There has been talk this week about debt-to-income ratios due to the Reserve Bank asking the Government to consider it as part of its macro-prudential toolkit.

At its simplest, a DTI rule would be that a borrower cannot borrow more than five times their gross annual income. The UK has applied a DTI rule for owner-occupied houses of 4.5 since June 2014. Debt includes mortgages and any other debts like personal loans, credit cards etc.

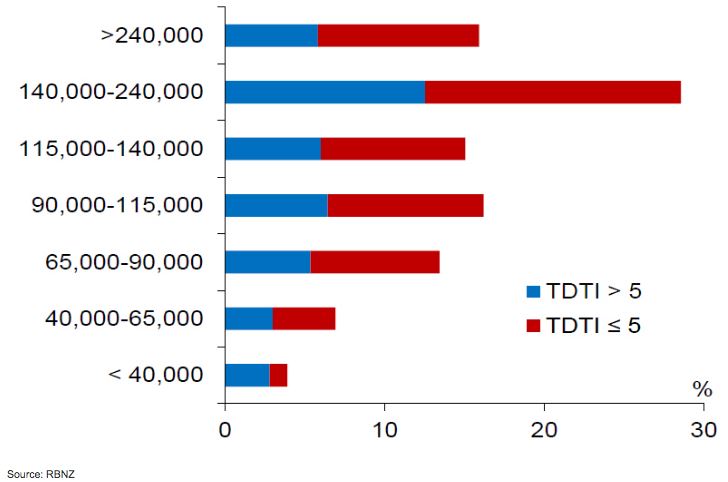

For the majority of our clients any rule around DTIs would have no impact. A Reserve Bank survey of our major banks last year showed that 74% of first home buyers are below a DTI of five and 63% of other owner-occupied. Arguably a DTI approach may allow the Reserve Bank to slightly loosen LVR (loan-to-value) restrictions for first home buyers, alleviating deposit requirements.

DTI by Income (Source RBNZ November Stability Report)

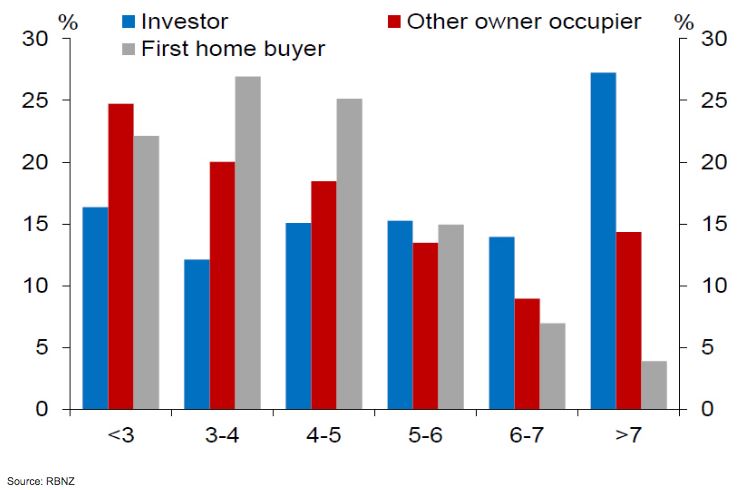

DTI by Borrower Type (Source RBNZ)

The tricky situation that doesn’t fit nicely inside the DTI box is maternity leave. If I have a client with one of the borrowers on maternity leave, they may be prepared to run a high DTI initially over the first 2-3 years. This is a very common scenario in Auckland where two incomes are often required for servicing and new parents are older. In these situations, a higher DTI might be reasonable but would sit squarely outside the rules as an unintended consequence.

Banks already apply servicing calculations to test a borrower’s ability to service their lending. These calculations use a mortgage rate of around 6.50% (compared to an actual rate of around 4.30%) and assume P&I over a 30-year term. Then there is the Responsible Lending Code which requires lenders to properly account for living costs. Between these, banks are already properly assessing affordability for first home buyers and applying a degree of conservatism.

It could be argued that the DTI is therefore a blunt instrument that is not about being prudential, It is either (1) nanny state – protecting people against themselves, or (2) the RBNZ doing the Government’s job for it in an effort to control house inflation. The Reserve Bank has had to step well outside of its traditional mandate lately to counterbalance a Government that in my opinion is too laissez-faire.

