The recent move by the Reserve Bank (RBNZ) to increase the Official Cash Rate (OCR) by 25 basis points will likely only have a relatively moderate impact on mortgage borrowers.

That's because the increase in the OCR pushed up floating interest rates but not fixed rates, and relatively few mortgages are on floating rates.

According to the Reserve Bank, the total value of all residential mortgages was $399.9 billion at the end of May, but just $40.7 billion (10.2%) of that was floating rate mortgages; the remaining $359.2 billion (89.8%) was all fixed rate mortgages.

Following the increase in the OCR, the major banks all moved to increase their floating rates and they passed on the full 25 basis points.

Changes to floating rates usually take effect fairly quickly once they are announced, so customers with floating mortgages should notice the increase in their mortgage payments over the next few weeks.

At face value, the increase for most borrowers will not be huge.

An extra 0.25% on the mortgage rate would add about an additional $250 a year ($4.80 a week) in interest payments per $100,000 borrowed, or about $24 a week on a $500,000 mortgage.

The bigger impact is likely to be on how borrowers structure their mortgages and in their level of caution in taking on debt.

While just 10.2% of total residential mortgage debt is in floating mortgages, they are more common with newly established mortgages.

According to the RBNZ, $8.475 billion of new residential mortgages were issued in May this year and of that, $1.541 billion (18.2%) were floating mortgages, with the remaining $6.934 billion (81.8%) on fixed rates.

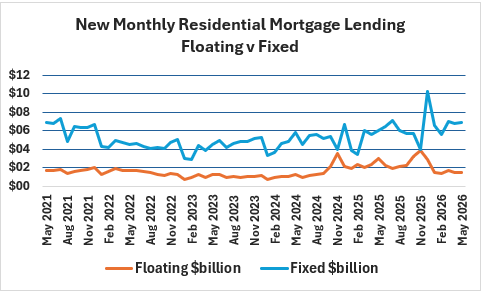

Looking back over the last five years, the percentage of monthly new mortgage lending that was on a floating rate peaked at 49.4% in November 2025, and has been in a more or less steady decline ever since. This trend can clearly be seen in the graph below.

Between November 2023 and November 2025, the average two-year fixed rate charged by the major banks declined from 7.04% to 4.49%, so many borrowers stayed on a floating rate in the expectation that rates would continue to fall and they could switch to an even lower fixed rate a few months down the track.

But since late last year year mortgage rates have been rising, with the two-year fixed rate increasing from 4.49% in November last year to 5.26% in June this year, and the common expectation is that they will rise further over the rest of this year and possibly into next year.

So the incentive to maintain a floating rate mortgage in the expectation of switching to a lower fixed rate at a later date has already disappeared.

Hence the decline in the popularity of floating mortgages with new borrowers.

Possibly the biggest impact of the latest increase in the OCR is that it will have reinforced the idea that we are in a rising interest rate cycle in the minds of borrowers, which will make them more cautious in taking on debt.

That in turn will likely increase the already prevalent levels of caution in regard to house prices.

So there's caution on top of caution in the current market.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.