A Financial Markets Authority (FMA) survey suggests investors are relatively optimistic despite COVID-19 sending the world into a deep recession.

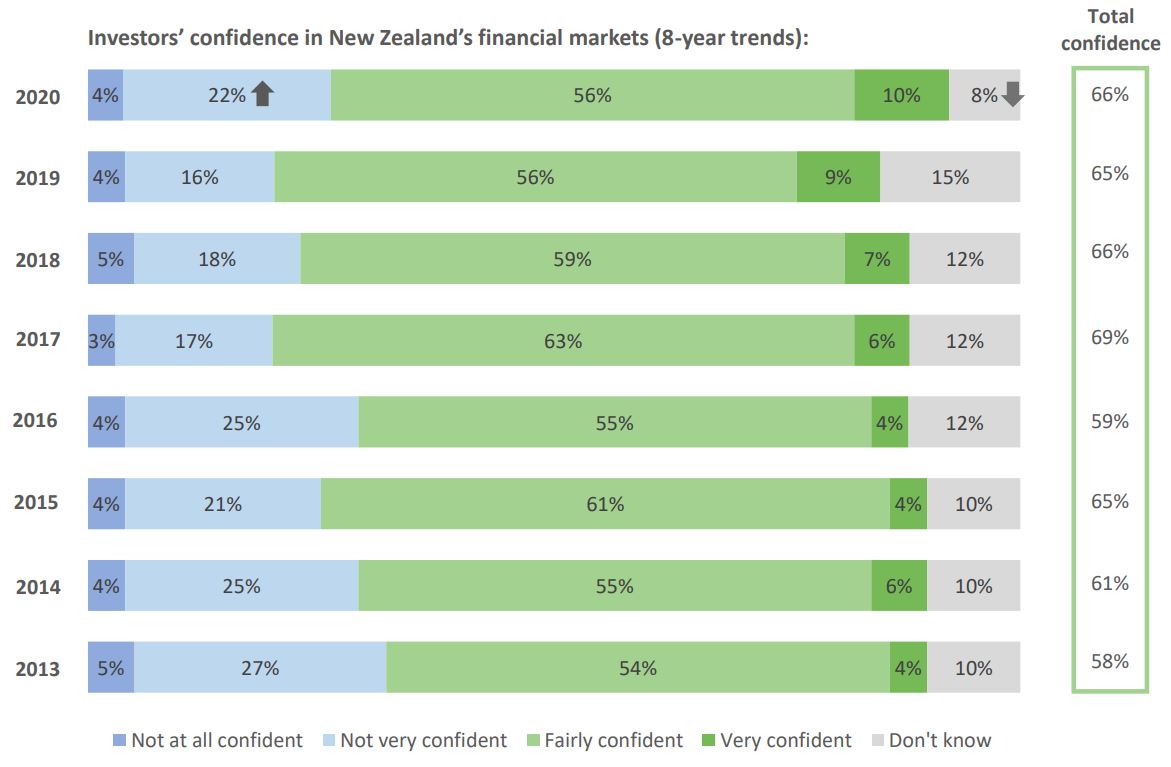

Of the 1003 New Zealanders surveyed during Level 3 lockdown, between May 5 and 14, 10% said they were “very confident” - a slight increase from the previous year and an eight-year high.

The portion who said they were “fairly confident” remained at 56%, meanwhile the portion who said they were “not very confident” rose from 16% to 22%.

