Content sourced from the World Gold Council

The rapid ascent of cryptocurrencies over the past year has drawn the attention of investors. Often, investments in cryptos are equated to investments in gold. Despite some apparent similarities, we believe that gold stands apart from cryptocurrencies, both fundamentally and practically.

Our analysis demonstrates that:

• sources of gold demand are more diverse.

• supply and ownership of cryptocurrencies are more concentrated.

• cryptos have mostly contributed to portfolio performance through returns but have added significant risk.

• gold is a high-quality liquid asset and portfolios with cryptos may benefit from higher allocations to gold.

• evolving regulatory frameworks may change the value proposition of cryptocurrencies.

Gold and cryptos are fundamentally different

The advent of blockchain and cryptocurrencies has catalysed innovation in the financial industry. Their proliferation and recent exponential price increase have captured investors’ imaginations. However, the recent developments in blockchain and cryptocurrencies do not imply that cryptocurrencies are a substitute for gold. The argument that gold and cryptocurrencies such as Bitcoin are similar appears to stem from perceptions of:

• their limited supply

• their role as alternatives to fiat currencies.

However, this comparison is simplistic and overlooks fundamental differences between gold and cryptocurrencies – not only in terms of their market dynamics but also in terms of their performance and the role they play in portfolios.

Gold has a dual nature

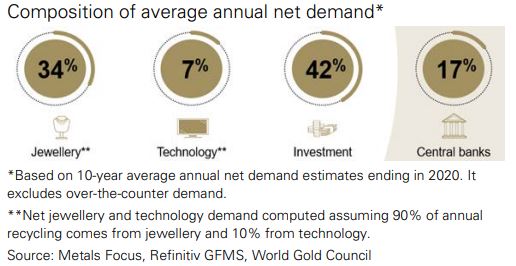

The sources of demand for gold are very different from those for cryptocurrencies. For more than 2,000 years, gold has served as means of exchange and been used as a store of value. Gold is owned by institutional and individual investors, as well as by central banks (Figure 1).

Figure 1: Gold’s demand is linked to investment and consumption

Jewellery is an integral part of the gold market. A large portion of gold demand is deeply connected to cultural and religious beliefs, especially in India and China. Gold is also widely used in high-end electronics – including for components in computers, mobile phones and other technology (which, interestingly, are needed to ‘mine’ cryptocurrencies).

This sets gold apart from many assets, giving it a unique dual nature that historically has allowed it to perform well in times of economic stress as well as benefiting from longterm economic expansion. This underpins gold’s strategic role in portfolios as a source of returns as well as an effective diversifier.

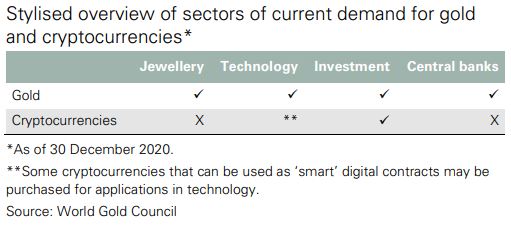

In contrast, cryptocurrencies are digital (non-tangible) assets and, in our view, their current primary – if not only – source of demand is for investment (Table 1). For example, Bitcoin’s recent performance and volatile behaviour may suggest that it primarily responds to price momentum, which is usually linked to more speculative than strategic positioning.

Table 1: Gold has more diverse sources of demand than cryptocurrencies

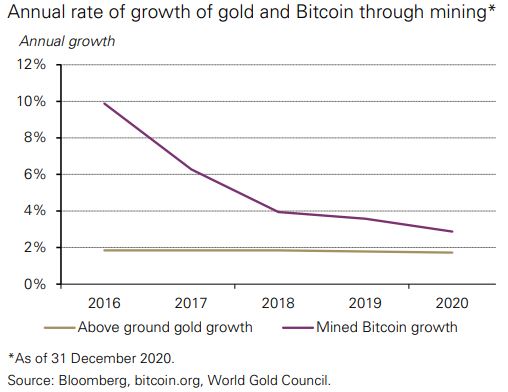

Chart 1: Growth in above-ground stocks of gold remains below the equivalent growth in Bitcoin

Gold is a unique and scarce natural element

One of the most referenced similarities between gold and cryptocurrencies is scarcity. Gold’s above-ground stocks grew at a rate of 1.7% through mine production in 2020 (Chart 1) – and that rate has not changed much over the past 20 years. The stock of Bitcoin is currently increasing at an annual rate close to 3% and is engineered to slowly decline to zero growth around the year 2140.

