We still live in the shadow of the financial crisis. For example, high debt levels in the crisis countries mean international interest rates will remain much lower than "normal" for a protracted period still.

The effective level of the OCR is another example. While the actual level is 1.75%, the effective level that allows for the impact the financial crisis is still having on interest rates faced by borrowers is dramatically higher as explained in this Raving.

In addition to the 1.75% level of the OCR greatly overstating how low NZ interest rates are, three game changing factors are at work in the NZ economy that mean predictions of higher interest rates are likely to be misguided. This has parallels with the experience in 2010 when the economic forecasters similarly overlooked negative game-changing factors that were at play well before the Canterbury earthquakes struck. Just as I was alone in 2010 in correctly warning clients that interest rates could fall, I seem to be alone again in warning that interest rates are more likely to fall than increase because of the game changing factors the forecasters are largely overlooking, as discussed in our July economic report.

The financial crisis still casts a shadow over NZ interest rates

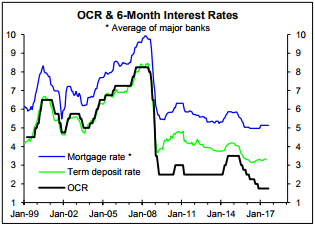

There was a dramatic change following the financial crisis because banks had to fund more from retail deposits relative to overseas funding. As a result, the six-month term deposit rate increased relative to the OCR (e.g. the term deposit rate is currently 1.56% above the OCR compared to it generally being marginally below the OCR prior to the financial crisis).

But the six-month mortgage rate has continued to largely move in line with the six-month term deposit rate although the gap has increased somewhat (e.g. the current gap is 1.83% versus the 1.45% average gap prior to the financial crisis).

The result is that the average six-month mortgage rate offered by the major banks is currently 3.39% above the OCR compared to the average of 1.39% prior to the crisis. In effect, this means the current level of six month mortgage rates is what you would expect prior to the crisis if the OCR was 2% higher (i.e. 3.75% versus the actual 1.75%). This is the lower bound of my estimate of the effective level of the OCR.

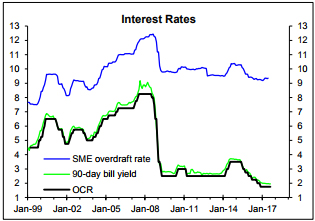

Prior to the crisis the SME overdraft rate averaged 3.2% above the 90-day bank bill yield and 3.53% above the OCR. Now it is 7.41% above the 90-day bank bill yield and 7.61% above the OCR. The current SME overdraft rate is consistent with an effective OCR of 5.83%. This is the level the OCR would have to be now to generate the current 9.36% SME overdraft is the pre-crisis premium still existed (i.e. an OCR of 5.83% plus the pre-crisis premium of 3.53% = 9.36%). This is the upper bound.

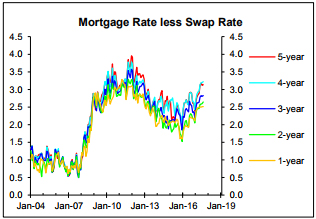

Prior to the crisis mortgage rates were around 1% above swap rates but now the premiums range from 2.5% to almost 3.25%. This points to the effective level of the OCR being around 2% above the actual level for mortgage borrowers but for business borrowers the effective level of the OCR is higher.

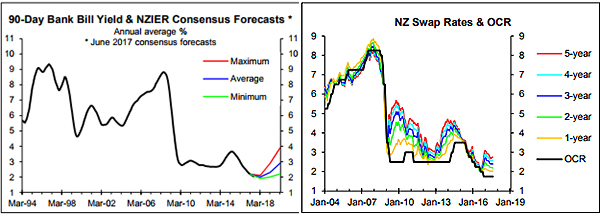

While this implies that the effective level of the OCR is more than double the actual level of 1.75% it doesn't tell us what the current appropriate level should be. The consensus view of the 8 economic forecasters surveyed by NZIER last month was that the 90-day bank bill yield would increase to 3% over the next three years (blue line, left chart below), none forecast that the 90-day bank bill yield would fall (green line) and the most hawkish predicted an increase to almost 4% (red line).