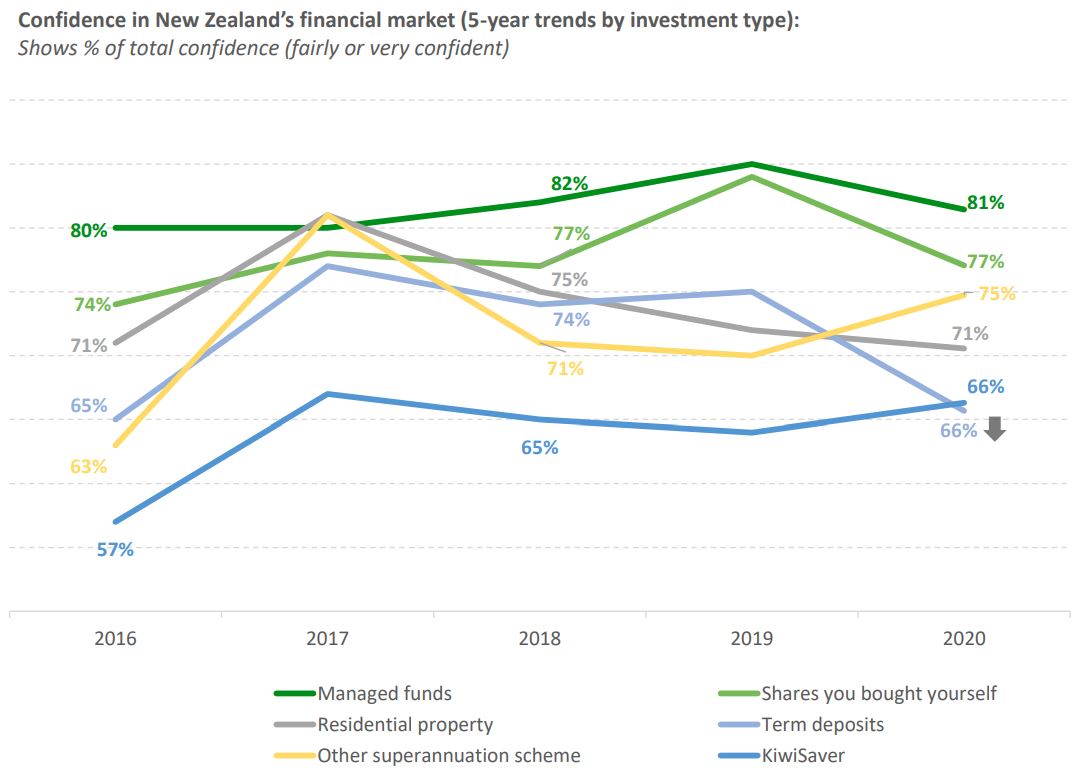

Confidence was higher among higher income earners. 73% of those with incomes above $100,000 a year were "fairly" or "very confident", while only 61% of those with incomes between $20,000 and $49,999 were this upbeat.

Comparing types of investments, investors were most confident in managed funds and shares bought themselves. Confidence in term deposits saw the greatest drop, most likely as interest rate cuts have lowered yields.

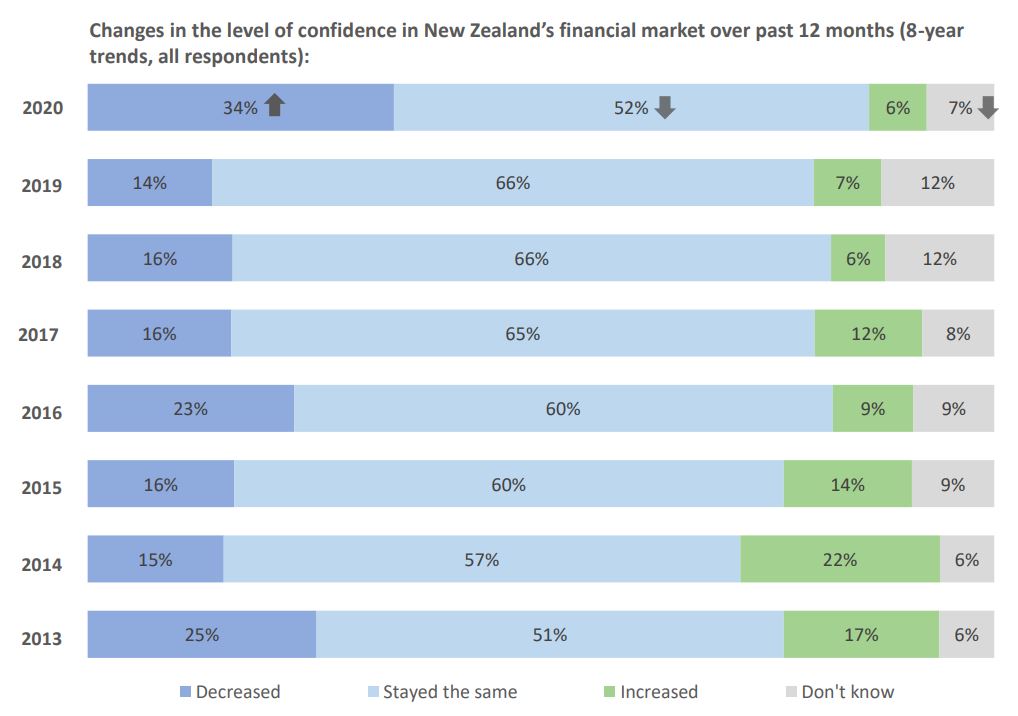

Despite current confidence being relatively stable, around a third of respondents felt their confidence had decreased over the past year.

The relatively upbeat results are perhaps unsurprising, given how active investors have been...

