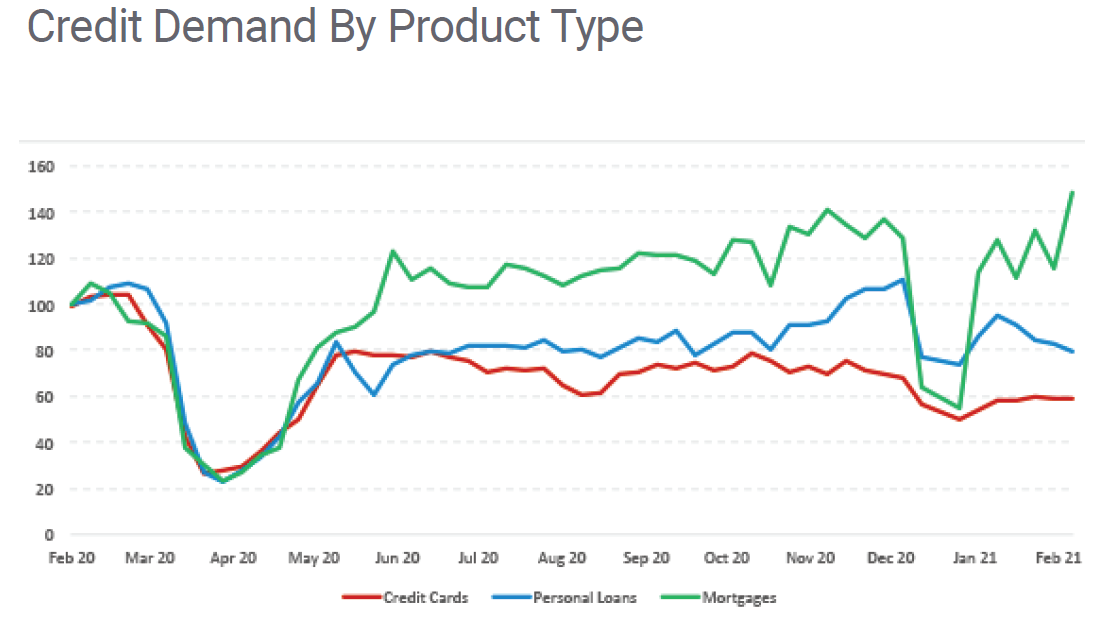

New credit card applications are down 40% on what they were prior to the onset of Covid, according to credit bureau Centrix in its monthly review of credit trends.

Centrix says people took steps to pay down their credit cards last year and diversify their spending through options like debit cards and Buy Now Pay Later.

"With recent consumer confidence stable, and retail spending remaining strong, we will be interested to see if there is a reversal in the downward trend for credit card demand," Centrix managing director Keith McLaughlin said.

One thing seeing plenty of demand is mortgage lending.

"Mortgage lending has continued to climb and is now up 50% year-on-year as the booming housing market continues to drive credit demand," McLaughlin said.

But credit means debt - and Centrix says after a historically low month in December, arrears levels have climbed almost across the board at the start of this year.

"While still at low levels, the overall proportion of accounts reported in arrears went up 10% in January with seasonal increases seen across all credit types.

"In fact, credit cards arrears have increased to the same level as April 2020 when we were in the middle of the Alert Level Four lockdown. This might be an early warning that some households are facing significant financial strain."

And its not just card debt. Mortgage arrears are climbing.

"Residential mortgage arrears increased for the fourth month running, with 17,000 mortgage accounts currently past due," McLaughlin said.

"With the mortgage deferral scheme scheduled to end on 31 March, we will be watching very closely what happens with mortgage arrears next month."

By industry, vehicle finance was the top source of credit demand in February, up nearly 15% year-on-year, another sign of confidence as consumers look to borrow for discretionary items.

McLaughlin said following the Christmas spending season, Buy Now Pay Later demand eased back to "more regular levels" .

"Interestingly non-bank financial services products like credit cards and unsecured loans are at the lowest levels recorded since May 2020, as Kiwis seem to be shying away from higher-interest credit products."

