581bn (GSE debt $422bn and MBS $159bn) during Q2, up from Q1’s $60.4bn and Q2 2015’s $216bn. Here as well, Q2 saw the strongest expansion in GSE Securities since Q3 2008. For perspective, GSE Securities increased $293bn in (bond crisis) 1994, $474bn in (Russia/LTCM) 1998, $593bn in (Y2K) 1999, $642bn in (tech crash) 2001 and $547bn in (corporate Credit crisis) 2002. The big buyers of Agency securities during Q2? Money Market Mutual Funds increased GSE holdings by SAAR $403bn during the quarter. ROW snapped up SAAR $104bn.

Riding a nice GSE tailwind, securities finance enjoyed a banner quarter. Federal Funds and Security Repurchase Agreements increased SAAR $627bn, the biggest quarterly increase since Q1 2008. This reversed two quarters of Repo contraction, in what has been extraordinary quarter-to-quarter volatility. Funding Corps expanded SAAR $27bn during Q2, increasing one-year growth to $233bn, or 16.8%. Read more

The day the bubble bursts , the fortunes of those baby boomers will evaporate faster than Mayor Brown's political life after being caught eating a little Chinese ...

... and we come back to Gareth Morgan's contention , that our taxation system punishes workers and business owners ; but rewards property investors ....

If you remove property from the wealth equation Bernard , how much capital do older generations really hold .... are they really so rich , once their $Million Auckland houses are excluded ?

"The day the bubble bursts , the fortunes of those baby boomers will evaporate faster than Mayor Brown's political life after being caught eating a little Chinese ... " Along with everyone else's kiwisaver "fortunes".

.. and we come back to Gareth Morgan's contention , that our taxation system punishes workers and business owners ; but rewards property investors ....

Yes, but let's not forget neo-conservative (crony capitalism, balanced budgets etc) ideology in this mix.

The genius of the austerity narrative for two or three years after the crash was that it sounded quite fun, a Blitz-style project that would both unite us and remind us of what was really important. Yoked to the donkey that was “big society”, it was supposed to be exciting to cut social security and pare back the shared resources of the state. It would give us the space to show how much we really cared for one another. Community spirit, in this frame, had been crowded out pre-2007 by too much generosity from the centre.

It was always nonsense, as many of us politely noted from the start, and should never have been called austerity but rather a redistribution from the poor to the rich. As the years of belt-tightening have made life less liveable, the social landscape has come to replicate an unhappy marriage: what were previously points of difference – were you more or less concerned with sovereignty, more or less happy about immigration, more or less international in outlook? – have hardened into positions that are completely irreconcilable. Read more

https://www.youtube.com/watch?v=Xe1a1wHxTyo -

Four Yorkshireman - who would think thirty year' ago we would all be sitting in our 1 million properties drinking champagne for breakfast.

You try telling that to yoong ones today, you think they believe you?

Bernard, why do you not use some common sense?

See - Statistics New Zealand reports

What this says is that "The longer you owned your house the more the equity you have and that is unfair"

Because you finish up saying

That means the over 35s, the generations born before the 1980s, are worth more than 20 times that of the youth of today.

So let us look at this

If i bought a house in 1975 and you bought a house in 2010 then we should both have the same equity

Hahahaha

No wonder the country is in a mess just look at the people that get elected

See Fridays Top 10

Just look at this complete moron following stupid orders like a robot. And he wants to become Mayor.

You can also see it here

https://www.youtube.com/watch?v=_PktVoSDrHI&feature=youtu.be

My God no wonder the country is in a mess.

The new norm seems to be the parents have to downsize to help their offspring.

... that's the best idea I've heard all day ... I've seen that reality TV show from America ... " Little People , Big World " ...

If more parents were unselfish , and downsized into becoming midgets , they'd save a fortune ... to help their offspring ...

... they could buy kids clothes for themselves ... live in tiny homes .... gosh , even a dog-box would look like a spacious bungalow when you're less than 4 foot tall ... ... and how much does it cost to nourish a dwarf ... the little tykes would be a doddle to feed cheaply ...

Where to start. Bernard just think. If Banks print money - and they do, 93% of all money in circulation has been printed by the Banks - the Government can print money to keep universal superannuation going. The damage the Banks do by printing money is because they virtually only lend it on one product - real estate and that is how inflation in the property market occurs. Now by printing money for super annuitants that money circulates into the general economy. It doesn't get fed into one product the way the Bank money does. It is not rocket science for gods sake. The other day I worked out how much the house I bought in 1971 would be worth one hundred years from that date. The price then was $21k. In 2070 years it will be around $58m. Do you think the average annual wage will be around $19m in 2070. I don't

Patricia - well spoken. It is all about who controls the money and its supply.