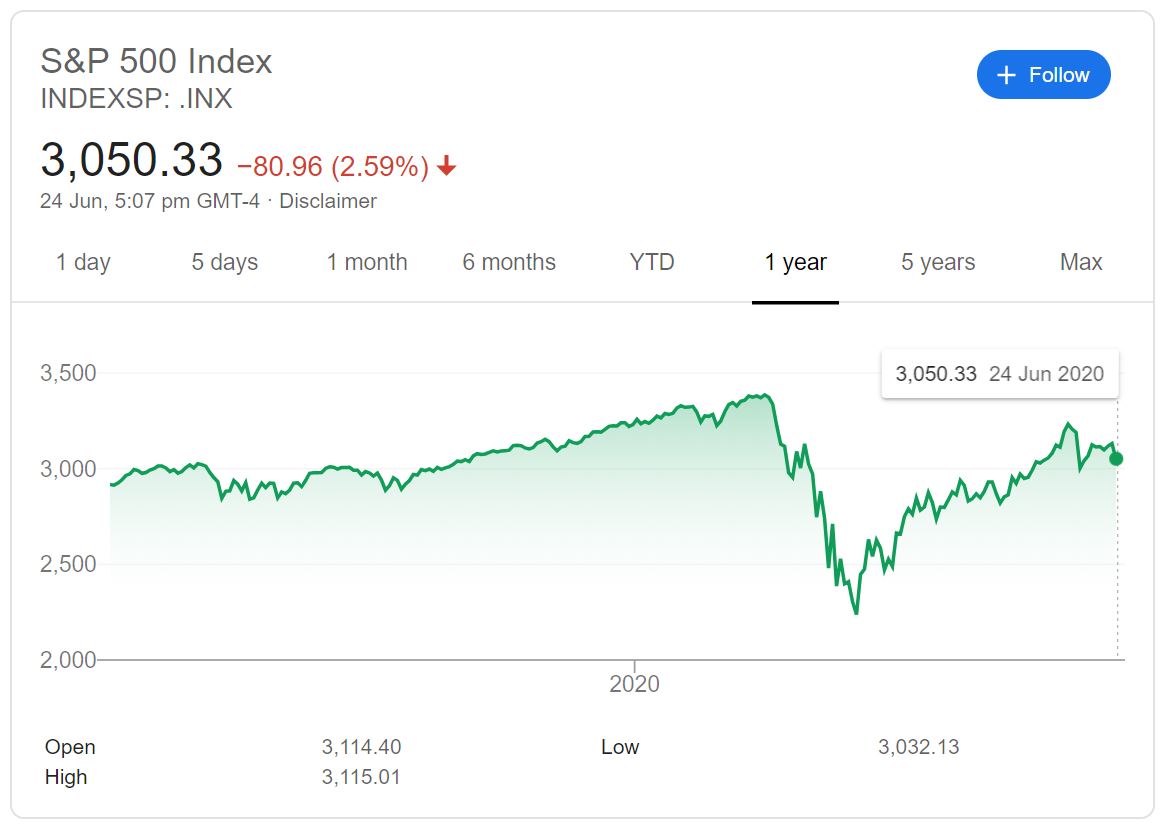

... and how quickly markets have rebounded. The S&P 500, for example, is above where it was at a year ago, all the while the number of COVID-19 cases around the world grows, government support like wage subsidies are due to run dry, unemployment is set to rise, and there's no vacine on the horizon.

Authorised Financial Adviser and Summer KiwiSaver Investment Committee chair, Martin Hawes, put the disconnect between the “real world” and equity markets down to a few factors:

- Investors diving in to the market due to fear of missing out on bargains;

- The low interest rate environment prompting them to invest in riskier assets in search of yield;

- Quantitative easing seeing a lot more cash looking for a home as it filters through the banking system;

- KiwiSaver and pension funds in other parts of the world providing a floor for markets;

- The rise of the retail investor at the margins, with new online platforms making this more accessible, and possibly betters looking for something else to do as sports betting is restricted.

While these factors are propping up equity markets, Hawes believed there would be another wave of selling. He maintained it might not re-test the March/April dive, but said a lot has to go right for the bulls in the market.

He said there would need to be a catalyst for another sell-off, like climbing reinfection rates, so remained cautious.

