The Financial Markets Authority (FMA) is reporting a big spike in the amount of money withdrawn by the over-65s from KiwiSaver accounts in the past year.

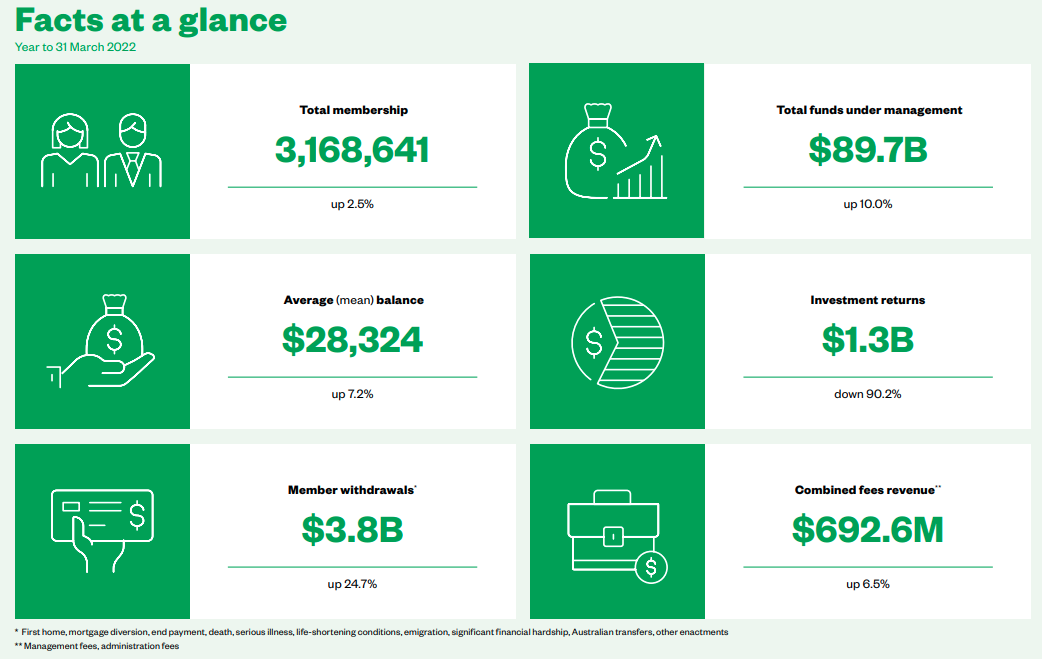

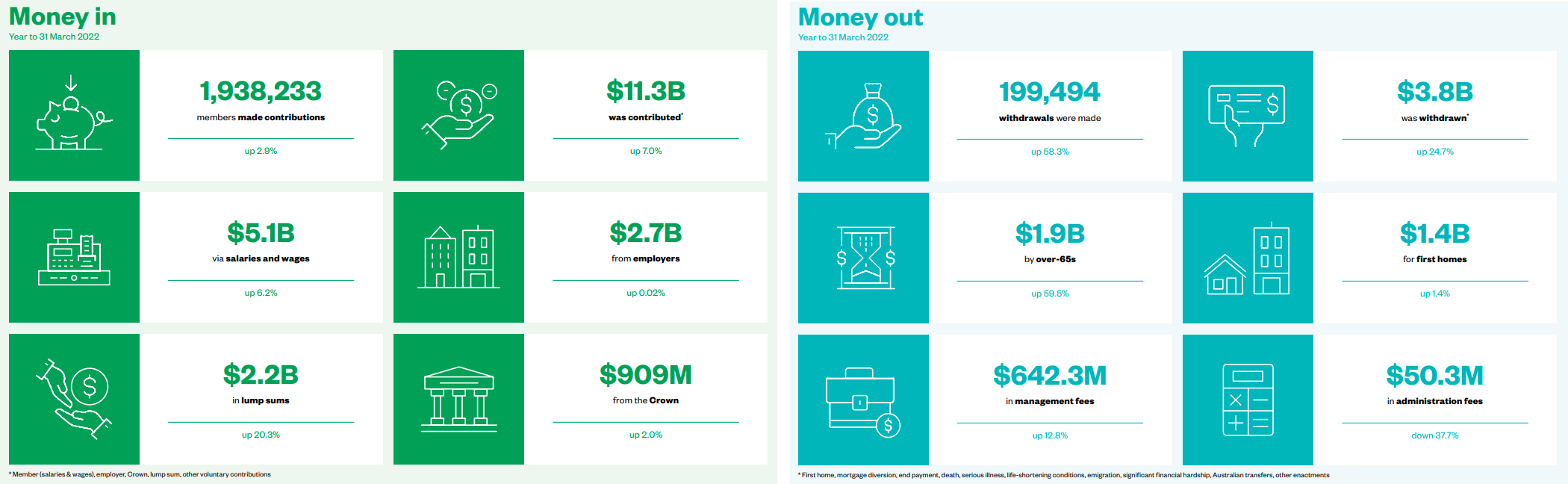

The FMA's KiwiSaver Annual Report for 2022 says that in the year to March 2022 the over-65s withdrew $1.95 billion – which was up a whopping 59.5% on last year’s $1.22 billion, and almost double the amount this age grouping withdrew just three years ago.

"This means retirees are again the biggest withdrawers, after a dip last year that saw them exceeded by first home buyers for the first time," the report says.

More retirees chose to fully exit KiwiSaver this year too – up 10.0% to 21,466.

The number of over-65 members kept growing, however, by 14.0% to 168,028 – on top of last year’s 15.0% increase.

The FMA said this trend is in part due to KiwiSaver being more popular with ‘younger’ people over the past 15 years, i.e. more signing up in their fifties, who are now reaching retirement age.

Asked about the big spike in withdrawals in the past year, an FMA spokesperson pointed to the move as "a sign of KiwiSaver’s maturity and that is working as designed", meeting its original purpose of providing income in retirement.

"We expect the amount withdrawn by over-65s will continue to increase in years to come."

First home withdrawals stayed relatively static after rising a lot last year, up just 1.4% to $1.44 billion.

However, this is still double the amount withdrawn in the year to March 2018, which the FMA said can be attributed to the corresponding rise in house prices, and heightened public awareness of KiwiSaver home withdrawals.

With unemployment down during the year, so too were significant financial hardship withdrawals, decreasing 33.4% to $106 million, back to the levels seen before a jump last year.

