This is an update of a note I wrote in April 2007. It uses a longer housing price series that starts in 1962 (instead of 1980) and finishes in 2016 (instead of 2007).

It shows that while historically housing prices have risen a little faster than consumer prices, the increase has been sharper since 2001 (except for the period when the Global Financial Crisis impacted). It goes on to use the historical record to speculate on possible patterns of future prices. The focus is on house prices for the whole of New Zealand. There can be considerable divergences between regions.2

Nominal Housing Price Trends

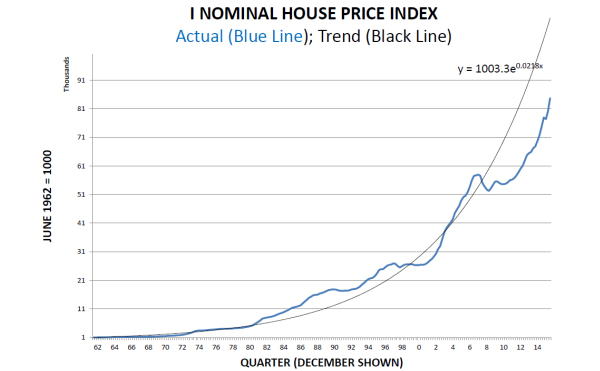

Graph I shows the Reserve Bank of New Zealand nominal housing price index (that is, prices not adjusted for inflation) for the 209 quarters from 1964Q2 to 2016Q2. Over the 52 years, the prices rose to over 80 times their initial level, an annual average increase of 8.6 percent per annum; this was faster than inflation.

Graph I: The blue line is an index of actual house prices. The black line is the exponential trend line between 1964 and 2001. The growth rate for (nominal) houses prices averaged 9 percent a year.

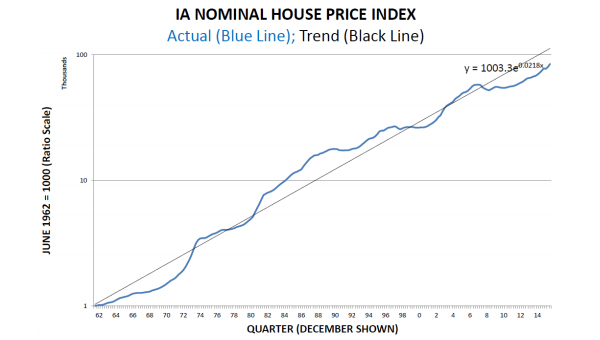

The linear vertical axis of Graph I does not show growth rates of prices. Graph IA does, so that the same slope reflects the same inflationary growth rate. Although there have been concerns about sharp rises in recent years, the big inflationary periods – where the graph line is steepest – are in the early 1970s and the early 1980s. Even the recent house price increases have not been as sharp as they were in 2002 to 2008.

Graph IA: This graph is the same as Graph I except the vertical axis is a log-linear (or ratio) scale. Now the black trend line is straight – that is, it has a constant growth rate. Where the blue line of actual house prices rise faster than the black trend line, prices are rising faster.

House Prices Relative to Consumer Prices

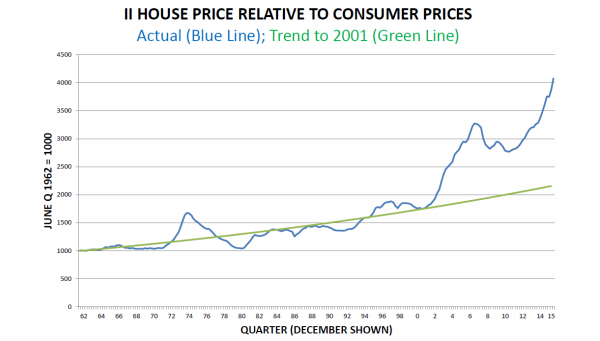

Graph II shows the ratio of house prices to consumer prices, which presents a different picture of relative housing inflation. Historically there has been a tendency for house prices to rise faster than overall consumer prices. (The appendix discusses alternative deflators.)

GRAPH II: The blue line shows house prices relative to consumer prices. Where it rises house price inflation is rising faster than consumer prices. The green line is the trend growth line from 1964 to 2001. It shows that while nominal house prices may not have been rising faster in the 21st century than they had earlier, they were rising faster than consumer prices because the later period was one of much lower consumer inflation.