Where DTIs would work, is if applied to investors. Roughly 60% of Investors have a DTI over five. This is to be expected as investors can generally divert more income to servicing and therefore carry higher leverage. A retired investor could have a portfolio of $3m of investment property with $1m of debt and at a yield of 4% they’ have a DTI of eight.

My own experience is that high DTIs will be prevalent in the Asian market with there is significant equity but lower taxable incomes, and investors near or in retirement. Banks refer to these types of clients as “rent reliant.” It’s also a space where spruikers work encouraging middle NZ to leverage up to their eye-balls on property.

For investors a DTI is again a blunt instrument and I wonder to what extent it works better than the servicing tests already applied by banks. Banks use a mortgage rate of roughly 6.50% on a P&I basis and only include 75% of rents to allow for property expenses.

Bear in mind that the Reserve Bank has already removed the ability to use foreign based income for servicing (which was a smart move), and it has tightened up AML requirements making it near impossible for foreign nationals to borrow money in NZ. Both changes positively impacted on the issue of cheap foreign capital pouring into our property market, which has always been my main bugbear and was ignored for years.

Rather than pulling out the bazooka of DTIs I’d like to see the RBNZ use a rifle and continue to finesse the rules already applied.

As a starter for ten – property investors should not be able to include boarder income or rental income from their owner-occupied property for servicing. You’d be surprised how common this is. It’s these sorts of subtle rule changes that hit the parts of the market that are genuinely highly geared whilst not having unintended consequences elsewhere.

The banks have already demonstrated that they are on-board with this approach having rigorously applied the RBNZ direction throughout the year.

As I’ve noted in previous posts I think the Reserve Bank has already applied sufficient force to the property market, and this is still playing out. There is an increasing risk if they get their meddling wrong, it could create a liquidity trap. For some business owners caught out by the last set of changes, it already is.

From here I’d like to see more finesse and less sledge hammer, so we can avoid more unintended consequences.

John Bolton is the "Chief Squirrel" and CEO at Squirrel Financial Services. This article was first posted on the Squirrel Mortgages blog, and is here with permission.

58 Comments

Repetitious ,self serving, and frivolous. Why are mortgage brokers necessary . Worried about a downturn in mortgage volume ,less business, Bolton reveals his character.

What's exactly did he write that is self serving and frivolous? I think he makes a valid point about being cautious with DTI's. I've used plenty of mortgage brokers. They always get better rates than going to the bank directly.

"They always get better rates than going to the bank directly .' And your supporting evidence for this statement is ? Out of curiosity why the assumption of a DTI at 5. The mention of maternal leave is frivolous, the rest is self serving.

The supporting evidence is that they exist and are widely utilised.

If they didn't represent value, there would be none around. Simple.

It's just buy in bulk and pass on savings arising from effectively lower overhead costs on goods. You should be familiar with this notion by now..

Because that is what the RBNZ has used in its analysis on the NZ market. See their Financial Stability Report November 2015.

Have read many of the RBNZ financial stability reports, actually commented on them just last week including investor loans. The DTI of 5 that the RBNZ uses is for illustrative purposes only and they could equally have used 4 or 6 or indeed 3.5. What is disturbing is the amount of lending over a DTI of 5 primarily to 'investors' . No where does the RBNZ state what DTI multiple it would like to see introduced . Unless JB has been given copies of its release to the government , your claims of a DTI of 5 within your article have no validity. As you will be well aware , any reasonable DTI restriction will have a significant bearing on all mortgage brokers.

It is hard to prove that you get a better deal. I can tell you as a customer it is less hassle and they understand the banks credit processes so they can advise which bank best fits the customers situation. I've got better things to do than apply to every bank and then negotiate with each of them. I can say that I have done it both ways and I'll be using a broker next time.

wow. Cowpat what a brain fart. It shows real intelligence to pull the "mortgage broker self-serving thing out." Haven't heard that one before! I'm simply saying that DTIs are too blunt but have always been supportive of stoping house price inflation. Play the ball, not the player. How are DTIs not too blunt? What is it about the current rules (properly applied) that aren't working? The problem all along has been cheap foreign capital and I'd much rather see that being dealt with directly, incidentally which it is.

JB, there has not been a singular previous occasion that I would lower my four legs and stoop to a tiresome exchange, debating who has the larger intellect. ' I'm simply saying that DTIs have always been supportive of stopping house price inflation' your words , but we at JB Squirrel do not want them because our business model would suffer immeasurably and we would not be able to list on the stock market in 2017 . If it looks like a duck , swims like a duck quacks like a duck its probably a squirrel.

