This is a thought piece. Not a conclusion piece. It’s just that something about recent Reserve Bank forecasts continues to niggle us.

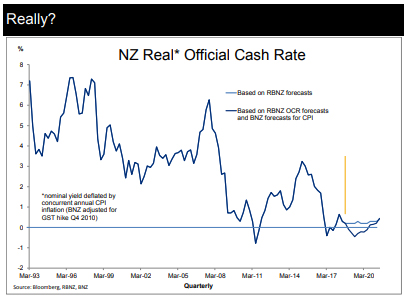

That is, their inference of a near-zero Official Cash Rate (OCR) in real terms, right the way out to 2021.

Yet the Bank has also inferred, by way of other material, that New Zealand’s neutral real cash rate is in the vicinity of 1.50%*.

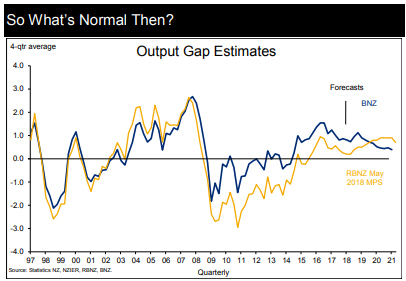

We are having trouble reconciling these two things, especially as the Bank is forecasting a positive output gap.

Indeed, if we can believe the Bank’s current base case projections for the OCR, we reckon New Zealand’s real cash rate will effectively go negative before too much longer. While the Q2 headline CPI disappointed market expectations (and ours), it hardly disturbed our view that annual inflation will keep pushing higher, reaching 2.3% in a year’s time. The pickup reported in core inflation reinforced this, as will wage inflation trends soon enough.

But can we really be heading into an extended period of a negative NZ real cash rate? This prospect could, instead, be forcing us to confront the possibility that;

1. We have it all wrong on inflation. That it will, in fact, fail to pick up, even in the glacial manner the Bank currently projects (thus keeping the real cash rate moderately positive). But this would surely apply pressure on the RBNZ to cut the (nominal) OCR further to the bone, in an attempt to boost annual CPI inflation to 2%.

2. GDP growth won’t live up to the Reserve Bank’s expectations of robustness. There are certainly ongoing risks of this, in our view, including from recent indicators of near-term NZ growth (such as the PMI and PSI). But this would likely make for a slacker economy than the Bank is contemplating, again prompting a reach for the OCR joystick.

3. That the exchange rate will, for whatever reason, be charging higher, doing the monetary work. And to such an extent that the OCR will be forced to run extremely low for longer. But this, also, is not in the Reserve Bank’s assumptions, which actually have the TWI running broadly sideways over the coming period.

4. The NZ central bank is in la-la land with its view of both a positive output gap, and a real cash rate persisting decidedly below its own estimate of neutrality, for a number of years.

5. The RBNZ misjudgment actually lies with the neutral level of the real OCR. Perhaps it is closer to zero, than the 1.50% it officially touts. To be fair, the Reserve Bank has estimated a range of approximately plus or minus 100 basis points on this, while also a slightly diminishing tendency in the mean over time. Nevertheless, this still suggests 1.50% might be roughly as much an underestimate, as an overestimate, of the “true” real neutral cash rate.

Either way, something doesn’t seem to add up.

We are not quite sure how the conundrum is resolved. But a conundrum it is. Our best guess, at this stage, is that New Zealand’s policy rate will need to rise by more than is currently anticipated by all and sundry, providing economic growth holds together and inflation continues to grind its way higher.

Conversely it would probably take a material slowdown in the NZ economy to reconcile with the idea of the real cash rate remaining near zero over the coming years.

Underlying all of this is arguably a deeper clash of ideology – one that we sense all the time in market analysis and commentary. It all boils down to the impact you think interest rates are having on GDP and CPI, above all else.

In one camp are those who think interest rates are playing a crucial role in this regard. And so we should be careful in “normalising” rates, lest GDP and CPI fail anew. Not surprisingly, central banks are invariably in this camp. If they don’t believe in their own tools, who else would be so bold? This way of thinking also manifests in the idea that economic projections hold together only because of the (usually accommodative) role of policy rates. Perhaps there is a bit of this in the Reserve Bank’s latest set of forecasts

The other camp tends to claim that interest rates are well below the point at which they are providing a marginal boost to GDP and CPI (while the system largely heals itself, naturally via the passage of time, not because of prolonged monetary accommodation). But that the degree of monetary accommodation is having a powerful influence on asset prices, along with attitudes to leverage and risk.

The trouble is that, both schools of thought leave one nervous about the way ahead. One says the world economy is highly dependent on very easy monetary policy. The other says the financial system is now highly vulnerable to the removal of such monetary stimulus.

