By Elizabeth Kerr

I’m quite a simple girl at heart, in that I like to understand what I am investing in and I like to have reasonable control over the process. That is why I personally tend to boost our Money Machine with investments that I can administer myself.

Recently someone emailed in asking about Harmoney - peer to peer lending, or P2P for the cool kids.

This is a relatively new concept here in NZ but has been operating overseas for a number of years. The two most popular ones are called Lending Club in the US and Zopa in the UK.

In little ol’ NZ, Harmoney is our first licensed P2P lending platform.

On the face of it, P2P is a bit like an online dating service. Essentially Harmoney, as the online platform operator, introduces people wanting to lend money to people wanting to borrow money. As an investor, my money doesn't go to Harmoney itself. It's held in trust and is lent to borrowers in exchange for an interest rate return. This interest rate return can vary between 9% and 24% per annum, which is much better than what I could receive if I squirrelled this money in the bank, and to some extent the stock market.

On the other side of the Harmoney coin, people may borrow this money at a lesser interest rate than they could at the bank or local loan shark, so it appears that it’s a win-win relationship for all of Harmoney’s customers.

Now I admit that when I first learned of P2P lending my imagination had my hard earned dollars being poured into the local pokies via someone who saw P2P as the last stop on the line for their gambling habit. I figured if the bank wasn’t going to give them money then I sure as hell wasn’t either. (Admit it, you thought this as well didn’t you?!).

However, it’s not like that at all. Borrowers are required to fill out loan applications just like at a bank and, if approved, they are then categorised according to their risk of defaulting on their payments. Those marked 'high risk' seem to be charged higher interest rates then those who are deemed a lower risk. In return those who choose to lend their money to high risk borrowers are rewarded with higher interest rates of return. Seems fair to me.

Harmoney and your Money Machine

If you put your money in a bank you might get an interest rate return of maybe 3%, if you invest in a term deposit you might get slightly more – say 4.6%. But if you invest in P2P you could expect anything between 10-24%. So, it’s a good way of getting your machine to work harder for you.

Be warned though. Just because it is the first P2P lender in NZ licensed by the Financial Markets Authority (FMA) does not mean your investments are insured. Should Harmoney go up in a financial ball of flames you are not protected by any government or insurance compensation schemes. However, Harmoney points out the (FMA requires it to have continuity contingency in place so if Harmoney ceases to operate, loans continue to be administered, payments to investors are still made, and collections pursued.

The low cost P2P business model, which doesn't have the branches or capital requirements of a bank, helps make the higher interest returns possible. In terms of the risks of investing via P2P platforms, FMA director of compliance Elaine Campbell, suggests it's for those who could absorb the loss of both their principal and interest should things turn pear shaped, although this certainly isn't to say that's necessarily what is going to happen. Rather, understanding what you're getting into - like any investment - is key.

Still not sure if it’s for you?...Well let’s put it to the test to see exactly what kind of returns it does cough up.

The minimum amount one can invest in Harmoney is $500, but I’m going to throw in two lots of $2500.

The process begins…

Okay, so first up read the terms and conditions…who does that these days? But they are actually quite easy to read and understand, so don’t skip this step.

Basically, failing smashing the borrower over the head with a big stick, Harmoney will do its best to get my money back. All borrowers go through a credit assessment before their loan is put on Harmoney's marketplace.This includes credit bureau checks, affordability calculations and fraud detection. Thus far, Harmoney says, it has rejected 68% of borrower applications.

Sometimes I can be as useless as an umbrella in Wellington when it comes to IT challenges - thus the hardest part of the entire registration process was getting my laptop's camera to work to take photos of my drivers licence for verification. This is a mandatory part of the process and you can’t escape it. You have been warned.

Once you’re set up you need to transfer money into your Harmoney account to begin distributing it to borrowers. Waiting for your money to clear is a bit of a let-down if you’re eager to get started, but in the meantime you can think about whether you’d like to be a self-directed investor - by choosing your own loans to invest in - or just use the ‘quick invest’ option, which gets Harmoney’s software to choose your investments for you.

The great thing about the self-directed option is that you might be able see what the borrower wants the loan for.

It’s actually quite fascinating. There are the usual debt consolidation and car finance loans, as well as one dude who wants to take his son on a once in a lifetime trip overseas, and another guy wanting to instal water tanks to complete his eco-house. There are only 34 loans that I can choose from today and it’s recommended that no one fund more than 10% of any loan.

The downside of this self-directed option is that it can be hard not to get all judgeypants - as it goes against my grain to see people borrowing money for consumer items. So, I’m quietly yelling at my laptop: “You want how much for a second hand car?…Are you mad?…Is it encrusted with diamonds?"!!!