Totally agree Cowpat.

Not Rocket Science really.

Thanks for the article JB, as before for your previous articles, it is good to have your perspective.

It seems that we agree that DTIs , if set at 5 or so, will be effective without hurting FHBs who borrow responsibly.

I would further suggest that DTIs, set at the right level, will significantly benefit FHBs because:

- they will have a more even playing field relative to "investors".

- they will not have to compete with other FHBs in terms of the riskiness of their borrowing.

You state that DTIs will work if applied to investors. I suggest that they absolutely MUST be applied to investors, because it is that group which presents the greatest macroprudential risk to NZ's banking system .

You set out an example of a retired investor, with $3m of investment property, with $1m of debt, and a rental yield of 4%. It is clear that investor has taken on excessive debt, - a DTI of 5 would limit that investor to $0.6m of debt, which seems entirely appropriate given that the investor is retired. ( I note that the central bank of Singapore does not allow tenure of loans to investors to extend beyond 65 years of age).

You have stated your reasons as to why you think that DTIs are a "blunt instrument" and are "not about being prudential". I disagree. The impact of investors, who often leverage housing price rises into additional house purchases in markets with low elasticity of supply, is a huge macroprudential risk. Their capacity for mobilising huge quantities of credit is far above the capacity of any owner occupier. Even at current LVR limits (of 80% of owner occupiers and 60% for investors), the capacity for mobilisation of credit by investors is nearly 90% greater than for owner occupiers.

In short, aggressive negatively geared investors are a huge systemic risk to NZ's financial system, particularly now that it has a very high level of private debt. The benefit of appropriate targeted DTI limits will be to reduce this looming risk to NZ, with side benefits of limiting house inflation and giving FHBs a fair go.

Peri, your comments do not make sense. How can a retired person owing $1 million on a $3million dollar portfolio be excessive. Where is the risk? If the property market falls 67%, there will be more to worry about that a retired person going to mortgagee sale and the bank coming out at break even. Why can't this person have a $1 million dollar mortgage, when they want this loan and the bank is happy to lend. Hardly represents a prudential risk to the economy. I would also say that investors with an LVR at 60% do not risk a prudential risk to the economy. So the property market falls 40% and banks are at tipping point where they have to tip into their own pockets, what is the problem? And at the new LVR rates of 60% for investors I'm sure you will find that there won't be a lot of negatively geared property going forward. Adults can make their own decisions. So if these loans do not represent a prudential risk then it is simply nanny stateism, promoted by the usual jealous types who are always a day late and a dollar short. As they always think the sky is about to fall, cannot weigh risk and reward, and can't pull the trigger, because they are always waiting for the perfect pitch that never comes. Then they sit back and resent those who reap the rewards of decisions made when the future looks murky.

Thanks mja, a good challenge.

I was struck by the example of the retired investor at several levels: i) why a retired investor would have such a level of debt that he would get very little usable income (unless he has an interest-only loan which would be a separate worry), ii) why investors can get tenure of loans beyond their retirement age (contrary to good practice in Singapore); iii) even though as you point the investor has considerable equity and it would take a large drop in the market to be a risk, I am of the view that investors buying existing rental property with negative gearing represent a significant risk to the system.

However, perhaps I implied more concern than necessary for this particular investor's situation, but here is my concern in respect of an an investor with a portfolio at the LVR limit of 60% LVR, where prices are rising at 9% per yer:

- by revaluing and refinancing on his existing portfolio he can access credit at a rate of 5.4% of his portfolio value per year;

- by applying that cash to purchase of existing properties he can access at an additional 8.1% of his portfolio each year.

That is, his portfolio can grow at 13.5% (1.5x) when house prices are increasing at 9% per year. This means explosive growth of lending to the investor sector, as we have seen.

Only if the LVR limit were at 50% would the growth of the "investors" portfolio value be limited to the rate of growth of house prices.

It is this leveraged leverage effect that makes the investor activity so incredibly dangerous from a system perspective.

It is even worse when applied to a market with low elasticity of supply.

With an elasticity of supply of only 0.7 ( I think the Akl market is less than that), then the system is inherently unstable (explosive growth then bust) unless the LVR limit for investors is less than 40%, or we have a DTI applying to investors which achieves the same result.