While both gold and Bitcoin are finite, Bitcoin’s predetermined number of units in existence may seemingly create an advantage. However, gold’s relevance has been cemented by a combination of elemental physical and chemical properties, as well as a good balance between availability and scarcity. Thus, while there exist other metals and precious metals, such as silver, palladium or platinum, gold was by far the preferred asset used in currency standards and has remained a key component in foreign reserves even after the end of the Bretton-Woods system.

In contrast, nothing prevents additional – and possibly more efficient – cryptocurrencies from replacing existing ones or potentially adding to the overall total supply. The crypto space has exploded in recent years, and it is estimated that there are more than 10,000 cryptocurrencies available through various online platforms.

At present, Bitcoin has benefited from its name recognition and large network effect, but the space is highly competitive, and it is still too early to know how this issue may play out. For example, Bitcoin Cash, which follows the same structure but allows an increased block size to reduce costs and increase speed, was launched a few years ago. Various other Bitcoin spinoffs (or ‘forks’) followed. And while they are not always prevalent, they are more than just a proof of concept that could result in unforeseen expansions to supply.

Gold production and ownership is diverse

Gold mining is well distributed around the globe. The top five gold producing countries are China, Russia, Australia, the US, and Canada, with various Latin American and African countries not far behind. Average annual production is evenly distributed across regions, with Europe the only continent accounting for less than 10% and no continent capturing more than 25%.

Equally, ownership of above-ground stocks is widely distributed. The US Treasury is the largest known single holder of gold but only owns 4% of all above-ground stocks. Almost 50% exists in the form of jewellery (distributed globally), while 21% is owned by a large number of investors – individual and institutional – in the form of bars, coins and gold ETFs.

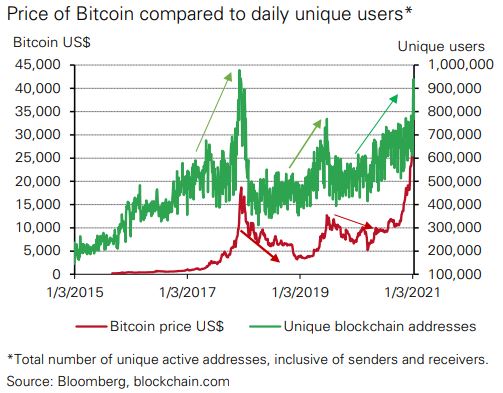

Concentration risk has been flagged as a key issue for cryptocurrencies. The number of Bitcoin ‘miners’ has been whittled down from thousands to just a handful of key participants. As reported by Bloomberg, “five mining entities – all of them based in China – control 49.9% of all computing power on the network, the highest concentration of mining power ever, a new analysis from TokenAnalyst found”, which, if increased, could pose severe risks to the network.

Furthermore, while the number of Bitcoin holders has risen over the past year (Chart 2), ownership is very concentrated – just 2% of Bitcoin holders own 95% of all available Bitcoins. As a counter-indicator of performance, perhaps as a by-product of the aforementioned concentration, large spikes in the number of unique addresses have historically coincided with significant pullbacks in price.

Chart 2: Sharp increases in Bitcoin ownership have coincided with significant selloffs in recent years

