By Alex Tarrant

So, the Official Cash Rate (OCR) is on hold until at least September 2019, perhaps as late as March 2020.

Right then. Nothing to see here. Run along now. Even Peter Dunne’s election manifesto will be more exciting than the outlook for short term interest rates.

If you’re thinking that, I don’t blame you. But just hold on. What if I said there’s an alternative world where the OCR is hiked by the end of this year, and is heading towards 2.5% in three years’ time.

For that world might exist. We might be closer to it than we think.

We’ve been warned.

The Reserve Bank of New Zealand’s upside risk scenarios in its May Monetary Policy Statement (MPS) should be mandatory reading.

They might have you thinking twice about how soon short term mortgage rates might rise, what sort of CPI inflation we’ll see in the next few years, and how much of a wage increase you might ask for next pay round.

And don’t just listen to me rabbit about it. Last week I sat down with Reserve Bank Deputy Governor Grant Spencer to chat through the May MPS and the Bank’s forecasts for the NZ economy. His comments are in quotes – the rest are mine.

How about that fan chart...

First, a bit of terminology.

Capacity pressure: The rate of inflation tends to increase when overall demand for goods and services exceeds the economy’s capacity to sustainably supply those goods and services. We tend to increase interest rates to ward off the inflationary effects of capacity being less than demand.

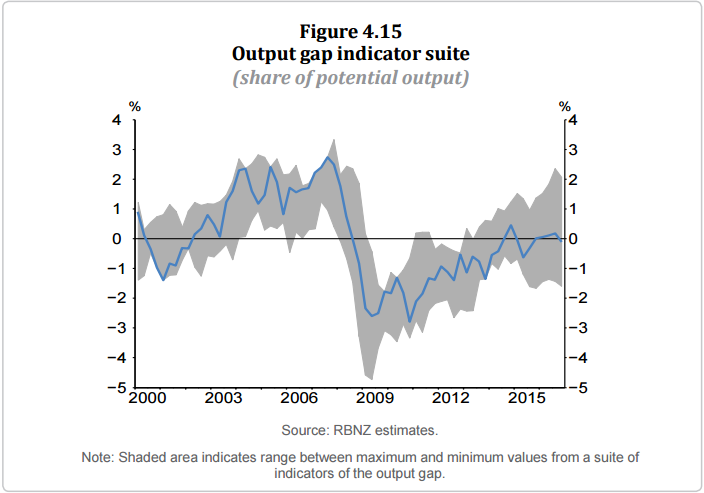

Output gap: a key concept in monetary policy, reflecting pressures on resources in the economy. Positive equals more pressure.

Now, The Reserve Bank last week was keen to draw peoples’ attention to the uncertainties about the current degree of capacity pressures in the economy.

Back in February it had thought that, by now, we’d have a ‘positive’ output gap, leading to greater wage and price inflation pressures.

Despite this, the Official Cash Rate (OCR) – the base for short term interest rates – was only expected to be raised from 1.75% to 2.0% from September 2019 at the earliest.

Since February, economists had been telling us that capacity pressures in the economy looked to be greater than the Reserve Bank had been thinking. The Bank would therefore have to bring forward its expectations for OCR hikes due to the Output Gap being more ‘positive’ than it had thought, we were told.

Mortgage rates would be set to rise earlier than expected.

Not quite.

As it turned out, the Reserve Bank in May told us that its February forecast had got ahead of itself. The output gap right now is not positive. It’s zero – in a sweet spot.

Or at least, it might be zero. It also might not be.

A key chart in the May MPS highlights the forecast ‘fan’ variations around the Bank’s output gap projections.

The fan is clearly wider than it was a year ago. This effectively means the Bank’s uncertainty around its forecast has increased.

Labour market conditions have continued to tighten. Employment growth has been strong, and the number of unemployed falling. All point to capacity pressures.

But nominal wage growth has been subdued. More so than if you’d been expecting capacity pressures and a ‘positive’ output gap like the Bank had been expecting in February.