In terms of the big picture over the past year, KiwiSaver investment returns were $1.3 billion, a sharp fall on 2021’s extraordinary $13.2 billion gain, yet up on 2020’s Covid-induced $820 million loss, and in line with the more ‘normal’ year to March 2019, which gained $3.8 billion, the FMA said.

KiwiSaver funds under management have shown net growth of 10% to $89.7 billion for the year ended 31 March 2022, despite another turbulent period for global markets.

The 10% net growth in funds under management was largely driven by $11.3 billion in contributions from 1,938,233 members. This included a significant 20.3% increase in lump sum contributions, totalling $2.2 billion.

"After its 15th year, KiwiSaver’s size is now equivalent to around 25% of national GDP (up from 15% of GDP in 2017)," the FMA said.

FMA's director of investment management Paul Gregory said the data in this year’s report shows the strength of KiwiSaver as a long-term savings vehicle, with resilience to volatility a necessary feature of its design.

"While we celebrate World Investor Week, the report reinforces our messages about taking a long-term view for investing."

The total amount invested in growth and balanced funds surged 17.7% and 20.8%, respectively, while assets in conservative funds fell 14.4% in part due to bonds suffering significant price declines but also as around 300,000 default members were moved from conservative funds to balanced funds under the Government’s new default provider settings in place from December 1, 2021.

The FMA said the shift in the amounts invested across the different fund types is consistent with a longer-term trend where the numbers of investors in conservative funds (excluding previous default members) has shrunk 3.6% from 2017 to 2022 while growth fund membership has ballooned 54.8% in the same period, now accounting for nearly half of overall membership.

