The founder of Harmoney, New Zealand's biggest licensed peer-to-peer (P2P) lender, says he can't see a viable P2P lending model in New Zealand which is why Harmoney has started lending its own money.

In a podcast with Peter Renton of the US-based Lend Academy, Harmoney's Neil Roberts says since launching with a Financial Markets Authority licence in 2014, Harmoney's "had reason to question the regulatory environment in which we operate." This, he says, has led to a move to simplify its funding model.

"We operate as a peer-to-peer lender, we’re licensed as a peer-to-peer lender with 18,000 lenders operating on our platform. The regulatory environment just threatens that business model just because of Harmoney’s ability to earn so where we see our future is going on balance sheet, we started that journey in December," says Roberts.

He also talks of "unclear federal laws that don’t perhaps work well together."

Thus, Roberts says, since 2015 Harmoney has; "Been slowly operating a pivot and moving to lending our own money which we started to do December last year and we’re rapidly, you know, picking that side of our business up because the regulations, particularly in New Zealand are such that we don’t see a viable model for us doing peer-to-peer lending way into the future and we are sort of managing that and have been for some time."

On the legal front the Commerce Commission successfully argued at the High Court Harmoney's platform fee was a credit fee, despite Harmoney's opposition. Roberts has previously told interest.co.nz that prior to "pioneering" P2P lending in New Zealand Harmoney "went out and got the best advice that you can get, we believe, in the market place from Simpson Grierson."

Roberts' comments come with Harmoney expected to soon reveal a capital raise of more than $30 million involving several investors. In July Harmoney posted a maiden annual after-tax profit, courtesy of adoption of a new accounting standard that boosted its after-tax earnings by $7.5 million. Harmoney reported a $7.22 million after-tax profit for the year to March 31, compared with an after tax loss of $1.84 million the previous year.

Meanwhile Roberts also talks about why David Stevens is taking over as Harmoney's CEO from himself and co-CEO Brad Hagstrom, hinting at a potential share market listing, - in Australia.

"Yeah, so the first thought or what I’ve always thought is that a lot of founders flounder when they get to the public markets and in this part of the world, the deep pockets of capital are in the public markets. As you know, Peter, companies tend to go a little sooner to those markets for that reason and, you know, the ASX is trying to attract those that perhaps don’t have the market cap to go on the NASDAQ. The source of super in Australia, is I think $2 trillion or some crazy number like that, so it’s a huge source of capital to access," says Roberts.

"So, for me, I’ve always felt that, you know, I wouldn’t want to be a public market-facing CEO for two good reasons. I don’t think I’d be very good at it and I don’t think I’d enjoy it."

In March Harmoney announced a $50 million securitisation programme in partnership with BNZ. Stevens tells Lend Academy Harmoney's "looking to roll out another one in New Zealand with another bank and then also a couple in Australia as well in the coming months." This, Stevens says, will give Harmoney "some really good diversity of funding and also allow us to maximise the returns."

Since launching in September 2014 Harmoney says it has facilitated more than $1.2 billion of loans, matching lenders with borrowers online. The biggest chunk of lending done via Harmoney is debt consolidation. Harmoney says it has arranged more than A$100 million of loans in Australia.

