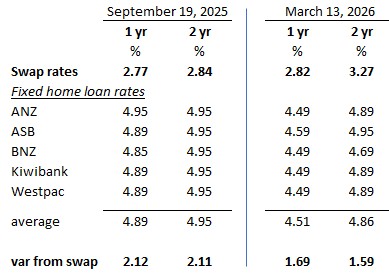

Followers of wholesale swap rates will know they have been on the rise recently.

In fact, the one year swap rate is back to mid September 2025 levels. And two year swap rates are now more than +40 basis points (bps) higher than those September 2025 levels.

So it is timely to ask now how that might affect fixed mortgage rates.

Swap rates are a good indication of the banks cost of money. But they aren't the only factor that goes into retail rate settings. However, they are an important factor and set a base from where banks assess their pricing.

But first, why does mid-September 2025 have relevance in this assessment? Well, it was the last time there were Middle East tensions large enough to disrupt international trade, and affect the global cost of money. The entrance to the Red Sea was under threat from forces in Yemen with a proxy war playing out between Iran and Saudi Arabia. And of course the Gaza tragedy was just getting started with its own explosions.

Financial markets shifted to risk-off modes and benchmark interest rates fell on the assumption that sovereign debt was safe and that equity returns were under threat.

Now of course we have another and arguably larger geopolitical crisis. But this time sovereign debt, especially US Treasuries, are no longer looking as safe under the Trump Administration mismanagement. These benchmark rates are now rising, and risk premiums are flowing outward. In fact, there are also liquidity issues now. Fewer international investors are prepared to come to the New Zealand swap market transactions. A shortfall like that inevitably drives up interest rates.

After the moves this week, bank margins have been compressed. Whatever you may think about their levels, they are now -40 bps to -50 bps lower than our reference period. Bank treasurers will be feeling the compression.

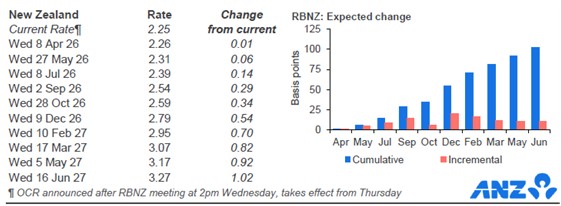

If these pressures play out as they usually do, we could see +50 bps rises in one and two year carded fixed home loan rates, and fairly soon. And they will come even though financial markets are not pricing in any Official Cash Rate (OCR) rate hikes until at least July, and probably September 2026. Certainly none at the April 9 or May 27 OCR reviews.

Daily swap rates

Select chart tabs

Then there is the question: Will savers get the same boost if home loan rates do in fact rise?

67 Comments

At this trajectory, 7 or 8% mortgages are possible fairly soon, in a more inflationery world.

Those acustomed to cheap debt, believing it to be the norm, will be seen as the village idiots, soon.

PDK - respectfully, as this is your mastermind topic. Given the resource wars are now amping up for us all, over the last, hard to get bits, where will prevailing inflation land, in your opinion?

"will be seen as the village idiots, soon" - so will people who are currently employed that will be unemployed, or people with a business who will have it destroyed.

Not sure why some on here get excited about the RBNZ having to stall the NZ economy, its in a bad enough way as it is.

Very simply JJ, inflation is exploding right now.

Like it or not, the RBNZ has one spanner to fix this.

7% or 8% mortgages should be no problem, if banks were responsible.

Unless you have a speculative bag of assets, you need to dump on a dumber debt junkie/buyer??

You're right if it keeps going this way they will need to raise OCR. I am more wondering why that makes you happy?

Those village idiots have one entity to blame - the RBNZ that told them to load up on cheap debt (OCR at 0.25%) as it was going to be around for a long time.

Whether the OCR is raised or not will depend on what's going on in the real economy. If unemployment begins a sharp rise, the RB isn't going to add insult to injury by increasing borrowing costs.

If that was the case, they would have raised rates during Covid, not cut them.

They aren't meant to give a toss about unemployment. They will have to raise if inflation is going to increase above 3%.

Officially they don't have to take responsibility for employment but they ultimately do. The RBNZ mandate is not an exercise in absolutism like many on this forum think it is.

Please look up the meaning of MANDATE.

-No not two blokes going out for beer.

Agree, but they would only do that if inflation is somewhere near target (or they can claim it will be soon). If inflation is obviously heading up towards 4% they will raise OCR.

I don't recall being "told" in fact I recall Mr Orr cautioning to the opposite.

REA and bank messaging had more appeal apparently

Fixing for 4.49% for 1 yeae could soon be free money.

More inflation = more house price inflation. Just when we were beginning to see prices coming down.....

In today's bubble, higher debt servicing costs will dive price only one way and it's not up. Look at the last 24 months. Job losses everywhere and further inflation will accelerate that as well.