The Bank has put some of this down to the effects of us having low inflation in the recent past – we haven’t needed such large wage increases to cover a low rise in the cost of living.

There was enough evidence in May, though, for the Bank to shift back its expectations for when capacity pressures will start feeding through to inflation.

And that’s one of the key reasons for why it was able to keep the same OCR track in May as in February.

Despite what everyone else was saying.

Pressure is coming, look busy

Pressure is coming, though.

Once that output gap does turn positive, capacity pressure is expected to drive a lift in business investment. The economy will grow above trend in response to population growth and accommodative monetary policy.

There will be labour shortages. The unemployment rate will trend lower. Wage-setting behaviour will respond to increasing headline inflation (albeit gradually because we’ve all got so used to low inflation, apparently).

All this will apparently happen with the OCR at 1.75% through to September 2019, when the Bank might look to start raising it. In any case, we’re expecting 2% by March 2020.

Except, it might not.

Because, like the slightly annoying repetitive London tube station warning, we’re being told to ‘Mind the Output Gap.’

Mind the gap

You can see a larger band to the upside. So, what could this mean for inflation, and most importantly, the OCR and mortgage rates?

Helpfully, the May MPS presented an alternative scenario analysis. The Bank wants us all to keep this in mind:

In light of recent data revisions, the estimate of current capacity pressure is now lower than previously thought. However, some measures suggest capacity pressure could be stronger than the current assessment.

That’s from the May MPS.

What does it mean? Well:

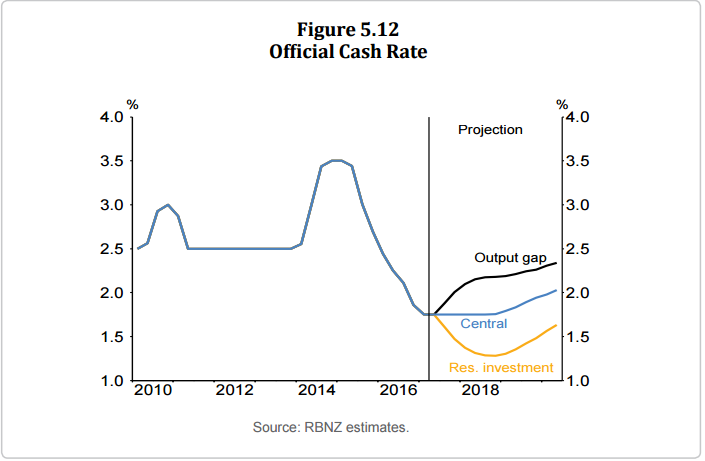

Higher-than-estimated capacity pressure over 2016, with the same growth and demand outlook, would place additional upward pressure on non-tradables inflation relative to the central projection. Without a policy response appropriate to the true level of capacity pressure, this scenario would result in CPI inflation increasing more rapidly than in the central projection, returning to 2 percent by the end of 2018 and eventually settling around 2.3 percent.

To offset the additional inflationary pressure in the scenario, the OCR would need to rise, reaching 2 percent by the end of 2017 and 2.25 percent by the end of the projection (figure 5.12).

That’s quite a bit different from the central scenario. (Another scenario discusses lower-than-expected residential property investment - read about that on page 33 of the MPS.)

Why? Last week after the MPS was released, I sat down with RBNZ Deputy Governor Grant Spencer and asked just that.

He told me that while the outlook had been for more positive capacity pressure, and inflation pressure in the future, as time went by and the next round of forecasting came in, it just wasn’t showing through as expected.

“A lot of it is due to the fact that we’ve been surprised by continued migration, which has increased potential output, which then drops down your actual capacity pressure,” Spencer said.

In February it looked like we would be ‘positive’ by the time May rolled around.

“But now we’re not – we’re back around zero. So, the emergence of more inflation pressure has tended to be…pushed out. That’s what’s happened again [in May].”

