By David Chaston

Reading the international business media, as I do, you find analysis gems that trigger the question: But how does New Zealand compare on that basis?

Today, on Bloomberg, was a story that leads like this:

Australia is riding out a huge gamble on property. The bet: 27 years of recession-free economic growth—during which Sydney home prices surged fivefold—would continue unabated and allow borrowers to keep servicing their debt.

The gamble has turned dicey. Tighter lending rules are deterring investors, and lofty prices are starting to deflate. A banking probe is exposing dodgy practices, and a mountain of risky loans that helped fuel the bubble needs refinancing—just as global borrowing costs rise. Now Australians are stuck with the highest household debt levels among G20 nations.

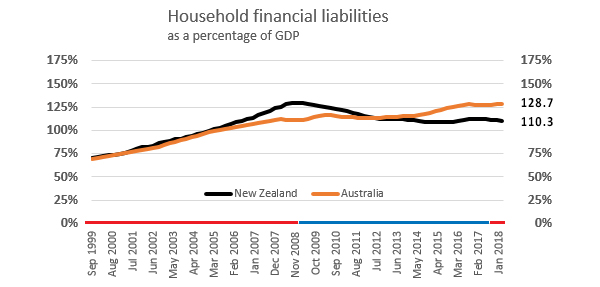

The key data item is that "Australia household debt exceeds 120% of GDP".

And yes, it did trigger the question, how does New Zealand compare on that basis?

Here is the answer:

This data surprises somewhat. New Zealand's excess to "over 120%" occurred over a decade ago.

The recent run-up in our household debt has been matched by strong GDP growth. While the Aussies have been increasing their load, we have been easing back on ours. In fact, we are back to levels we last saw in June 2003, 15 years ago.

But even at 110%, we are still relatively high. That Bloomberg article is based on Bank for International Settlements data that shows New Zealand with only 91.8% at December 2017. The US has 78.7%, Canada has 100.2%, Germany has only 52.9%, while the UK has 86.7%.

Clearly the BIS data (based on US dollar values) makes adjustments from what the official statistics show for New Zealand and Australia.

For the record, the above chart uses RBNZ series M5 and C22, while the Australian data is from the ABS, series 5206.0, tables 3 and 34.

The surprise in this data is that a) New Zealand has lower levels than Australia, and b) that our levels have been falling for a decade. Wasn't expecting to find that.

24 Comments

What about the relative difference in retail interest rates between New Zealand and Australia? If you take into account Australia's lower rates, could both nations effectively be "maxed out" on borrowing?

Looking at the reasons for NZ's housing debt--a bank-fueled / govt-sponsored housing bubble generated by buying and selling of existing housing stock--our h'hold debt may not be "severe" but it's definitely a waste of resources and human productivity. If you compare h'hold debt to GDP, we're actually worse than Japan at the peak of their bubble. That's relevant because Japan appears to have been deleveraging forever and a day and h'holds have to to live with the implications of that. Somehow the Anglo-Saxon nations' leaders seem addicted to bubble economics. Saying it's all going to end well or miserably for indebted h'holds is a tough call to make. At the moment, all I see is a rise of modern-day serfdom. Personally I think the poor might have it better than the middle class who has bought into this nonsense hook, line, and sinker. That is where people are really entrapped.

I'm not the least bit surprised that New Zealand has lower levels than Australia. Has there ever been a statement that NZ had higher household debt than Oz?

"Bank for International Settlements research showing that household debt starts dragging on future economic growth once it’s equivalent to 80 percent of gross domestic product".

NZ is at 110% so WELL over. Just not as much as Oz (a cold comfort)

When and how much is this going to drag on future economic growth?

REAL soon.

When and how much is this going to drag on future economic growth?

Something I think about too. Let's look at what we know: housing bubbles stimulate consumer spending, which people should understand is the the guts of economic activity for most developed countries (not exporting milk powder and merino wool fashion wear). As soon as h'holds start to "deleverage", consumer spending is negatively impacted and creates a negative feedback loop, which exacerbates it all. I think there are signs of this already as I alluded too some time ago. Discounting is rife in the retail sector. If spending is "demand driven", it appears that NZ consumers are already "price shoppers". There is a good reason for this: Most people are tapped out and living paycheck to paycheck.

http://www.nielsen.com/nz/en/insights/news/2018/the-470m-opportunity-ch…

Yeah, to be honest, when I read the article after reading the headline I was a bit surprised to see our debt ratio was “only” at 110% vs aussies 128%. They both seem to me to be awful numbers. I struggle to see how this is “not as bad as you think’ and how we are exercising “control” over it

Dang, we missed out on the gold medal. But silver is a nice colour too.

