By David Hargreaves and Jenée Tibshraeny

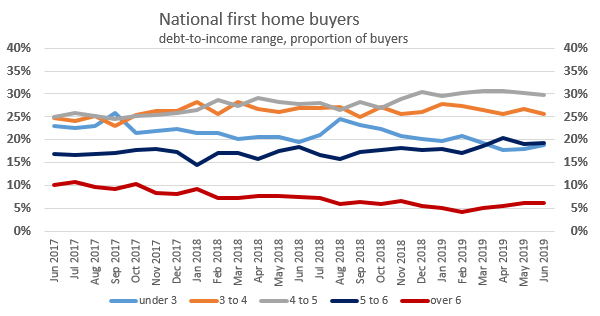

New Reserve Bank figures released for the first time on Monday show that a third of all Kiwi first home buyers have debt that's over five times their annual income.

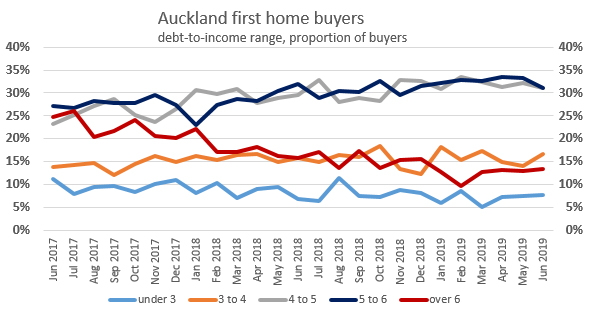

In the pricey Auckland market, nearly half of the FHB debt is at a DTI of over five. The ratios are based on gross (pre-tax) income.

This information is now going to be made available on a quarterly basis through two new tables the RBNZ's compiling, namely this table and also this table.

The RBNZ, in giving examples of the new series said that June 2019 DTI statistics show that for owner-occupiers taking out new mortgages:

- 31% of borrower debt was at a DTI over five, down from 37% in June 2017.

- 33% of first home buyer debt was at a DTI over five.

- In Auckland, almost half of first home buyer debt was at a DTI over five.

- First home buyers most commonly borrow between 4-5 times the size of their income.

- In June 2019, the average gross income of first home buyers was $116,000 per year, compared with $132,000 for other owner-occupiers

The release of the new information comes as the Government is considering including a DTI tool in the RBNZ’s 'macro-prudential toolkit' as a part of Phase 2 of the Reserve Bank Act currently underway.

The second of three rounds of consultation for this second part of the review closes on Friday.

The RBNZ previously pushed for inclusion of a DTI tool under the previous National Government - but the Government delayed it beyond the 2017 election. However, the RBNZ has continued to see some form of DTI tool as a useful addition to its macro-prudential measures, alongside such things as the already in use loan to value ratio (LVR) restrictions.

In releasing the new information on Monday, the RBNZ said it didn't have a hard and fast number of what level of DTI would be concerning among house buyers.

RBNZ's Head of Department Financial System Policy and Analysis Toby Fiennes said the data would demonstrate how useful a DTI tool would be.

Asked whether the release of the data was a move to put pressure on the Government to include a DTI tool in the RBNZ’s toolkit, Fiennes said: “No, it’s not for that purpose. It just happens that now is the time when we have enough confidence in the data and we feel we can put it out there.

“If we did have the tool, we would be very unlikely to be using it right now."

He said the central bank had seen the vulnerabilities of the housing market as having reduced over the last two or three years "and that’s why we’ve been reducing the LVR restrictions".

"The level of high DTI has also been coming down over the last couple of years."

Isn't it still high though?

“It’s high, but it’s not at an extraordinarily high level… We have to have a pretty sound reason for introducing restrictions into a market.”

The RBNZ said it developed DTI data to better understand risks to financial stability from mortgage lending activity. Monthly data is available from June 2017, and is sourced from a survey completed by all registered banks in New Zealand.

“Banks supply us with summary data on the debt and income of their new mortgage customers,” Head of Data and Statistics Steffi Schuster said.

“The DTI statistics we’re publishing today give an insight into the ability of homeowners to service their mortgages.”

DTI data was important to inform financial stability risks, as households with higher debt levels relative to their income may be more at risk of defaulting on mortgage repayments.

Borrowers with higher debt levels relative to their income are more likely to reduce spending in response to shocks, such as a loss of income or higher interest rates. This could create stress for individual households, and have an impact on the wider economy.

In addition to informing financial stability risks, DTI data is also a useful tool for assessing housing affordability for recent homebuyers.

“DTI data can be viewed alongside other information to give richer insights into New Zealand’s housing market,” Schuster said.

“For example, by comparing DTI figures with loan to valuation data, we can better understand risks from households with a combination of large loans relative to the value of their property, and large loans relative to their income.”

62 Comments

Any reason they havent published the Average DTI for Auckland FHB's? rather than just stating the % over 5 times?

Correct % over 5 times could be anything. Is it just over 5 times or 8 or 9 times (As even that is over 5 times :)

isnt that ridiculous!!!

and this is published by the RBNZ.. are they part and parcel of the housing ponzi???

This con job goes all the way up to our reptilian overlords!