“But the risk is, because of the range of these measures…the risk is that, actually, capacity utilisation is greater than we think it is. It may be the output gap is plus 1% rather than zero,” Spencer warned.

“In which case, there’ll be more inflation in the pipe and we have to react to that down the track. That’s seen as an upside risk in these overall forecasts – that we’re underestimating capacity utilisation.”

“The more uncertain the forecast, the less likely you are to act. The more likely you are to say, ‘let’s wait and see what actually happens,’ before you respond. That’s essentially the story,” Spencer said.

I noted that, pretty soon, there will be a positive output gap and wage inflation to boot. Aren’t they worried about that? Especially if the Bank is planning on keeping the OCR at 1.75%. Why not move now, or at least sooner than they’re projecting?

“We’re saying it’s all very well to do these forecasts, and the forecast is that there’ll be a positive output gap. There’ll be more wage inflation, and we’ll move back towards the midpoint. But the risk is there’s a repeat of what we’ve had in the past, which is, that additional pressure doesn’t actually eventuate,” Spencer said.

It’s a fair point. An uncertain forecast means the Bank is more likely to wait and see what happens a bit more before reacting, than if it were more certain about its estimates.

We might be ok. The central scenario might pull through.

Just remember though, the Bank has chosen to present the situation as the output gap being faced with a greater risk that capacity utilisation has been underestimated rather than overestimated.

And that means it may have under-estimated inflation pressures, meaning the OCR will have to rise earlier than expected.

You’ve been warned. Mind the output gap.

*This article was first published in our email for paying subscribers early on Friday morning. See here for more details and how to subscribe.

50 Comments

A fine article Alex. It does rather suggest that immigration is keeping wages in check and putting off interest rate rises. So more fuel for asset price inflation. Presumably they think asset price inflation good, wage inflation bad.

Do they understand that asset inflation is highly destructive as it decreases our productivity? It does this in two ways, firstly by encouraging capital misallocation into low or negative productivity projects; and secondly by pushing up our overhead costs as a nation.

I find myself equating Spencer's ramblings with those poured forth by Fed officials.

These FOMC statements are in many ways quite like that; the Fed continues to act as if it portrays any useful economic meaning when long ago, almost six years, to be exact, the bond and funding markets slammed the door of real power on it. They may from time to time appear interested in the rambling ruminations of the perpetually confused, but for all that really matters these things are whittled down to mere televised ceremony. It’s a big deal for the financial channels and even for filling media page views, but eurodollar futures truly designate what moves the Earth now. And it isn’t transitory. Read more

That must be the 12th article in the last 6 months, warning about upcoming interest rate rises, I STILL don't buy it.

Do you know the difference between short, medium, and long term?

Because that might be intuition that you are missing.

In the long term we are all dead. But in the interim:

If we use $16T as the approximate GDP and a growth rate of, say, 3.5%, the total of goods and services would increase one year to the next by about $500B.

Meanwhile, referencing the Grandfather national debt chart with the USDebtClock data, the annual interest bill is $3 trillion ($2.7 trillion year-to-date).

In other words, those receiving interest are getting 5-6 times more than the increase in gross economic activity.

Using your oft-referenced Pareto Principle, about 80% of the population are net payers of interest while the other 20% are net receivers of interest.

Also, keep in mind that one does not have to have an outstanding loan to be a net payer of interest. As I attempted to earlier convey, whenever one buys a product that any part of its production was involving the cost of interest, the final product price included that interest cost. The purchase of that product had the interest cost paid by the purchaser.

Again using the Pareto concept, of the 20% who receive net interest, it can be further divided 80/20 to imply that 4% receive most (64%?) of the interest. This very fact can explain why/how the system (as it stands) produces a widening between the haves and the so-called 'have nots'.

In other words, the wealthy own interest-yielding assets and the rest of us owe interest on debt. Read more

Or a Chevron perhaps, and borrowed huge amounts of money at less than 2 per cent in the US, loaned it to themselves at 9 per cent in Australia and not just wiped out their taxable profit but even made a profit from the ATO.

https://www.michaelwest.com.au/plutus-the-police-raids-the-ato-and-the-…

You keep saying that interest rates will not increase but never give reasons why.

