A four-year high in investment in gold drove price gains and demand growth in 2016, according to the World Gold Council.

But that enthusiasm waned sharply in the December quarter.

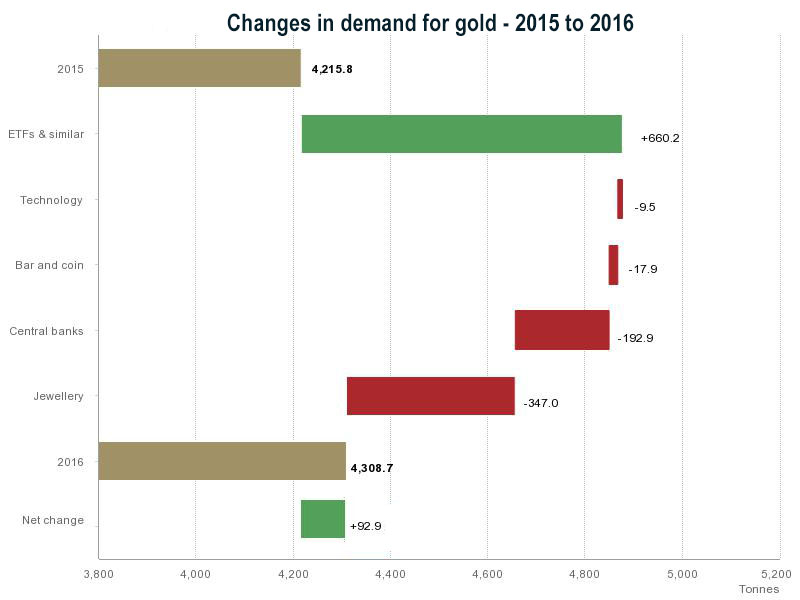

2016 full-year gold demand gained +2% to reach a 3-year high of 4,308.7 tonnes.

Annual inflows into ETFs reached 531.9 tonnes, the second highest on record. Declines in jewellery and central bank purchases offset this growth.

Annual bar and coin demand was broadly stable at 1,029.2 tonnes, helped by a Q4 recovery from a very weak Q3, and taking the quartely demand back to 2013 levels.

Source: Metals Focus; World Gold Council

The World Gold Council is talking up the overall 2016 changes. But shifts in the final quarter of 2016 undermine their story.

Yes, demand by retail investors for coins and bars did pick up in Q4, but it languished at unusually low levels for most of the year.

Yes, annual demand by exchange traded funds (ETFs) was higher in 2016 than 2015, but these same ETFs bailed out of the yellow metal in the December quarter in a big way.

And these is no hiding from the lackluster jewellery demand. 2016 brought a 7-year low for this segment. Rising prices for much of the year, regulatory and fiscal hurdles in India and China’s "softening economy" were key reasons for weakness in the sector.

India’s shock demonetisation policy brought the market to a virtual standstill. An initial rush for gold following the policy announcement came to a swift halt in the ensuing cash crunch. This is exactly the sort of regulatory shock you might have thought would raise demand for gold, but in fact the opposite happened. It is an event that has undermined a key reason why investors thought they should buy and hold gold.

Nor is there any hiding from declining central bank demand. It has been a favourite acquisition by bully states (Russia, other ex-Soviet states, some Arab states), but even they now show disenchantment with gold's store-of-value possibilities. They may still be net buyers but they bought a massive one third less in 2016 than 2015. And investors need to be wary when about 10% of the demand underpinning the price is determined by such dodgy sources. Despite this, 2016 was the 7th consecutive year of net purchases by central banks.

The gold price ended the year up +8% in both US dollars and New Zealand currenmcy. Having risen by an impressive +25% by the end of September, gold relinquished most of those gains in Q4 following Trump’s election win and the FOMC’s interest rate rise.

However, that +8% rise needs to be seen in the context of an unusually low starting point. See the chart below. In fact, for most of 2015 it traded at levels much higher than where it ended in 2016.