20 Comments

50% increase in mortgages year on year. That, in the context of Covid and contracting credit issued to businesses is simply mania. You can't call this situation healthy, sustainable or beneficial to the long-term economic prospects of this country. I liken it to the Titanic slipping beneath the waves. As the deck area reduces more people are concentrated in an ever smaller section of the ship. Such is the situation in NZ property. It is the stern. The last bastion of illusion that this gamed system is worth your time and effort. Lives are built on this financial wizardry. Families raised and fortunes earned. Without it, we are in the freezing Atlantic of low productivity and decades of underinvestment in education and innovation. Most people should be cheering Orr and the bilge pump, because those people will suffer in a future of hard honest work.

I suspect your description has merit Rosey. Also, there is no good data on the extent to which h'holds are living paycheck to paycheck. I'd imagine it would not paint a good picture. And I suspect this was 'normal', even before Covid. Flash Harrys are a dime a dozen in NZ, even though many of them probably don't have 2 sticks to rub together.

The RBNZ with all its undemocratic powers cannot insulate our economy against a shock that both sabotages the primary incomes of high LVR borrowers and also reduces the recoverable value of their mortgaged properties to below equity.

"Residential mortgage arrears increased for the fourth month running, with 17,000 mortgage accounts currently past due," McLaughlin said. "With the mortgage deferral scheme scheduled to end on 31 March, we will be watching very closely what happens with mortgage arrears next month."

How many of these houses will be forced to go on the market after March? Even if only a third of them need to, that's still suddenly at least 5k houses all in the market all at once. Suddenly, oversupply.

Even if they were all in Auckland (and assuming that all of those people are magical and no longer need somewhere to live) that'd still leave us ~45k houses in accumulated undersupply based on RBNZ, MBIE, Treasury and Council estimates.

Latest estimate was ~40K empty houses in Auckland alone.

There are about 7,000 empty homes in Auckland, based on net figures I have worked out. The higher figure is Gross and is meaningless.

I hope that Cat Maclennan is a better Lawyer than a researcher.

Yeah but it never seems to work like that does it ? In fact nothing these days works like predicted, something comes out of left field and blindsides it. What are the chances of this government suddenly introducing a special mortgage assistance package for those 17,000 in strife ?

This would send a very negative message telling people the can over-leverage themselves with no consequences which would heat up the market even more. I doubt they would be that stupid but hey wouldn't be surprised if that happens given this Government's track record.

They have already sent that message by granting the deferrals in the first place.

The financially prudent and responsible are a laughing stock in this clown country.

I think that's guaranteed. Absolutely baked in. If there are a lot of mortgages at risk of default, having the Gov't step in to pay the shortfall keeps the banks happy, keeps the Hosk happy, keeps the market up and proves how great our economy is going. Great optics all round. Slap on the back.

Speaking of the ZB troll farm, I see the PM has cancelled her weekly interview with the hosk.

Times are a changing. It's no longer as important to pander to the outnumbered boomers whose radios haven't changed off 89.4 since FM was introduced.

You do realise that people outside your bubble exist right. That there are views other to your own and the baby boom generation are often the ones with the most business, political & investment control. You need to work with people and understand how they formed views in order to make changes and have a larger population buy in to your ideas. Or are you falling for the same old ignorant trope of calling the silent gen boomers. It is not in anyway funny, it is just derogatory.

Well it wouldn't keep me happy.

I'd be looking back over the last decade thinking I should have lived less frugally, lived it up a bit more then waited for my bailout.

Would be interesting to see the No of rate arrears, last figure I saw for Christchurch was 24,000 properties, what is it now and what are the figures for wellington& Auckland???

"But credit means debt "

Someone had better have a quiet word to Keith McLaughlin.

As was so well explained to us by a fellow poster earlier in the week, "Credit means Balance Sheet Expansion" not Debt!

I'm not too concerned by the residential mortgage borrowing figures, we just have to acknowledge that the New Zealand financial system will be increasingly vulnerable to changes in interest rates (e.g. inflation) or unemployment. We are trading economic stability for growth.

and getting neither

I'd be quite happy for the govt to buy those residential owner occupier distressed mortgages that would most likely default and pay the bank what it is owed and not the market value of the house and rent it to the incumbents. At some stage in a few years time they could be offered back to the incumbents who defaulted in the first place to buy back at a market related price. Failing that back on the open market or keep depending on the situation at the time.

Soo what happens to any equity they have? And given the 15% price rise in the last year they almost certainly do have a chunk of equity.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.