Up to 2002 the average house price rise was 1.4% p.a. above the rate of inflation. By later standards this rise was small. Aside from measurement error, it might be the consequence of the supply of housing increasing more slowly than the underlying demand. We can speculate why, but any effect was not great.

After 2002 the average annual rise increases markedly to a rate of 8.2% p.a. The slow relative shifts in supply and demand described in the previous paragraph are surely insufficient to explain the quintupling of the relative rate of housing inflation. Moreover, as identified in the 2007 note, the change in the trend housing inflation rate is very abrupt.

Note that there was a five-year period between 2007 and 2012 when house price rises were checked by the Global Financial Crisis. Take this period out and the average increase across the country from 2002 was 12.4% p.a. – almost ten times as high as before 2002.

The price increases will vary by region. Auckland’s are among the highest. The increases reported here may seem less than the housing price rises headlined in the media. But those figures are often for sales only or for selected regions. The Reserve Bank of New Zealand index derived from Quotable Value applies to all housing. It is in the interest of those doing a beat-up during a speculative boom to give the impression that asset prices are rising faster than they actually are.

The acceleration in the relative premium after 2001 coincides with President George W. Bush increasing the United States’ fiscal deficit which flooded the world with financial liquidity. That made it easier for New Zealand banks to borrow offshore using the cash to fund housing purchases. While the housing price rise was not confined to New Zealand, The Economist reported in 2017 that New Zealand’s house price relative to inflation is the highest in the rich world.4

Another source of funds from the international liquidity was investments by migrants or off-shore based investors. Some would have purchased the houses they would live in. But anecdote suggests that some purchasing was for speculation. Probably the source of the funds was capital flight especially from China; instructively Sydney, Melbourne and Vancouver have experienced similar price rises.

The funding inflow generated a speculative bubble, especially as the stock of housing cannot be easily increased. A speculative bubble is typically driven by expectations of strong asset price rises coupled with leveraged borrowing, giving a high return as long as the prices rise.5 But the price increases cannot sustain the spectators’ expectations forever and eventually the bubble pops or deflates with over-leveraged speculators stranded. Usually there are knock-on impacts which damage those who are innocently (that is, non-speculatively) involved. The lack of an effective capital gains tax in New Zealand has probably compounded the strength of any speculative bubble, especially when speculators could cover part of their purchase price by borrowing at fixed interest below the nominal house price increase.

The boom staggered around the time of the Global Financial Crisis, when international liquidity dried up. It returned when the central banks of the world began quantitative easing, which again injected liquidity into world financial markets. Confidence, expectations and the state of the labour market may also have contributed to this outcome, but may well have been a part of the transmission mechanism from the contraction in international liquidity to the housing market.

The way overseas borrowing works is not straightforward. Suppose I take out a mortgage of $1 million to purchase your house. You deposit the $1 million in the bank so the net position of the bank is unchanged and it can pay off the overseas loan it has used to fund my house purchase. The net position after the transaction appears to be zero.

If this was the entire story, any international borrowing only lubricates the sale and purchase transaction. But in the course of the sale there are transaction costs: real estate agents, banks, lawyers, valuers, surveyors, movers, and so on, while house buyers often go on to commission builders to alter the house and to purchase durables and furnishings. The total costs may be a considerable amount – in one modest case I know of they were in excess of $30,000 including the costs of selling the previous house (a downsizing too). In total this amounts to a considerable expenditure each year (100,000 houses at $30,000 per sales transaction is $3 billion) which is, in effect, borrowed offshore. Observe that it can hardly be argued that this offshore borrowing is funding ‘investment’ – although some is so classified in the official statistics.

If the long-run relativity that existed between 1962 and 2002 had persisted through the following 14 years, house prices today would be half the level they actually are. It could be argued that this is a measure of the degree by which housing is overpriced. We use this doubling up (or rather halving down) to illustrate the general proposition of the adjustment which follows a speculative boom.

