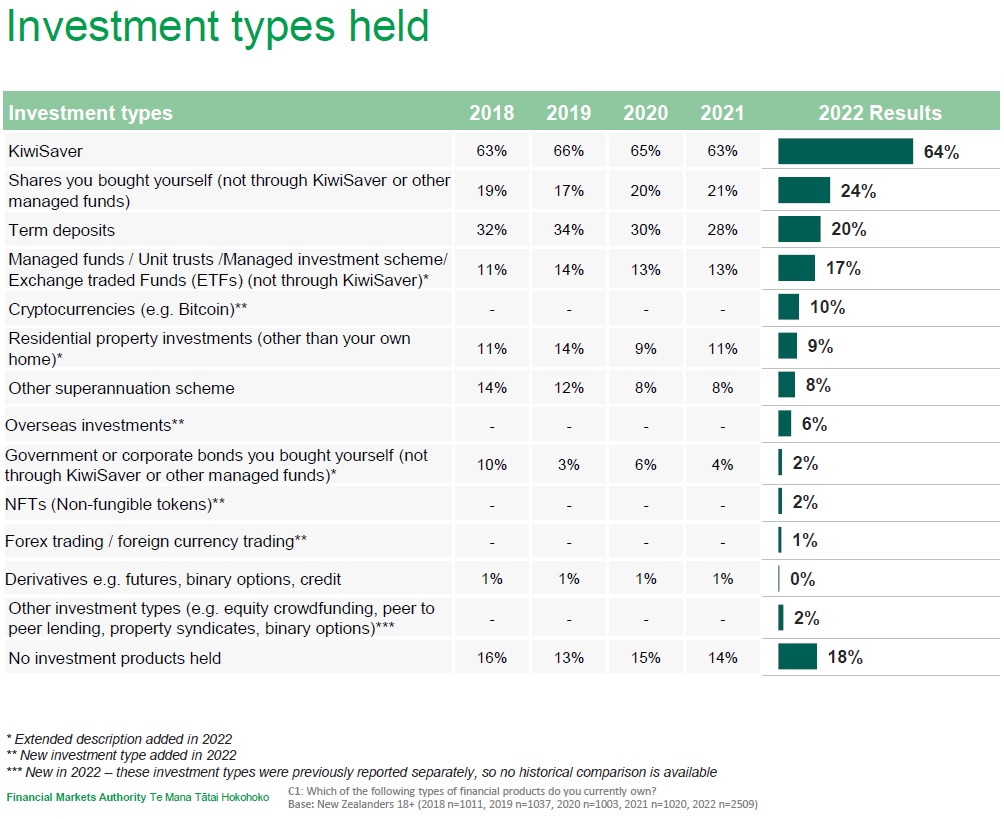

One in 10 Kiwis are now holding crypto assets, according to the latest survey conducted for markets regulator the Financial Markets Authority.

And direct investment in shares has overtaken term deposits in popularity for the first time in the survey, although KiwiSaver remains by far (64%) the most held type of investment.

Meanwhile, confidence in New Zealand’s financial markets has slipped back in the past 12 months, after last year’s record score, but overall, two-thirds of investors remain confident.

The Financial Markets Authority (FMA) - Te Mana Tātai Hokohoko 2022 Investor Confidence Survey shows 66% of investors remain confident, compared to 72% in 2021.

The FMA said this year’s score is consistent with investor confidence levels recorded in 2019 and 2020, and has been impacted by the most recent Covid-19 uncertainty and global events.

This is the 10th FMA Investor Confidence Survey. It was conducted by independent market research firm Fiftyfive5 via a 25-minute survey among a representative sample of 2,509 New Zealanders aged 18 and over between March 15 and April 11, 2022. The FMA said a larger sample size this year has enabled the FMA to obtain greater insights and deeper demographic information beneath the scores.

FMA chief executive Samantha Barrass said: "It is no surprise that overall market confidence fell back in the last 12 months, given the volatility we have seen. The prolonged impacts of COVID-19 on supply chains, the end of quantitative easing by central banks around the world, and the return of inflation internationally, have significantly shifted market sentiment, both at home and abroad."

While the 2021 survey had asked about crypto in terms of 'new' investments made by people, this year's survey has for the first time included crypto assets in the list of investments already held by Kiwi investors. And it shows that 10% now hold crypto.

