By Daniel Hynes and Soni Kumari*

Highlights

•Investor demand for gold is strong, amid heightened geopolitical risks.

•We see gold continuing to be a good hedge against inflation.

•Prices are sitting in a neutral zone of USD1,920–50/oz .A break above USD1,960/oz would be a bullish signal.

Outlook

Heightened uncertainty stemming from geopolitical tension has raised concerns over higher energy and food prices. Although history suggests that the impact on the market of geopolitical tension is usually transitory, this time looks different. Stagflation risks are rising, encouraging investors to divert funds to safe havens such as gold.

Central banks are tightening monetary policy as part of efforts to contain inflation. Supply chain disruptions and elevated commodity prices may prompt the US Fed to make more aggressive rate hikes through the year, dampening investor appetite for gold. The downside looks limited, with gold well supported at USD1,900/oz over the next six months, in our view.

Investors demand for gold in futures and ETF flows is robust. Central bank gold buying is likely to continue this year, despite January’s net fall. The Central Bank of Russia (CBR) has resumed gold purchases after a two-year break, but it may have to buy from domestic miners because of war-related sanctions.

We expect gold to remain well bid in the short term. Further upside looks possible after closing above USD1,950/oz last week. The price of silver will largely follow gold, given the geopolitical backdrop.

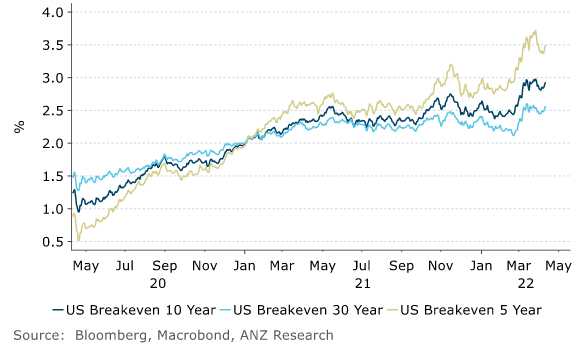

Figure 1.Inflation expectations are elevated

What has been the primary driver of gold?

As gold is a good hedge against uncertainty, geopolitical turmoil will be the primary driver in the short term. The consequences of the various crises are likely to support the market in the second half of the year, as indicators suggest higher inflation and slowing growth. Although much economic data indicates expansion, things could turn swiftly. The US yield curve is flattening, suggesting expectations of a slower growth. The macro backdrop looks challenging, with central banks finding it difficult to set policy for 2H 2022. Market volatility is likely to remain elevated, which should see them building strategic positions.

How long can geopolitical events sustain higher gold prices?

Previous geopolitical events suggest such crisis have a fleeting impact, and gold quickly sheds its safe haven gains once the event subsides. Geopolitical risk does not trigger long-term monetary policy adjustments. The most recent similar event was the invasion of Crimea in February 2014, which saw gold rising from USD1,220/oz to USD1,382/oz on 14 March. But those gains were quickly lost, with prices falling 7% in the next14 days and 10% over the next three months. Should the geopolitical crisis trigger an economic slowdown and then monetary policy changes, this could lift prices for longer.

How different is this geopolitical crisis?

This is a relatively bigger set of crises than any since World War II and is coinciding with a particular phase of the business cycle. Inflation is rising rapidly, and conflicts and the pandemic have caused commodity supply shocks that could keep pressure on real rates, which, prior to the pandemic, had fallen very close to record lows, creating a supportive backdrop for gold. Also, Russia is a major producer of gold so current sanctions will impact supply. Although we expect that to be minimal. Central bank purchases could increase overall, as Russia’s central bank buys gold from its domestic producers.

Will the US Fed rate hikes kill off any rally in gold?

Theory suggests rising interest rates make bonds and other fixed-income investments more attractive, pushing investors into higher-yielding investments such as bonds and money market funds. Rate hikes also coincides with economic growth cycles, which encourage investment in risky rather than safe haven assets.

Is gold a good hedge against inflation in the current scenario?