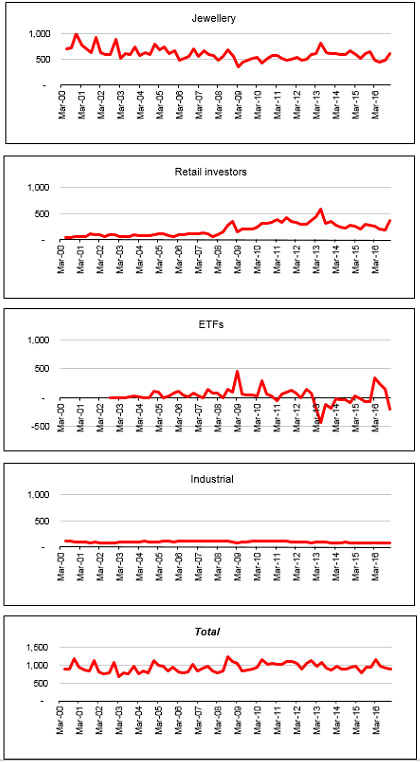

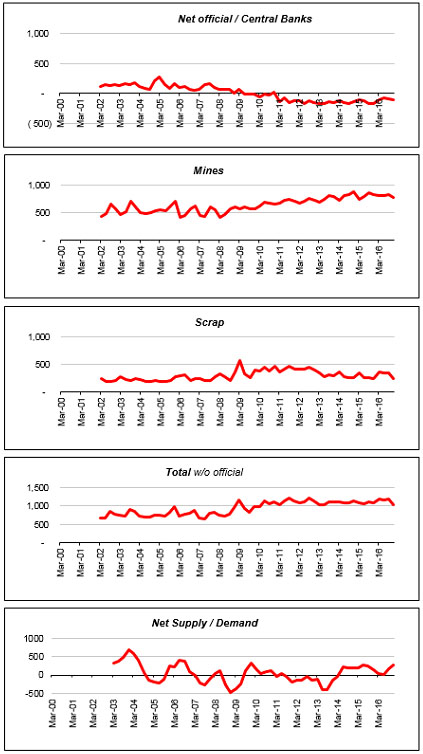

Here are the long run global gold demand charts (in tonnes):

On the supply side, things were not much better.

Mine production was down. Scrap sources were lower too. You would think lower supply would have supported prices in a fundamental way. Perhaps they did, but it was demand factors that seemed to drive pricing more than restrained supply.

The reaction of gold demand in India, and international prices, to their demonetisation policy is perhaps the most interesting and surprising event of 2016. And one that will worry gold bugs because it shows gold is not 'money' in a crisis; it is just another commodity.

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

12 Comments

Not what you're trying to say David Chaston, but the intrinsic value of gold from a cultural perspective (think China, India, Japan, Vietnam, etc) is much more difficult to quantify. Somehow I think that demand for gold and its inherent value will be perceived differently by the majority.

Nor is there any hiding from declining central bank demand. It has been a favourite acquisition by bully states (Russia, other ex-Soviet states, some Arab states), but even they now show disenchantment with gold's store-of-value possibilities.

Is that so? Germany hoards as much as China and Russia combined

Gold Reserves in Germany decreased to 3377.94 Tonnes in the third quarter of 2016 from 3378.25 Tonnes in the second quarter of 2016. Gold Reserves in Germany averaged 3417.30 Tonnes from 2000 until 2016, reaching an all time high of 3468.60 Tonnes in the second quarter of 2000 and a record low of 3377.94 Tonnes in the third quarter of 2016. Read more and more

{kind=link}

Casey research is not a reputable research company. Just look at their track record. Terrible. They belong in the same basket as Zerohedge. The fake news basket. Just look at the graph and be honest with yourself. It's silly and ridiculous.

I beg to differ. Nothing wrong with the graph it simply shows what happened in previous bull trends, that is factual so what do you mean? Are you suggesting that the graph is false?

Maybe. But as your references point out, they are "hoarding" less and less.

Here is the World Gold Council's 2016 report on central bank holdings.

And here are the current 'hoard' levels.

My memory fails me in respect of how central bank gold leasing deals get accounted for in sovereign balance sheets. One might find published vault reduction levels could well be associated with such third party trading arrangements.

I also suspect China's sales of US foreign reserves find themselves unreported in term currency swap deals rather than outright sales for another currency, presumably CNY.

Some unusual observations from here in Munich. I recently saw an bank advertisement in an ATM kiosk advertising 50g bars of gold as store of value gifts "from a bank!!!". A few days later at a McDonalds I saw a competition to win one hundred thousand euros - either as cash or gold. They had pictures of gold bars on the poster. If enough people perceive gold as money then gold will be money.

Similarly, in Japan you can see massive outdoor advertising for gold dealers in the subways. It's not actually that new. I know of the first foreign licensed gold buyer in Japan: they're primarily buying gold jewelry from cash-strapped individuals.

It will be interesting to see how the Indian government's strategy of promoting bank accounts to the currently unbanked affects gold.

After all, if you keep your savings in gold because you have no choice, what happens when you do have a choice.

For investors the real gains are in the gold and silver miners; various global mining companies indices gained +50% in 2016. My little ASX group gained 17% in January 2017 slightly more than the ASX XGD index which gained 13%. No-one really knows the future hence use of a trailing stop-loss is essential. I think this year will be great in this sector but there will be high volatility such is the unstable state of international politics and economics right now. Think Italy and maybe France EU breakaway for a start let alone Ukraine heating up again now and add in global trade, currency and inflation tensions. And we know Trump loves gold...............

http://www.321gold.com/editorials/hamilton/hamilton021017.html

This is a great article on where gold mining stocks are at right now in the cycle. This guy is one of the few that I have found to be right more often than not.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.