The average annual fee paid by active members rose by just 2.1% to $245, while the average annual fee paid by default members fell 11.1% to $64.

"New Zealanders have become increasingly aware of the role KiwiSaver can play in their financial well-being and preparedness for retirement, particularly when the likelihood of owning a home becomes less certain," Gregory said.

64 Comments

Pull it out and spend it baby, you cannot take it with you. The global uncertainty that has been Covid and now we are basically facing a financial crisis bigger than the GFC, best just to have a good time a spend it while you can.

or take it out and put it into term deposits where there are no fees and they pay more than what "cash" funds do. Sure, like most things now, they have negative return wrt inflation but hopefully this will not be the case for very long.

Doesn't that fly in the face of the adage "it isn't timing the market, it is time in the market?"

NZ Superfund has averaged 10% since inception (2003), gross. Returns are similar for core index funds eg SP500, NZ50. The great thing about a falling market is you are buying more units/shares per dollar invested.

Disclaimer-I have zero skill or formal experience in investing.

Upon the assumption that in the long run markets always go up................

I have my doubts.

All fun and games until you need to be looked after in your old age and that doesn't come cheap. Invest in retirement homes now and reap the long term gains :D

Ryman for example is languishing.

Because its first and foremost a property play.

This is true, and Morning Star have it recommended as a buy stock right now. Good or bad? Time will tell...

"best just to have a good time a spend it while you can."

Bit short-sighted Carlos, sure things are not well now and will get worse, but nothing lasts. You're not investing in Kiwisaver for 2-3 years.

- deleted -

Looks like business as usual

Yes, this is how the scheme has been set up.

No need to point finger at boomers.

We are a ageing country and yes more and more getting old retiring and want their money in their own pockets than in some fund.

It's risky going fully into cash at 65 if you intend to live for another decade or two, or three - almost certain to have your lifestyle nibbled away by inflation. Much better to keep some portion in growth assets.

But its only been very recently that term deposit rates are negative wrt to inflation. With an increasing cash rate it shouldn't be too long before TD rates go +ve.

Trouble is, you need interest rates on the TD to cover tax and inflation just to stand still. If you actually want spending money you either need an even higher rate, or you are eating into the capital meaning you're in a downward spiral hoping you don't live long enough to exhaust the funds.

Keeping some diversity may feel risky but it gives you a chance of outrunning the inevitable risk of inflation acting over a couple of decades.

Fair enough but my plan is to not to have anything saved or in the bank when I cark it. Yes I plan to use it up. Except that my children will inherit my house. (No horrible reverse mortgage planned).

What did you pick for your life expectancy?

Doesn't really matter, when I am really old NZ super plus the little bit of Govt super I get should cover my rates, utilities, house mtce, and a little bit of food.

That's a very reasonable plan. You earned it, you enjoy it. Worth looking into annuities for that strategy - you should expect a higher income than TDs and someone else taking on the risk of running out of cash. The downside risk is you die early and 'lose' the gamble, and the excess isn't available to your kids but that's your plan anyway.

Annuities were (are?) the standard way to approach retirement in the UK. Can be inflation linked, you know exactly what your income will be until the day you die. Good protection against cognitive decline as well as you don't have to make complex decisions into your old age, the money just arrives in your bank account.

Growth assets are by their nature risky. You're saying in the long term they pose less risk than zero risk zero reward?

Failing to keep up with inflation is also risky. You're just trading one kind of risk for another. Diversification gives you a chance of finding the narrow path between inflation risk and volatility risk.

So these two sides of the argument make a really good case for just spend and enjoy it.

And then what do you do when you run out? I guess we have super to keep things ticking over.

Making a decent return on your capital means there is more money to spend and enjoy. The challenge is balancing future needs and returns against your future ability to physically do the things you want to spend money on.

Inflation is really cranking and look at the health of the stock market! Even with all of the kiwisaver money pouring into it!

Much better to keep some portion in growth assets.