The FMA doesn't have a regulatory role with crypto as such, but some crypto activities can fall within its regulatory remit. The FMA does include detailed information on the subject on its website.

And it describes crypto assets as "high risk, speculative products that operate differently to traditional investments. Only invest what you can afford to lose and use New Zealand-based platforms to give yourself some level of protection".

Last year the FMA made a submission to Parliament’s Finance and Expenditure Select Committee when the committee held an inquiry into "the current and future nature, impact, and risks of cryptocurrencies".

In that submission it said: "As a general observation, most offers of cryptocurrencies and most cryptocurrency exchanges deliberately structure themselves to operate outside of the reach of mainstream markets or securities regulation.

"There has not been a regulated offer of cryptocurrencies yet in New Zealand nor is there a regulated financial product market here. We have however seen a number of offers made in other jurisdictions that may have been taken up by people in New Zealand. The regulatory protections available in such circumstances are very minimal," the FMA said in that submission.

Back on the latest survey - it also shows that 24% of those surveyed now directly own shares - IE ones they've bought themselves rather than through KiwiSaver or other managed funds.

That's up from 21% last year. And it compares with just 20% now holding term deposits (down from 28%). Managed funds have also risen to their highest level at 17%.

Barrass said it was the first time since the survey started recording - in 2016 - detailed information of what investments people actually held that there were more investors in shares than term deposits.

"Building on last year’s trend, term deposits have continued to decline, while investments in shares and managed funds continue to rise. This represents a notable shift in investor preferences, as we have traditionally seen New Zealanders choose more conservative assets," she said.

In terms of detailed results from the survey, although overall confidence is lower than in 2021, investors and non-investors alike feel more confident that New Zealand financial markets and financial service providers offer good long-term opportunities (71% in 2022, vs. 63% in 2021), offer protections for investors and customers (66% in 2022, vs. 61% in 2021), and are more confident that they will be treated fairly (70% in 2022, vs. 65% in 2021).

Despite this, just three in 10 New Zealanders feel confident that they would know what steps to take if they experienced unfair treatment from a financial services provider.

Investor confidence in effective regulation is stable at 65% of investors surveyed, slightly down, but within the margin of error, from 67% in 2021. “While market sentiment has impacted investor confidence it is pleasing that confidence in the regulation of the markets has held up and more investors have confidence that they are provided protection, and are fairly treated,” Barrass said.

This year the confidence of non-investors in both the markets and effective regulation has increased considerably, suggesting there is an increasingly positive sentiment towards investments, even from the sidelines.

Fewer people recalled receiving investment materials compared with last year, (down from 80% to 70%), and there was a small drop among this group who found the materials helpful, now at 59% (from 63% in 2021).

"However, encouragingly, among those who found materials helpful, there was a large increase in the investors who said the materials were clear, concise and effective, up from 74% to 85%, this year.

“The usefulness of investment materials is an important focus for the FMA as we want investors to make well-informed decisions. There is an onus on providers to make sure materials are easy to understand. Clear disclosure makes an essential contribution to acting in the best interests of clients.” Barrass said.

Those surveyed who are aware of the FMA are much more likely to say that the FMA helps promote trust and confidence, integrity, and fair and efficient, transparent markets. These scores also tend to be higher among older men, with higher incomes.

“The FMA’s mandate is now expanding from investors to consumers of all financial products. Our surveys will start to reflect this evolution in our mission to the promote the fair treatment of all customers of financial services,” Barrass said.

31 Comments

Crypto was the talk in 2021, even more so when Elon Musk bought some.

Residential properties had a 5 year run, mega landlords are millionaires. And many owner occupiers are wealthier than they have ever been.

Managed funds did well for the past few years, the new interest environment rocked and dismantled trading strategies. "Growth funds - invest for 5 years to see the results, even all the ups and downs" like the end cycle of a ponzi.

I see some "Investments" as pure desperate get rich quick schemes to try and get ahead. Plenty of people at the bottom who can least afford it get burned while the people at the top get richer.

I see some "Investments" as pure desperate get rich quick schemes to try and get ahead. Plenty of people at the bottom who can least afford it get burned while the people at the top get richer.

100 XRP aint going to make you rich. But there are some benefits in owning it: You have to go through the processes of buying the coins and storing the coins. Hopefully, you will learn some other basics like how to take coins of the exchange and storing them in a secure wallet (ideally cold storage). However, the cost of a storage device is going to be far more than 100 XRP.