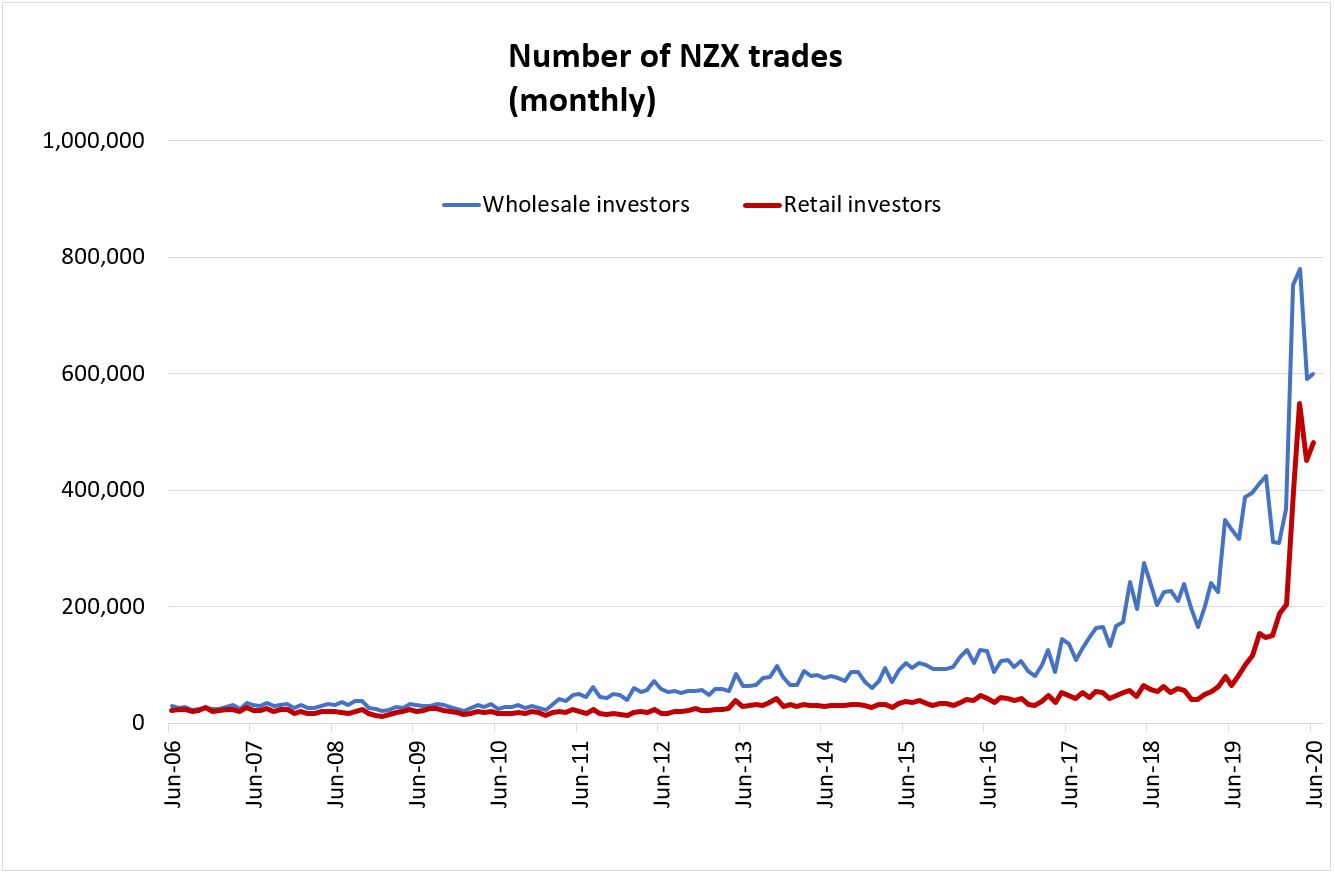

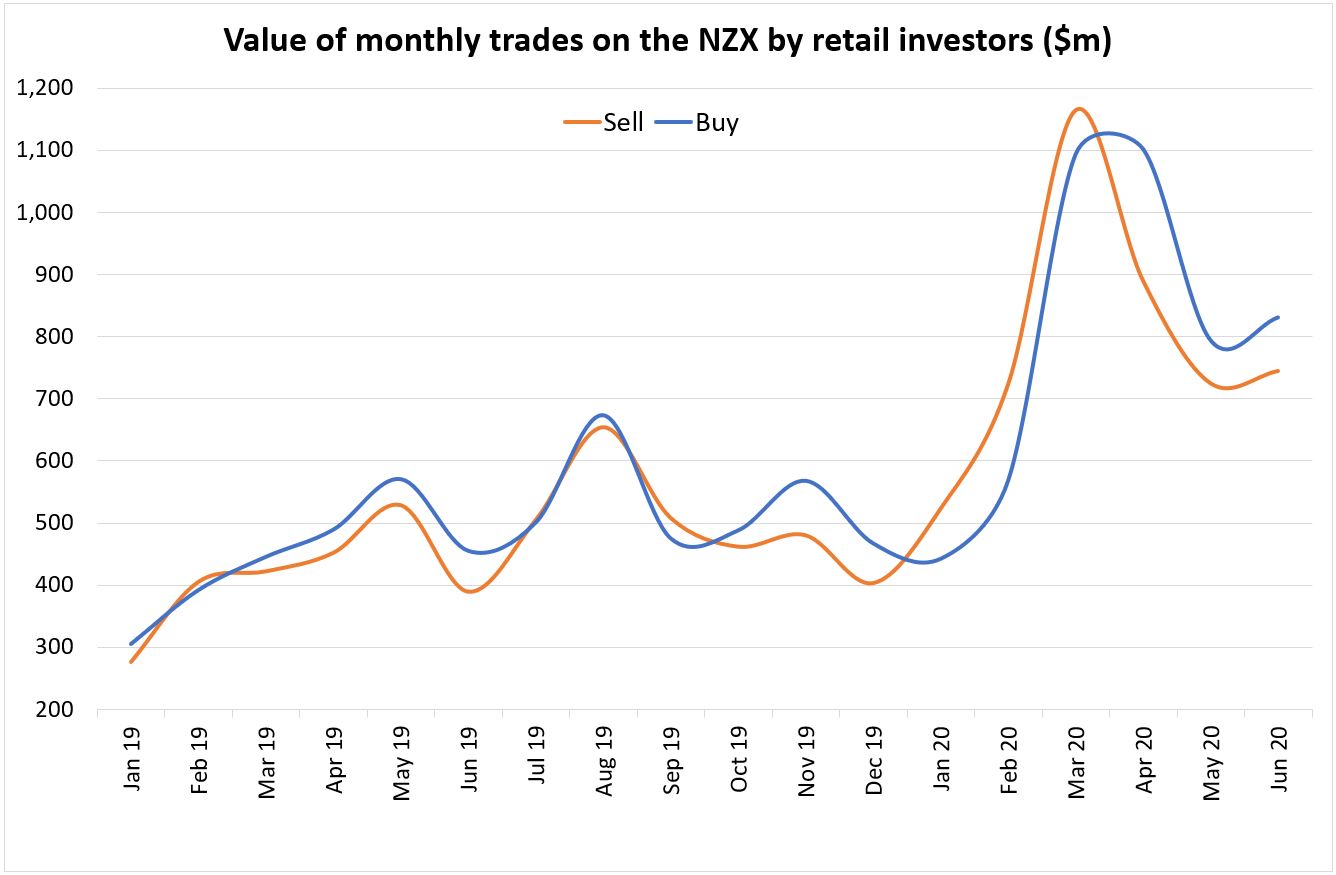

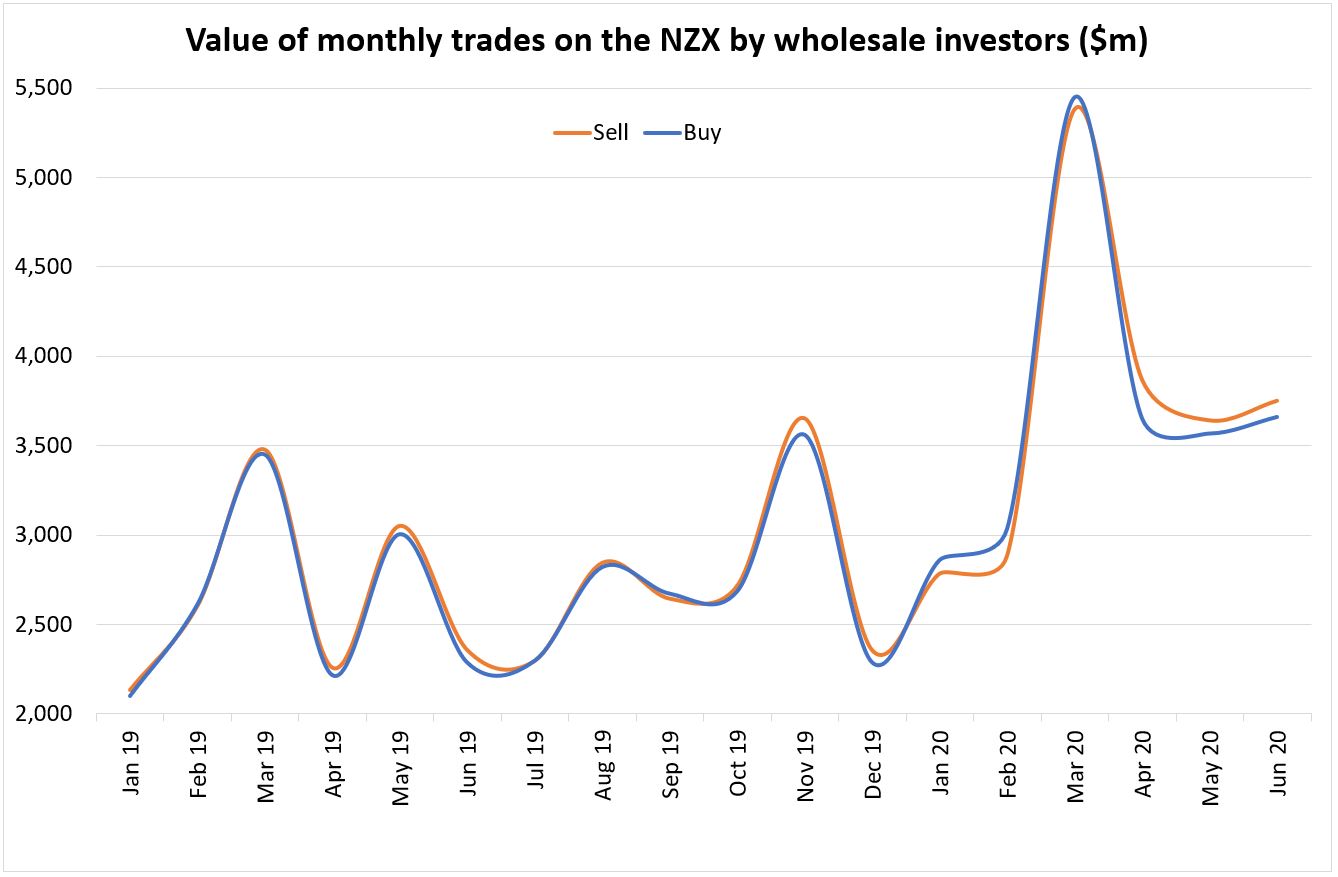

NZX data provided to interest.co.nz shows that in the past three months, wholesale investors sold more than they bought, while retail investors bought more than they sold.

The difference between what NZX investors bought and sold was very large in April, shrunk in May and picked up a little in June.

The FMA in May suggested do-it-yourself investors don't dive head-first into the share market now, if they haven’t done their homework.

“We would caution against developing a new, untrained, appetite for trading on the NZX during this period of volatility and uncertainty without doing sufficient research,” it said.

The regulator’s warning came as its Australian counterpart, the Australian Securities and Investments Commission (ASIC), released a paper ringing the alarm bells over the spike in retail investors chasing quick money.

"Retail investors chasing quick profits by playing the market over the short term have traditionally performed poorly – in good times and bad - even in relatively stable, less volatile market conditions," it said.

39 Comments

A sign of stagflation.

The ‘Pe’ on a 1.5% term deposit is around 66. Makes a Pe of 20 on a utility such as Mercury seem very attractive.

What you are saying is correct. However there is also the volatility of the share investment versus a term deposit. Individuals who can't afford a sudden decrease in the value of their investment (for example, if you need this money in less than, say, 5 years) may still prefer the term deposit option. There is still the possibility of a OBR event, though, and also the risk of inflation kicking in.