Why?

Because the global economies have NOT recovered from the GFC. I think when QE stops & interest rates go up, the economies will tank.

There you go

The global economies have recovered significantly from the GFC. Both the US and European economies are performing much better and while they are not out of the woods they are performing much better than people believe. I think your statement is nothing more than scaremongering. You can stick your head in the ground (which I believe you are doing) and ignore the fact that things are slowly improving. At some point QE has to end. If New Zealanders have gorged themselves on debt and now can't face the fact that there is a very real prospect on increasing interest rates you have to wonder about their financial intelligence - noone forced them to borrow and if they can't service the debt they have taken on they deserve to loose the "shirt off their back".

"Recovered significantly"? - have you been to Europe & the UK lately? More economically stagnant towns than I have ever seen.

While households make their own financial decisions - those who bought houses in the last 6 years did so in the environment created by this government who set policy encouraging and permitting high immigration and active offshore selling of property, so NZers forced to buy at highly inflated prices in their own country. So letting borrowers 'loose' (lose) their shirts may be an interesting option.

Robotics is great for automation - not so effective for systems thinking.

Firstly Europe and the UK is not the entire world and secondly we are talking about New Zealand. You seem to blame the government and yet abdicate any personal responsibility. Again no one forced people to borrow. Things change however. You are also talking about home-owners yet in your original reply you included a much larger group of borrowers - what about them. Your proposal seems more like the "zombie loan / bank" problem that has infected some countries - ignore reality by keeping interest rates low and ignoring the problem that people have borrowed more that they should have.

If you have to resort to an insult in an argument - you have already lost the argument (and you are making the rather arrogant assumption that you are right).

Maybe we both have reasonable arguments BadRobot (you named yourself surely).

Personal responsibility for borrowing, & risk management re rate increases is valid, while looking for system causes of why households have been put in a position of needing large mortgages to buy a home for their families is also valid.

Regardless of 'blame' you do need to think about the wider economic effect of borrowers not coping with interest rate hikes - the fallout would affect us all. And whether that factor is a constraint on hikes.

I so wish you were wrong about this .. however I think you are right.

Yvil, they really haven't got a clue.

There is no way rates will increase much even though the Banks need people to put money on deposit with them to fund mortgages.

The reality is that the LVR policy that they have adopted in that they have changed the goal,posts for the security percentage, will mean that the Banks lending will drop.

Increase the rates and even fewer people will borrow.

Analysts are almost always wrong and that is why they are still working for wages.

But last year economists were saying that interest rates were going to stay low for a long time and now they say interest rates are going to increase. You say they are wrong - but who is wrong.....

Fewer people may borrow but increase the rates and margins increase. If Banks dont increase rates then their margins are squeezed as cost of borrowing has increased. Not a great thing for shareholders if your profit growth rate is decreasing. Not sure if shareholders will be happy.

Remember the Chinese saying..Beware what you ask for, you may get it.

Interest rates will need to be cut, due to falling lending, & worry over house price growth slowing.

Always think counter-economic prediction.

Yes bank lending into some sectors is falling (e.g. the property market where NZ actually needs investment), and the reason for that is that NZ savers/investors such as myself are pulling money out of banks and putting it into higher risk investments that provide an acceptable an income stream, and being prepared to sit out a fall in that over-priced asset. The RBNZ can't cut rates because the RBNZ no longer determines where rates go, the banks do - and the bank are driven by what savers/investors are prepared to accept, and the latter are now on strike.

So no matter what, central banks cash rates aren't going lower from here unless there is a severe financial or economic shock that panics cash back into bank accounts, and from the way people worry here about OBR issues, a good amount might not even go back there then. Rates are going slowly higher over time as they "normalise" until they work for both sides of the market (irrespective as to whether the RBNZ hikes or not), but if the RBNZ has got its inflation forecasts wrong, it won't be slowly when/if they realise that.

