Gold is in a bit of trouble.

And without three dictators, things would be much worse.

In the September 2018 quarter, Putin's Russia bought more than 90 tonnes of the yellow metal, Erdogan's Turkey bought more than 18 tonnes, Nazarbayev's Kazakhstan bought 13 tonnes. These three bought 83% of all central bank purchases in the period, and they were joined by India who also bought 13 tonnes. These four accounted for more than 90%.

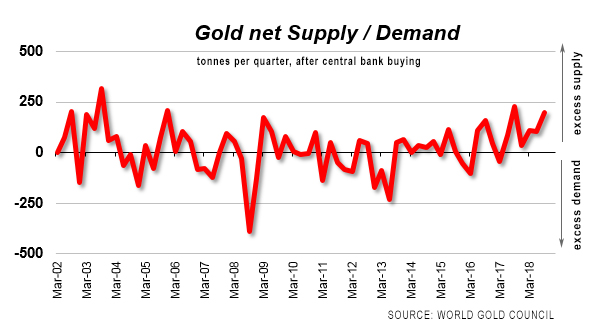

Gold needed them. Other than central bank buying, supply rose and demand fell according to the latest World Gold Council data. In fact supply in Q3 2018 was 1,162 tonnes and demand was only 816 tonnes, an oversupply of 346 tonnes. So even with strongman buying the overhang was almost 200 tonnes in the quarter. How long the price can hold up in the face of the strong supply flows is an open question.

From November 1, 2017 to November 1, 2018 prices in US dollars have slipped -5%. In New Zealand dollars they are virtually unchanged.

But what will happen to the extra 197.2 tonnes produced in the third quarter of 2018? Don't forget that is on top of the 104.2 tonnes of excess supply in Q2, and 110.3 tonnes of excess supply in Q1. It is mounting up; in the past year the excess is 445 tonnes, even after those handful of 'central banks' above bought 426 tonnes on the open gold markets. Without central bank buying, the excess has been 872 tonnes of more supply than private market demand. That is a massive 24% overhang over the past year.

Unfortunately, jewellry demand is stagnant at 2,220 tonnes in the past year. Technology demand is always stagnant at about 330 tonnes a year and has been like that for seven years (and prior to that it was higher), while investor demand is declining and only 1,056 in the past year (down -9.3%). A recent loss of faith by professional buyers for exchange traded funds isn't helping and overshadows the decline by the traditional bear-investors in coins and bars which itself is -8.4% lower in the past year to September than in the equivalent prior period. For them, they have the ongoing costs of storage, so a lack of price gains will add to their overall losses.

You kind of need a sort of blind faith to keep buying gold. Yes, it might have the sort of counter-cyclical insurance feature often touted, but that seems a very risky bet these days when the supply overhang is as much as 24% ! and the only main buyers are three dictators.

And even for them, their holdings are minor. Russia for example has now amassed more than 2000 tonnes in their reserves as they actively de-dollarise. But at today's prices that is worth only US$80 bln and is equivalent to about 5% of Russian GDP, or a bit over two weeks of activity in their economy. Hardly a big reservoir of financial stability. And it will be an increasing problem for Russia if this 'investment' loses value in international terms.

Here are the long run global gold demand charts (in tonnes) with the Q3 2018 data added:

![]() Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

Our free weekly precious metals email brings you weekly news of interest to precious metals investors, plus a comprehensive list of gold and silver buy and sell prices.

To subscribe to our weekly precious metals email, enter your email address here. It's free.

Comparative pricing

You can find our independent comparative pricing for bullion, coins, and used 'scrap' in both US dollars and New Zealand dollars which are updated on a daily basis here »

Precious metals

Select chart tabs

7 Comments

Gold has certainly failed to live up to a lot of expectations over the last decade. What I can see in that chart embeded in the article is a change in trend late 2014 from negative to positive. That looks to be reflected in the price.... just. Not that I think gold will ever be money, or part form a meaningful part of SDR's as some believe, but gold could be an answer to the question of where to put money in the presence of a credit fueled asset bubble. All assets demanding a yield are now part of the bubble of everything. How gold will behave as the lack of aggregate consumer demand takes the heat out of credit creation is going to be interesting.

Potential plays in both directions are that gold gets sold off during collateral calls as the asset bubble starts to unwind. A lack of liquidity might keep pushing up interest prices though as a counter force that outweighs selling. Or the opposite is that money creation by governments goes into overdrive to buy distressed assets. They do have prior for this in the US with MBS purchases. Plus the BOJ buying up assets. A sort of hyperinflation event like that also has potential outcomes in both directions. Safe haven buying to protect purchasing power, or the money is instead put into front running governments by buying assets? Interest rates will drop in this instance, so gold may hold value in a negative interest rate environment.

Where will the smart money go? Lots of possible scenarios, add yours below :-)

If at anytime money starts to flow into gold in significant quantities it could exacerbate a liquidity crisis.

Andrewj's link bloomberg link to Taleb yesterday on the 90@9 has about as good advice you can get on the matter. It is near the end.

I wear a gold ring on the third finger on my left hand. That's all the gold I need.

Anymore than that and she would just spend it anyway.

Gold has been on the up in recent weeks and historically it does extremely well when equity markets turn bearish for the long term. Personally I believe that the recent market volatility is a sign of whats to come so Gold could be a great play moving forward. Watch this excess supply drop in the coming years.

Some back of the envelope calculations. Total above ground gold (according to google) = 187200 metric tonnes. At today's price that equates to 7.42 trillion US dollars. Some other market caps in USD for comparison. US housing market = 31.8 T, US stock market = 30T... Food for thought.

So you could almost say it’s under valued, well colour me surprised...

Gold prices quoted are for investments (paper) and those contracts normally have the disclaimer that instead of future delivery of physical gold, you can be compensated with fiat currency at a predetermined currency value. For some people wanting to utilise gold as a store of value, there is a difference between holding something physically in your hand or place you consider safe, and holding paper with "promise to deliver physical gold" (or pay with paper, also referred to as fiat currency). If the values quoted above are for real physical gold in existence, then what is the total value of paper contracts? Bear in mind, some of which may not deliver what people expect.

Likely only in extreme circumstances of a major international currency or settlement system changes (perhaps forced rather than voluntarily), will the real value of unencumbered possession of gold be determined. But when such changes happen, some with foresight or understanding what true wealth really is, will benefit in ways that many lifetimes of hard work may not achieve.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.