All share markets right now are a stimulunatic Frankenstein created by the most reckless bureaucrats I've ever seen operating what is now a global command economy controlled by central banks. We have a global Gosbank, effectively, and the West (which means nothing philosophically anymore) will go the same way as the Gosbank took the USSR; we already have largely zombified economies under debt and regulation over-kill and over-reach.

But what I really object to is price discovery (free markets) has been deliberately destroyed by these same bureaucrats so they could destroy the prudent saver, and savings themselves as the foundation stone of prosperous (small state) free markets; they sacrificed their returns to the credit freaks sitting on their growing unrepayable Everest of debt.

Just an opinion of course. But bring on the Great Reset. If you're in these share markets you're in the biggest ponzi ever created: you don't want to be in them when reality finally overthrows big brother state hubris: and it will. And even the IMF can see reality this morning. Although of course there's the kicker: you leave shares where do you go? It's a world of toxic risk for no reward (probably bonds by this stage are a bigger risk than even shares).

'Stimulunatic'. Outstanding !

Shout out for omishambles

Great summation. Just don't say boo to loudly, or the chickens will scatter.

If you are holding dollars you are part of an even bigger ponzi scheme.

All this confidence is consequence of cheap and easy money floating in the market promoted by more and more printing by government. More worrying as is not based on economic fundamental (Except few techonology and health companies) but QE.

Understand many first time investors have entered as were sitting at home and with cheap money tried their luck and almost all have made decent profit who entered in April and have never witnnesed a lose so are getting more confident and bold to put more and more for easy money without understanding the risk involved at this stage.