But that is taking it too far. At this point in the game I’m looking at nothing but risk and return and I shall keep my judgeypants to just between us. (Although I feel a column dedicated to the users of Harmoney coming up…)

Fractionalisation is the key to why P2P works

Before you begin investing, your money is exchanged into “notes”, which are in $25 lots. So, two lots of $2500 gives me 200 “notes” with which to invest. I’ll try to invest 100 notes using the “quick invest” option and 100 “self-directed”.

Remember that every borrower is given a risk rating that tells us the likelihood of them defaulting on repayments.

Imagine someone is given a 5% chance of defaulting and a 95% chance of paying back their loan. If you fund their entire loan of say $2000 or “80 notes” then you have a 95% chance of getting your principal plus interest back, but also a 5% chance of losing the lot.

However, if you fractionalise, or spread your investment notes across a range of borrowers – say 80 loans - then you could imagine that 76 people would pay back their principal and interest and just four would be lost. With this approach you would be quite happy with your return.

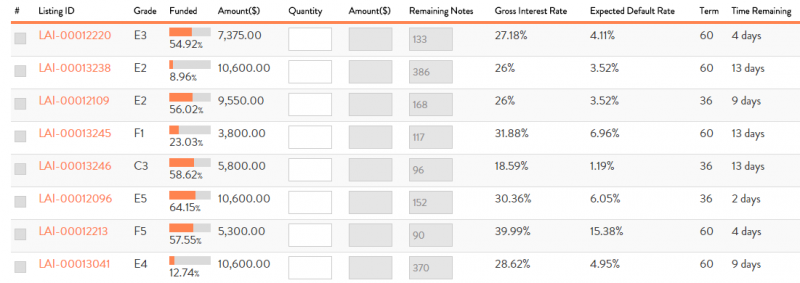

When you are set up you will be greeted with a breakdown of all the loans available to invest in, similar to this below:

As you can see the loans with the highest return interest rate seem to have the highest expected default rate as well, so, I think I’ll take my time with self-directed investing as there is no pressure to use the money in my account all at once.

Where is the catch?

Most investments have a fee and there is no reason why Harmoney should be exempt. They take a 1.25% fee from the principal and interest repayments to the investor on every note, regardless of the interest rate you have invested at. Keep this in mind! Essentially a low risk 9.99% is actually only 8.74%. Still, it's nothing to sneeze at now, is it?

I have to admit that the advertised interest rates on Harmoney’s website were a little vague in that it is not specified over what term the interest rates are for i.e. per annum or over the entire 3 or 5 year term of the loan. (The website has now been updated to make it clear the rates are per annum). A 20 minute wait on hold while the customer service rep went to clarify it as per annum seemed a bit odd to me.

The other catch is that once you have invested your notes you can’t get your money back out in full again until (if) the loans are paid back, therefore, it’s best not to invest money you might need in a hurry. Each month investors receive repayment that includes interest and a portion of their principal. By the last month of a loan term, all principal will be repaid on a performing loan.

So, here goes everyone…I’ll load up my dashboard with 100 notes on the nose each way and let you all know what horse comes in to make my money machine a winner/loser over the coming months.

35 Comments

Other Interesting things.

What happens if a borrower pays back the loan immediately

- are you charged the 1.25 percent per note - yet you receive no interest ?

Also bear in mind the default rate is per year so a let say 3% per year ie not 3 out of 100 loans but roughly 9 over a duration of 3 years. Now those nine are most likly going to happen in the first few months of a loan originating - as the longer you get into a loan the more safer in theory it becomes (danger zone being 3-4 month payments). There is a chart buried deep in the site that explains this. So at the moment i think its a diversification game - ie the more notes - the more diversfield you are to loan defaults (yet more likly to experience them). In order to achive that diversification your looking at 400 notes * $25 (various forums around the internet)

So for example 1000 * 25 gives you a much greater return than 10 * 25 notes - once you take into account a 10% default rate - when the defaults are loaded to the front of the loan duration.

the curve chart is located on this page at harmony site

https://www.harmoney.com/investors/loan-performance

yes the width of the diversification pretty much guarantees some losses...

What happens if a borrower pays back the loan immediately? This:

$24.69 05 Nov 2014 Paid OffSo I invested $25 and got $24.69 back.

LOL, welcome to NIRP beyond junk.

According to Harmoney csr, If the borrower pays back early then the principle is returned back to the investors account and there is no fee deducted from it.

Some borrowers will repay their loans ahead of schedule. In this case, the funds are returned to the investor’s account and will be available for re-investment or withdrawal.

---

That will be funds less fees.