So, in the event that something does come unstuck, in trying to extricate oneself from low interest rates, both camps will probably say “I told you so”. But with one saying we should have never tried, while the other says we should never have painted ourselves into such a corner to begin with.

*see speech by RBNZ Assistant Governor McDermott, “Looking at the Stars” (26 July 2017)

Craig Ebert is a Senior Economist in BNZ’s Wellington dealing room. You can contact him here. This article was originally published here and is reposted with permission.

31 Comments

Craig - you may not have read my comments hereabouts lately, but the essence of them is that money issued as debt, debt is an expectation that the future will repay, and interest is a bet that the future will repay more.

So far so good.

But it's consumption of finite parts of the planet that we're talking about biggering, which takes work, which requires energy - also currently from finite planetary sources. So at some predictable point, the future would start to beg unable to underwrite, and the shortfall would spread exponentially.

This process has probably been coming since about 1980, but narrow visions, local focus and specialisation blindsided most folk. But the debt has never been bigger, the future has never been more resource-depleted, and there is no room for positive interest-rates in that scenario unless the banks are displacing the wealth from someone really productive.

Maybe you might have to re-train? :) The money-lenders might have been thrown out of the temple for good reason.....

indeed pdk. In very simple language I recall attending an investor seminar in the 80’s the main thrust of which was the power of compounding interest in terms of an investment outcome And that is true enough, most would agree. But what happens when it is turned around and you have compounding debt. Only one answer. Eventually default.

The universe is to all intents and purposes infinite so therefore the resources available to humanity are to all intents and purposes infinite. Does that resolve your dilemma?

Hardy - no it doesn't. My guess it that that was Cameron's underlying point with Avatar.

We have trouble keeping space programmes going, and we haven't been back toi the moon in a long time. Even at light-speed, with as much cargo capacity as our current oceanic shipping fleet, you're too late already already.

Which is why it's time to either have a John A Lee type talk about the state (us) owning the issuance of capital and the fee charged for it, or to legislate the banks to cease charging compound interest. Other cultured do this - you can't demand compound interest from folk with two camels, a rug and a teapot in the desert. The only way they could repay would be to sell the teapot to each other, for more each time. The bank could loan each next buyer, all you'd need was an enthusiastic teapot-valuer to justify the business case.

Oops, I just described the selling of houses to each other in the wertern world these last frenzied years.

What we need is the charging of a flat fee, upfront. Yes, it would curtail business, growth and GDP. But the planet is doing that to us now, and it is better we fit in than that we crash. If the banks can adapt, fine. If they can't, they just ran out of business case themselves.

Per general relativity, the sum total amount of energy, and mass in the universe is equal to the number 1. We can exchange it into various forms, but the notion of the universe being infinite does not integrate with our models of it.

I think RBNZ biggest misjudgment and Governments in general was expecting that the China capital flow would carry on forever and now it looks as though we're headed for another Asia recession (Caused by China's over spending and Trumps tariff war) which may not be a bad thing, recessions happen all the time, you think we would have learned by now.

So yes it is in the banks (including the Ozzy banks) interest to drop their rates otherwise the property market will stagnate and then crash. If the market is allowed to crash that means lots of negative equity and then home loan defaulting = property repossessions. This is very bad news for banks.

logically the banks need to drastically drop their rates to help prevent negative equity so people can continue to borrow and afford to pay their loans. Bad news for savers though.

If you want to see just how low the mortgage rates need to drop just take a look at the UK. A first time buyer with a 20% deposit can get a 1.64% 2 year fixed mortgage rate. Where as here you're looking at at almost three times at rate here. https://www.money.co.uk/mortgages/first-time-buyer-mortgages.htm

Since the Australian market is also starting to feel the falling property market pain we'll probably have to follow their lead.

Article: Home prices across Australia's major cities slipped for a ninth straight month

https://www.smh.com.au/business/the-economy/home-prices-fall-for-ninth-…

Oh and by the way, RE's are going to have to drop their commission rates too, if 1% is good enough for London RE's (That includes all the marketing) then it's good enough for the likes of you.

this puts it well:

https://steadystate.org/the-negative-natural-interest-rate-and-uneconom…

Thanks for the link, darn good article pdk

Interesting read!

Shall we become hyper-Keynesians and push GDP growth to maintain full employment, even after growth has become uneconomic?

Or shall we back off from growth and seek full employment by job sharing, distributive equity, and reallocation toward leisure and public goods?

A key point some miss whenever there is discussion of why it's important to ensure more of the population is getting more of the pie and is able to circulate it through the economy.