Gold and crypto prices behave differently

High potential reward brings added risk

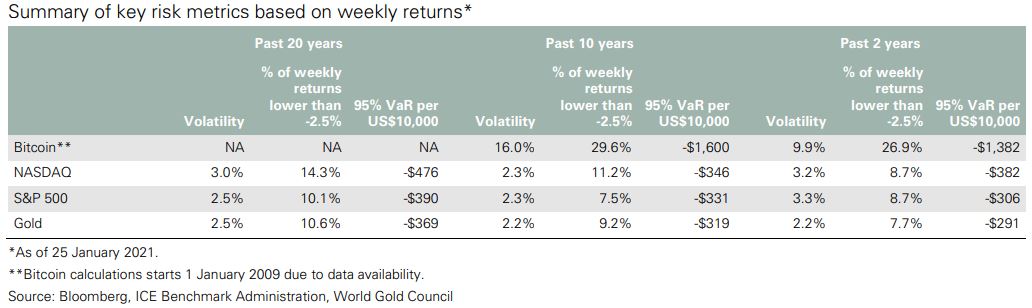

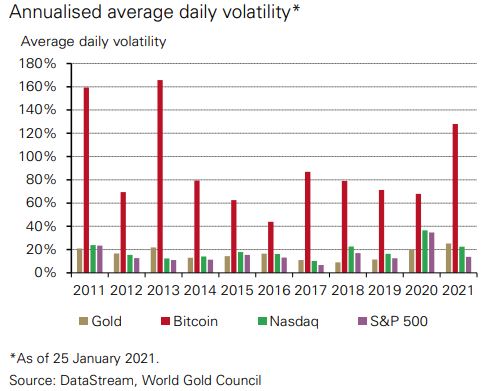

Cryptocurrencies have captured the imagination of investors with their exponential growth over the past few years, likely in part due to widespread asset price inflation on the back of ultra-low interest rates. Bitcoin quadrupled in price in 2020 alone and has increased ninefold over the past two years. 16 These gains have led some institutional investors to consider, or make some incremental level of investment in, Bitcoin over the past year. However, as with any other financial asset, reward does not come without risk. Not surprisingly, Bitcoin’s ascent has been accompanied by substantial volatility and drawdown risk (Table 2 and Chart 3).

Bitcoin has been three times more volatile than the S&P 500 or the NASDAQ composite over the past two years, and more than four and a half times more volatile than gold.

Bitcoin has lost 2.5% or more once in four weeks on average compared to once in 12 weeks on average for the S&P 500 or NASDAQ, or once in 13 weeks on average for gold. Finally, Bitcoin’s Value-at-Risk (VaR) has also been considerably higher. On any given week over the past two years, investors had a 5% chance (95% VaR) of losing at least US$1,382 for every US$10,000 invested in Bitcoin – almost five times more than the VaR for an equivalent investment in gold. And while investors may choose to embrace high-reward tactical assets such as Bitcoin, they still need the appropriate tools to manage the additional risk. In our view, a higher exposure to cryptocurrencies warrants a higher allocation to gold.

Chart 3: Bitcoin’s annual volatility is still multiple times higher than equities and bonds

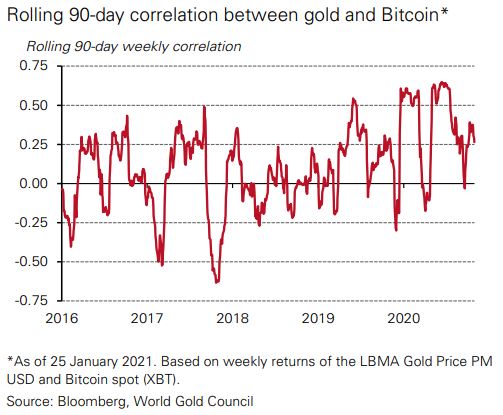

Diversification is not just about low correlation

The correlation between gold and Bitcoin is low, ranging from -0.5 to 0.5 most of the time. And while it was positive on average during 2020, it is still by no means consistent in one direction (Chart 4). This indicates that gold and Bitcoin are not behaving as substitutes.

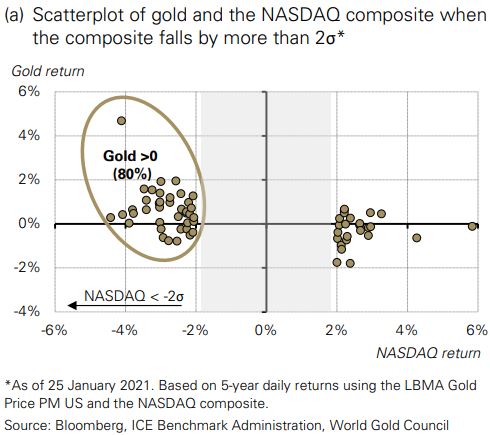

Furthermore, if Bitcoin were a replacement for gold, it would behave similarly to gold in terms of its reaction to the performance of other assets – in particular, equities. And while both gold and cryptos have generally had relatively low correlation to the equity indices such as the S&P 500 or the NASDAQ composite, it is the correlation when equities fall that matters most to investors as this is usually when diversifiers are most useful.