In the last 10 years central banks globally have forced rates down to all time historic lows, and held them there for too long. They have induced billions of people into increasingly over-priced assets, and now the likes of the RBNZ is risking taking that even further (unlike the Fed) in making the non-thinking borrower too complacent as to how much longer he/she will get to enjoy them - they risk setting up these people up for a massive fall. As the saying goes, when/if the tide goes out, lets see who's been swimming naked

Spot on and highly relevant. Retail rates will rise because they must. Deposits need to be attracted to fund (even limited) credit growth.

Any chance mortgage rates will go below 4% within the next 6 months ?

Move to the UK or Germany etc & enjoy a starter mortgage rate of 1.5% - forget 4/5%

But this is not the UK or Germany. As New Zealand is currently not self funding and has not adopted QE , New Zealanders have to pay the local interest rate. New Zealanders live beyond their means - so they have to pay.

There are actually ways of financing indirectly from offshore & using for NZ purchases.

So your conventional argument is getting a bit outdated in our globalised world.

And NZers are getting a bit tired of being used as the testing ground for Expensive products.

You're trying to tell us an offshore bank will lend on NZ security? Youd be nuts to borrow in anything other tnan NZD, because you'd be exposed to massive FX risk.

Badrobot - probably is many who assume others will lend to us directly or indirectly from overseas, do not under stand what the RBNZ's core funding ratio means for NZ banks

and zero interest for savers. no thanks.

Smokey - move to a country like those that have a better savings attitude and can fund their own borrowers, as compared with a small country like NZ that relies upon the good will of others globally that will always require an interest rate premium to cover the credit and currency risk that they incur to do so. Unfortunately too few NZers understand that basic issue, and tend to bleat on about why they can't have it both ways - even the existing NZers savers are deserting those borrowers now.

All crap! Don't fix more than a year or max.18 months, interest rates are not going anywhere definitely not upward. You will be saving a lot with short term fixed rates than going for longer term for the considerable future.

What makes you think interest rates are not going up.

Because the propensity of the real economy, consumers, small business, small farmers, borrowers, households, bank lending rates, homeowners towards higher interest rates is very low.

The global economy has not really moved on on in a realistic way from the 2008 GFC.

Because NZ interest rates are the highest in the developed world.

Interest rates keep lower for longer, .....

And who's fault is that. Your rationale seems more like scaremongering than a true reason ( or even worse some type of threat) . Nobody forced people to borrow money. If people can't look ahead and foresee that things might change you really have to question peoples financial intelligence.

Not really a matter of whose fault it is - it's reality. A reality that every lender will assess to test the limits/tension between the desire to increase the amount of lending and the desire to increase interest rates.

Large sectors of the economy and corporations depend on low levels of financial intelligence in the population - of course. That's how, for example, dual income households have 800k+ mortgages etc.

It is totally someone's responsibility - no one forced people to borrow. People have to take responsibility for their actions and knowledge ( or lack of knowledge). This doesn't however support your argument that interest rates will be kept low.

Do banks wish to lower the amount of lending, or lower the growth rate of lending?

Banks will, and are, lowering their trend rate of lending growth and pushing out their margins to compensate them for that and their increasing funding costs as depositors desert them - eitherway, the result is higher interest rates whether they're lending more of less,

Banks have crawled over each other over the last few years to lend money basically to whoever wants to buy multiple investment houses. Now with the subdued housing market, lending volumes will be down and a large number of borrowers will be in default having borrowed too much.