At the moment it is private banks, not the people or the government who control money - Crony capitalism

Bernard complains that those over 35 have 20 times more wealth than the generation from 25-34 years old.

But with 5x more people in the older age group, who have worked on average 5x more years, and in more senior positions, they should have well over 25 times more wealth - not just 20 times.

So Bernard's figures show us the younger generation are accumulating MORE wealth PER YEAR in junior positions, than the older generation have over their whole working life.

To compare the wealth of cohorts but fail to factor in that one cohort is 5 times bigger, and has been working 5 times longer, would get you a fail at primary school maths.

Okay then, now chuck the most important asset you can own into the equation, just that, none of the other things, education, relatively higher wages etc - go on I dare you to, and see how things compare. The simple truth is staring us in the eye, the younger generation is finding it much, much more difficult to house themselves and thus get ahead.

I am a boomer, but I am becoming very ashamed of my fellow boomers who seem to be scratching around for anything they can salve their conscience with.

PocketAces - The blame game is what you are all about. Let us not find the real cause let us just blame some of the people,

We KNOW the real cause, it is foreign money, either in the form of outright, not living here foreign or immigrant money. Those on the right side of that equation ie existing homeowners and "investors" are making any excuse they can for no change in legislation that might compromise their capital. Sod those behind them.

As far as I am concerned the price of housing should reasonably reflect what can pay for it, where it is, not somewhere halfway around the globe.

Houses are ALREADY in the equation.

People continually confuse the Auckland housing problem with a New Zealand housing problem.

Over the last 5 or 10 years, plenty of places have had house prices go up by LESS than inflation. i.e. Napier, Invercargill, Palmerston North, Whangarei, Dunedin.

In these places it's EASIER to buy a house now than 5 or 10 years ago, and most of these places have lower unemployment than Auckland. i.e. the whole South Island has been under 4% unemployment for years.

You can easily buy elsewhere (well some elsewhere's) on Auckland's wages, however, it is becoming a much different story if you are limited by what you earn by living where the houses are

There are numerous places in NZ where -

- house prices are reasonable

- unemployment is much lower than Auckland

- quality of life is much better than Auckland

Photonz1 - in stating that wealth accumulation is mostly a factor of time, aren’t you missing Bernard’s point that there has been a significant structural shift in relative incomes for younger vs older people, especially given it is harder to assume investment risk without income or existing equity to leverage off?

Also – wealth does not accumulate in the linear fashion you suggest. There are windows of opportunity to make significant gains and periods of time, sometimes extended, where wealth accumulation potential is lower. If an age cohort happens to coincide with one of these flatter periods, capital gain will not be as available to them compared with those preceding (or perhaps following) them.

For the passage of time to address intergenerational wealth discrepancies, you’d have to assume the same potential to accumulate exists in a roughly consistent fashion across all time periods (leaving aside inheritance). While it has in the past, it is quite possible that present pricing barriers to home ownership and low real inflation are driving a permanent structural change to previous wealth accumulation patterns, that time alone will no longer fix.

Bernard's figures show that young people today are accumulating more wealth per year of work right at the start of their careers, than the baby boomers have over their whole lifetime.

It doesn't show any structural shift. It just shows what has always happened for centruries - that each generation is going to be wealthier than the previous one

yes I saw that stat: 20 times more wealth than an age group spanning 9 years vs. the rest of the working population, remembering that much of that wealth be transferred to this working group when they inherit....anyway from the start I knew this was a hit job story....I remember sitting on a 12 foot tinnie fishing with a few buddies about the time Bernard had sold up and left to Wellington, thinking how he gets things so wrong as I was actively buying multiple properties in Auckland at that time....what amazes me is that he gets published in the NZ herald as some sort of authority....to mention the super fund not gaining 20 billion is always 20/20 in hindsight...if anyone should know Bernard should...

Wasn't Bernard one of those at the time of the GFC telling people they would have to be insane to borrow money to invest in risky assets like equities?

I don't think what we are seeing in property is economic growth. Is the problem that there is too much debt issued as bonds and the bond market has peaked. Investors are starting to wonder if bonds are safe? Can the debt ever be repaid? So get your money out paper assets and into physical assets like property. But then what do you do when your housing investment has values that are becoming ridiculous? Who will buy your property when it peaks and if you sell where do you invest? I think value that's being printed could vanish as the distortions increase. The establishment that run the world are trying to hyperinflate the debt away, but people on the street are starting to think that the system is rigged.