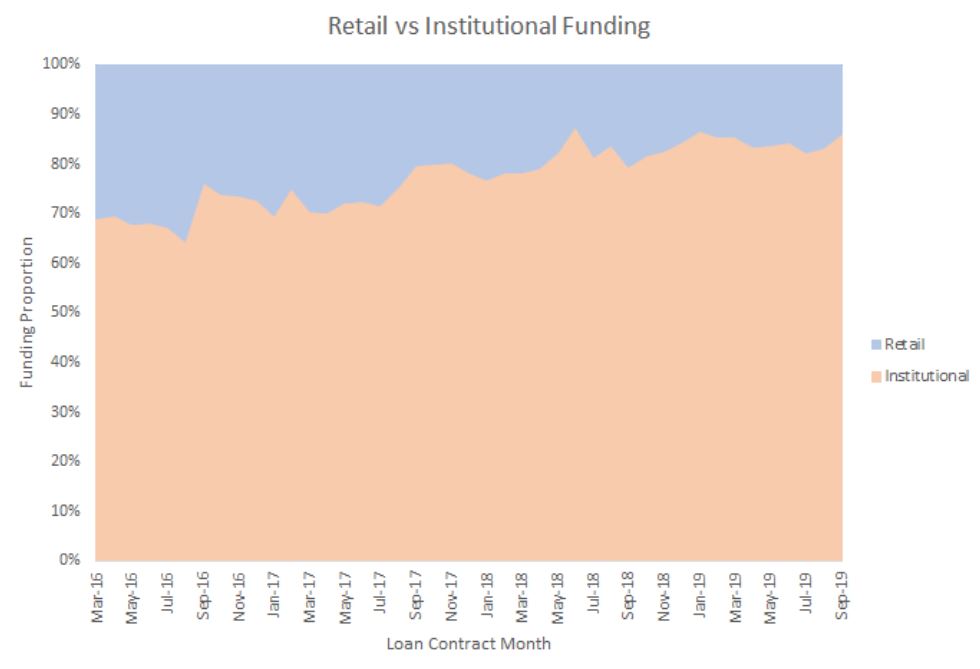

Harmoney's biggest shareholders are the Neil Roberts Trustee Company Ltd with 39.74%, Heartland Bank with 16.92%, Trade Me with 15.13%, and P2P Global Investments Plc with 7.81%. Almost 80% of Harmoney's funding currently comes from institutional investors including Heartland Bank and TSB, with the balance from retail investors.

*This article was first published in our email for paying subscribers early on Tuesday morning. See here for more details and how to subscribe.

21 Comments

I think you are right!

The route cause is because the monetary system is broken, having been gamed by the US Federal Reserve owned not by the government, but people like the Rothchilds, etc.

Their game of printing money no longer works, as they have enslaved the masses with debt who cant afford to pay interest let alone principal back. I personally like your model, as its sustainable, however you probably entered the game to late to get the scale you are looking for.

The returns on lending presently are too small, and do not reflect the forward risks. This is creating a misallocation of capital to assets that are overpriced already. My money is on sustainable industry practises, which governments should be encouraging, rather than get rich quick scheme margin trader and traitor Jonkey engineered.

It's surprising as Harmoney is one of the few places you can get a decent return - sure as hell better than a term deposit. Probably in part Harmoney's own doing - I've heard as an investor it is hard to find loans to fund as many are snapped up first by the retail investors.

Exactly.

The true P2P lenders get to choose from "what's left" after the institutional lenders have picked over the loan applications - the higher risk stuff.

It's hard to suggest Harmony is a P2P lender at all, when 'a peer' is supposed to be a borrower and a lender of equal standing?

"Almost 80% of Harmoney's funding currently comes from institutional investors"

I am sounding like a broken record, but the regulatory environment means that the incumbents are rewarded and the new players with new ideas are stomped out. So with the way things are going there won't be peer-to-peer lending in NZ. I am sure the Commerce Commission and the FMA are mighty pleased by their efforts. Who benefits from this myopia, banks, and who misses out, the general public.

New Zealanders complain that we are beholden to the big 4 banks and that we can't offer proper competition. Here is part of the reason.

Whenever the market isn't working the answer is always "more regulation, because see, the market isn't working".

Of course they never consider that the market might not be working because of the existing regulations which by and large benefit large corporations. Instead they just add more complex and costly regulations which further benefit the banks and hurt Joe Blo.

Becoming just another loan shark then ?

Will they open a branch along with all the others in the Otahuhu shopping parade , where they are more loans sharks per square KM than anywhere I have ever seen on the planet ?

Of course this p2p model was never going to work , any sensible person who has saved his hard-earned money one Dollar at a time is not about to lend it to some idiot who has got himself up to his eyeballs in debt

And other problem I suspect is at play, is that credit applicants behaviuoral scores are not as reliable as lenders think , the applicants tell porkies , making often misleading statements about their true financial position .

Its a minefield lending to the poor and indigent , and one should not be start-struck by the "illustrative yields"being touted , the default risk is very, very high , and you can lose it all

I've been hovering at around 12% return on Harmoney, and I've been lending on it for about 3 years. It's very hard to lose it all if you only go for one piece of each loan (each piece being $25). The only catch is that there aren't enough loans that you can invest your money very quickly.

Complete rubbish as usual Baotman. I've had a few thousand dollars in Harmoney for a while now, and unless you go out of your way to pick bad loans there is no way you could lose it all, unless harmoney itself is nothing but a complete scam.

If you have $2500 invested at $25/loan you are invested in 100 different loans, what are the chances of a 100 different loans all falling over?

My writeoffs are running at about 10% of interest received, and all were from loans i invested in early inthe piece when I was to busy trying to get the money out there earning for me and wasn't being selective enough in who I lent too. All were E rated borrowers, no write offs in the A-D range so far., and a fairly stable RAR of around 11.5%. The big problem is Harmoney themselves hoovering up all the loans, there aren't enough loans to invest in anymore, otherwise I'd be adding more funds.