If stock market falls many will bleed as thus time is also supported by retail investor in a big way. As many first time investors are aware of the risk but as have not witnessed a fall realization will only come when it happens.

Central bank and government policies are puttting safe investors at risk as are now forced to come out and invest in high risk assets.

"In the past 3 months, wholesale investors sold more than they bought, while retail investors bought more than they sold".

There will be a lot of burnt fingers when the markets finally acknowledge economic realities and fall-heavily. Sure, ever lower interest rates help prop up overpriced assets, but not forever. At some point, wholesale investors will be net buyers and the new retail investors will be net sellers.

RBNZ should be very happy, they wanted savers to look at alternatives for their money. And here they are doing exactly that.

The platforms enabling people to buy franctional shares here and overseas have been a great help in investing small amounts, which from hundreds of thousands of investors add up to a sizeable amount.

The brokers are making merry and some intrepid investors too, short term. Seems to be addictive.

Is New Zealand benefiting by this ? Some New Zealanders certainly are.

Point #5 above: "The rise of the retail investor at the margins, with new online platforms making this more accessible, and possibly betters looking for something else to do as sports betting is restricted."

Let's translate this into Interest-speak:

"The rise of clueless amateur investors with time and money on their hands, denied other outlets, seduced by new platforms and slick advertising."

