Special events are the mainstay of news but too often economists also give excessive weight to them.

This appears to be the case with Auckland Council's (AC's) chief economist's assessment of the impact of the Unitary Plan. Based on an article on Interest.co.nz, AC's chief economist is attributing too much to the Unitary Plan and not enough on other factors (e.g. building by Housing NZ, Special Housing Areas and section market developments).

A desire for higher density housing near rapid transport routes appears to taint AC's economists' analysis.

The Unitary Plan is having an impact and more so than I expected. But it doesn’t take much analysis to show that it isn't having anything like the impact that seems to be claimed by the AC's economists whose analysis seems rife with attribution errors.

This Raving provides some debunking analysis including an assessment of Unitary Plan type developments in the pipeline.

Is the Unitary Plan the be-all and end-all?

The chart below is from an interest.co.nz article that reports insights provided by Auckland Council's chief economist. The article includes a number of interesting insights but I am wary of AC's chief economist's interpretation of the impact the Unitary Plan is having. An attribution error appears to be at work (i.e. putting too much focus on the known special factor and due to substandard analysis not taking into account sufficiently the impact of a range of other important factors).

The following is a quote from the article:

During the months preceding the [Unitary] plan becoming operative in November 2016, land owners held off lodging their consents until they could be certain about the level of densification allowed on their properties. This hesitation lingered for the nine months following the Plan becoming operative. Norman [AC's chief economist] said the pick-up is notable now, with the growth in Code Compliance Certificates being issued rising to 28% per annum, as we find ways of getting projects signed off quicker.

It makes sense some developers held off waiting for confirmation of the plan, but other factors and even much more important ones were involved.

AC's chief economist would appear to be saying that the temporary stalling of upside in Auckland new dwelling consents in 2016/17 was mainly due to developers' behaviour related to the Unitary Plan and that the subsequent increase in consents highlighted in the chart can be mainly if not fully attributed to the Unitary Plan. Maybe AC's chief economist was quoted out of context or not in full but my interpretation of the quote above seems justified based on AC's economists having in the past put too much emphasis on the Unitary Plan based on insights provided by an earlier and also interesting interest.co.nz article.

As an aside, the article accessed by the link above references some bizarre analysis done by the AC economists comparing recent developments with those in 2010 when the housing market was still being impacted hugely by fallout from the financial crisis including funding for developers undertaking more intensive housing developments largely drying up. The comparison with 2010 when very different factors were at work suggested to me the AC economists are on a mission that is likely to blind the quality of their analysis. They seem to be starting with the conclusions they want and warping their analysis to fit the desired conclusions.

What other factors could in part explain the latest increase in Auckland consents?

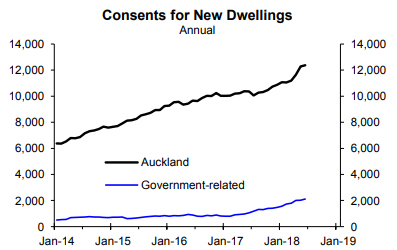

In terms of the increase in Auckland new dwelling consents highlighted in the first chart, factors other than the Unitary Plan will account for over half of it; factors the AC economists seem to overlook in their enthusiasm for the Unitary Plan.

From the end of 2016 when the Unitary Plan became operative until most recently the annual number of Auckland new dwelling consents increased by 2,343 (23%). Clearly some thing or things have provided a major boost. Over the same period government-related consents for new dwellings that are dominated by Housing NZ consents, the vast majority of which are likely to have been in Auckland, have increased by 1,294. It is possible almost half of the increase in Auckland new dwelling consents since the Unitary Plan was partly operative in late-2016 is due to building by Housing NZ that was already in the pipeline and mainly related to Special Housing Areas.

The appendix has a map showing the locations of the 154 Special Housing Areas approved between 2013 and 2016. Many of the SHAs are in existing urban areas including a number in the vicinity of rapid transport routes. Quite a few of these are Housing NZ projects but many aren't. Progress with SHAs will include suburban apartment projects that are likely to account for at least a moderate amount of the increase in Auckland new dwelling consents since late-2016.

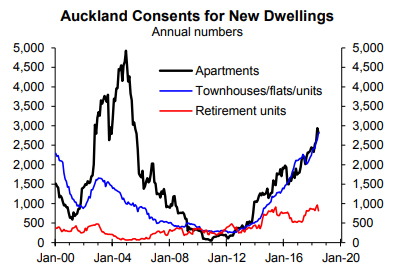

Since late-2016 there have been large increases in Auckland consents for apartments as well as for townhouses/flats/units (next chart). Housing NZ activity will account for a reasonable amount of the increases while private apartment developments including some in SHAs are likely to partly explain the sustained increase in consents for apartments.