Falling Nominal Housing Prices

There seems little doubt that in some sense today house prices are unusually high as the consequence of a speculative bubble. What will happen when the bubble pops or deflates? Usually this involves a fall in asset prices, in this case house prices, but how and by how much and with what consequences?

We cannot be sure. In particular, overseas experience may not always be relevant because of different circumstances. It is certainly true that the United States’ house prices collapsed in many parts of the country after the Global Financial Crisis – indeed their boom and bust was one of the causes of the crisis. But the obligations of mortgagors (typically banks) and mortgagees differ between the two countries. It is easier for mortgagees to walk away from a house in the United States than in New Zealand, leaving the banks holding the title and the expenses which go with it; that encourages fire sales.

Nor need history be a good guide. I hunted around for evidence of what happened in the 1930s but there is no data. In any case, mortgage arrangements differed because banks were not as heavily involved. There were mortgage and tenant relief measures but arguably they occurred because of general deflation and falling nominal interest rates.

The speculative housing boom in the early 1970s – evident in the graphs above – does not seem relevant because it was followed by a period of high consumer inflation during which house prices stagnated, returning to the relativity track between housing and consumer prices. There is no expectation of high consumer inflation in the immediate future.

Graph I shows that over the 52 years falls in nominal housing prices have been small and rare and, usually, for only a quarter or so; they are but market stutters. The one exception was the period from 2007Q4 (which precedes the usual date for the beginning of the Global Financial Crisis of August 2008) to 2009Q1. The fall across the five quarters was around 10 percent – 2 percent a quarter.

So New Zealand’s post-war experience is that significant falls in nominal house prices are unusual across all regions although sometime special factors affect a particular region. (This conclusion may not apply elsewhere – such as in the United States.) This probably arises from a ‘nominal house price rigidity’, paralleling the nominal wage rigidity which Keynes wrote about.

Suppose the speculation stops. There will be a steadying of house prices. Most home owners who traded up their houses during a boom – not unaware of the speculative gains – will now sit tight rather than sell their house below the peak price. There will be some distressed selling from those who cannot service their mortgages and some necessary selling from estates of the deceased, from those who have to move, or those who have had a dramatic change in their family size or circumstances such as ageing.

The bubble activity from speculation and trading-up will cease. It is understandable that speculators withdraw from a market when there is little expectation of price increases, when home owners stay tight and do not look for improved accommodation - forgetting that the house they would be buying will have fallen in price too. It can be compounded by the individual’s assessment that the quality of a house is partly a function of the perceived price, which is not an assumption in economists’ standard theory of demand.

Whatever the case, the indications are that – aside from traumatic economic and financial events such as a massive rise in unemployment – the nominal house price will be sticky downward because most homeowners will not want to move if prices fall. They will hang onto their home valuing it at its current (peak) price. (In behavioural economics this is related to the endowment effect, the theory that people place more value on the things that they own.) The price of housing is not going to fall by much in the short term.

Suppose the price slippage is at an annual rate of 8% (similar to the 2008 fall) and that consumer prices rise at 2% p.a (the current long-run assumption). After allowing for the rising pre-2002 relative trend (of 1.4% p.a.), it would take until 2022 for housing prices to return to the trend that existed before 2002. By that time, the average house would have lost about 40 percent of its nominal value. (My 2007 calculation was more optimistic because it assumed a higher rate of inflation while the over-valuation was not as great. It did, however, assume that house prices would stay the same, rather than drift downward.)

The previous paragraph is not a prediction, but an exploration based on a series of assumptions. It is to indicate that it is going to be difficult for housing prices to rebalance with consumer prices.

Turning to Graph II we see that the longest period of relative price stability was the six years following the wool price collapse of late 1966. The longest period of housing prices falling relative to inflation was also about six years – in the mid-1970s – but this was a period of stagnant nominal housing prices and high consumer inflation. The implication is that six years of even mildly falling nominal housing prices would be unusual.

Stagnation and Low Market Activity

What happens during periods of stagnation and low market activity?

First, the housing transactions industry is likely to contract; that will be most evident among real estate agents but others – financiers, solicitors, valuers and so on – will also experience a reduction in their activities.