Chart 4: The correlation between gold and Bitcoin remains low despite an increase seen in 2020

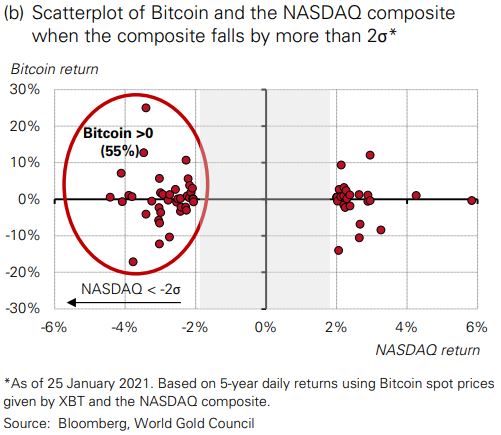

Chart 5: Gold prices tend to increase when tech stocks fall but the same has not been true so far for Bitcoin

Here, gold and Bitcoin stand apart. Gold tends to show a negative correlation to equities during significant stock market falls – as seen by the behaviour between gold and NASDAQ (Chart 5a). In contrast, Bitcoin has been equally likely to rally or fall in periods when the NASDAQ tumbled (Chart 5b).

Bitcoin has yet to prove itself as a safe haven

Bitcoin trades like a ‘high-octane’ tactical asset. At times, market participants have noticed ‘safe haven-like’ behaviour in Bitcoin, as it has appeared to directionally move in a similar way to some traditional hedges, such as gold. However, there is no consistent trend.

For example, in March 2020, Bitcoin fell by more than 40% from peak to trough, ending the month down 25% and behaving more similarly to US technology stocks than gold. In contrast, while gold initially fell in March – by 8% from peak to trough – it quickly rebounded to end the month back to the level where it started, and then continued the upward trend as investors added hedges.

Improving risk-adjusted returns

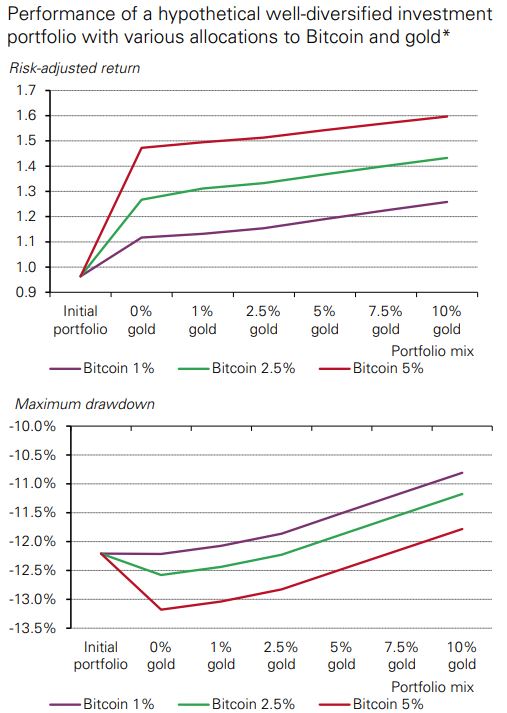

Some studies have suggested that adding Bitcoin to a hypothetical portfolio would have increased risk-adjusted returns. Our own equivalent analysis shows that over the past five years, a 1% to 5% allocation to Bitcoin would have increased the risk-adjusted return of a well-diversified hypothetical portfolio (Chart 6). However, the improvement would have come from Bitcoin’s rapid price appreciation and not from a reduction of portfolio volatility, as one would expect from a diversifier or safe-haven asset. In contrast, gold’s portfolio impact over the same period would have come from both a contribution to portfolio returns as well as a reduction in volatility. This highlights gold’s relevance as a strategic risk-management tool in asset allocation.

Our analysis also shows that the same hypothetical portfolio with a 2.5% allocation20 to Bitcoin and a 1% to 10% allocation21 to gold would have improved risk-adjusted returns even further over the same period.

Chart 6: Gold improved risk-adjusted returns and reduced drawdown risk on a well-diversified portfolio containing Bitcoin

Furthermore, a 1% allocation to Bitcoin alongside a 10% allocation to gold resulted in risk-adjusted return equivalent to a 2.5% allocation to Bitcoin without gold, but the portfolio with gold would have had a significantly lower maximum drawdown. Overall, this not only suggests that Bitcoin fails to replace gold’s role in a portfolio, but also that adding Bitcoin to a portfolio may warrant a higher allocation to gold, likely as a way of managing the additional volatility.

