You can't look at a current swap rate chart without wondering what is going to happen next to fixed home loan rates.

The last time they were at this level, in April 2025, the one year fixed home loan rate was 4.99% at all the major banks and most of the challenger banks as well.

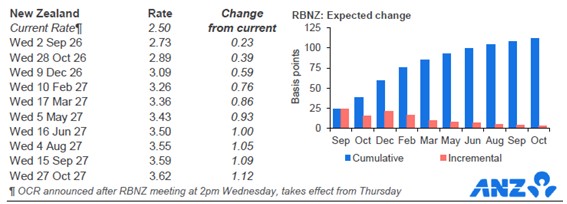

At its July 2026 review, the RBNZ upped its OCR by +25 bps. After the signals they gave with that change, financial markets have since priced in two full +25 bps hikes for the rest of 2026 (even knowing there will be restraint over the election campaign period) and have a one-chance-in-three of a third increase priced in as well. There are only three more OCR reviews left for 2026.

Obviously, moving these background wholesale rates up is 'risk', principally of higher global inflation ahead and the expected global monetary responses to check its rise. Geopolitical uncertainty is a key driver of the higher inflation risk.

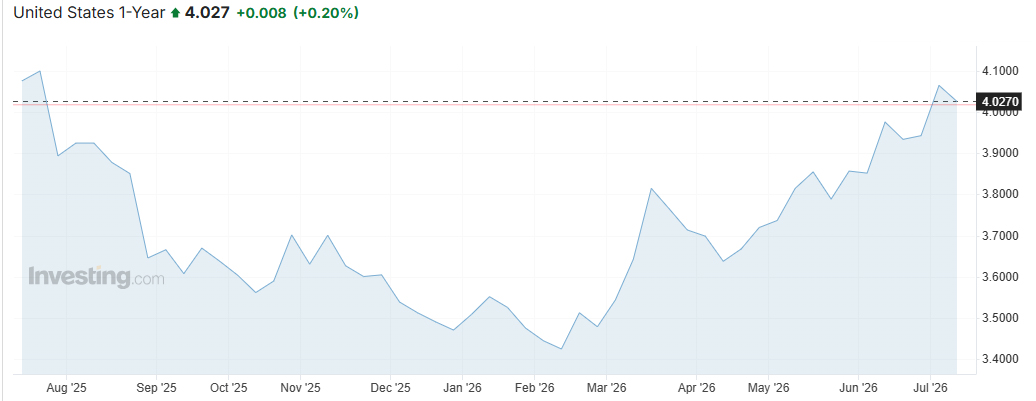

You can also see this clearly in shorter term bond yields. Investors want higher returns for the risks ahead, and the equivalent benchmark US Treasury yield has been moving up for all of 2026 so far. Ugly US budget management doesn't help.

Today, the one year fixed home loan rate is between 4.65% (ANZ, ASB) and 4.79% (BNZ, Kiwibank and Westpac). The wholesale pressures on banks are for at least a +25 bps rise soon to these 1 year fixed rates, possibly +35 bps for some. For a two year fixed rate, the pressure is only slightly less.

Obviously we have no idea what or when banks will move next. But the pressure points seem obvious now.

For savers, who currently are offered 3.45% / 3.60% / 3.90% for six, nine and twelve month term deposits, they will be hoping for increases too. But if banks maintain their recent form it seems unlikely they will get the full equivalent increased offers. The best way to pressure them for a full improvement is to shop around. If enough savers do that, the banks will get the message. For many savers, the Depositor Compensation Scheme makes changing banks largely risk-free when chasing a better rate. Borrowers have built the habit of switching for a better deal. Unless savers build the same habit, banks will likely short-change them as they rely on long-standing replication habits.

If you are a borrower with a fixed rate, you need to ask yourself whether it is worth waiting for 'spring' and the anticipated competition that often arrives in the more elevated real estate selling season. Is that likely to happen again in 2026?

Fixed mortgage rates

Select chart tabs

Daily swap rates

Select chart tabs

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.