The banks will want to maintain their bottom line and cover losses from default borrowers. They cannot drop deposit rates but will increase interest rates to cover their profits.

banks are being more proactive chasing depositors, I am getting phone calls and emails touting for more money

also some are now offering treats

https://www.bnz.co.nz/personal-banking/everyday-banking/rapid-save

https://www.tsbbank.co.nz/accounts-and-cards/everyday-accounts/connect-…

big change from the last few years where only borrowers were offered treats

BadRobot - what I've observed over the last 5 years in this country is that generally speaking, people have very little self control and are strongly influenced by what other people are doing. So if it becomes the 'norm' to borrow a lot and have a couple of rental properties, its very difficult to buck the trend. How else would you explain the predicament we find ourselves in in terms of personal debt? If we were wise, we would have viewed the period of low interest rates as the perfect time to pay down our mortgages and have a reserve of savings ready for a rainy day. But instead greed won the day, and people viewed it as an opportunity to buy more and borrow more. People have done the complete opposite of what they should have been doing.

So do people need more supervision when it comes to the amount of debt that we lend to them - it appears the banks 'pretend' to care because they are supposed to look reputable/reliable. So if the banks aren't responsible, and its clear people aren't responsible (if they were we wouldn't be in this situation) so where do we go? I don't have the answer, but I've been surprised by how 'out of control' people are in their spending habits and their desire 'to get one up' over their fellow citizens - result being a housing bubble of epic proportions where 'at the end of the day' no one wins, we all lose at its a zero sum game.

This analysis ignores some key international factors at play and could therefore turn out to be irrelevant. Some of these possibilities include:

- Central banks have NO influence over long term interest rates. When the tide of big money turns then interest rates can certainly shoot up, with or without central banks moving.

- Another crisis in Europe, which is only a matter of time, will see a capital exodus and a surge in the USD and a liquidity crisis. This will ensure higher interest rates as well.

Simply assuming that interest rates "can't" go up because the economy would tank is naive and wishful thinking. However, people will believe what they want and the majority is generally always wrong.

Think the reserve bank would tolerate some overshoot on inflation after such an extended period of falling under the target band. The reserve banks forecasting is very poor however so I do accept inflation could go either way.

I will keep standing by my 2013 prediction that interest rates will keep trending down. The end game happens when yields on investment follows, and people have to sell assets for income.

I don't think the interest rate rises and the talk is a prediction, its suddenly out there so your mentally being prepared for a rise when it happens. The banks are preparing you for a rise in advance so it doesn't come as a complete shock and we get the "But I told you so 6 months ago....". Its time to start getting your $hit together for when it happens.

My 10c worth if i may.

Next year and 2019 - Euro zone and US have rollover of lots of bonds.

There will be next to no bid. Here's why..

Lowering of confidence in Govt mainly the EU. ( The us can chew up a fair bit of theirs as their Fed and state debt are seperate. The EU is not. The ECB owns 40% of all govt debt as well. The US Fed has stated they shall not roll over.

No bid = interest rate rises to attract the bond buyers ....

We shall see ...

Nice observation based on data points, not like some *cough MortgageBelt* commentators here.

"The central bank also stated that monetary policy will remain accommodative for a considerable period, as numerous uncertainties remain and policy may need to adjust accordingly"

http://www.tradingeconomics.com/new-zealand/interest-rate

.

'Monetary policy will remain accommodative" May 2017

Did even read the article you're commenting on?

"The Reserve Bank of New Zealand’s upside risk scenarios in its May Monetary Policy Statement (MPS) should be mandatory reading."

vs your statement

"Interest rates will need to be cut, due to falling lending, & worry over house price growth slowing.

Always think counter-economic prediction." based on the fact, if I understand your position, that banks will want more lending. But that fails to take into account the cost of said lending - retail deposit rates, capital adequacy etc all play a part in that.

What would the NZ economic environment have experienced if the RB had left interest rates at 2008 levels after the GFC?

What level of interest rate 'accommodation' is currently needed to keep the system afloat?

Survival first for any economy.

MisterB - very true - the problem with the desperate is that they only focus upon the bits that they want to hear, and totally block out all possibility that they might actually be wrong. Unfortunately they're the ones who can least afford to handle the shock of a surprise

To focus on the local NZ macros is having the blinkers on ...

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.