Peri, the business model you are concerned about cannot happen on mass in the real world. Most investment property owners only have 1 or 2 houses. As JB states banks work off 6.5% interest rate and principal amortising over 30 years, the repayments P+I in calculations would be approx 8% of total loan amount. And if banks use 75% rents then if most cases, rents used would be 75% of about a 6% gross yield (less in most major centres). So with bank calculations using 8% P+I loan, and 4.5% revenue from rents, we have 3.5% negative cashflow in bank servicability calculations (because your model relies on no deposit and simple recycling equity as market rises). This is where the rubber meets the road assuming house 600K purchase fully using equity from existing portfolio, bank assumes P+I of 8% 48K, and rent revenue of 75% of 6% gross yield so 4.5% or 27K. So bank calculations show negative cashflow of 21K per annum, this is the reason most investors only have 1 or 2 properties (other reason is they buy in low socio-economic areas seduced by theoretical high yields, then chuck in the towel within 2-3 years as have a guts full with the tenants). I have experienced this first hand, I am a professional in my early 40s would earn 7 times the median wage have a free hold home and a property portfolio with LVR at about bang on 55% comprised of 6 brick and tile 10 year old homes all in 180-220sqm size, in Wellington region located in suburban decile 8/9 areas. Admittedly all would be under rented, but prefer low stress so don't raise rents on sitting tenants (most there more than 2 yrs). I have never missed a loan payment, but at this level of borrowing just over 2 million it is a real "s**t fight" to secure further funds. So I only see your model being applicable if people are prepared to embellish income etc, use multiple lenders, and in general act in a slightly dodgy manner. So are we really prepared to restrict the activity of citizens who act in an above the board manner, to restrain those who push the boundaries. Because those who push the boundaries in most cases will find a way around further regulation anyway.

Thanks for the feedback mja

Your example suggests banks are applying a DTI limit of about 12 (=1/0.083), so that your 600k example could secure a loan of about 324k (= 12x27k), equivalent to an LVR of 54%.

This illustrates how a DTI of 6 would be a very strong constraint.

I understand you see that would be unjustified. However given the fact of explosive growth in debt attributable to property investment, I remain of the view that more constraint is required.

As JB has said in a previous article: “ the idea was to buy, get capital growth and then recycle your deposit into the next property.” and

" Up until the RBNZ changes, it was possible to buy up to 3 properties at 90%. We had clients with multiple properties at 80% still able to buy the next one at 85% or even 90%"

Pri and MJA aren't you losing sight of the point made? A retired person borrows $1 mil against a $3 mil property. your scenario only seems to discuss that the loan is secured against an asset over the loan value. Isn't it more important that the person is able to service the loan? The value of the property may change, possibly radically so ultimately the value of the property may become moot. The risk, and most significant issue I see here that matches reality is that the banks have been banking (no pun intended) on ever growing property values as much as the investors. I suggest that they have even got to the point of lobbying to prevent any real measures that might actually have an effect to protect their own positions. the result has been at the significant cost of ordinary Kiwis.

Thanks Peri.

I agree around speculators being the problem. I don't agree that this investor is a risk to the economy.

There is no systemic risk at 33% LVR and to bundle them up with the problem would be wrong. As you point out the issue is being driven fundamentally by speculation. Blame market hype, immigration, councils, foreign capital, low interest rates and for a long time lax application of credit rules. This poor old bugger has probably owned property from well before the current crisis.

Even from an income perspective my "retired person" in the example could have it on a 5-year interest-only loan of 4.70% and roughly $60,000 of income net of costs which is a lot in retirement. They could sell one of the properties in 5 years time and be debt-free if they chose to but for now they want the income. I have a client like this with $5m of property and just over $1m of lending and his bank refused to lend him anything - so the current rules are hard enough!

Maybe it's not such a great investment, but we can't protect people from themselves, and we certainly need to be careful how far an unelected, unaccountable regulatory body can go into dictating people's lives. The RBNZ does an awesome job. (They've been forced to cover a Government asleep at the wheel and the market got away on them.)

How do we deal with small business owners under a DTI framework? If a business owner has a bad year due to poor stock choices or over recruiting, or not cutting staff numbers, does a DTI mean they cannot borrow against their house? The RBNZ would exempt businesses (in theory) but in practice there would be plenty of collateral damage here too. Do we care about small businesses and entrepreneurs? These people go for it. They don't sit on their arse waiting for the State to look after them. They don't complain and they take significant personal financial risk all the time. How do we view them? Is it ok if they are taken out by a sledge hammer?