Only if you believe infinite growth on a finite planet is possible.

Much better to invest the money in things that will reduce your future outgoings and increase resilience, eg: buy an electric car, pay down your mortgage, insulate your house, install a wood burner, solar panels, batteries, etc.

Sign me up!

That's all great for diversification too, no arguments here. I'd still keep a portion in stocks and property just in case the future actually does look like the past.

If the future does look like the past, it'll more likely resemble something further back than you are probably anticipating with this comment.:-)

Could be, but I'm not sure having a bunch of term deposits would provide much protection from that either.

Maybe part of the diversification is a seed bank and a gun?

An old guy once told me there are three stages to your retirement years..

Go years

Slow go years

No go years

And your better to spend your money in your go years

Its most likely going to get worse, if you are not in it don’t sign up. Manage the money yourself instead of locking it all in and watch it gets eaten away by inflation.

Yes it's going to get worse… and then it will get better… and then worse again… and then better… Don't be short-sighted, Kiwisaver is a long term investment and over the long term, with regular contributions no matter how good or bad returns are, you will have a nice nest egg when you're 65

Unless its worse when you become 65.

Sorry but this is a poor understanding of how investing works over the long term. Whether your Kiwisaver will be in an uptrend or downtrend when you reach 65 will make very little difference!

You think the current system is not near breaking point then??

No, not at all. Were you expecting your Kiwisaver to only ever go up?

If you're an employee you should at least put the minimum in to get the govt and employer contributions. Doubles your money straight away (minus fees etc obvs).

It's not only Kiwisaver that retirees are going to be cashing in to retrieve their savings of a lifetime, to live out their final years. And it's not just New Zealand.

I would say if they took it out last year then they have picked the market right. If they had left in there they would of lost between 10-15%, meanwhile the fund manager takes his cut. Take it out, if you can get 4-5% TD then better than some BS story from a fund manager. After all with a fund manager you are just part of a massive pool of money, they don't really give a hoot about little old Johnny and his life savings.

Better still, become a fund manager…… It doesn’t require any skill - just a fun game of miss and hit at the expense of others.

You’ll be paid plenty and drive round in a fancy car, so you can’t lose.

TTP

Well I know a fund manager, and yes he does spend a lot on his cars. He also does not invest his own money where his team invest the kwisaver funds that roll in every week. He would be sacked if he didn't follow the crowd into the sharemarket.

"Better still, become a fund manager…… It doesn’t require any skill - just a fun game of miss and hit at the expense of others.

You’ll be paid plenty and drive round in a fancy car, so you can’t lose.

TTP"

Or swap 'fund manager' in TTP's comment with 'property broker' and the same applies.

Exactly. A wise move out of growth 9 months ago when it was certain central banks would have to raise rates for 7%+ inflation. Also next year there will be a lot of overseas trips by the 65s to 75s, will be a boom. There will be many kiwisaver withdrawals for this.

I love a good boomer pile-on but 'retirees making use of retirement savings' isn't quite enough of a zinger to work with.

I'll also add that if you're in a position to take cash out now to spend on cashflow-freeing things (like electric cars, solar or clearing the last of a mortgage ahead of refixing) and you aren't confident those funds are going to be there in the future through a market drop then this is a pretty logical thing to do.

That is the idea of KS, isn't it. Use it for your retirement time. Unless the KS funds managers introduce an age specific fund for these 65+, with some decent return guaranteed and capital protection, they would withdraw to fund their living and leisure.

Sounds a bit like an annuity. Which I think nobody offers in NZ?

I recall some stuff about annuities becoming available in NZ sometime within the last couple of years. Not sure if they are actually available, or if they're actually on terms that are attractive or not. They're a bit like reverse mortgages which have higher interest rates, because the provider is making a gamble on how long you're going to live and so have to set the payout at a level that to them seems like they'll be profitable.

Seems to me like there's a huge counterparty risky with such a thing - give them your money now and they promise to pay it back to you at a certain rate forever, but you're taking the risk that they stay solvent. At least if you keep the money in term deposits you're much more directly in charge of what happens to it at any given time.