The 90-day bank bill yield forecasts can be viewed as proxies for OCR forecasts. By contrast, swap rates have fallen since the peak level late last year (right chart). The money market is starting to backtrack in terms of expectations of OCR hikes which I see as being justified by the game-changing factors currently at work that have the potential to justify lower interest rates as discussed in the July economic report.

The lower swap rates haven't flowed through to lower fix mortgage rates yet.. However, as was the case in 2010 when there was a sufficient market-led fall in interest rates to result in lower interest rates faced by borrowers, the market is well ahead of the economic forecasters who were similarly predicting higher interest rates in 2010.

There are some differences between current prospects and what occurred in 2010 but the parallels are strong enough that they should be taken seriously as outlined in the July economic report.

*Rodney Dickens is the managing director and chief research officer of Strategic Risk Analysis Limited.

32 Comments

You are not alone in predicting lower interest rates Rodney. I have continuously & repeatedly posted on this site that i was not buying the "imminent threat of rising interest rates" because there is simply too much debt at both government and private levels.

Too much debt at govt levels!? Eh? And I didn't realise govt was funded via the OCR?

Want to have another go at that?

Aggregate debt in most western economies is very high, this leads central banks to cut rates over time, if they dont then that high debt load weighs on growth, which reduces borrowing, which reduces inflationary expectations and so on it goes. Plausibly it hits a wall some day but its very hard to know when that will be.

Nah~ government saving was around 90 percent in 2016.

Debt level is extremely low, too low, we should've invested more on infra to imbed all the immigrants before they arrive.

Bobster - Monetary policy everywhere is suppressing interest rates to try & kickstart some growth.to inflate old debt away ... so hows that working out?

Weak appetite for more debt suggests someone is full..

Don't understand your comment Bobster ?

History has shown beyond doubt that lower interest rates just increases the debt levels.

The problem is paying off the debt when interest rates rise.

The RBA will lead the charge with a cut by early-mid 2018.

Unless a cut is required to maintain inflation within its band, or to counter a significant deterioration in the economy, there will be no cuts. The RB will not save you.

Luckily I don't need to be saved.

Australian inflation is in the lower half of its band, and besides the RBA has cut many times in the past while inflation is around 2%. The Australian economy is deteriorating, car manufacturing hasn't even fully closed yet and the bounce in Iron Ore prices is transitory.

I don't think a cut in Australia or New Zealand would move the dial on retail interest rates though. I think they will continue to drift upward.

It would move them down, and if it didnt then the reserve bank would move to force them down.

How would RB force retail rates down? Esp given 60% of bank funding is offshore over which RB has no control?

A small fraction of the past few RBA cuts have been passed on and the "actual rate on outstanding loans" has crept back up to close to the level it was when the cash rate was 50bps higher.

http://www.rba.gov.au/chart-pack/interest-rates.html

See Australian Housing lending rates.

The RBA have had the expansion in private household debt they were looking for, to try to ease the transition from mining to construction/services. But that avenue is spent now. If they cut it is because they need a lower AUD to try to foster some competitiveness, not to reduce retail interest rates.

It's certainly an interesting area, no pun intended. I was talking with a significant mortgage broker company and they are expecting rates rises not too far off as banks come under pressure from their owners to increase revenues, at a time when new lending is not an area they're really looking to get that revenue from.

If you're not going to be increasing your mortgage lending massively, where do you get your revenue increases from? Presumably through pressure on your deposit and mortgage rates?

Yes, with new lending in decline banks will look to protect yields by taking the benefit of rate cuts. They would also say this yield protection is appropriate as it reflects their increased risk lending in a falling market. Plus their offshore funding rates (60% of total funding) will continue to increase, although this may be slow. So we will not get bailed out by OCR cuts.

One day The World will realise that lower interest rates aren't The Answer, they are The Problem. The lower they go, the harder the road back, and at some stage ( perhaps 'they' have realised it already?) it's too far to turn back .Scott knew that at some stage on his way to the Pole, and pressed on, because he knew that death was inevitable, so why not go 'all in'. He did, and I'll suggest, so too have we.......

lower interest rates are just buying us (some) time to ignore resource constraints...