We seem to all be ok with it when it is the evil property investor, but "the law of unintended consequences" reaches far, far wider than that.

As I said in my previous blog we haven't yet felt the full impact of what the RBNZ has already done to tighten credit markets which is quite extensive. We just need time to see how that settles in.

Many thanks for your response JB, much appreciated. Hopefully you might also better understand my perspective in my reply to mja above.

I do acknowledge the risk of unintended consequences, but you will see that I have strong concerns about the macroprudential risk of the investor sector who borrow, not to access income as you have now clarified, but borrow to leverage property price growth. I think some risk of unintended consequence is acceptable given the huge danger of unregulated credit to the investor sector.

In short, my only concern about the imposition of DTI on the investor sector is that the RBNZ will leave it too late.

DTI's are a blunt instrument. If one is being prudential, then there are 2 ways to do so. One is to have a high stable income relative to the debt and the other is to have a high level of equity relative to the debt and income which can service it (rental or other). The scenario of having $2m equity on property worth $3m provides minimal risk to financial stability and I would say less risk than someone earning $200k a year and has $1m mortgage on a house worth $1.25m.

DTIs are now an internationally accepted macroprudential tool, to be applied alongside LVRs. As the Treasury has said:” DTIs are particularly salient to financial stability as they are more reflective of sustainability of debt through the ability of borrowers to repay, and are less influenced by fluctuation in the asset prices (which bite at the point of sale) that LVRs are subject to”

The problem with LVRs alone is that values have already been pumped up to unsustainable levels.

I didn't say they didn't work but there will be undesired effects. The first round of LVR's blocked a bunch of first home buyers out of the market and robbed them of the capital gain they would have received and now they have to take on bigger mortgages as a result all in the name of financial stability.

No, easy credit and investor activity raised prices, and it is high prices which blocked FHBs, LVRs were a necessary (and overdue) response to constrain the cause of the problem: - easy credit.

Had LVRs been applied sooner FHBs might have had a fair go. If there has been robbery, it is robbery caused by easy credit.

The real reason house prices went up was because demand outstripped supply. Cutting first home buyers out of the market only helps investors as those people have to live somewhere. Some measures are needed minimise the risks to the system, but cutting out chunks of buyers to suppress demand is just benefiting those who already have made their money and have plenty of equity. Supply side measures are a far better solution.

You are right Dave

Most won't believe you on here because they want prices to crash!

They will flatten in Auckland but if they bring in the DTIs it will kill it for first home buyers

Prices will be supported by supply and demand. More people wanting land and since the supply of land is limited prices for land will go up. We can't all have 1/4 acre sections 10 mins drive from the CBD. You can argue that investors have caused the prices to go up. You can also argue that the RBNZ made them go up by lowering interest rates. You can argue the government made them go up by allowing first home buyers to access their kiwisaver funds so they had more funds available so they could spend more. It is too hard and too expensive to build a house so people trade the current stock. The more restrictions that are put in place the more the system will favour those who already have houses and money.

Hi John, can you explain why you think First Home Buyers won't be affected by a Debt-to-income limit, such as for example at the level you said the UK set being 4.5? Consider a young couple that are first home buyers with gross annual income of $100,000. Would they be able to buy a home with a loan of less than $450,000? This seems unlikely in Auckland where Squirrel operates. Interested in your thoughts.

Hey kermit

I think for a start RBNZ would set the DTI at 5 and there would be a buffer just as there is with LVRs. In reality affordability goes out the door above 5 so most home buyers can't buy at that level now. There would always be an exemption for Welcome Home Loans at the lower end of the income spectrum.

For a couple on $130,000 which is about the average we see in the City, that would be $650,000 of lending let alone deposit over the top of that.

I think currently more first home buyers are locked out of the market because of the LVR rule than would be by a DTI rule.

There are always going to be casualties as I mentioned in the article. The biggest impact will be on those with young families and only one partner working. This group is almost always at the upper end of the DTI spectrum and wouldnt be covered by Government policy exceptions.

I'm a fan of debt-to-income measures (and affordability), but would much rather see banks using their current more sophisticated assessment than a blunt instrument that cannot cater for the nuances of the real world. By all means tighten it up doing tweaks.

John, I live in Christchurch.

Had a family member living in Auckland a couple of years ago and he reckons everyone he knew up there was not earning much more than what they would in Chch if any.

You are the broker so I expect you know what incomes are for young couples in Auckland.