Second, with the reduction in turnover it will be harder for people to find the houses they require. That they cannot move on will reduce the turnover further. In effect there will be substantial reduction in market ‘liquidity’. This term is usually used for more homogeneous financial markets but it can be applied, to some extent, to the very heterogeneous housing market.

The standard theory of financial markets observes that speculators contribute to markets’ liquidity by being willing to buy and sell the asset, matching market deficits or surpluses. Presumably the same thing happens in the housing market if we include speculation to cover buyers upgrading their housing, with nominal capital gains as a partial reason. The lack of this liquidity occurred to some extent in the immediate post-Global Financial Crisis housing markets and, arguably, may be occurring since late 2016, adding to the market stagnation.

The macroeconomic adjustment may be complicated but the size of the necessary discussion means that it cannot be fitted into this paper. There will be falling employment in the housing transactions industry. There may be less house building – but more house alterations since incumbents may adapt their houses rather than change to other ones. In principle a government concerned with housing a growing population (and/ or replacing poor quality housing) might increase housing construction from the public purse; the houses will be smaller though – and presumably more of them. Insofar as there is a fall in the exchange rate because offshore borrowing falls, there may be some surge in the tradeable sector, although New Zealand supply responses tend to be slow. In any case it is not obvious how to convert real estate agents into export salesmen and saleswomen.

Conclusion

At this point the reader may ask, what is to be done? However, this paper is about what has happened, what is happening and what may happen. Before deriving quality policy conclusions it is necessary to get those questions clear as well as to decide on priorities and options.

Moreover, there will be other things happening which will complicate the policy response. What happens to mortgage interest rates during a housing market downturn will likely depend heavily on the driver of the downturn and its macroeconomic consequences. If interest rates were to rise they would compound the difficulties of those who have over-borrowed in a stagnant market.

My view is that the government should not be concerned about those who have got into difficulties because they have over-borrowed, although there will be public pressure from them. I am not a fan for the coupling of privatisation of (especially speculative) profits with the socialisation of losses. The transfer of the losses of speculation – even those of owners of single homes – onto the public balance sheet is not a fiscal priority. It is accepted that the public – and hence the government – has an interest in ensuring the stability of the financial system. Recently published Reserve Bank of New Zealand stress test results suggest that the banks are not threatened by stagnant or gently falling house prices.6

In my view, the priority is to ensure that the population is adequately housed - which is not the same thing as being housed in mansions bigger than they need, the extra size being a part of their speculations. While rental housing, including public rental housing, will be a part of the solution, my impression is that the stock of housing is better looked after by owner-occupiers. Enabling families (including families yet to be formed) who currently do not own houses to purchase their own houses has to be a central part of the nation’s policy objectives.

Indeed, the housing market stagnation may create an opportunity for a programme of the building of modest-sized new housing and replacing dilapidated existing houses funded, in part, by offshore borrowing. This would more efficiently house the population while adding to the assets of the country rather than – unlike too much of the borrowing of recent years – disappear in transaction costs.

As recent and historical experiences show, the private market cannot be left to do this by itself. My earliest knowledge of public intervention is the workers’ cottages under the Seddon Government. (About the same time, owned housing was partially exempted in the asset testing for eligibility for the Old Aged Pension.) However, the measures undertaken by the Massey Government in the early 1920s were much more successful in achieving widespread housing and framed policy for the next half century.

Historically then, it was not just a matter of building public housing but also of facilitating the financing of private purchasing (some of which led to the private construction of housing). How to successfully house those with inadequate housing while getting a better relativity between house and consumer prices (that is, by avoiding further house price inflation) and without excessive fiscal exposure is a complicated policy issue. That will not stop fools rushing in where angels fear to tread, or tread only after much analysis. This note, one hopes, will be useful to some angels.

Notes:

1. I am grateful to Tama Easton, Julienne Molineaux, Bill Rosenberg and an anonymous economist for comments on an earlier draft.

2. For a paper which pays particular attention to Auckland house prices, see Elizabeth Kendall (January 2016). ‘New Zealand House Prices: a Historical Perspective’ Reserve Bank Bulletin Vol. 79(1). It has less on the future course of prices.

3. n.a.