There is no road back to easy abundant resources (especially if you look on a per capita basis)

https://ourfiniteworld.com/2017/06/12/falling-interest-rates-have-postp…

Automation – and the general shift from physical to digital – is NOT being effected in order to solve demand problems and improve service: it is being applied to increase margins, boost profits, and thus make the 3% élite even richer than they are already. This reduces mass demand further and further, until the entire model of automated mass production produces two outcomes. First, enormous gluts and inevitable depression; and second, further dilution of spending power among the 70% mass of ordinary people.

https://hat4uk.wordpress.com/2017/08/02/analysis-seven-swords-pointing-…

If the concern is business funding then the answer is simple adjust the risk weighting of business loans or double the residential risk weighting to level the playing field. This is a risk related regulatory issue.

However I recall developers managing to do quite well with 10% interest rates up until Councils started treating anyone applying for a building consent like a criminal. That's a separate regulatory issue but it's a part of the problem.

I'm not sure lower interest rates would help, it just offers more opportunity for people to make stupid decisions and escalate asset inflation even further. Could there be a crisis event that requires lowering interest rates? Sure, but why lower them prior to an event that could be years away?

There are a number of factors which will mitigate the current slip in house prices.

Continuing low interest rates is one of them.

In the last few weeks banks have been reducing deposit interest rates quite a bit. This could indicate that they aren't doing enough new lending so don't need the deposits. Also they are less likely to give much of a better rate than what is advertised if you ask them for a better rate. Thwy are down about .25 percent from 6 months ago on deposits of less than12 months.

Mortgage floating rates of 5.95 is very high relative to global conditions, and relative to the NZ OCR.

Cuts are more likely than hikes if any global signicant events hit.

Why would an OCR cut takes rates lower ?

Because as the RBNZ explains "The OCR influences the price of borrowing money in New Zealand and provides the Reserve Bank with a means of influencing the level of economic activity and inflation."

https://tradingeconomics.com/new-zealand/interest-rate

.

Tracking mortgage rates to the OCR

http://www.rbnz.govt.nz/statistics/key-graphs/key-graph-mortgage-rates

While there may be some 'uncoupling' , there is still some relationship.

.

."By affecting overnight rates, the Reserve Bank has a strong influence on short-term interest rates such as the 90 day bill rate and floating mortgage rates."

.

However, as you imply, perhaps a lower OCR will be ignored by banks, as they have realised recently that they can get away with not passing on cuts to their borrowers.

.

The OCR was 2.5% in 2012 2013 yet floating rate the same as current.

Should the floating rate even be at 5.95 when the RB at 1.75. Doesn't seem normal all ready

The OCR was about 7 and floating about 9 at the end of the last boom, how does that work in

Because the OCR has nothing to do with the interest rates when all the banks are owned by other countries !!!! and my prediction is an interest rate rise regardless of what the OCR is doing.

Could there be a lack of competition among lenders? Perhaps if fewer lenders are interested in new lending?

Well I got a pamphlet from iRefi.co.nz who claim be able to get 1 year fixed for 4.09% !!!

fully agree on the rates coming down. My opinion is based on gut feeling not scientific.

I and other investors are grumpy about the National Government for demonizing us. However we have never had it so good. For all the wrong reasons I am doing really well because the rents, demand and property values are up and the mortgage rates are down. This is enabling me to pay down debt as soon as it is accumulated (it goes up whey I purchase another property!) My guess is other long term investors are in the same boat and it is this paying down of debt that is keeping rates low. What do other medium sized investors think?

I also think you are not alone in predicting the likely track for interest rates is down. There is no foreseeable inflation, I think we are at the point in the economic cycle where interest rates are as high as they can go. Don't quote me but I think tradeable is negative so if get a bit of non tradeable slow down then the ocr might need to at near zero; following the same sort of path as other nations with a near zero ocr but minus the drama caused by thier lack of regulation

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.