When gold backed the US dollar, it was a hedge against inflation and a way of protecting investor purchasing power during high inflation periods. Today, its impact is weaker and linked more to inflation expectations than the actual inflation rate. Investor demand for gold has been rising since Russia invaded Ukraine, which is linked to both inflation expectations and haven demand. Should the Fed move aggressively to contain inflation, we could see consequences for the gold market.

How will US dollar movements impact gold?

Normally, the USD is inversely related to gold. A stronger dollar lowers gold prices However, this relationship can weaken during crises, during which both gold and the USD can rise. This was evident during the GFC in 2008 and at the start of the pandemic in 2020. As geopolitics will be a dominant factor this year, gold and the USD could move together in the short-term before resuming their normal relationship.

What would be the impact of US sanctions on Russia?

The US and G7 have announced sanctions, banning individuals from dealing with Russian central bank’s international reserves of gold. Violation of this would draw secondary sanctions on people who trade with Russian gold. This aims to prevent Russia from buying and selling gold. Russia holds2,300t of gold, which is 21% of its total reserve. Sanctions will prevent Russia’s gold from flowing through markets elsewhere but it could still find its way into Asian markets. We don’t see any material impact on the gold market overall.

Does physical demand matter?

While the jewellery sector is the biggest consumer of gold, prices are dictated by investment demand. Unlike jewellery, investment is more volatile and moves with changes in global capital flows. A risk-off tone across financial markets tends to support investment flows into gold. Investment demand has grown by an average of 14% a year since 2001.

Due to a strong inverse correlation with many other asset classes, gold performs well as a risk diversifier. When the equity market plunged in 2008–09, gold investment demand jumped by around 100%. A portfolio containing gold would have seen much better returns than one without.

Daniel Hynes and Soni Kumari are commodity strategists at ANZ. This article is a re-post from ANZ and is here with permission.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

9 Comments

If this were an article on property there would be 50+ comments already…but hours now and none.

Gold/miners has worked well for me the last few years. I added to my holding back in 2019 when things looked frothy and 2/10 inverted. That $$ has doubled in 2-3 years.

If there is a further rush to safety as share/property markets retreat, then it might be a good time to switch from gold back into shares/property.

But who knows what the future holds with crazy central bankers doing what they can to protect the debt ponzi they are trying at all costs to protect 🤔

Stagflation might be their version of kryptonite.

Do you hold physical gold in a private vault or through some ETF?

Any pick on miners such as NST:ASX?

If this were an article on property there would be 50+ comments already…but hours now and none.

Yes, To be honest, I'm very frustrated with gold (reasonably satisfied with silver). Compared to other commods, the price performance is dreadful. I just watched a Kitco interview with Gary Wagner and he's talking about a 20% retracement and gold peaking in 2022 and being flat for a few years. Being a long-term gold owner, I think that is pathetic in terms of market price. If that's the best we have with all this money printing, every other asset price will need to collapse by 60-70% to make it s worthwhile hold in the medium term.

Similar timing to yourself. Once it become apparent that Fed can’t raise rates it’ll be off to the races.

Also any think that bonds won’t become preferable to gold until the real rate becomes positive again? Which given inflation that might require yields to be over 8% which I think would be a stretch too far for our economies to manage…

Interesting times ahead.

Holding bullion is seen as unsexy (poor returns) and risky because you might get burgled. There are imaginative ways to store it plus, if you fancy buying some when everyone else is, good luck! Premiums will mean you will pay well above spot price, if you are lucky to find a supply. It is primarily a store of wealth and I recommend Googling <b> Exter's Inverted Pyramid </b>. Mike Maloney's Hidden Secrets of Money series is worthwhile watching too. https://www.youtube.com/watch?v=DyV0OfU3-FU

I don't whether gold is a good investment now, but what I don't understand is why this blatant marketing is permitted on this site.

Do you also disapprove of the blatant marketing of real-estate when there's an article about housing? (which is pretty much every other day) Or blatant marketing of fiat currency when there's an article about monetary policy or exchange rates? What about cryptocurrency or the equity market, or the uranium, Nickel, Palladium & Platinum markets. interpreting a financial article as "blatant marketing" seems kinda weird.

Pax Gold digital tokens staked on Celsius with a 5.4% APY is looking attractive

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.