Who would borrow at 39%pa? (bridging??) with the short return penalties in P2P investment it seems desparate to say least.

yes and some of the p2pl borrowers already have mortgage loans collateralised against their family home. Is that reasonable?

I don't disagree with you. There is defiantly a column brewing about this very thing. Some people honestly just do not understand how interest works and then there are others who just don't care and will pay anything to get what they want.

Whilst I don't think P2P lending seeks to exploit this, I do have some issue with there not being a person to eyeball the borrower and question their sanity or look over their business plans etc....

If someone is considering getting a personal loan, they are welcome to step up and email me first for said "eyeballing". Elizabeth.kerr@interest.co.nz.

glad you checked on that per annum issue.

That used to be the catch the "loan until payday" groups used to use with 9-19% loans... for a fortnight (at 9-19% per fortnight !)

It was you? good to put a face to a name, so to speak. Yes we got there eventually..... And as you can see my husband has 'written off' $5000 (his words, not mine lol).

holy cow, 9~19% PER fortnight?

52/2=26x12% (say) = OMG.

You should spend sometime helping out your local budgeting service to see how bad it is out there. The usual loan sharks are charging just as much plus admin fee!

Good luck Elizabeth. I think you're mad - but good luck.

I don't know who HARMONEY lend to but in December i got a note from them saying i haved been preapproved for a loan up to 20k.

Somehow i don't think they know that i am unemployed/able.

Did you apply to see how far through the application process your so called "pre approval" took you? *just wondering*

I got halfway through before they wanted 3 months of bank statements by which time I lost interest. Interestingly they wouldn't let me continue unless I declared some debt. After the very first form it said "almost done" not even close LOL.

Simple answer no.

About 2 weeks later i recieved a letter from ANZ saying that i was able to increase my ccredit card limit by a good margin .

Surely they must have seen no money going into my account for the previous 4 months.

Could have had a field day.

This is funny, I thought it was an angel investor type scheme, never bothered to look. The dash for trash is on, reaching for yield. Retun free risk. I'll gladly pay you tommorow for a cheeseburger toay! I expect your real return will be worse then my serious saver at 4.2%. Unless of course there is the capacity within harmony to refinance your old loan with a new loan, somewhat like Greece. That would be the ultimate ponzi!

One day I may put money into an angel investor fund, to help someone build a business, i was lucky enough to have someone help me. Bad debt for consumption fugetaboutit!

If you took the self-directed option you can choose to only invest in businesses. It's not personal but i really really hope i can prove you wrong :)

I would be happy to be proven wrong, hopefully we are all around in 3-5 years to congratulate you. There are some listed loan shark companies on the NZX, which the last time I checked were getting an IRR of about 15%. That had to have been about 4 years ago though.

I may look at the options, for 30% I could even put it on my credit card. Joking. It would have to pass the wife acceptance factor (WAF) she may even accept.

I can understand that for New Zealand this is a new thing and a cause of concern,personally i thought the fees and charges to borrowers were somewhat high,as it is in the lenders interest for the borrower not to fail.

But as said this is old hat in some parts of the world,would i think because a bank wouldn't lend ,i would be concerned,no i wouldn't use banks for fiscal guidnance when they have not so long ago sent the world into economic decline though wreckless lending and in many cases criminal activity.

Many global banks have arms that deal with second finance house loans at higher borrowing rates ,one of my own loans many years ago reached 22% from a major high street bank.

An interesting one in the UK is Dave's Bank which i believe now does have quarantee,i would imagine the doco made about his bank ,as a sucessful businessman he was so p ' d off with banks not funding viable business ventures that he started his own bank .

That aside New Zealand is still somewhat like the wild west and does not have the safety nets more advanced nations have .

I can understand that for New Zealand this is a new thing and a cause of concern,personally i thought the fees and charges to borrowers were somewhat high,as it is in the lenders interest for the borrower not to fail.

But as said this is old hat in some parts of the world,would i think because a bank wouldn't lend ,i would be concerned,no i wouldn't use banks for fiscal guidnance when they have not so long ago sent the world into economic decline though wreckless lending and in many cases criminal activity.

Many global banks have arms that deal with second finance house loans at higher borrowing rates ,one of my own loans many years ago reached 22% from a major high street bank.

An interesting one in the UK is Dave's Bank which i believe now does have quarantee,i would imagine the doco made about his bank ,as a sucessful businessman he was so p ' d off with banks not funding viable business ventures that he started his own bank .

That aside New Zealand is still somewhat like the wild west and does not have the safety nets more advanced nations have .

