Westpac New Zealand is joining some other banks in detailing the impact on its credit card loyalty and rewards schemes of the Government's move to regulate interchange.

Westpac NZ says it's introducing a new tiered system for its consumer credit card rewards following the introduction of regulation to cap some fees paid by merchants to banks. The bank says it's contacting customers who use Airpoints and hotpoints cards about the changes, that kick-in from February next year.

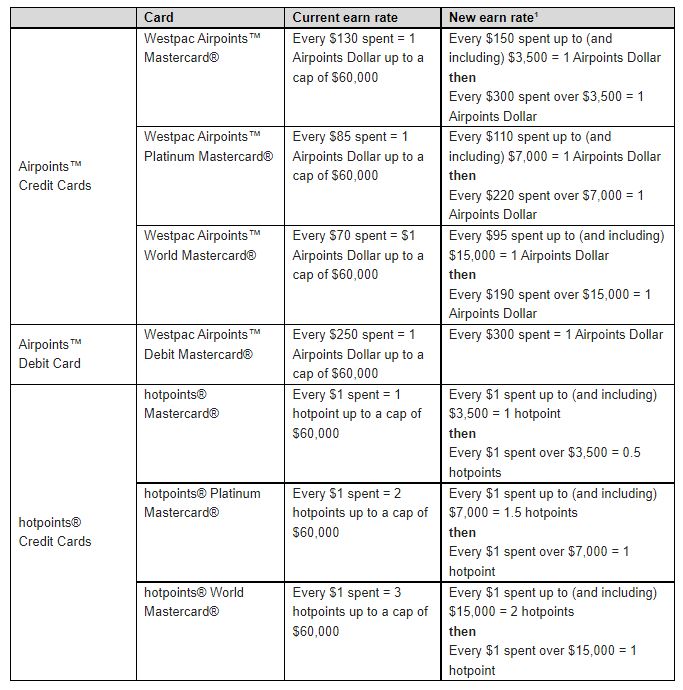

"As an example, a customer with a Westpac Airpoints Mastercard currently earns 1 Airpoints Dollar for every $130 spent on eligible purchases up to a cap of $60,000. Under the revised programme, they will earn 1 Airpoints Dollar for every $150 spent for the first $3500 of eligible purchases in a month," Westpac NZ says.

"For any eligible spending over $3500, they will earn 1 Airpoints Dollar for every $300 spent."

Westpac NZ Chief Product Officer Kerry Conway says the bank has tested the new tiered system "successfully with our customers."

Conway says although income for the bank from interchange fees has decreased, it isn't passing on the full cost to its cardholders through changes to its reward schemes.

“Instead, most of the cost of this change is being absorbed by Westpac,” Conway says.

See changes made to their rewards and loyalty schemes by other banks here.

Regulation aims to help SMEs

Changes to banks' credit card rewards schemes come with the Retail Payment System Act (the Act) having taken effect in November. This means the Commerce Commission now regulates interchange, bringing NZ in line with comparable countries such as Australia, which have regulated interchange for years.

The Act follows a 2020 election campaign promise by the Labour Party, which said if returned to government it would regulate merchant service fees charged to retailers and other small businesses by their banks. For small and medium sized businesses (SMEs) card acceptance fees can be the third highest cost of doing business after wages and rent. As well as saving SMEs money, the idea is that reducing these fees should also ultimately flow through to consumers.

Commerce and Consumer Affairs Minister David Clark has said government estimates put savings for merchants at about $74 million per annum within the first year of the Act taking effect. If these savings are passed on by merchants to consumers, this will reduce "the regressive wealth transfer" between users of lower-cost payment methods and high-cost payment methods.

Interchange is the biggest part of a broader merchant service fee charged by card issuing banks to their business customers. According to a government regulatory impact statement, interchange can be 70% to 80% of the merchant service fee. However, each bank sets its own interchange rates within a cap set by Visa and Mastercard, whose cards the banks issue.

Interchange fees for credit card transactions have been capped at 0.8% of the transaction value, and interchange fees charged for online debit card transactions are now capped at 0.6%. This is in line with Australia. Retail lobby group Retail NZ had said small retail businesses could pay fees of more than 2% for credit transactions. Additionally many retailers were on blended rates of more than 1.6% for all transactions including contactless debit.