Banks swaps rising reflect lack of trust in the speculative financial gambling that been happening. Private credit is today's headline, next is bank and pension fund failures. Note most of this is happening offshore, we are just collateral damage.

Note most of this is happening offshore, we are just collateral damage.

Be careful. Aotearoa has a false sense of security in the idea that all our problems are caused externally. This narrative needs to be buried.

Agreed. Just more a comment that we dont create any waves any in global finance but their bad behavior your will wash up here big time.

Nice try.... H:)

You run property, propeller, staircase, onewoof, seminars???

H - it has in fact worked the exact opposite, in the high inflation world, since 2021.

House values have plummeted in both nominal terms - in REAL terms they have super plummeted!

Nz Housing, has been the worst inflation hedge ever!

Wrong way around there Hamish IMO: Higher inflation --> less disposable income from increase cost of goods and services --> lower ability to pay for rents --> more mobile population due to high rental availability --> lower rents --> lower yeilds --> higher housing supply for sale --> lower prices.

Remember the reasons prices spikes 2020-2022 was not due to inflation, it was due to RBNZ removing LVR limits, the FLP promoting banks to lend as fast as they could, lockdowns causing people to return to NZ to live increasing demand, govt giving out free money so consumerism was on the up.

Wondering what your logic is for a causal relationship between inflation and house prices?

He has just proven, to not have a clue. But very well "property seminared".....

Please don't use insulting language. You're attacking my credibility rather than engaging with what I'm actually saying.

A question for you. If the story was about mortgage rates falling, would you think that this would lead to house prices rising?

If the answer is yes then I would suggest some introspection - if all logical roads are leading to houses becoming more expensive, then perhaps there is a flaw in your thinking.

For me the logic is pretty clear - higher interest rates, lower house prices. Lower interest rates, higher house prices. All other things being equal, of course. You may be extending your logical time horizon until it aligns with your priors.

Thanks for your question mfd. You make a good point. To answer your question, yes, when interest rates drop, property becomes more affordable and can result in higher prices. Yes, when interest rates go up, the ability to service the mortgage on a house is reduced which has a dampening effect on prices. However, I'm simply offering some balance to the prevailing views here that a 50 or 100 basis-point rise in the OCR (by no means a given) is somehow going to tank house prices. I guess what I'm saying is that when high inflation comes in to play, it's best to invest your money in something that atleast keeps up with rising prices, and property has historically been a good place to park your money - even during periods of extreme oil-crisis-induced inflation.

I certainly wouldn't think a 0.5% rise in rates is going to make much of a difference one way or another, a small downward force at the margins.

My general thinking is predicting the future is hard and diversification is best - in the most recent bout of inflation stocks performed much better than property and anyone who was all-in on NZ property has done very poorly in the context. I own my home already so I have plenty of skin in that game, so my surplus gets invested in other assets and countries. I think a FHB buying a house to live in around now makes a lot of sense, but buying further properties in NZ as a pure investment to me is questionable.

Yes, I 100% agree that diversification is really important. In addition to my own home and an investment property, I too am investing elsewhere.

Purely because of what inflation does to the cost of building a house. That has flow-on effects to the value of all houses. In 2017, we built our house for around half a mil. Now the same sized house would cost closer to $900k to build. Inflation.

According to the (admittedly flawed) General CPI inflation calculator on the RBNZ website, 500k in Q12017 would be $663,500.00 today. Notwithstanding supply issues and demand from locked down people doing Reno's in COVID times had a significant factor in this, as well as price gouging so I myself can't pin that sort of increase on inflation alone. Even with higher wages that might not explain 900k with profit margin included.

Build cost only impacts new properties, and most don't build a brand new house as a rental unless you consider the current trend of buy, subdivide and build townhouses which may buck that trend, however many of these were to buy, subdivide, build and sell, and we can already see the impact of a glut of townhouses and what it is doing to the housing market. Primarily selling below cost.

If inflation increases house build cost, this doesn't take into account rental availability and yield for already build homes pre-2020 which are the majority of the market.

Building costs haven't tracked general CPI inflation. They have been way higher.

Yes. People still cannot afford housing either way. If anything this will just suppress land values to feed affordability. Otherwise the construction se tor is in for ongoing very tough time.

Construction will be in for a tough time going forward if rates jump back over 6% again. This will lead to another shortage of housing which will in turn force up prices.

Yes a shortage, after this current record glut and empty (zombie homes) clears..... so a shortage after 2030 perhaps??

This just adds more cost to building houses which in turn decreases house building which will lead to a shortage of housing, which will lead to even higher house prices. Stagflation = a weaker NZ dollar = higher prices and more inflation. A longer course of meds (higher OCR) is required to get inflation under control.