If (when) super becomes means tested then there will be some compulsion to use your kiwisaver funds to purchase an annuity or similar, otherwise retirees will just spend it to avoid the means test.

Exactly!

Leave it in at your own risk!

Plus you then have the counterparty risk as mentioned in an earlier post on this thread.

https://www.lifetimeincome.co.nz/ used to offer annuities but it looks like they quietly canned that in 2021? Now their product just looks like a fancy income PIE fund.

https://investmentnews.co.nz/investment-news/lifetime-drops-guarantee-i…

Offered annuities with guarantees secured by an insurance policy, ignoring whether they could achieve the returns, how good was the insurance policy if it all went pear shaped? Who owned the insurance policy? How deep where their pockets?

Once you looked at the policy fees, the insurance fees, not sure how the returns could provide the annuity, guess I wasn't the only one that worked that out.

no surprises about the figures,the facts at a glance are compelling you to take the money and run.

And no one has a clue whether tomorrow the world (financially too) will be worse than today so no one knows if taking it out now is a good or bad idea.

https://coingape.com/bitcoin-takes-the-center-stage-amid-talks-of-credi…

Another Lehman-like moment is brewing up in the banking space with Swiss banking giant Credit Suisse being at a “critical” moment now. Credit Suisse Chief Executive Officer Ulrich Koerner said that the bank is preparing for the latest overhaul and has asked investors less than 100 days for a turnaround story.

The Swiss bank’s credit default swaps i.e. the cost of insuring the firm’s bonds against default jumped 15% last week to levels not seen since the 2009 Lehman crisis.

Along with Credit Suisse, Deutsche Bank is also assumed to be in a similar situation. The asset base of these two European banks combined is $2.5 trillion which is four times the asset base of the Lehman brothers during the time of its collapse.

As we see history could be repeating itself, global investors are driving their attention once again to Bitcoin as a safe haven. The decentralized cryptocurrency was created after the Lehman collapse to insulate investors from the global banking institutions and global markets.

I know people that carried on working for an extra year in the hope the fund would go up... how did that work out ...

The guy from the big short has sold ALL his shares (he was just holding a few in old age housing).

Kudos to Michael Cullen here. I hated him but KS is a fine thing.

Yup my father pulled all his out. Now he's spending it on expensive unnecessary crap because its sitting in his bank account burning a hole in his pocket. And we wonder why inflation is so high.

Or maybe it's because inflation is so high that he is spending it on expensive unnecessary crap?

Most retired kiwis probably remember what happened to our previous superannuation scheme in December 1975.

The worst decision by a New Zealand politician, ever | Stuff.co.nz

They probably trust themselves utmost with their money. It's understandable.

Well to be fair he did campaign on abolishing compulsory superannuation (Dancing Cossacks tv commercials and all) so it was no secret. The fact that Boomers voted Muldoon is just consistent with the mentality of that "me me" generation who would rather shift their retirement cost burden onto future generations.

The Comex Gold is being drained by big buyers taking delivery. Foreign banks have been repatriating their gold the past few years.

New Zealand has zero gold reserves. Set up a gold standard. Silver will make triple digits in the next run.

Everybody in the world can see the geopolitical whirlpool in front of us.

Didn't this happen about 18months to two years ago. Comex ran around looking for the real stuff to deliver. LME had to supply them some mas well I think.

I think it did! And it's happened again. The physical market is much smaller than the paper market.. much smaller.

Under Basel III, monetary gold now qualifies as a Tier 1 asset, and is 100% valued in calculations establishing banking viability. However, gold derivatives (which are not considered the same as monetary gold), are excluded from this new framework. So basically, monetary gold is now counted as risk-free capital among banks.

It is the only real money. Not fiat, after all fiat derived from Latin only means "let it be done,"

Annual returns vv fees tell the story, and Grant sold out?

In 20 years, we'll have the same article with "Gen-X cashing out of KiwiSaver" for the headline.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.