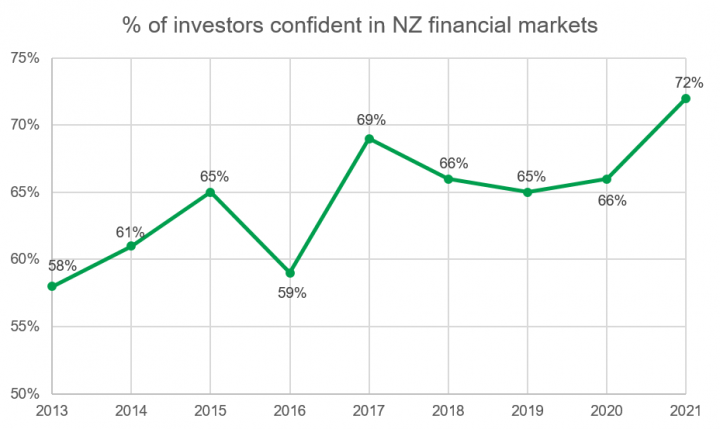

Investor confidence in New Zealand's financial markets is the highest it has been for at least eight years, according to a survey conducted on behalf of financial markets regulator the Financial Markets Authority (FMA).

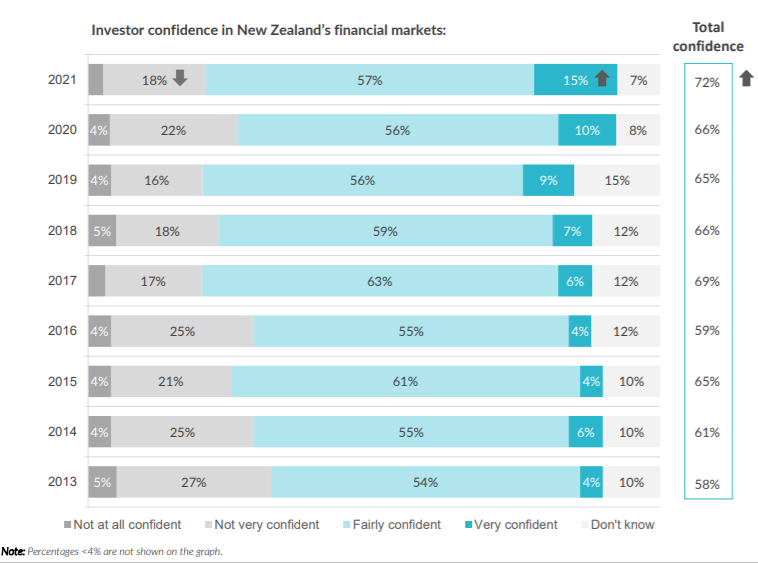

The FMA's annual investor confidence survey shows 72% of investors are confident in the country’s financial markets. That's up from 66% last year, and is the highest since the survey began in 2013.

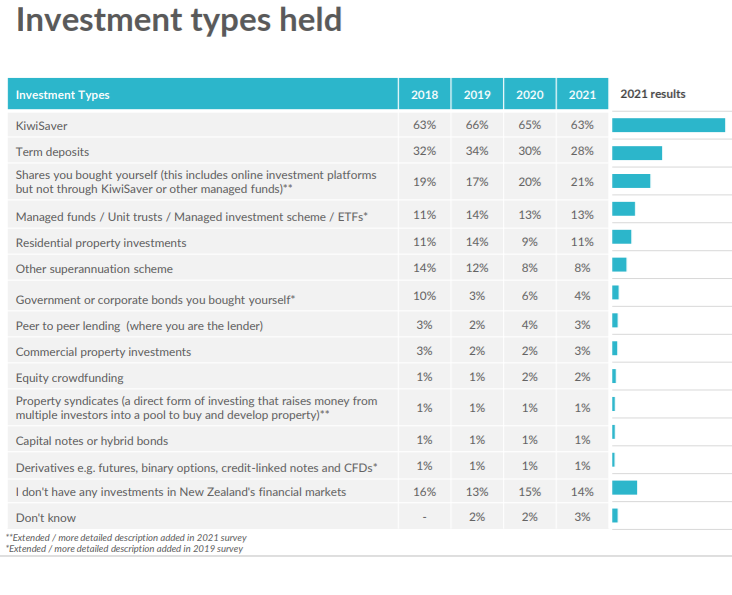

Although the types of investments NZ investors hold hasn’t changed much over recent surveys, over the past three years, the number of people holding term deposits has dropped and the number of people holding shares has increased. This year 28% of investors surveyed hold term deposits, down from 34% three years earlier, and 21% hold shares, up from 17%.