FYI, we have updated this article to make some corrections and clarifications. Look out for more from Elizabeth on P2P & Harmoney as she gets her teeth into this new addition to New Zealanders' investing and borrowing options.

Hi Elizabeth,

I have read your articles since you started last year. I would like to email you the details of my current financial position and have your feed back along with the other expert commentators on here as to what I should do next. Similar to what you did for the couple in Auckland with two houses awhile back. Keen to here the pros and cons of my options.

How do I get you the info?

Hi Sprogg,

You can send me your details to Elizabeth.Kerr@interest.co.nz. Just be aware im not a qualified financial adviser... just opinionated <laughs>.

Regards,

Elizabeth.

PS: anyone can write to me, i promise not to publish anything without your permission first.

Thanks Elizabeth. I have just emailed you.

Hi Elizabeth

I have been following your article and comments on Harmoney and wondering how things are going with your investment. I started investing just over 3 months ago and although there have not been any defaults, I am getting concerned by the unreliability of the dashboard. Often there are no arrears shown but when I look at the individual investments arrears appear there. Also outstanding principle never seems to tally with returns on investments. Although they inform us that work is still being done on the the dashboard, I think that I will hold fire on any more investment until I have some confidence in their database. How have you been getting on?

Cheers

Richy

"They take a 1.25% fee from the principal and interest repayments to the investor on every note, regardless of the interest rate you have invested at. Keep this in mind! Essentially a low risk 9.99% is actually only 8.74%"

I think this is too simplistic a calculation especially as it ignores the fact that the fees are also charged on principal repayments. I think a better way to look at it is:

Calculations using Excels PMT() and RATE() formulas.

I have put a toe in the water with Harmoney investing $10,000. Here are my observations:

At this stage the market is relatively small and there are frequently less than 6 loans on offer although checking back a day later might well find up to 20 loans on offer. There would appear to be a lot of funds looking for a home as most loans appear to be fully funded within a day or 2. With a limited number of loans on offer at any one time it can be difficult to get sufficient diversification unless you are prepared to place your funds over a number of days. In my case funds were invested over a week across 40 or so loans. 60 would have been a better number. Of course there were loans I would not contribute to. Sorry a 20 odd year old borrowing to go to a mates 21st in Australia won't get my money even if the rate is 39%.

So far so good and all loans have met their 1st months repayment. One thing I am a little uncomfortable with is the recent facility Harmoney has offered to borrowers called "redraw". It is not actually a redraw facility but a top up facility where borrowers can increase the size of their loan. A not insignificant number of loans are currently offered as redraws. Harmoney shows the borrowers past payment history and it appears that most redraws are very soon after the original loan many having made only a few repayments or none at all. One of my loans has already been subject to a redraw. I emailed Harmoney about redraws and was advised that with redraws the funds are used to repay the original loan a a new loan is established. I have concerns over this on two fronts. Firstly maybe I'm too conservative but I feel that when you ask for a loan you should prepare your budget and ask for only what you need at the time. To come back only a month or two later asking for more is not a good look and I would have concerns as to the financial literacy of the borrower and future ability to repay. Admittedly banks and finance companies are always asking their customers to borrow more so Harmoney are not alone in this respect. My other concern is that as the original loan is repaid Harmoney then takes its 1.5% fee and will then take it again when the new loan is repaid. This of course is to the detriment of the original lender. I note that the redraw facility started about the same time as Neil Roberts resigned from the board so wonder if there was maybe some disagreement agreement over this initiative.

As I said earlier so far so good. Its too early to see how the loans perform over the medium term. I do hope that Harmoney is a success as I would very much like to substantially increase my investment but will need a much larger number of loans to be available before that is possible.

Harmoney is waste of time & money, longterm you loose

Hi Elizabeth

May I ask what is the taxation for an investor in Harmoney?

Thanks

R

Elizabeth, touching in on this thread that only seems to have messages from 2015 - can you give us an update now that we are well into 2016? Any defaults? Have you worked out an annualised rate of return on your initial investments?

Hi Elizabeth, interesting article and comments. I have just started investing with Harmoney. Would be interested in how you got on now that you have been in over a year now.

Thanks

it is a scam, trust me borrowers and harmoney gain, killing lenders.

in my case $400 taken by borrowers and harmoney out of 467 received in a year on $2000 investment

Service / Lender fees -$93.54

Withholding tax -$154.34

Charged-off principal -$147.78

harmoney doesn't take any action, they take fees upfront from borrower and then they happy if they pay take commision, other wise simply if borrower doesn't pay they Charged-off principal, lenders suffer, no lender gain in longterm

$467.69

GROSS INTEREST RECEIVED

and you show me

17.13% p.a.

YOUR RAR

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.