If increasing GDP makes us worse off we will not admit it, but will adapt to the experience of increased scarcity by pushing GDP growth further. Non-growth is viewed as “stagnation,” not as a sensible steady state adaptation to objective limits. Stimulating GDP growth by increasing consumption and investment, while cutting savings, is the only way that hyper-Keynesians can think of to serve the worthy goal of full employment. There really are other ways, and people really do need to save for security and old age, as well as for maintenance and replacement of the existing capital stock. Yet the Fed is being advised to penalize saving with a negative interest rate. The focus is on what the growth model requires, not on what people need.

Yet people are clamouring for this bad approach in order to protect the value of their inflated asset portfolios...

"Got mine. F you lot."

Good article and thanks for the view points which are well considered. I see Goldman Sachs see rates rising as early as Q1 2019, but I guess Goldman's positions are purely speculative on currency movements rather than actually being in the hock to a load of mortgage debt, so they will be talking rises (keep the currency strong) while their clients' sell out of NZ dollar positions. The lending banks however, BNZ amongst them will probably want to posture to the RBNZ for rate cuts to slow the defaults that CJ099 alludes to. What will happen? My guess, and it is just a guess is that the Reserve bank will cut again (under pressure from the Aussie 4). Mortgagors will be handed a lifeline of time while we cut the dollar loose to fall against the world. There will be imported inflation but it shouldn't matter too much as most of peoples income will be spent on servicing the mortgages anyway... 2-3 year stay of execution before rates then sky-rocket to bring the NZ dollar back from its near Argentinian status! House prices will fall all the way through despite the lower rates as incomes are squeezed and fewer buyers take the risk..

The banks will also tighten who they will lend to, all the while BNZ's Tony Alexander will be out on his bike talking the market up with his 19 reasons philosophy from 2011 (which he still thinks applies after the boom has passed), all in an attempt to slow down the pace of price falls and the reduction in new loans being written.... Teaser rates will get very very attractive.

https://www.youtube.com/watch?v=HnnmmQb1XO4&feature=youtu.be

Was it Nero who still fiddled whilst Rome burned? Watch the video and picture TA with a fiddle doing a little jig.

Well Nic in our more modern times we had something of the equivalent perhaps as a leader of similar, shall we say build, fiddled while Christchurch crumbled & colleagues in government with their togas over their eyes with a view to housing and other basics for the plebs.

You're right Foxglove. All the lessons were there to be learnt from the Northern hemisphere banks errors of the 2000's, However very loose regulation has created a bubble where 1/3 of the country (the third that carry an average $400,000 in mortgage debt) are now at risk of a major wobble in the economy.

8 times multiple of income mortgage anyone? Interest only perhaps? I still see a major lender going to the Aussie government before the end of next year.

A compelling narrative - property market here in for a tough decade.

Hmmm. Maybe the concepts are deceptive. There is an argument that all this angst about setting interest rates is best solved by just using the current 2 year government bond rate. That, of course, relies on the ridiculous notion that the crowd knows best, that market participants are not stupid. Obviously that is a completely unacceptable argument if you are a highly paid bureaucrat. Why do we need these authority figures to intone their serious deliberations at us? The chances of them actually really knowing best are not likely to be high. There are some hilarious comparisons between their projections and what actually happens, here and elsewhere. "Sub prime is contained", anyone?

https://www.mcoscillator.com/learning_center/weekly_chart/bond_market_k…

Well that is the rub fair enough. To return slightly, to my above theme, we learnt very quickly in Canterbury

2010/11 that everybody was an expert on a particular EQ after it happened. And then there other examples commercially. Remember Fortex. Everybody pulled the balance sheet apart and said I told you so after the insolvency. If and when we have another GFC meltdown there will be exactly the same parade.

As someone who really struggles to understand a lot of what is being suggested, I understand that the local cash rate is a nonsense. We borrow off those who are bigger than us, who borrow off those who are bigger than them, who sell debt from thin air. My point being we are literally at the bottom of the food chain here. The UK situation is interesting. They are totally, politically and economically confused right now and I'm not sure how their plight is our plight, although recent noises as to their interest in our side of the planet are interesting. Back to my original concern, I'm a little bearish just now, I have to admit, but then I've been skeptical about QE since 2009/10. At first I thought it was quite a wonderful thing, but then realised what was really going on. How many layers of debt can we live with and for how long? Someone's going to get hurt.

