The following article is "Box A" taken from the Reserve Bank's latest Financial Stability Report, released on Wednesday.

Vulnerability of owner-occupiers to higher mortgage rates

The ability of households to service their mortgage debts under a range of economic scenarios, including a sharp and unexpected increase in mortgage rates, is important for financial stability. Widespread difficulty in meeting mortgage payments can precipitate or exacerbate financial instability by causing borrowers to either default, sell their house or cut their consumption sharply.

New Zealand is particularly vulnerable to a sharp rise in mortgage rates as the banking system funds a large proportion of its mortgage credit from offshore wholesale markets. The cost of this funding can increase sharply if there is an unexpected increase in global interest rates or a change in investor risk appetite, and banks are likely to pass on the higher funding costs to customers through higher mortgage rates.

Banks’ loan origination standards partly guard against the risk that higher mortgage rates cause household stress by ensuring that new borrowers are able to continue servicing their loans if mortgage rates increase. Some banks incorporate a buffer of around 2 percentage points in their serviceability assessments, or a minimum interest rate of about 7 percent.1 However, serviceability assessments also often rely on assumptions about minimum essential living expenses and the reliability of income sources, and typically do not test against large increases in interest rates.

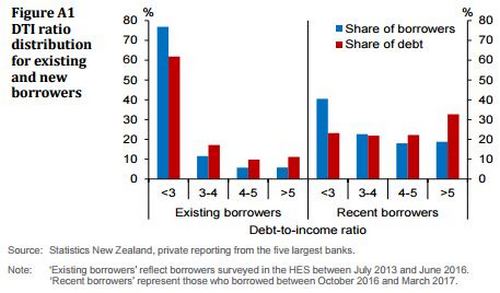

The Reserve Bank has conducted a simple stress test of current owneroccupier borrowers to an increase in mortgage rates to 7 percent and 9 percent. An interest rate of 7 percent is close to the average two-year mortgage rate over the past decade, whereas 9 percent provides a more extreme but still plausible scenario. Data from the Household Economic Survey (HES) were used to assess the resilience of a sample of existing mortgages originated before July 2016, while survey data on the debtto-income (DTI) ratios of bank lending flows were used to assess the resilience of more recent borrowers.2

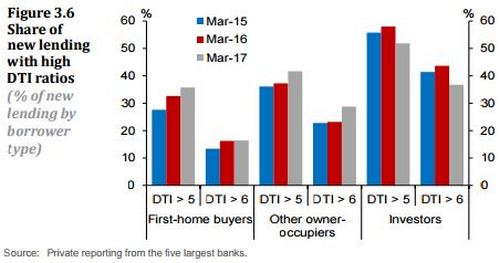

DTI ratios tend to be highest for recent borrowers who have had limited time to pay down debt or increase their incomes, and because house price inflation has been strong relative to income growth in recent years. After removing outliers, 19 percent of recent borrowers have DTI ratios above 5 compared to 6 percent in the overall stock of borrowers (figure A1). The share of new borrowers with high DTI ratios has increased in recent years (figure 3.6), which, if maintained, will increase the indebtedness of the overall stock of borrowers over time.

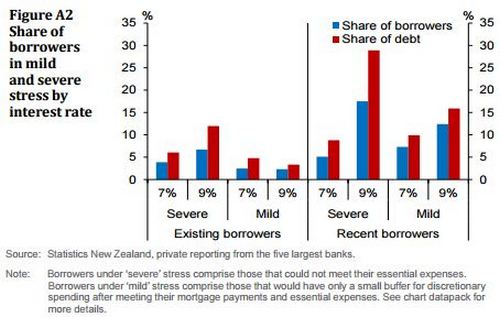

The vulnerability of borrowers to higher mortgage rates was assessed by comparing borrower incomes to mortgage payments and other essential expenses. Essential expenses are estimated using the HES, and are calculated based on the lower quartile expenditure for a given household type and income level.The estimated essential expenses generally increase with household income.