As a long term equities investor I've bet against the int.co doomsters club house for over a decade, with very positive outcomes. I confess to a secret perverse enjoyment in reading the numerous catastrophic predictions made by commentators and doing the opposite. But this time it really is different, with depression bearing down on us accompanied by astonishing levels of stimulunacy. Japans experience is only partly applicable, lessons from 1930 not especially instructive. Fundamentalists cling to their anachronistic PE bibles refusing to accept that a malignant new heresy of low interest rates has redefined the investment returns landscape for an extended period. Mark Hubbards anguished wail concludes with a pertinent question - where do you go in a world of toxic risk where Weimar Republic wheel barrow cash devaluation viably competes with Wall Street wolf Jordan Belfort in potential outcomes. In the end elevated risk has to be accepted if tea and milk arrowroot biscuits in retirement don't appeal. Hedge to keep the demons of fear quiet at night but ride the tiger to some extent you must.

The uptick from retail investors certainly is interesting, but I wonder if it overstates the phenomenon. With wholesale trades still something like 5x the value of retail trades I'm not sure they can be considered the dominant force.

Agree. Short term they are price setters but as you say their comparatively low volumes mean their impact on pricing will diminish over the longer term. The sharsies crowd will wither under the blistering sun of a major correction but meantime they present a milking opportunity.

Others will know better than me in practice but I read that the Robinhood/Sharesies investors have a disproportionate pricing impact not by total volume in the market but by volume traded daily. Although the overall volume of wholesale is much higher, wholesale traders don't trade often, so lots of retail trades can drive price, especially when a lot of retail investors (NYC lockdown millennials, Portnoy fans, etc) are trading hundreds of times a day. If so, some share prices might be much more heavily influenced than (what until recently was) 'normal' by the (re)tail wagging the wholesale investor dog. Hertz may be an extreme example?

The Sharesies herd.

Money printer. Brrrr. Take away Fed / central bank support and watch the markets crash!

Latest weekly release (US Thursdays post-close, this morning NZ time) shows Fed total assets - the $3T brrrrr that started when markets fell in Feb -stopped end May and is quietly easing down slightly: https://fred.stlouisfed.org/series/WALCL (Click on 1YR tab for closer look).

Never tell the lemmings what and how and why

The volume of opinion that finds its way into print by those who should know better is troubling

Eighty percent (80%) of all superannuation and managed funds are index funds that follow an index. Often those indexes are synthetic and compiled by the fund manager. Many managed funds select a fund manager based on the composition of a particular index. All managed index funds have a "title" or "articles of association" which are published for the investor to evaluate what type of fund they wish to invest in ie "Growth, Diversified, Conservative, Balanced, Agressive". Cash flows into the hands of the Fund Managers on a continuous basis. The fund manager does not hold cash unless cash is within the ambit of the fund to hold cash.The Fund Manager is obliged to invest according to "Title". This is based on successful cases of litigation by members against fund managers and fund trustees who have sat on cash while the underlying "titled" investments have risen.

Thats why the markets have continued and will continue to rise, unless members decide en-masse to shift funds

Have known for 25 years waiting for someone in the business to publish

'Cash flows into the hands of the Fund Managers on a continuous basis' - early signs cash is being hoarded in banks. Fund contribution holidays will increase. We could see inflows reduce.

Un-employment will do that for kiwi-saver automatically

The question is what might cause members to shift funds? The need to spend capital as they are already in retirement? Lack of yield in the fund? Seeking to lock in gains? Fear of losses once it does turn?

Then is there a lack of new members coming in to sell to due to demographics?

I think Ray Dalio has the answer in that the yield won't keep up with the rate of inflation.

“new online platforms making this more accessible“. Some US platforms, such as Robinhood, as of a few months ago have zero trading fees. Young novices are pouring into the market. As probabilities go, this is very likely to end badly.

Those closest to the Central Banks money spigot are the real winners.

Two points of interest.

A recent Bloomberg article described central bank easing with the phrase “pumping money into the economy.” That’s a misconception. Monetary easing is actually an asset swap. The public was holding savings in one form, and now it holds it in another. The Fed buys Treasury securities from the public, and replaces them with currency and bank reserves (base money) that someone has to hold, at every point in time, until the Fed sells its bonds and retires the cash. All monetary policy does is to change the mix of government obligations held by the public. Only fiscal policy – specifically deficit spending – changes the total amount of those obligations.

Historically, base money has earned zero interest. Forcing people to hold more zero-interest money makes them more eager to chase interest-bearing alternatives. That response made for a very pretty relationship between the ratio of base money / nominal GDP and the level of Treasury bill rates at any point in time. In recent years, the Fed created such a huge pile of zero-interest money that the only way it could raise interest rates, without slashing the size of that pile, was to explicitly pay interest on excess reserves (IOER).