JK 2007 "It's the housing Stupid"

JK 2016 " Look, um......."

Shame about losing the 20 billion from the superfund... luckily we hav'nt built up huge debt, and still own all our assets.

Wow, a comment all the way from a parallel universe? How's the weather over there, wherever you are?

WOOSH! right over your head

Woosh, right over your head.

Bernard - If you bought a house 30 years ago, and now, after that 30 years, you are mortgage free. Answer this question.

"How much did you pay the bank over those 30 years?"

Lets take a look

Using today's money

We pay the bank, say $2000 per month for 30 years. That is $720,000 the bank gets paid.

Now the house is worth $1 million so i have made $280,000 unearned income over the 30 years. That is just under $10,000 per year.

AND how much has the bank made?

Further if i lived in any other part of New Zealand i would have paid the bank more than the house is now worth.

It has been the case for centuries that you end up paying the bank more than the house is worth.

Stop being one eyed and get your facts right.

You have just clearly demonstrated how it is that the upfront initial cost of a house and income at the time of purchase is the real determining factor of whether or not it is possible to purchase or not. If today's younger generation are never able to buy or have to wait till much later, then they, indeed, will never achieve the asset wealth that you did, even given the amount of interest paid to the bank over those years.

Perhaps another factor to consider is the amount of dead money (rent) a fhb will have to pay before they can buy anything at all, if at all. That might balance things up a teeny bit, maybe more.

Many of the commenters on this article miss the point. What Bernard points to here is linked to the articles a couple of weeks ago by John Mauldin (the first here) where economic policies adopted by Governments are based on theories that are at their roots, fundamentally flawed because the assumptions that they are based on are simply wrong! The young here have missed out because Governments have failed in their fundamental responsibilities by regulating to prevent market manipulation, protecting ordinary Kiwis, keeping basics affordable, and delivering reasonable lifestyles.

The government's role should just be law and order with maybe a tiny smudge of infrastructure and healthcare.

If we were all decent people, in fantastic life long health, who always considered the effect they might have on others before doing something, like, say, building something that completely blocked your neighbour's sun, then I would totally agree with you. We aren't.

Wrong! The Government's role is to ensure that people are not manipulated out of the market by the greedy. That successive Governments have failed is patently obvious. Housing is a classic example. IMHO house prices need to fall by at least 2/3rds to be affordable for average AKers, and rents the same. The RBNZ and other observers who claim the rules put in place are being effective are BSing themselves as the investors move away from AK to the regions for those capital gains. In other words the virus that infected AK has spread to the rest of the country. The only way to fix it is by regulation, but as we have seen no pollie has the balls to do for the most, against a few. In todays 90 Secs, the Chinese can do it to their own, why can't our pollies do the same?

Great article BH - hit the nail on the head. I see three ways out of this.

1. A massive increase in progressive redistributive taxation. Wealth tax, foreign buyers tax, a 45% top tax rate for those earning over 130K, ring fence property losses, increase the trust rate to 45%, inheritance tax... that should be enough to start with.

2. A massive increase in productivity. New Zealand should aim to overtake Germany and China as the global nexus of industrial production. That kind of transformation should raise lower and middle class wages just enough to catch up and avoid a complete breakdown in social cohesion.

3. A total breakdown in social cohesion; New Zealand will become like the United States. Islands of opulence in a sea of misery. We'll have to have a Geroge Orwell like surveillance state to protect the wealthy from the angry poor. A draconian militarized police force will be required to suppress discontent in poor neighborhoods, and a captured and complaint media will be required to give the appearance of democracy.

2. I guess you are figuring we get enough wind over a long narrow country to just blow all the pollution away

I see option #2 as the least likely to happen under any government. Option #1 is the least likely to happen under a National government. So I guess that leaves either a change in government or option number 3

Think we might have opted for that already tbh. There is monumental change coming, one way or the other, we are either going to breed ourselves out of house and home and take everything else with us as we claim more and more of the planet for ourselves http://maraelephantproject.org/ then we probably will blow each other to bits for a while until we've got rid of enough of us to start the whole pointless process of growth again.

I am just hoping (against hope, no doubt) that we can see through this intelligently and leave all the nutty stuff behind us, for once and for all, and live on this planet, complete with what we have managed to save in the way of other species, if only for our own souls.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.