Thorough, unbiased analysis of Auckland consents suggests increased building by Housing NZ and the boost to building apartments and maybe to some extent townhouses by SHAs most likely together account for more of the increase in new dwelling consents since late-2016 than the Unitary Plan that the AC economists seem too ready to attribute most of the credit.

This issue can also be approached from the perspective of what is going on at the coalface of the market (i.e. are there lots of Unitary Plan style developments in the pipeline?).

To answer that question the following is an extract from the September quarter Auckland Barometer report that provides quality, unbiased insights into prospects from Auckland residential building, house sales and house prices. In my biased opinion it should be a must have for firms, organisations and investors involved in the Auckland market.

Extract starts next [words in parenthesis added].

An article in the latest Property Investor magazine suggests the Unitary Plan is making it much easier to build on existing sites and gave some good examples. Being housing investors we get the magazine but it is a pay-to-view publication so we can't include the content here. Instead we searched the two main real estate websites for examples like those quoted in the magazine to see how prevalent they were. There were examples but in the context of the size of the Auckland market the number was relatively small; raising questions about the impact of the Unitary Plan. We focused on old Auckland City where this sort of development should be more prevalent.

The links below provide examples of what appear to be Unitary Plan style developments on TradeMe and www.realestate.co.nz based on a search of all the 299 listings for old Auckland City that appeared when we used "brand new" on TradeMe and only the first 100 of the listings on the realestate website that appeared when again we used "brand-new" as the keywords; the vast majority of which weren’t brand new. [Only one of the first 100 listings on www.realestate.co.nz after we narrowed the search criteria beyond just searching for "brand new" was for a Unitary Plan style development, so we stopped searching]. We used Google maps to check what used to be on the sites.

Four new houses on what was an elongated two dwelling site:

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1720303983.htm?rsqid=2778e3a8966c49498a244f dba0a6ff79Five new houses on what was a one-house site:

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1708541847.htm?rsqid=2778e3a8966c49498a244f dba0a6ff79Probably more than two new houses on what was a one-house site:

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1701818818.htm?rsqid=2778e3a8966c49498a244f dba0a6ff79Several new houses but this may be on what used to be more than one site with the ad only being for one new dwelling:

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1705195733.htm?rsqid=2778e3a8966c49498a244f dba0a6ff79Four dwellings on what was a one-house site:

https://www.realestate.co.nz/3361154The examples above are from different parts of old Auckland City. We also found some listings for mainly older dwellings on larger sections advertised as having development potential, suggesting real estate agents are starting to respond to the Unitary Plan, like this one but there were better examples:

https://www.realestate.co.nz/3374174The experience in Hamilton last decade when the council allowed developers to build 3-4 retirement units on existing housing sites potentially helps put what is currently happening in Auckland as a result of the Unitary Plan in perspective. As part of research we did for the council in 2008 we came across far more examples of developers building 3- 4 retirement units in Hamilton than we have found examples of Unitary Plan style developments in old Auckland City on the two real estate websites.

The search on TradeMe also found examples of new dwellings for sale in 3-5 story apartment buildings that may relate in part to the Unitary Plan [but may in part relate to SHAs]:

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1705150769.htm?rsqid=e9b56692e2a74c18b8377 ee82b8c8db2

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1678875880.htm?rsqid=e9b56692e2a74c18b8377 ee82b8c8db2

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1695545736.htm?rsqid=c8e15e1afd8c451a826146 c31158fd56

https://www.trademe.co.nz/property/residentialproperty-for-sale/auction1658126527.htm?rsqid=5179b9e5198b41bcaf1823 99ea7a9a65

"Politics" to the fore in one of the AC's chief economist's comments

AC's chief economist has a clear preference for brownfield development near rapid transport routes over Greenfield development. In the context of the majority of the recent increase in consents for new dwellings being in brownfield not Greenfield areas he is quoted as saying:

Given the increased choice the Unitary Plan has delivered, guess where people want to be? They actually want to be close to their jobs. They don’t want to sit in traffic for an hour to get to work by building 40km away.

To me this is a "politically" motivated comment based on an overzealous desire to force people to live in higher density housing near rapid transport routes when market research suggests this isn't what most people want.

The fact a high percentage of the recent increase in consents has been in brownfield areas shouldn't be interpreted as a clear indication of preferences because other factors have contributed to this outcome: (1) the location of Housing NZ building that has little if anything to do with where people want to live; (2) the location of SHAs that reflect a range of factors and not necessarily so much where people want to live; and (3) council policies that contributed to section prices rising to levels that priced many people out of buying new houses in Greenfield areas (chart on the next page).

Attributing the 2016/17 stalling of upside in consents to the Unitary Plan misguided

Upside in Auckland consents for new dwellings stalled in 2016/17 and it would appear AC's chief economist is largely attributing this to the Unitary Plan based the Interest.co article commentary:

During the months preceding the plan becoming operative in November 2016, land owners held off lodging their consents until they could be certain about the level of densification allowed on their properties. This hesitation lingered for the nine months following the Plan becoming operative.