Many borrowers are estimated to be vulnerable to higher mortgage rates (figure A2). It is estimated that around 4 percent of all borrowers, representing 6 percent of the overall stock of mortgage debt, and 5 percent of recent borrowers, representing 9 percent of recent mortgage debt, could not meet their essential expenses (‘severe stress’) if mortgage rates were 7 percent. A further 2 percent of all borrowers and 7 percent of recent borrowers would only have a small buffer for discretionary spending after meeting their mortgage payments and essential expenses (‘mild stress’). Stress would be much higher at a 9 percent mortgage rate, with 7 percent of all borrowers and 18 percent of recent borrowers expected to face severe stress.

Auckland borrowers appear particularly vulnerable to higher mortgage rates. Around 5 percent of existing Auckland borrowers are estimated to face severe stress if mortgage rates were 7 percent, compared to 3 percent of borrowers outside of Auckland. The share of recent borrowers in severe stress is also expected to be greater in Auckland, particularly if mortgage rates rose to 9 percent.

There is evidence that borrowers with high DTI ratios are the most vulnerable to rising mortgage rates. At a mortgage rate of 7 percent, around half of existing borrowers with DTI ratios above 5 are expected to face severe stress. However, this represents just 3 percent of borrowers.

Overall, this analysis suggests that a significant proportion of New Zealand borrowers are vulnerable to a material increase in mortgage rates. A sharp and unexpected rise in mortgage rates could see the most vulnerable households default, sell their houses or reduce consumption to repay debt. Recent borrowers in Auckland and borrowers with high DTI ratios appear most vulnerable, signalling that a continued high share of lending at high DTI ratios is concerning and may present a risk to the housing market and financial stability.

1) The Australian Prudential Regulation Authority has provided guidance to Australian banks that states that they should assess a potential borrower’s ability to service their mortgage if mortgage rates were at least 2 percent above the current mortgage rate, and at a minimum mortgage rate of 7 percent.

2) Data used in this analysis are imperfect. For example, the DTI survey data include a significant quantity of ‘outlier’ borrowers that have been excluded from the analysis.

10 Comments

Im surprised at the number of recent investers with 6+ DTIs, with the market cooling do they take their profits now or hold on for the long haul while the capital gains slide?

There is an interesting assumption you made there... recent investors are unlikely to have any profits at present.

The second footnote needs edification. A significant number of "outlier" borrowers excluded from the analysis? Let me guess, these outliers are in the the DTI strata much higher than 6... these "outliers" are likely to be the first horses attempting to bolt from the barn, and are quite important to where the future lies.

A significant number of NZ'ers are vulnerable to a rise in interest rates QED rates wont rise. Or is it now the RBNZ's job to crash the economy?

No need for the RBNZ to get involved in the so called "Crashing" of the economy. The fact that so much money has been borrowed by our banks from offshore banks, mainly US banks, means it will follow a natural path without any intervention at all.

Scary.

Sorry, but the writing has been on the wall about this for several years. The RBNZ only needed to read interest.co.nz, and peoples comments. It is going to all end in tears for some, unfortunately.

.. Prof Steve Keen was interviewed on Radio National recently ...

If there's any deeply indebted Kiwi property investors who enjoy wandering around in soiled nappies ... might I suggest you have a listen to the good professor .. .. ( at the very least you'll have a little something warm next to you , in the winter of our discount tent ... as the nation's property equity tumbles downwards )

... as dismissive as I once was of his alarmist calls on world debt ; and his trek up the Kosiousko Hill in Australia , due to a failed bet on the subject ... he did pick the GFC correctly ... and our private debt over houses ( non-productive assets ) does leave us vulnerable to an almighty pooping of the pantyloons if the property bubble does burst ... ... ffffzzzzzzzz ...plop !

It's rare that I complain about people's comments but such grossness is out of order on this fine website.

The filthiest of words used here.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.