Very simple outcome here: much, much lower land prices.

Solved.

Even if I gave you a piece of land for free, ending up with a legal, finished house on it is still very expensive.

Exactly.

Exactly, at $1000/m2 of bare land in Hamilton's northern suburbs there's plenty (and more) room for adjustment.

So the article mentions swap rates up 30–40bps but then says bank margins are 40–50bps lower. So I guess they pretty much cancel each other out, therefore the “mortgage rates about to jump” seems bit of a stretch really

That doesn't make any sense.

It says swap rates are up 30–40bps but bank margins are 40–50bps lower than last september. So if both of those are true the net funding pressure doesnt look that dramatic, so “rates about to jump” seems a bit of a stretch

What do you think banks are going to do to restore their margins?

Have a read of this page on how banks have to manage their interest rate risk:

https://www.rbnz.govt.nz/hub/publications/financial-stability-report/20…

"Banks use strategies such as matching the repricing maturities of assets and liabilities to mitigate interest rate risk. For example, one-year fixed rate mortgages could be matched with one-year fixed rate funding (for example, term deposits), so that the impact of rising interest rates is offset. They could also use derivative products such as interest rate swaps, futures and forward contracts to hedge any remaining repricing mismatch in their exposures. These strategies can help banks manage the impacts of interest rate changes on their balance sheets. In New Zealand, both of these strategies are commonly used to control risk.

After the 2008 Global Financial Crisis, additional requirements were implemented in the New Zealand financial system to enhance resilience by strengthening capital and liquidity requirements. We expanded prudential requirements to address capital and liquidity risk by requiring banks to have robust frameworks for managing interest rate risk. New Zealand banks are required to hold sufficient capital to cover potential losses arising from interest rate risk, which provides banks with an incentive to manage related prudential risks carefully. They are also required to value their liquid assets at market price instead of book value."

Summary - they can't just hold rates low because you want them to - they are mandated to raise rates so that the interest on the mortgages they are issuing match the rates they hold on wholesale swaps (ie the equivalent duration and interest rate asset and liability - and matched across the whole portfolio). So when wholesale rates go up, and a new mortgage is issued or re-fixed, the rate has to go up if the wholesale rates are up. They can't just hold them lower because they want to be nice to Welly-FHB. They risk going bankrupt if they do.

Yeh sure banks hedge interest rate risk and thats what the rbnz page is describing. But that doesnt mean retail mortgage rates automatcally move 1 to 1 with swaps. Margins can compress for periods depending on competition and some sort of funding mix. My point was simply that the article itself notes margins are already 40–50bps lower, so the “rates about to jump” framing seems a bit strong.

Or your desperation for rates not to go up is a bit strong.

Either way, banks will do what they need to do.

Just discussing the article, not hoping for any particular outcome

They don't cancel each other out. Swap rates are higher, which means bank costs are higher, which means their margins are squeezed by a similar amount.

The way this is typically resolved is by banks increasing their rates to restore margins.

Yeh fair point, they may or may not lift rates to restore margins. I was just noting the article itself says margins are already 40–50bps lower, which makes the “rates about to jump” line seem a bit over the top

They have no choice - they have to hedge their interest rate risk. Its mandated by the RBNZ.

They have to manage interest rate risk for sure, but thats not the same as mortgage rates having to move every time swaps move

Well that is how the banking system works - so you can accept it or deny reality.

Im sure if wholesale rates were dropping and the banks didn’t drop mortgage rates to match the falls you’d be saying ‘this isn’t fair!!’ But now they are going up you are saying ‘they don’t need to raise mortgage rates’ Can’t have it both ways.

That aint what I said. I didnt say banks wont raise rates, simply that the article itself says margins are already 40–50bps lower, so the “rates about to jump” framing seems strong. And the bit about me complaining if rates were falling is a position you've made up

So you're thinking that the fact that the banks are currently accepting lower margins means they may continue to accept lower margins?

I wish I shared your optimism.

That misrepresents what I was saying. I didnt say banks will keep accepting lower margins just that the article itself mentions margins are already 40–50bps lower, so as I’ve been saying the “rates about to jump” line seems a bit strong.

Ok, then I don't understand your logic. The logic of the article I think is that margins have a fairly consistent level, they are currently below that level, and therefore you should expect them to spring back to the normal level.

Which bit do you disagree with? I thought it was the last bit but apparently not.

Well the article assumes margins must revert quickly via mortgage rate rises. I’m saying that outcome aint guaranteed or immediate, hence my view that the rates about to jump angle seems a bit much.

Because you think swap rates could fall again first, or because you think the banks will accept a step change down in profitability for no obvious reason?

On the former, do you think there is also a similar risk of swap rates rising even further?