Seems to be excessive 130k for a young semi unskilled

couple in Auckland bearing in mind that they would want a child at some stage and therefore one wage perhaps so it would only be 65k.

This would,allow only 325k to be borrowed rather than the 650k, so I think you are wrong in believing the the DTI requirement at 5 wouldn't affect first home buyers.

Thanks for the comment.

The RBNZ graph (which was survey of the banks) shows only 30% of FHBers are above a DTI of five. With the noise around DTIs you'd think it was the other way around.

In the article in the first instance we are talking to clients, as it was from our web site, so not a standard demographic. Still, I do draw out young families in particular (due to drop in income) as being the group most impacted by DTIs if implemented.

Income wise in Auckland $130k is average for the FHBers we see. That's people capable of getting into the market under current rules. There are plenty of people in Auckland and NZ who cannot buy even under normal lending criteria. As I said in other comments, a DTI of 5 is already high even under current rules.

John, fair enough, still think that it will stuff first home buyers around the country.

Speaking from experience in finance and being a professional full time landlord in Chch.

I know from the tenants that we have in our properties, that they will not be able to buy in Chch at a multiple of 5 unless it is in a lower socio area.

A lot of people in Chch would only be on 40k and a couple say 80k would be able to borrow 400k and 20 per cent deposit they would need 100k.

Most would never save 100k on that salary anytime in their lives.

The median price of houses in Chch is totally flawed by the as is where is properties that have been sold in huge numbers in the past few years.

Yes there are a lot of 2 bedroom units in Chch but the first home buyers want far better than that and will continue to rent.

You forget that prices will drop as interest rates go back to normal levels. DTI's are coming. Get used to the idea.

Gordon, won't worry me one iota.

It is the first home buyers in Chch that I am concerned about because yes it will affect them.

Prices in the lower to mid bracket will not drop much at all in Chch if at all!

But then you have friends all around the country that will be telling you different haven't you?

Interest rates also won't move up much in the next decade either.

You are not worried about FHBer's The Boy. Like the brokers and agents you are worried that DTI's will finish off what LTI's have started. Everywhere in NZ investors and developers are already struggling to get finance. If you really worried about FHBer's you would not have your so called portfolio in Christchurch. I have to say that I am amazed you have put all your eggs in such a basket. We all meet people all over NZ who have left since the big quakes. You have plenty of land and your population is getting smaller by the week. Your so called portfolio would have to have more risk attached to it than my shares. No you are really scared, in fact I can smell the fear in your latest comments. The RB is coming. It is only when not if. The RB smells blood on the floor and is now going to go for the throat of you speculators. They will not make it harder for FHBer's. They want to make it easier for them. They work for the RB because they are bright. I presume you have never worked for the RB.

What about all the FHBs that have bought in the last year? Collateral damage?

In Auckland they have already lost equity. They were warned. Of course we all want it now. It will be interesting to see Octobers data. Agents in Auckland are not seeing the same action they saw earlier this year. Those who got in when it got frothy were taking a risk.

This is good news. We want to have a bit of a rest in Auckland. I would like to see a bit of a drop showing up in the October figures quite honestly.

Income wise in Auckland $130k is average for the FHBers we see.

Understandable given anyone/couple on anything less wouldn't be even contemplating becoming a FHB - and what percentage of the under 30s would that be I wonder? Seems to me that it is likely a majority of under 30s that simply aren't in the market in Auckland - at all.

In your example, a couple earning $130k pa would be buying a house worth up to $812.5k. That Mortgage would cost them around $3200 a month or $740 a week. Are first home buyers really signing up for that at those income levels? That is a lot to owe unless you have good potential for income to increase. It also makes a difference on how that income is split too.

Point is they wouldn't be able to borrow over 450k on that income currently anyway as wouldn't meet servicability requirements of most banks.

A few currently could claim a boarder income if they get the house, but as JB says this is dodgy as likely no follow up on whether they get the flatmates or not so shouldn't be included in calcs.

Personally beleive that investors with positively geared property is far safer bet for the Banks than owner occupied.

Owner occupiers tend to have more mortgagee sales than investors.

Owner occupier loses their jobs and don't get another whereas the investor can always get another tenant if the tenant doesn't pay but that has never happened to us.

The DTI system is crackpot really, it is far more sensible to have the ability to service.

In Chch for a buyer to buyer a home at say 500k with 20 per cent deposit they would need 400k and at a 5x DTI they would need to be getting 80k which not many are. Couples maybe but childless for long time or mother continues to work and kid in daycare and that has costs.