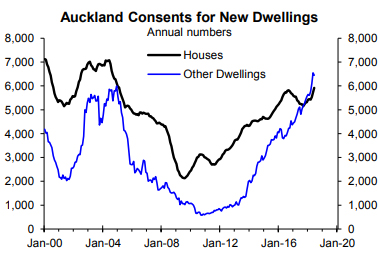

The reality is that falling consents for new houses was the main reason for the stalling of upside in Auckland total new dwelling consents in 2016/17 while consents for other new dwelling that should have been impacted by the Unitary Plan continued to surge (next chart).

The "game-changing" factors were partly behind the 2016/17 fall in consents for houses (i.e. the moderate market-led increase in mortgage rates that started in November 2016, the October 2016 lending restrictions aimed at investors and are likely to have impacted on some investors buying new housing and tighter bank lending criteria).

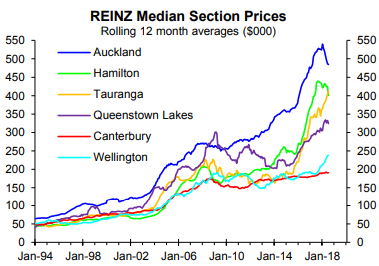

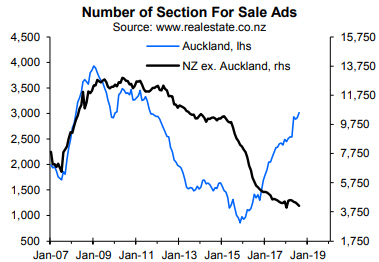

Surging section prices (next chart), a falling supply of sections (second chart below) and especially a dwindling supply of affordable sections (third chart) will have contributed to the 2016/17 fall in consents for standalone houses.

The number of section for sale listings on the main real estate website won't be fully reflective of overall market developments but the huge fall in listings for Auckland relative to the rest of NZ between 2011 and 2015 will partly reflect council policies to limit Greenfield development and boost the cost of developing new sections (second chart in the adjacent column).

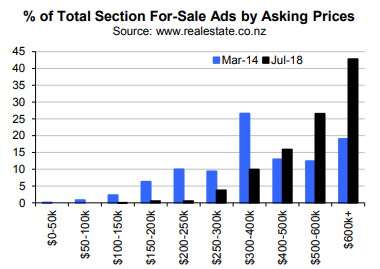

In terms of more affordable sections, based on the March 2014 survey 29% of the section for-sale Auckland listings on www.realestate.co.nz had asking prices of $300,000 or less while by July 2018 it was 5% (bottom chart adjacent column).

The building of standalone houses is making a comeback not fading away

Something AC's chief economist obviously wasn't keen on pointing out is that there has also been resurgence in consents for standalone houses this year (chart previous page). Based on the insights provided by AC's chief economist you would think building of houses was fading away.

Things are changing in the Auckland section market. Auckland section for-sale listings have increased dramatically since early-2016 vs. further downside in the rest of NZ (second chart, adjacent column) and the Auckland median section price reported by REINZ that should be broadly reflective of market-wide price behaviour has fallen (top chart, adjacent column). These developments will most likely reflect a lagged impact of SHAs.

With the supply of sections in the Auckland market increasing significantly and signs section prices may be falling it should be no wonder that consents for new houses are making a comeback. If the council and government did what was needed to significantly reduce section prices - something the Minister of Housing says he plans to do (Yeah. Nah!) - we could truly see what types of housing most people preferred to live in.

Consistent with the market research I've seen I would expect the preference to be weighted more towards standalone houses even if they are on small sections in suburbia than to higher density housing near rapid transport routes.

A number of factors contributed to upside in Auckland new dwelling consents stalling in 2016/17, to upside resuming in the second half of 2017 and to the changing mix of consents. I haven't seen mention of these factors in the media by AC's economists; which I suspect reflects more what the media is fed than a bias in the coverage.

We will investigate whether SHAs are contributing to in increasing supply of less unaffordable sections in the Auckland market. This will most likely be released in a special report for clients rather than free in a Raving.

19 Comments

Good article, Rodney. I had the distinct feeling of cheer-leading in the AC 'economists' piece, and now you've exposed the 'find me the Man, I'll find you the Crime' sort of skewed 'research' one expects of essentially political operatives. Congratulations for calling it out the way you've nailed it here.

But why would they lie about it? If the unitary plan is indeed driving new building, doesn’t that imply:

A) Auckland councils old planning rules were stifling building and causing significant social problems (I hope those planners feel good about themselves)

B) the lame unitary plan that Auckland council proposed was luckily rejected and rewritten by the independent panel to help this building occur. How can the council take any kudos for that?