4. The Economist. (2017, March 9). Daily chart: Global house prices. http://www.economist.com/blogs/graphicdetail/2017/03/daily-chart-6

5. Ryan Greenaway-McGrevy. (2015, July 26). ‘Bubble trouble’. Briefing Papers. Auckland: The Policy Observatory. http://briefingpapers.co.nz/bubble-trouble/

6. Reserve Bank of New Zealand. (November 2016). Financial Stability Report. http://www.rbnz.govt.nz/-/ media/ReserveBank/Files/Publications/Financial%20stability%20reports/2016/fsr-nov2016.pdf

Brian Easton is an adjunct Professor of the Auckland University of Technology and is currently writing a history of New Zealand from an economic perspective. This article is a repost of a paper published by AUT's The Policy Observatory. It is here with permission.

6 Comments

Mr Easton notes that "the average increase across the country from 2002 was 12.4% p.a. – almost ten times as high as before 2002."

As indicated by the RBNZ recently, perhaps it is banks slackening their lending standards that provides the best explanation.

Coleman (2007) provides some interesting historical perspective on the size of loans available to borrowers in NZ over time. Prior to the mid-1980s deregulation, bank mortgage providers faced regulations that limited the size of mortgage repayments relative to income. After those rules were eliminated, Coleman reports that banks maintained similar internal rules: for example a major bank required customers to be able to “meet minimum monthly payments” using “30% of sole income or 25% of joint income” using a 20 year table mortgage. By around 2000 these rules had been eased so that some customers could borrow 33 percent of joint income, or slightly more if they had a large deposit. These rules, alongside declining mortgage rates, meant that the maximum loan available to customers (relative to their income) rose substantially. Coleman suggests that a household earning $50,000 might have been able to borrow around $79,000 in 1989, but $191,000 in 2005. In DTI terms, the maximum DTI permitted had risen from around 1.6 to around 3.8.

"Auckland’s are among the highest. The increases reported here may seem less than the housing price rises headlined in the media".

Yes it would be good to see a chart that was specific to Auckland, considering how inundated that part of NZ has been with; Immigration, Foreign Buyers and a lot of Auckland local Investors were pushed out to the regions in the last few years which pushed up house prices.

So now that one of the key price property pushers has gone (Foreign Buyers), the question is how much is NZ over inflated property prices really worth?

Better Dwelling article: Impact On Global Real Estate Markets

Quote: Real estate markets that saw locals scramble to cash in on foreign buyers are now noticeably cooler. Toronto is seeing new listings hit an all-time high, coupled with a massive dip in sales. New Zealanders that were complaining about a “flood” of Mainland Chinese buyers, are now complaining about the market cooling faster than expected. Australia’s leading property analyst is now telling people to prepare for a 10% drop in prices soon.

Mainland Chinese buyers were buying a lot of international real estate, but over excited locals bought into the narrative way too much. Countries that are nice, but not global leaders got way too excited that they were the next “New York.”

https://betterdwelling.com/chinas-massive-international-real-estate-buy…

Good to see someone of Brian Easton's standing enter into the housing debate. Very good research and well-considered conclusions.

"My view is that the government should not be concerned about those who have got into difficulties because they have over-borrowed, although there will be public pressure from them."

This is effectively what happened after the GFC: Reserve banks dropped interest rates to ultra-stimulatory levels, where they have remained, which protected the owners of over-priced houses, and triggered further housing inflation, to the cost of savers, who have to put up with derisory returns on their deposits.

I noted, here, http://waymad.blogspot.co.nz/2017/06/why-house-prices-took-off-2002-3.h… one major reason for the incredible gain in prices after 2002 ish - the Welcome Home loan scheme.

A universal pricing signal - 'forget about what you had thought the shack was worth, price it at the WH loan minimum for the area and add a bit for the selling expenses. Cannae go wrong....'

Unintended consequences......

Just one point missed in relation to the big picture. The NZ Government's main asset is property. The banking sector's main asset in NZ are mortgages secured over property. These two large players will do everything possible to maintain their asset values, but pretend with spin and political PC comments that they are concerned that prices do not rise further. NZ has more conflicts of interest that are greater than even the property price trends !!! That fact conceals some deep seated concealed corrupt market practices that are covered up with selected paid-for expert reports, ignoring Treasury recommendations, and misleading political spin.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.