Interestingly, we also found that a 1% allocation to Bitcoin – often viewed as a tech investment – would have given the same risk-adjusted return as a 7.5% allocation to major US tech companies – in particular, the so-called FAANGs. Yet, the allocation to FAANGs would have also resulted in a lower maximum drawdown.

Bitcoin has so far improved the efficiency of portfolios through extremely high returns, which are by no means guaranteed to continue at the same rate.

Gold’s liquidity helps investors manage risk

Gold trades in a well-established and liquid market. Collectively, gold trading volumes exceeded US$180bn a day on average in 2020 between over-the-counter transactions (primarily through spot), futures and gold ETFs. This in turn helped keep bid-ask spreads of most gold-traded instruments quite tight – usually less than a couple of basis points – thus giving investors the ability to easily enter or exit their gold positions.

In contrast, Bitcoin spot trading volumes – which can vary widely from source to source and are not always easy to verify – were estimated to be less than US$2bn, on average, in 2020, with a range up to US$4bn. And while volumes seem to have increased substantially so far in 2021 reaching levels close to US$10bn, reporting in online platforms is not regulated and may not be homogeneous.

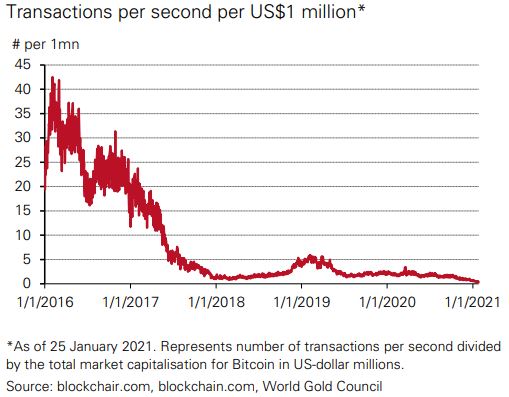

Additionally, the number of Bitcoin transactions as a function of its market cap has decreased to almost zero (Chart 7). We believe that this trend could indicate insufficient liquidity in the market if many investors, or even one large one, were to attempt to exit the market. And anecdotal evidence suggests that bid-ask spreads not only remain wide but vary substantially.

Chart 7: Bitcoin transaction velocity has waned, raising potential liquidity concerns

An evolving regulatory environment

Some crypto enthusiasts have argued that Bitcoin could replace traditional currencies in transactions. While some vendors do accept Bitcoin, on average only about 340,000 Bitcoin out of approximately 18 million in existence are used for daily transactions, which is less than 2%. In comparison, the US dollar transacted nearly US$6trn per day on average in 2019. At the time, this represented 40% of the total M2.

This may also be in part because Bitcoin lacks the regulatory framework to appropriately function as a means of exchange. Furthermore, limitations of the network itself could prevent widespread adoption. Bitcoin’s network capacity is fewer than 10 transactions per second, approximately, compared to VisaNet – Visa’s payment network – which reportedly can handle up to 65,000 transactions per second. This limitation is well known, and many possible solutions have been suggested, but these would either change Bitcoin fundamentally or rely on less secure but higher capacity parallel (‘off chain’) networks such as Lightning.

Perhaps more importantly, widespread adoption of cryptocurrencies would likely result in more extensive government regulation. We believe this may stem from two key considerations: consumer protection and policy efficacy. For example, effective monetary policy requires a central bank to be able to control money supply. At a hypothetical extreme, if individuals do not transact in an official currency but in an independent cryptocurrency, monetary policy becomes moot. Of course, government intervention would occur before that happened. And while regulation may not remove the viability of cryptocurrencies altogether, it may change their investment proposition, objectives and, likely, their performance.

In recent years, partly because of concerns surrounding ‘stablecoins’ such as Diem (formerly known as Libra), governments have looked more closely at digital assets. Specifically, there has been growing interest in the development of digital versions of national currencies, also known as Central Bank Digital Currencies. This may, in turn, catalyse changes to the regulatory environment of cryptocurrencies.

Gold is proven and established

Our analysis suggests that gold stands apart from cryptocurrencies in general and Bitcoin in particular. Gold is an effective, tried and tested investment tool in portfolios. It has been a source of returns rivalling that of the stock market over various time horizons; it has performed well during periods of inflation; it has been a highly liquid, established market; and it has acted as an important portfolio diversifier, exemplifying negative correlation to the market during downturns.