To me if the unitary plan is a success it just shows how much problems the council had actually caused.

In 1071, the up-zoning of single house sites to subdivisable sections has had an impact. 800m2 sections with older homes are purchased for ~ $2 million, divided in two then a 280m2 plus house is built on each 400m2 section and marketed for > $2.5 million. Not exactly affordable but it is increasing supply.

It's happening, but they're often ugly sh*tboxes, making 1071 quite an unattractive suburb compared to other Auckland coastal areas (Pt Chev through St Mary's Bay, Devonport through Takapuna etc). The "heritage" in 1071 is generally ex-state housing and/or ugly brick &tile sausage flats from the 1970s. There's possibly only a handful of homes in Mission Bay that i'd aspire to own on an aesthetic basis.

Popular with the Twyford-sounding market though - noticed the yellow Lambo parked up in Coates Ave?

The only time I have visited Okakei was on the 'rat run' to work some years back. It wouldn't surprise me if there was a Lambo up there. Probably a few sneakers on the power lines as well. Those types of places, including sausage flats aren't the types being subdivided and certainly wouldn't be marketable at a premium.

Nice article, well done.

These developments will most likely reflect a lagged impact of SHAs.

Also 2016 changes to the Unitary Plan removing the urban boundary restrictions from every town in the region (except Auckland) - allowing private sector "live zoned areas" to be developed in and around rural settlements. There has been a significant increase in these developments.

https://www.aucklandcouncil.govt.nz/plans-projects-policies-reports-byl…

So you are saying around half of the increase is due to SHA activity rather than the Unitary Plan.

But wasn't the main thing a SHA enabled, was to apply the Unitary Plan rules, even though they weren't yet operative. So activity that is attributed to the SHAs, is in fact due to the Unitary Plan rules?

That's right, the SHAs effectively brought forward development rights under the Unitary plan.

So it's a bit disingenious to say its the SHAs, not the unitary plan

I was thinking the same thing when I was reading through this.

Naturally I was glad to realise I wasn't going crazy when you highlighted the same thing.

Ironic that he chastises AC for bad science (foregone conclusions) and then displays the exact same thing..

TradeMe searches as evidence of development patterns?

Poor understanding of the AUP provisions.

Surging median section prices - which represent the now capitalised development potential.

Falling sections for sale - I'm surprised that due to his love of correlation he didn't notice that turning points coincided perfectly with AUP timings; announcement of Unitary plan process, Draft plan, and final implementations.

Sure the AC analysis wasn't that great, but Righteous Rodney has once again missed the mark completely. How he ever sells paid content bewilders me.

I think some of his work is good, but this is really poor and misinformed. Also while hnz development is significant, it's still very much in the minority. Also much of the hnz development couldn't be done without the unitary plan as a planning basis.

Auckland Council AUP (non-SHA) changes opened up a lot more potential development sites than the SHA activity, but the SHA changes occurred a couple of years prior to the AUP changes. What gets attributed to which varies with analysis.

To me this is a "politically" motivated comment based on an overzealous desire to force people to live in higher density housing near rapid transport routes when market research suggests this isn't what most people want.

This is unduly generous to the policies of Auckland Council. Auckland Council policy forces suburban development to occur 40 km away.

Market research can be easily swayed in whatever direction desired. Want to show people dislike high density near trains - just ring landlines and only get oldies.

For me, the desire to put in a new bathroom, get a CCC and rent out the previously unrented unit was nothing at all to do with the unitary plan. It was solely that my rates have skyrocketed. Lots of infill housing will be due to this. ie It was already allowed under the old plans, but the huge rates bills (and high property prices) are now a very strong driver.

High costs are normally considered the exact opposite of strong drivers for property investment. If you were a new entrant to the market and wishing to do an infill build you would be better off investing in any other city apart from Auckland, because of huge rates bills and high property prices. This reason (along with foreign immigration) is why Auckland has a pro-longed housing crisis.

Auckland rates arent much higher than other NZ cities are they? Our rates bill is only 0.25% of the properties value, hardly enough to base an investment decision on.

All I know is that

1/ The current value of my section is ridiculous.

2/ The direct rates may be about 0.25% of its value, but this is about double what it was under the North Shore city council. Plus there are the rubbish bin, water and petrol taxes on top of this.

3/ I am very scared of what the central rail link costs will be. The council/ govt seem to think that this project is necessary whatever the tender prices come in at. Therefore rates will increase by some huge additional amount in future years plus there will be the ever increasing interest costs of the on/off balance sheet max debt level.

It all adds up to: I have to do something. I have to do it now. So I did it.

As I say, nothing to do with unitary plan at all.

I'm wondering if the figures for new properties on brownfield sites have had the original demolished houses netted off them.

I don't think so, think it is solely the number of new consents. But it is more useful this way, it is a consistent measure across a wide number of different cities to not count the demolitions.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.