Great for landlords though as it will be easy getting tenants as the tenants will never be able to afford their own.

Can't see how it is going to work in Auckland at all.

Say reasonably basic house at 750k 20 per cent deposit so borrow needs 600k. You would need 120k income at the 5 DTI.

Seriously, wouldn't think there would be that many first home buyers on 120k maybe couples but they will be childless forever.

The solution is building more affordable houses in Auckland. I was looking at building a 5 br 3 bathroom house for around $1.15m including the land and everything else. If I built 2x 2 bedroom units on it I could have sold them for $650k each and made $150k but I wasn't allowed due to stupid rules. The same load would have been put on the councils infrastructure etc. This is why we have a affordability problem. New builds are not fit for purpose.

If National Government has decided come what may will not act and will protect speculators (so called Investors) and Non Resident buyers than someone will have to act.

Does RBNZ has a choice if the power has corrupt government.

RBNZ wants but will the government allows or will try to delay or manipulated has to be seen.

This is the trust people have of their government otherwise after announcing the intent ages ago what is it that Bill Englush is consedering.

Gordon, you are a delight!

Waste of time going over old ground as I acknowledge your jealousy!

That offer is still on the table if you are willing to accept it?

Can you please give me the proof that the Chch population is declining or is it just coming from all your friends from around the country?

t

The other day when I was doing a bit of research on the word rentier, suspecting that many people thought a rentier was someone who lived off rents that tenants paid, I found this quote and immediately thought of Gordon:

Hence the extraordinary growth of a class, or rather, of a stratum of rentiers, i.e., people who live by 'clipping coupons' [in the sense of collecting interest payments on bonds], who take no part in any enterprise whatever, whose profession is idleness.

You don't want DTI's as your speculative so called rentals will be at risk of dropping in value. Any one who calls himself The Man does not think about the plight of FHBers. You have in fact contributed to their current position but the RB is on its way. Just a mater of time. You should wish for a soft landing in housing values otherwise the RB will make it a hard landing.

Man who sells icecream would prefer summer to last all year round, more news at 11pm

In a completely non-mathematical sense, the bazooka of DTIs are required as well as the rifle to improve and tighten existing rules, because you need to bring everything to a fight against a figurative Death Star. When affordability and risk taking is through the roof for this bubble, and with a RBNZ that defaults to being late to the party rather than on the ball, it is hardly going to "kill" the property market. A long period of property value stagnation or small drop would be a lovely consequence.

Also, when you are trying to predict 30 years into the future, a 6.5% "stress test" is hardly stressful or prudent.

Gordon.

You haven't answered whether you are up for that challenge!

100k that the boy is in fact "The Man"

The 100k to go to the charity of our choice and an apology from the loser to the correct one on Interest.Co

We will be able to get details verified by someone from Interest.co

You think I'm the boy then back it up with the 100k to charity!

If you are not up for it then apologise and stop trying to upset me as it is very hurtful Gordon.

Await your answer!

The boy I already give enough to charity. If you want anyone to take you seriously you should use a different name.

Get a room, you two. All this crackling sexual tension is becoming a distraction.

DTIs will ensure NZ's current stock of houses will remain a shambles as no one can renovate (myself for example) rules are tight now and DTIs will totally suck

Trying to prove your income will be a hassle for people who are on commission or self employed etc. previously you could get away with having more equity but that option won't be viable soon.

Current income... mmm mine hasn't moved that much recently.. same as past income.

Gordon, come on think of 100k to your favourite charity!

If you like it can be your family trust!

You call me "The Boy" and insinuate that I tell porkies.

Great that you give to charity already but think of another 100k.

If you aren't up for it then stop calling me a liar, as I do not tell lies!

Have you got those figures as well regarding the reducing Christchurch population that you claim?

The Boy lets just wait and see what Octobers sales figures tell us. A few of you speculators must be holding your breath as the news of late has not been that great. The Banks are certainly getting tough to deal with. And it will not get any easier to deal with them from here in. They certainly will be looking at their customers under mortgage stress a bit harder these days. As I keep saying. Change your name and I will take you seriously.

Children, please...your mummies both want you back for supper...

Gordon, had to put a name down when registering and a female friend of my wife says that I am "The Man" so that is why The Man.

Anyhow doesn't affect me what you think about me but the offer is always there.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.