The recent performance of cryptocurrencies has been noteworthy, but their purpose as an investment seems quite different from gold. The crypto market is still in development, and liquidity is scarce. We believe that their price behaviour at this point, while still attractive to many investors, seems to be driven in large part by high return expectations – fuelled by momentum and aided by low interest rates.

Gold, too, is likely to perform well in a low-rate environment, but its behaviour responds to four key drivers that, based on our analysis, underpin the relevance of gold as a strategic asset.

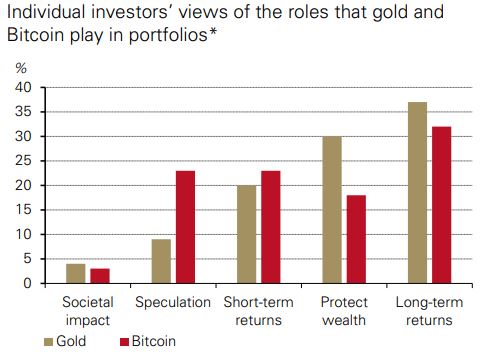

This explains not only why gold is uncorrelated to all major assets held in the typical investor portfolio but also why – fundamentally – cryptocurrencies do not replace gold’s role in a portfolio. Indeed, our 2019 investor survey indicates that gold and Bitcoin can play different roles in portfolios: investors see Bitcoin more often as speculative while they see gold as a means to protect wealth (Chart 8). Similarly, our conversations with institutional investors seem to suggest that gold and Bitcoin are seen as having different value propositions.

As such, as financial markets continue to evolve and new technologies develop, we believe that gold’s unique attributes and its contribution to investment portfolios make it a relevant long-term strategic investment. Chart 8: Individual investors more often view Bitcoin as speculative and gold as a means to protect wealth Individual investors’ views of the roles that gold and Bitcoin play in portfolios.

Chart 8: Individual investors more often view Bitcoin as speculative and gold as a means to protect wealth

This full report is available here. The full report contains extensive notes and references that are not in this version.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis (restarting for 2021 on Monday) here »

Precious metals

Select chart tabs

19 Comments

"effective monetary policy requires a central bank to be able to control money supply."

You can force people to use your money - but you can't force people to value it. That goes for gold too. That the gold council needs to advertise gold in the face of Bitcoin's ascent indicates gold is not behaving as it should as a true store of value outside the fiat system (or you wouldn't have to window dress over the fact gold did not hold value in the face of the most unprecendented money supply expansion in history).

I don't entirely agree with you. It is not that gold has not held its value over the past 18 months, it's price has not increased as much as expected relative to money printing. But you have to remember that the gold price is being heavily manipulated with the support of the ruling elite. JPM is allowed to continue to work its magic. The central bankers don't really care, as long as the price hasn't exploded upwards.

But I was describing price action, and you're explaining the mechanism, what's not to agree with? Gold is a controlled market.

You're arguing that gold has 'not held its value', but it appears you're basing that purely on its price action. Price is not necessarily indicative of value. Comparing the price of BTC with gold is spurious.

So what is the true value of gold beyond its price action?

So what is the true value of gold beyond its price action?

It's a good question. Gold's value is in its properties such as scarcity. Some of those properties are tied to culture. I've seen estimates of 5-6x higher than its current price but I'm unsure of what methodology is used. Price estimates are usually calculated by comparing gold to the money supply.

And how much of BTC price is based on speculation compared to gold? I’d say a hell of a lot.

So really they have zero reasons LMFAO

Gold then white gold etc. are the known wealth protector, it is like the rest (including housing) is subject to market price manipulation - The question usually how big is the country authority on guaranteeing them? in case of NZ, the guarantee already fallen into housing, but hey.. not long ago even Tulips got govt. guarantee.

https://www.stuff.co.nz/business/opinion-analysis/300223000/property-in…

I would have been interested to know who wrote this and their background?

Interesting article; not much I disagree with. Although I’ve said before I own BTC since 26 October just last year (an amount I can afford to lose) which is up 146% this morning (gold down just a tad under 5% for same period) and I hope BTC does become the store of value over gold because it’s so much easier to buy, store securely and cheaply and is portable... on all those counts gold is awful.