Contactless debit card interchange fees will stay at their current levels of 0.2% or less, and swiped and inserted debit transactions such as EFTPOS, will remain fees free for merchants.

'Regressive cross-subsidy'

In 2016 the Ministry of Business, Innovation & Employment (MBIE) estimated merchants had to increase prices to all consumers by about $187 million annually to fund rewards paid to certain credit card users.

"Because of the way credit card reward schemes are structured, this leads to an annual regressive cross-subsidy of $59 million from low income to high income households. These costs are ongoing, so they add up over many years," MBIE said.

The government regulatory impact statement set out that individual consumers being incentivised to use higher cost payment methods isn't necessarily a problem for them given they receive benefits for higher costs.

"I.E. a consumer may be willing to pay a surcharge for the use of a credit card, in return for rewards points accrued from the use of that credit card. For individual consumers, the costs can be outweighed by the benefits when rewards and the provision of credit are factored in."

However, the problem is when consumer preferences for higher cost payment methods impose higher costs on merchants, who may then choose to recoup these by increasing prices on goods and services or surcharging.

"This is a problem because it means that all consumers pay the same higher prices even when they use lower cost payment methods. This results in a wealth transfer from the users of low cost payment options to users of high cost cards, likely to be on high incomes due to issuer rules or higher annual fees," the regulatory impact statement said.

"This perpetuates the economic inefficiency of the current retail payments system because it means that users of low cost payment methods essentially fund reward schemes for users of high cost payment methods, rather than matching up the costs and benefits of those different payment types to their users. This cross-subsidisation compounds the inequities within the retail payments system." (There's more on this here).

Visa and Mastercard, meanwhile, run their NZ revenue through Singapore where they pay very low tax rates due to sweetheart tax deals.

*In 2020 I wrote a five part series on the NZ retail payments system. Part five, which ties the series together, can be found here).

Westpac NZ changes are detailed below.

15 Comments

Must be hard to make a buck in banking. Poor sods.

Not exactly reading the room

Bankers are incapable of

Bankers are incapable of . Operate in a vacuum . Live in Tawa .

Should have been regulated years ago. Failure by successive governments.

And credit to this government?

Westpac Airpoints Mastercard

Annual account fee: $70

Before: 1 Airpoints dollar per $130 spent on eligible purchases up to a cap of $60,000.

Revised: 1 Airpoints Dollar for every $150 spent for the first $3500 each month

Result:

- $60,000/year limit reduced to $42,000/year = ~28% decrease

- Monthly cap

- ~15% increase in spending to get the same benefit

- Overall opportunity to gain airpoints dollars

- Before: $461.5 per annum

- After: $280 per annum

- Total decrease in points possible: $181.5 per annum or 39%

Potential max benefit: $280 - annual fee $70 = $210

Factoring in the account fee and increases in airfares I just cannot see the point of this product personally. Any corrections in my logic feel free to let me know

Can't fault the logic here.

All you have to do is splash out an extra $210 dollars a year on your credit card (whereas the psychology of cash, or event Visa Debit/Eftpos is a bit different) and it's a waste.

It's worse than that: The $60,000 cap on airpoints dollar earnings was previously per month. So you could previously earn up to 461 airpoints dollars per month on that card (admittedly only for a massive spend).

Platinum and World may still be worth it though in order to collect the status points.

Tax free bonus for those with a work or business card.

_This was supposed to be a reply to Interesting1234's post.

Why is that ?

How can this be a reason to revise the terms? Regulators need to stop banks from passing on costs and keeping the profits.. What is the point for stupid rules when consumers n cafe customers, we pay for it either way..

I am going to switch to SBS visa, awarded by Canstar last 3 years..$1 cash back for every $150 spend. Simple deal.

Westpac toy with points and will toy with rewards next..

Ok if you pay no fees

Interestingly, the interchange fees are now lining up to Australia... but the rewards schemes don't seem to be as good over there. Other than big sign on bonus offers.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.