Text book deflation

Since the overriding goal is to identify the severity of monetary disruption, it makes sense to start in metals. Textbook deflation is often a commodity affair, so copper and gold being two parts of money and economy are as good a first intelligence as any. As you can clearly see above, there is an overall uniformity in both that matches pretty well the history of the last ten years.

http://www.alhambrapartners.com/2018/07/20/the-difficult-wargame-of-sor…

Text book deflation

Since the overriding goal is to identify the severity of monetary disruption, it makes sense to start in metals. Textbook deflation is often a commodity affair, so copper and gold being two parts of money and economy are as good a first intelligence as any. As you can clearly see above, there is an overall uniformity in both that matches pretty well the history of the last ten years.

http://www.alhambrapartners.com/2018/07/20/the-difficult-wargame-of-sor…

There is just no correlation whatsoever with the more than half a quadrillion in assets now sitting on the BoJ’s books and consumer prices in Japan. Core rates either suggest a restored “deflationary mindset” or, more likely, common elements with other global economies – the reflation/dollar crisis cycle of the post-Great “Recession” eurodollar decay.

http://www.alhambrapartners.com/2018/07/20/the-clowns-over-the-corrupt/

The path they’re heading down is a disaster, much like the ECB. The ECB is the only buyer of govt debt and there is no way out as no one else will offer debt at those low levels. The whole reason they started this moronic policy was to stimulate growth. That obviously didn’t work as debt is too high to start with and govts are consuming an ever increasing proportion of the economy through taxes, thereby reducing disposable income and economic activity. This will only get worse. In addition, this kind of policy hasn’t even worked once in history. We might as well let some primary school kids take the reins and we’d probably be better off.

Two thoughts....its hard to spend in an inflationary manner when due to high debt, mortgage or otherwise, rental costs or precarious living theres very little spare cash or certainty with which to do so...

Interest rates...lower rates are deflationary on costs which removes a reason to raise prices...so if we all got generous wage rises that could add some much needed inflation to the economy....

I believe policy makers are seriously underestimating inflation. There are four major factors that will bring it back with a roar.

(1) Oil and petrol prices. International prices are up significantly and will be more so if Iran’s supply is blocked. Domestically the government is adding what 5%-10% depending if you live in Auckland.

(2) House prices and rents - enough said, these will put serious pressure on wages. Either prices drop or wages go up, I predict a combination of the two.

(3) Public sector wage pressure - this is going to be massive across nurses, doctors, teachers, police, etc, etc. The private sector will be forced to match these increases or do without workers.

(4) The exchange rate. Baring Donald Trump interest rates are going up everywhere else. This will put downward pressure on the exchange rate pushing up inflation.

So yeah, I think growth (nominal at least) will be high and inflation will be high enough to force the reserve bank to increase rates. Once they do that will resolve your conundrum right?

For a start oil prices are a construct of Wall street and the big oil companies.

Asset prices are the result of low interest rates, low interest rates have given us high debt.

Public wage sector wage increases will not be inflationary, the Government will either spend less elsewhere, raise taxes or borrow.

I don't think the exchange rate will protect us in a race to the bottom, Brazil and China are trying to support their currencies, a weak currency is a sign of a weak economy.

Asset prices have not gone up due to increased productivity but due to speculation and easy borrowing with the cheapest interest rates in 5000 years.

The problem is that everyone expects a recession to be short followed by a recovery, thats whats different about the coming crisis.

\

Not a subject matter expert on economics, so forgive me but, you say this coming crisis is different and I would like to understand that better.

Can you elaborate on that please? Is it due to the issuance of debt as capital by banks? I'm barely familiar with the A+B theorem of social credit, which more-or-less predicts this situation and outcome - is it our reluctance to reform away from debt-as-capital which puts us here?

Modern economics is a discipline that has been invented in an era of surplus resources, in particular energy. It's foundation, and models, assume infinite resources. Since we are coming to the end of the resources, the flaws are starting to show in the models. The very nature of interest itself sets up the constant need for growth.

Does anything that is not speculation back up this perception that inflation is underestimated? Inflation is more likely to be over-estimated, as far as I can tell.

If we look at National's performance, ie; in their first 100 days removing the zero unemployment policy target from the RBNZ charter, that would seem to be in fear of inflation based on Philips curve responses and the formulae defining NAIRU. I thought the Philips curve was an empirical observation, not something to be interpreted as causative relationship between unemployment and inflation. Basing monetary policy on NAIRU also seems outdated, and I'm still looking for evidence of this relationship comments like yours beat on the drum of fear regarding. The best I can find is the Philips curve...

The error probably lies in an overestimation of the output gap. Gdp growth will turn out to be the disappointment IMO.

Inflation is dead - in the pre-2008 era sense of needing to be beaten to death by rising interest rates/OCR at every turn.

There are quite a few Turks and Venezuelans who would disagree with you.

Failed States are outliers

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.