There is a good chance I believe that will happen simply because with BTC becoming heavily regulated it is getting substantial institutional buy-in, because of being regulated- to the chagrin of we libertarians - especially out of US, and so a contract of sorts is being worked out. A simple Google will give a list of the funds buying in, plus companies rather bravely investing their treasuries, the most prominent being Michael Saylor’s MicroStrategies which is all in to the tune of US$650 million.

Some observations of my own regarding points in the article:

1. Of course BTC is far more volatile than gold: the first has only 12 years of price discovery, the latter thousands of years, plus for traders that volatility is a feature.

2. One can see re future *uses* Crypto could be far more valuable than the old ‘clumsy’ metals as Crypto will be part of the fabric of our economic lives.

3. Although for now BTC only will work as a store of value, not as currency, or certainly not in US and New Zealand given capital gains tax laws in US and IRD’s published position here making any sale of BTC taxable. That is, the exercise of buying your groceries with BTC is rather ridiculous when to do so you have to first trace the historical cost (FIFO or weighted average) of the BTC used in that transaction - every transaction- work out the profit on the BTC per transaction then incorporate into the purchase the tax cost on that profit .... hopeless. Tax law at this stage has destroyed, sadly, Crypto as currency. But that’s what tax does: destroys. And I suspect the state fiat system is rather pleased about that as BTC’s main value, like gold, perhaps is a hedge against the current race to the bottom reckless destruction of fiat currencies and my savings by central bank monetary stimulunacy.

An addendum for NZ fund managers: I would love to have access to a NZ domiciled fund that gave me exposure just to physical gold and silver because they are such a clumsy asset for individuals to invest in by themselves.

This article is a classic example of the establishment being challenged by a technological upstart, and starting to go through the stages of grief. The first is denial. The next anger (likely to occur when BTC market cap flips gold). Followed by bargaining, depression and finally acceptance.

As an aside many of the propositions that underpin the foundation of the article are false. Here's three of the bigger ones:

Bitcoin supply is actually highly distributed. https://insights.glassnode.com/bitcoin-supply-distribution/

Concentration of miners is a non issue https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3506748

The supply of gold is indeed limited... On earth. You better believe Elon knows this. https://www.mining.com/web/the-golden-asteroid-that-could-make-everyone…

The religiosity of BTC fans does not mean that gold have no value.

Who said gold will have no value? It has practical utility beyond being shiny and attractive to magpies. Don't need religion to understand the laws of supply and demand though.

Who said gold will have no value? It has practical utility beyond being shiny and attractive to magpies. Don't need religion to understand the laws of supply and demand though.

You should understand that the value prescribed it it has to a Westerner sitting at his computer in suburban NZ is different to say an oligarch in Central Asia, a Japanese mafia boss, or even an Indian farmer. What is little more than a trinket to you is kind of irrelevant. It's a big world out there.

You should understand that $700 quintillion in precious heavy metals injected into the gold market would tank the gold market price.

What if the Nations of the World unite in a Bretton Woods type conference and decide to adopt Crypto as a medium of value and exchange for the next couple of Centuries ? That would show which wins, Gold or Crypto.

If they do, they'll join the party last. Governments will adopt BTC only through kicking and screaming as they can't use it to fund their pet projects. It's money out of their hands, and by the time they want it, it will be super expensive to buy. But I look forward to institutional adoption, and governments realising - oh shit - we don't actually create wealth - but the people who do are switching to BTC, so do we keep printing money or what?

Well this piece of propaganda for gold aged like Milk. If you’d read this and thought you should just buy Bitcoin instead, you’d be up 22% just two days later. Will gold be a better store of value than fiat $ over time? Yes no doubt. Will BTC be a better store of value than gold over time. Yes no doubt.

Wow what a joke of an article.

My personal highlights include:

Chart 1: only comparing the last 4 years for the annualised growth rates. And not projecting that forward for Bitcoin, because we know that with a 100% certainty, where as for gold...

How they compare the volatility on a Daily level!! and then on a weekly level for the VaR. Oh man if ever i saw some bias reporting this was it haha.

Whats with them and volatility? that how you make profits, just ask the stock market.....

Appropriate tool to manage risk, HOLD FOR LONGER THAN A @ YEAR PERIOD. pretty simple really.

Anyway, read this knowing I would have a good laugh :D

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.