Crypto? Wait until the public realise their houses are filled with one of New Zealands rarest and most sought after assets, plaster board.

this will not end well

So a lot more people have tiny amounts of money invested in shares and crypto. Others have been waiting to see what term deposits are going to do before committing.

These figures don't indicate any growing confidence in shares and crypto, just that a lot of people are dabbling as there isn't much else to do with property being so expensive, lockdowns and very low term deposit interest rates.

I doubt it is indicative of an investing renaissance. Probably just creating a whole new swathe of disillusioned people.

TDs are looking more attractive by the minute. The FED just went 75bp nearly doubled the rate in one hit. Will be interesting to see if that 20 billion reappears in banks here as savings now.

So a lot more people have tiny amounts of money invested in shares and crypto. Others have been waiting to see what term deposits are going to do before committing.

What is a 'tiny amount'? And remember everyone has to start somewhere. Buying and selling shares online is nothing new. People have been doing this for 25 years now.

Crypto assets?...

LOL

You are now laughing at your own comments Carlos? Bit desperate..

Bitcoin is the equivalent of the Semper Augustus tulip, rare, striped and expensive between 1623 and 1637. Other more common tulips were cheaper to bet on, just like most crypto tokens. Then by mid 1637 they all just became tulips again, with literally no value.

I'd say Bitcoin is more the equivalent of this lazy worthless analogy.

I like the Warrent Buffet rule, only invest in what you understand. I own no crypto... I understand blockchain (IT background) but still don't see the value.

At least the "bitcoin is an inflation hedge" nonsense can be laid to rest.

The best inflation hedge available to everyday people is to go long when fixing your loans and ride it out.

The best inflation hedge available to everyday people is to go long when fixing your loans and ride it out.

Debt slavery is the primary reason why the world is massively overleveraged. Resigning yourself to it being the best one can acheive is actually part of the problem.

The best arguments for crypto to me only legitimise a case for it as a service, rather than an actual unit/store of value itself. Like a modern day Western Union or MasterCard. I can't see why you'd want to have your wealth tied up in what is really a transitory state.

Only 9% of people own a residential investment property....

Only invest what you're willing to loose... Or loose 7% per annum in cash.

You $800k in cash looking good compared to the $800k sh##t box purchased last year.

Great for any FHB's with cash, their cash going up in value for that home every day.

One in 10 Kiwis are now holding crypto assets

Sounds like absolute BS to me.

'maybe perfectly true over two months ago but many investors would have lost resolve as they switched from "fear of missing out"to fear of doing their dough.

I'd say so, don't you get a few coins when you win a Candy Crush level to share with your friends on facebook?

So back it up then Rastus...do some digging and report back. Or just keep firing your worthless salvos..

A bit titchy this morning...owns crypto? I really don't care to back it up, but I can still call it BS.

Fair enough, didn't think you would bother. When do you think BTC to hit zero..this year, next year, the year after?

Actually after reading a book on early man and how values developed over time, I can see how it might work as a value of exchange. I can also see how good it could have been for developing countries, small villages, no banks, but with just a cheap phone. But just like the way google emerged from thousands of start-ups, which crypto comes out to be the 'one' is the question.

In this era of more and more 'control', I suspect the 'one' will be State driven.

Hardly surprising that with so much money in the system people are using it on speculative assets. This is just a consequence of reserve banks actions.

Crypto seems of no use other than to provide criminals a means to wash their cash, and to move it unseen across borders.

Hope the Joe Average investors riding out this very big slide downwards don't mind the fact they've given their money to drug lords and arms traders, and now have nothing but a digital key to try to feed and clothe themselves with.

Why use BTC when you can use your local bank?

Banking giant HSBC has been fined £63.9m by the UK's financial regulator for "unacceptable failings" of its anti-money laundering systems.

The bank has not disputed the findings and agreed to settle, resulting in its fine being being cut from £91m.

HSBC's failings cover a period of eight years, from 2010 to 2018, the FCA said. The regulator said there was "inadequate monitoring of money laundering and terrorist financing scenarios until 2014, and poor risk assessment of "new scenarios" after 2016.

What a shame we can't monetise played-out, irrelevant talking points. I'd be on Easy Street.

But sure dude, that's all it can be used for.

The most horrifying thing in that information from the FMA is that either they (or the participants) appear to think that NFTs are a legitimate investment class.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.