Me thinks Boatman is a lobbyist, paid by the banksters.

Increased entry and running costs suit the status quo, and the banksters in the game with scale this plays into their hands.

Most of the best investments needing extra capital get soaked up by existing networks. Thinking there existing accountants will have a pool of other clients to tap into. Harmoney is essentially fishing behind the net, and/or doesnt have enough existing connections to grow at the level it would like.

Whats wrong with organic growth anyway. Its just theirs too many greedy people out there, wanting to take more than their fair share.

Boatman,

As per usual, your total ignorance of a subject does not prevent you from forcefully expressing your opinion.

I have an investor almost from the start. My net return has been 9.48% and that takes into account the capital written off. That amounts to 1.50% of my total investment. I only lend to A and B grade borrowers,the ratio being 80/20. I am gradually withdrawing my capital, but only because most of the loans are going to the wholesale investors.

More widely,I find your sneering contempt for all the borrowers to be rather unpleasant.

I signed up very early on as a lender and, in the beginning, received amazing returns. I reinvested profits for a few years but a change to Harmoney's fee model (which I think was a result of the comcom case) reduced returns significantly. That, with the increase in institution lending leaving the dregs for the true P2P lenders left me no choice but to withdraw funds as loans were repaid.

I have found my self in exactly the same situation as you. Back when Harmoney was first launched it was fantastic, loans to invest everywhere and good profit to be had. About 12 months ago I noticed a sharp decrease in the quality of loans available and I had to"babysit" their web page just to get a loan to invest in as Autolend wasn't satisfactory. Since then I have been withdrawing all of my funds. Only a few thousand left now.

P2P is a disruptive model taking on perhaps the least friendliest institution in the world aside from the US military....but don't worry, netflix wasn't too crash hot to begin with and had to go through several product evolutions before it became the present day juggernaut that it currently is. If anything is holding Harmoney back its the appalling lack of financial sophistication of most people in this country. Try uttering the term 'mixed asset classes' during the next conversation you have with someone who is mouthing off about flipping houses and you'll see what I mean by the open mouthed vacant response you get in return.

You can’t blame the customers, or lack of them, for a company’s lack of success, it doesn’t work like that.

Netflix is indeed a juganaut, but those who have bought in at recent stock price levels are going to get burnt when the next market correction comes. It’s not good at any price.

At least Roberts is being honest about it now, perhaps safe in the knowledge that he's made his stack. Beware though Neil, investors have long memories, they aren't like voters. Businesses evolve to most clearly reflect the true values of their owners, a business staffed with ex gfc finance company dudes was only ever going one way. The RIP P2P was issued within 12 mths of them being given a P2P license.

Yeah the P2P model is problematic in a small county, especially when recession comes along, maybe even in a big one. I’ve been looking at Qudian (QD:NYSE) in China lately. Their model seems a good one, different from P2P and very financially sound, with fairly low risk it seems. Their value is in the abundance of data and data analysis they collect via their digital platform, which the banks don’t have and don’t want to do themselves. They are turning into an intermediary between funding institutions and young, small borrowers, with less and less of their own money, and a HUGE pool of potential borrowers. Small loans, big pool of borrowers, good data, turning away from P2P but still matching borrower to lender money.

I think the main issue with NZ peer to peer lending is the size of the loans. Peer to peer lenders I have seen elsewhere in the world tend to offer lots of smaller loans (<$1k), rather than large $5-20k plus loans.

Investors only want to put <$100 per loan, otherwise the risk becomes of a default has too large an impact on them. So the loans are Fractionilised. In theory a few investors and loan is made.

This is where NZ P2P falls down. There is enough investor cash overall, but not enough individual fractions to make up the large loans on offer. So they all offer to banks/institutions, and now itself. Which completely defeats the point of P2P Lending.

Wut? Not sure where you got that idea.

Its rare to see a loan of any size that makes it to the retail side of harmoney not get filled in less than 24hours, usually less than 4hrs. Largest loans are $70k, and they soon get snapped up (because they are only offered to "A" grade borrowers, the worse the borrower the lower the limit on loan size )

How do we turn this around? How do we get the bureaucracy that runs this wonderful, but under performing land, to craft better regulations? How do we stop fighting amongst ourselves and sort out the issues that confront us in a timely manner? Our problems seem so very solvable, almost trivial compared to other places.

Get Unaha-Closp to run the show?

Politicians seem to have the same issue as managers chasing a share price: short-termism.

I do not hold that there are not enough investors , we hardly get enough loans to invest in , I like many are removing funds because the good stuff is going to the big boys .

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.