Neither necessarily. My point was simply that the article assumes the adjustment happens quickly via higher mortgage rates. That may happen but it aint guaranteed to be immediate. We know banks compete for lending, swap rates move around, and margins can compress for periods, so the timing isnt certain

Wellingtank, Fact: Banks ARE UNDER PRESSURE TO RIASE RATES. It is going to happen soon.

If this stresses you: Deleverage. Diversify. You can then relax and un-sphincter-clench.

Happy days.

I question some thoughts and reality, only as some erroneously think : "high inflation = high house inflation"

When all history shows - the exact opposite scenarios to be True, as from 2021 to 2026.

- High inflation and Tanking house prices.

Some are now back at 2018 and 2019 pricing.

Both most recently and to now and the last major oil shocks, as in the 1970s.

Rampant inflation in all products, including building products!

- The 1970s, saw - 40% REAL losses in NZ property.

To heap this 1970s scenario, on top of the most recent Nominal and Real -30% losses, would be a shocker and a Real proposition that home hoarders, Landlorders, are well advised to consider.

Well that 1970s 40% real loss argument is pretty misleading. House prices still rose strongly in nominal terms, they just didnt keep up with very high inflation. For the homeowners with fixed mortgages inflation actually reduced the real value of their debt

100% not misleading.

REAL returns is all that counts, inless we are in the mindset of 5 years olds.

When your DEFLATED DOLLAR, buys you stuff all, at the end of a high inflationery environment, and your house price gains have "not even matched CPI" inflation, having your money tied up in housing is the worst, net negstive investment.

Having a house and stabilty has its own positives, yet net negative from an investment view.

Its akin to burning 40% of your 1970 dollars in 1980, if you punted it all on housing.

Many have not learned from history and made the same clusterfudge all in bets, since 2021, many have lost it all......in the event of negative equity sales!

Right wheres my coffee...

Yep real returns matter but housing is typcially leveraged. In high inflation times the real value of your mortgage dropss as well, which is why many owners in the 70s still benefited despite the “real loss” charts

Your argument treats housing like a cash investment, but almost nobody buys houses with cash as most have mortgages, and that changes the maths a lot because the debt is effectively being inflated away. Many people who bought in the 70s ended up very well off later on.

Also, your claim that “many have lost it all” simply doesnt match nz housing history. Thats extremely rare. Even during downturns the percentage of mortgages in serious trouble has usually been well under 1–2%. Even after the GFC mortgage trouble only got to about 1–1.5% of loans, meaning roughly 98–99% of borrowers kept their homes... So your doom narrative doesnt fit the data.

Real returns, matter above all in investing.

If your not beating the destruction in purchasing power (cpi) you are in a mugs game.

I've seen many property people (oneroofers) say housing is the 'best inflation hedge" it was and made gains atop of inflation from the 1980s to 2021.

Since then, it's been a mugs game, many are entrenched in the 40-year bull run story, that exhausted itself as values become a super bubble.

This bubble still has a lot of air to let go and will we see a 20-year crash, as Japan did?

Our short, 4-year NZ property crash, has been among the steepest declines in the world, this sucker is still going south!

I recommend you research the 1970s oil crisis and housing prices. You'll find that they did indeed hold their REAL value. In nominal terms, they sky-rocketed while debt on the house was being quickly inflated away over the following decades. That's the beauty of investing in property. Those with plenty of debt (on solid assets such as housing/land etc) are big winners during times of high inflation.

What lala land REAL prices have you been reading/smoking?

The peak of the 1970s crashed in 1980 and were at the better part of -40% down from the top.

Real Residential Property Prices for New Zealand (QNZR628BIS) | FRED | St. Louis Fed

Well heres the flaw in your argument: you keep treating housing like a cash only asset. In the real world most houses are leveraged, so during high inflation the real value of the debt is also being eroded away. A “-40% real price chart” is not the same thing as saying homeowners were wiped out.

Also, if housing was such a wealth destroyer through that period you would expect widespread mortgage wipeouts and forced selling. That really wasnt the nz experience.

Yep sure. Keep loading up......like its 2020......

Thanks for the chart. The Real price Q1 1970 was the same (slightly lower actually) as the Q1 1980 number - which exactly illustrates my point.

Yes for those "lucky enough" to buy on and sell on that 10 year horizon, they made ZERO on property.

If the purchased in the mid seventies peak, then sold in 1980, they lost a REAL -40%.

Winning asset class for sure........gamble more on property!

Yeh but buying at the exact peak and selling at the bottom would produce losses in almost any asset class. Thats more about timing than housing itself

Likewise, economic history is littered with looooong periods, where the sale price, is well below the cost of actual production.

Howling at the moon or Interest peeps and saying: "This house cost me this" "I must sell for this/that/other or 40% more" - won't make it so.

Markets have their own ideas and the investment world changed in the NZ Housing Ponzi, after 2021......

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.