When asked about investment activity over the last 12 months, 23% of respondents indicated they increased or made new investments, up from 17% in 2020. Buying shares online through an online investment platform was the most common activity at 43%. Next most common was managed funds at 26% and investing in residential property at 19%. Meanwhile, 13% purchased cryptocurrencies. It was the first year the survey asked about cryptocurrencies.

The FMA was launched in 2011 by the then National Party led government in place of the discredited Securities Commission. A key purpose of the FMA has been to restore retail investors' confidence after the wholesale collapse of the finance company sector and high profile share market casualties such as Feltex. Additionally Simon Botherway, chairman of the FMA Establishment Board, told interest.co.nz in 2010 a measure of the FMA's success would be greater investment outside property over time.

FMA CEO Rob Everett says it’s encouraging to see investor confidence in the regulation of NZ’s financial markets has remained steady at 67% (versus 68% in 2020) and, almost two thirds of investors continue to acknowledge the usefulness of the investment materials they receive. But he says these are two key measures both the FMA and the financial services sector can always seek to improve.

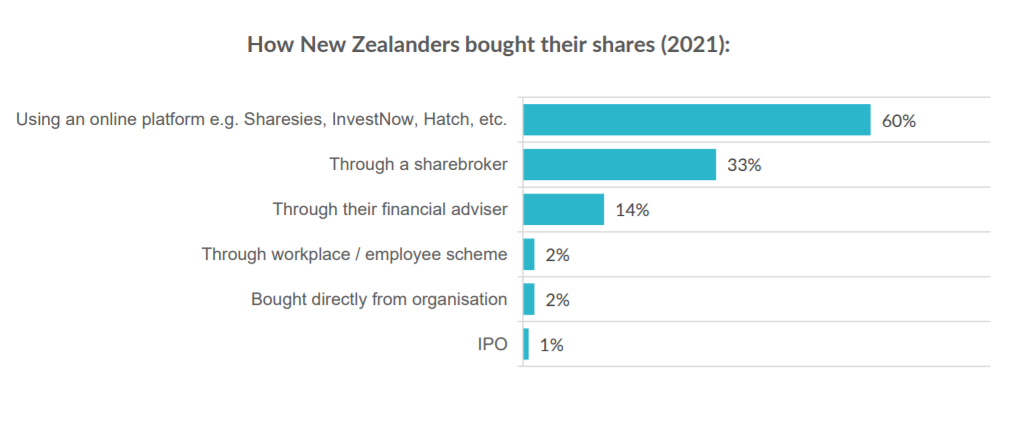

“Term deposits have tended to be the most prevalent investment product outside KiwiSaver, but in this low interest rate environment, with changing behaviours and preferences, individual shares are closing the gap. This aligns closely with the rise of DIY, or fractional, digital share investing over the last few years, with 60% of share investors now buying shares through these platforms,” Everett says.

The survey shows confidence is notably higher among male investors than female investors (+3 percentage points), those who have a household income of $150,000 to $200,000 (+17 percentage points), and those in full-time employment (+9 percentage points).

The top reasons given for feeling confident include:

• Observing or experiencing a strong bounce back from COVID-19 (New Zealand recovering better than other countries in terms of post-COVID-19 response);

• Having trust in the market, Government, or authorities responsible for regulation;

• Having high levels of knowledge of the markets and keeping informed/ updated.

Reasons for lack of confidence in the markets include lack of knowledge about the NZ financial markets and how they work, and uncertainty or lack of stability due to the impact of COVID-19, general instability of the economy, and uncertainty around the Government and its influence in the markets.

The survey results suggest 83% of New Zealanders aged 18 years and over hold an investment of some form, which has remained consistent over the past four years. At 63%, KiwiSaver remains the most common form of investment among New Zealanders, with the survey results suggesting it's the only investment held by three in 10 Kiwis.

The FMA commissioned Buzz Channel to undertake the survey. It was conducted online with 1020 people aged 18 or over between April 23 and May 17. The main objectives were to measure the level of confidence the public has in NZ financial markets and perceptions of the FMA and regulation.

13 Comments

It has nothing to do with confidence in markets.