Magpie economics

Would I be correct in assuming that you own a few properties Mr Chaston?

Wow!

Only one, the one I live in. And no Trusts either. More importantly, the data is what it is. I am not trying to fit it to some partisan position.

David, have you got a link to our prediction thread from last September/October? I'd like to check the relative performance after 8 months.

I stand corrected.

David , I am often amazed at how commentators make assumptions that some of us own multiple houses, as if we are part of some conspiracy, its quite annoying .

It may be a widely held perception about Baby-boomers , that we are all wealthy landlords

Like you , we own our family home and have no residential investment properties.

We do have a stake in a small old family -owned holiday home with our extended family, and its not owned for commercial gain .

Does our debt become an even bigger iceberg if our GDP takes a hit from this escalating trade war? Right now, this is a measure of our vulnerability. I suggest it looks stable when measured against an increasing GDP.

Correct me if I'm wrong but hasn't a lot of GDP been generated by this housing bubble? Also, debt to household income is another measure that's not looking so pretty alongside price vs rental yields.

Anyone notice there is not one total debt number in this? It's all quoted percentages of a nonsense measure called GDP.

Debt to income is indeed the worry, given that most incomes are being paid by the debt, if you trace them back. Every contractor is paid by a mortgage, which is an assumption the mortgage-holder will be able to pay back. Trace the income of a university employee, and a percentage is student debt. Essentially we're borrowing more and more from the future. Can't possibly last.

https://www.mckinsey.com/featured-insights/employment-and-growth/debt-a…

exactly.

The nonsense good news assumption in GDP figures is that more debt is being taken on because we are so confident of the future that we are "ïnvesting" in the future - in something that will generate more of something down the track... The reality is we are consuming the future because we dont have sufficient current income. Leverage is the only game in town.

Everyones incomes are now totally dependent on growing the debt ponzi ... which means interest rates must go lower. Money is free, Debt carries no risk & capital/savings are worthless.

Capitalism is eating itself. Like Marx said it would.

I think similar to you. Question is what is the nexus point?

Everyones incomes are now totally dependent on growing the debt ponzi ... which means interest rates must go lower. Money is free, Debt carries no risk & capital/savings are worthless.

Capitalism is eating itself. Like Marx said it would.

Yep. Someone said to me "what happens when we run out of people to rent to? Do we simply import more people rent to?" I think the idea of importing people to rent to seems to be the only weapon we have.

The more important point is: Is it a productive use of capital?

Everyone needs a house to live in, so from that perspective it is.

But most of the increased housing debt to gdp has gone into increased land prices.

This is not a productive use of capital and simply an added cost to living in NZ.

These are all average figures and can be most misleading as they include households with no debt.

Correct analysis requires segmentation into say deciles of only those with debt then comparing against their incomes as a much better view of the true risks out there. I suspect the picture would not be pretty !

Good point JB. There is a spread for many items which for this one is likely to be near the usual 80 - 20. ie 20 percent of the people carry 80%.

Having made that guesstimate it would be good to understand the real figure. DC?

What I am unsure of is that if it is that 80 - 20 sort of figure what happens when it all breaks apart. One could say the 20% get screwed, and the world and the rest of us sail on regardless.

The last data I saw some time ago was that roughly one third of NZ households have no mortgage. Again would need to segment by region - I would suspect wide variances.

If so - then you can increase the ratio's for the remainder by 50 % !

""The recent run-up in our household debt has been matched by strong GDP growth."" I'm not too sure how you measure household debt but presumably it is some total for individuals divided by the number of households; if so it will have been effected by recent heavy immigration by students who tend to have more adults to a house. Similarly our GDP growth looks good until divided by the rapidly growing adult population.

A point no one seems to have made from looking at the graph is that during the nine long years under National, characterised by so many in negative terms, our household debt as a percentage of GDP for the most part declined. Food for thought ?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.