Without IOER, short-term interest rates would only be about 12 basis points here because the Fed’s balance sheet (of Treasury bonds purchased from the public), and the corresponding pile of base money (held by the public instead) is still ridiculously large. If the Fed lowers interest rates today, it won’t be by “pumping money into the economy.” It will simply be by lowering the interest rate it pays on excess reserves. It may even create more reserves by buying more Treasury securities (QE), but again, even that is an asset swap. Link

The idea that “low interest rates justify high stock valuations” is really a statement that “low interest rates justify low expected stock returns as well.” Those high stock valuations are still associated with low prospective future stock market returns.

Worse, the notion that “low interest rates justify high stock valuations” assumes that the growth rate of future cash flows is held constant, at historically normal levels. If, as we presently observe, interest rates are low because growth rates are low, no valuation premium is “justified” by low interest rates at all.

Presently, the combination of record low interest rates and record high stock market valuations does nothing but add insult to injury.

...the iron law of investing is that a security is nothing but a claim on a future stream of cash flows. Valuation is a crucial determinant of long-term returns. The higher the price an investor pays for those cash flows today, the lower the long-term rate of return earned on the investment..

The corollary is also true. The lower the long-term rate of return demanded by investors, the higher the price moves today. So clearly, changes in investors' attitudes toward risk will strongly affect short-term returns. If investors become more willing to take market risk, it is equivalent to saying that they are demanding a smaller risk premium on stocks (that is, a lower long-term rate of return). Prices rise as a result. Now, the fact that current stock prices are higher also implies that future long-term returns will be lower, but that's part of the deal. Link

{kind=link}

Well Audaxes, the points raised by Mr Huxmann might have been relevant if they weren't nearly 20 yrs out of date. Also Mr Huxmann has made some rather sweeping assumptions regarding the drivers behind stock prices. His statement that "low interest rates justify high stock valuations" is fundamentally incorrect. DEMAND drives higher stock prices. Low interest rates don't justify high prices at all, what low interest rates do is increase demand for higher "potential" returns in the form of capital gain - hence the corresponding increase in real estate prices. It's just a hunt for higher yield.

It's a century plus formula and still applies today - which investment bank do you work for? Familiar with VaR?

Yes Audaxes, I'm familiar with VaR and no I don't work for an investment bank so I don't use the myriad of strategies and calculations available to them to purchase equities. What I would say though is using your "century old, still relevant formulae" didn't prevent most, if not all, fund managers taking a bath in '08/'09 nor has it prevented the same wetting this time around. My perhaps uneducated strategy of research, ROE, DCF, market position and simple CE holdings vs CO of a company when purchasing a stock has still allowed me to roughly (+/- 5%) match the returns of many funds and in fact exceed many of them. I'm also well ahead of the NZX and ASX index returns. I'm quite happy being a retail investor and data to date actually shows Investment fund managers rarely add further value than a passive Index fund. Just saying

It's utterly amazing reading all the "keyboard warrior" experts opinions. How many of you actually have "skin in the game" re: equities?? Here's the deal - if new retail investors want to spend money on daytrading it's totally up to them. The so called margin trades are of such a low effective volume/value rate that they have very little effect on all but the daytraders themselves. If the newbies lose their shirts then sobeit. Might teach them a thing or two about the market. Best lessons learn't are the hard ones. Rule #1 in the market - it's a "willing buyer/willing seller" game and someone has to lose so someone else can gain.

Newbies, please be aware of day trading ..

https://www.google.co.nz/amp/s/www.cnbc.com/amp/2020/06/18/young-trader…

Too true Ben, they do it at their peril. Only one other cardinal sin - "trend buying" Both will inevitably end in tears and a significantly reduced bank balance. As the old maps used to say - " here there be monsters" lol

I wonder what the NZX index would be on right now if bank deposit rates were the historical average of say 4.5 % ?

My guess is about 7000. Power companies might be closer to their appropriate PEs of around 5, not 35!!

So share prices right now are what they are not because they are 'worth' it, but what is being paid for them.

New investors should look at a 10 year chart of the NZX or S&P 500 and realise where on the curve they are buying at.

milking the bigger mugs

If enough mum and dad investors buy large amount of stocks, RBNZ will soon have a new mandate to save the NZX in addition to savings the housing market.

Sadly your exactly right. RBNZ sent them off to overpriced share and housing markets.

The point is that low interest rates, and growth in equites drive employment. The worse employment gets, the lower interest will be, and the more QE will be needed, and moaning here that that’s not the the way you would prefer things to work doesn’t change it.

growth in equities drive employment????...care to outline how exactly you think that occurs?

The challenge does not just stop there. Economy will not return immediately like it has been before this ruckus. But every challenge comes reward when done successfully. Stay safe everybody.

jack, @roofing companies tauranga

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.