People appear to piling into Shares because,

a) They can't afford property

b) Bank rates are $h!t

c) Easier to access due to rise of online apps, and

d) everyone else is piling in.

Has a very ominous 1987 feel about it.

Sure does.

when people pile in to investments they havnt even researched, you know the end is near!

Had a couple of conversations recently with people who are basically speculating in the stock markets, meme stocks and cryptos. They were not able to tell me why they thought they were good investments.

Caveat Emptor....

Yeah. Except that our institutions don't believe in Caveat Emptor -- they believe that every investor has a human right to make a profit. From South Canterbury Finance to the GFC...

They'll be bailed out if the SHTF. Asset holders are the only people that count, regardless of which gov't is in power. It'll be framed as bailing out ordinary folks' Kiwisaver.

Not Caveat Emptor more like a fool and their money are soon parted.

FOMO like property was

They'll have made money pist covid after the market crashed so they'll be feeling pretty good about the paper profit.

If the fundamentals aren't there to justify the value, be that asset base, profitability or future potential then its very risky.

Why would you hold Air NZ based on the future of tourism and air travel viability post covid and under the climate change concerns, yet people pile in.

It is about fundamentals, just not individual company fundamentals.

The whole NZX relatively small. So supply is limited. Yet we have a whole lot of guaranteed demand in the form of KS contributions piling into it every single month, and at this stage very little is being withdrawn.

In my view it doesn't matter what the state of the individual company is, as the general price of shares will increase. You may win or lose on individual shares, but globally superschemes will ensure stockmarkets continue to increase in value.

Both my adult children are into investing; shares, managed funds and crypto. They're all over a wide range of online forums. Think Reddit. They know there's no point saving money in the bank. They're light years ahead of me when it comes to tech shares.

Although the types of investments NZ investors hold hasn’t changed much over recent surveys, over the past three years, the number of people holding term deposits has dropped and the number of people holding shares has increased. This year 28% of investors surveyed hold term deposits, down from 34% three years earlier, and 21% hold shares, up from 17%.

Nonetheless,

Every security that is issued must be held by someone until it is retired

Consider a world where Alice has $100 of what people call “cash on the sidelines,” and Becky owns some stock certificates in ABC. It seems obvious that Alice can take her “cash on the sidelines” and instead put her cash “into the stock market” by buying 10 shares of ABC stock from Becky at $10 each. These phrases like “cash on the sidelines” and “moving cash into the stock market” all make sense, as long as we ignore Becky. Unfortunately, the moment we think about Becky, it’s clear that both phrases are completely incoherent.Who holds the cash now? Becky. It hasn’t somehow moved “off the sidelines.” Who holds the stock now? Alice. All that has happened is that the owners have changed. In equilibrium, there are no “sidelines.” The stock market isn’t some big jar on Wall Street where money “flows” in. Every security that is issued, whether it’s base money (currency and bank reserves), or stock shares, or bond certificates, must be held by someone, exactly in the form it was issued, until it is retired.A https://www.hussmanfunds.com/comment/mc210614/

You forgot about the central banks buying MBS and other forms of debt. New debt issuance being used to speculate in the stonk market. Then there are companies buying their own shares.

No reference to the ol' rat poison and other digital assets. Are the people at the FMA in 2021 or they stuck in the past?

The question about FMA is not so much about being stuck in the past, present or future, it is more a

question of just what are they focusing on...and I think the answer to that is..."themselves", ie growing the bureaucracy, salaries, job satisfaction, etc.. like most of our civil service. Just think of the $m of investor time wasted on meeting FMA b----s---. for each and every financial instrument they choose to make. How many significant money launderers and fraudsters have they caught? Count the bank time processing all this paperwork, time spent by investors, money taken by FMA in audit fees....has it all been worth it or are they just as useless as the old unlamented securities commission?

The question about FMA is not so much about being stuck in the past, present or future, it is more a

question of just what are they focusing on...and I think the answer to that is..."themselves", ie growing the bureaucracy, salaries, job satisfaction, etc.. like most of our civil service. Just think of the $m of investor time wasted on meeting FMA b----s---. for each and every financial instrument they choose to make. How many significant money launderers and fraudsters have they caught? Count the bank time processing all this paperwork, time spent by investors, money taken by FMA in audit fees....has it all been worth it or are they just as useless as the old unlamented securities commission?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.