Best highlighted with the analogy, very often latterly understood by central banks.

https://www.google.co.nz/amp/s/www.urbandictionary.com/define.php%3fter…

Yes. For couples earning $50,000 p.a. each ($100,000 combined income) it would be between 8 and 10 times for a modest 3 bedroom house in Auckland of $800,000 to 1,000,000!! Not to mention the 15 to 20 times of a single income $50,000 p.a.!

When my husband and I both worked for the largest global IT co, our combined income was about 250K. Yet we chose we live in a crosslease 3+1 house in West Auckland that cost less than 600K. There are plenty of houses in the 500K-600K range in West and S. Auckland. Why would someone earning 50pa or even 100pa dream of living in a 800k-1m dollars house? Shouldn't people do their maths and live within their means? Or is "living within your means" an alien concept among Kiwis?

I totally agree Rolo

The example from pathos is even based on 100 percent finance how crazy is that

"New Reserve Bank figures released for the first time on Monday show that a third of all Kiwi first home buyers have debt that's over five times their annual income."

So no bubble then.

Someone will correct me if I'm wrong but isn't that higher than in the US before the last bubble burst there?

"31% of borrower debt was at a DTI over five, down from 37% in June 2017"

Well, it's coming down, so that's something. But bugger me, imagine looking down the barrel of a student loan and then a 30 year loan x5-6 your combined income and the prospect of dwindling state pensions? Ay carumba.

I suppose what they fail to mention is that those 2017 buyers who had 10/20% deposit are now still over 5x DTI but now also have negative equity.

I heard a very smart bit of analysis; you know the market is crashing when the media starts to publish stories about young couples, families, and grannies who have been forced to sell (for whatever reason) and have lost all their equity.

Someone told me that at the start of 2018. A few months later those sorts of stories started appearing in Aus papers about Sydney. And we all know what happened next...

Will be interesting to see when those stories start popping up in Auckland.

I've seen a few places in the past few months that fall into that category but the owners aren't in enough trouble yet to have to accept the changes in prices that have already occurred. Give it another six months and I reckon the unfortunate reality will have come home to quite a few folks.

Sweet. Crisis averted.

Those 50% of FHBs will have no problems keeping the house in the case of a negative employment shock.

A DTI of 5 would cost 27 percent of gross income using fixed rate mortgage. That is very affordable.

Not sure how that's relevant.

Income after tax and kiwi saver is a more meaningful number to use when considering affordability as nobody in a salaried job gets paid gross.

"Income after tax and kiwi saver is a more meaningful number to use"

It might be more meaningful but that is not how housing affordability stat is calculated. From memory the gross income before income tax is used. That is why interest.co has highlighted it would be better to use net income figures and more logical as it takes account of tax rates. And as income tax rates are so low compared to earlier years I think your position does not hold water

Tax (~20%), kiwisaver (3%), student loan (∽10% of income)... oh, thats roughly 1/3rd gone.. if Houseworks 27% figure is accurate then thats 60% gone before food, clothing transport, healthcare, insurance.. oh and children.

No need for children. We just keep importing people. Which suppresses wages. Which means people living here can't afford children. But we'll just keep importing people....

Indeed, absurd that we make it ever more difficult for average Kiwis to have children then rely on bringing people in to boost the fertility rate.

Not bad then nearly half left after paying tax student debts and accommodation costs as well as setting money aside for savings. If I was a fist home buyer again and knowing what I do now about asset bases propelling a portfolio I would do that in a heartbeat.

If someone is still paying student loan I really don't think they should be having children? Have an education first, work for at least 10 years, build up equity, be financial stable and have your own roof over your head. It is called "Delayed Gratification". & yes, don't bring children into the world pls if you cannot afford to give them a good life. The world is over populated as it is.

So. Only ~54% percent of gross income in the case that one income earner loses their job.

Sweet. Again. Crisis averted.

Nice use of humour nymad

Yes, paying 27 percent of gross income is manageable for total debt payments for a household and does not create undue financial pressure. So a DTI of 5.0x results in a manageable level of debt payments at current interest rates.

The median household income in Auckland is about $94,378, so a DTI of 5.0x is about $471,889 for a mortgage.

The price of a median house in Auckland is $830,000. That means that the LVR would be about 56.9%.

In order to afford that house, the household needs an equity deposit of 43.1% (or $358,111). Not sure how many median household income families who are renting in Auckland have $358,111 for a deposit to purchase a median priced house in Auckland. If a household on a median household income is unable to afford a median priced house in Auckland, then that it unaffordable.

If you take the current median house price of $830,000 for Auckland, deduct a 20% deposit, then the mortgage would be $664,000 (a DTI of 7.0x). Assuming a 4.0%, 30 year P&I mortgage, then the payments would be $38,399 per year (or 41% of gross median household income). At 41% of gross median household income, housing in Auckland is thus unaffordable.

RBNZ's financial system policy head Toby Fiennes said lower interest rate environments could support higher DTIs.

What happens when the business cycle eventually hits a wall due to internal or external shocks and jobs are shed across the economy? How many households will turn delinquent under high debt load if unemployment ticks up just 0.5-1pp?

thats not his problem, he would be holidaying in one of his resorts...

Well, if they're really worried about high DTI then why did they cite falling prices in Auckland as one of the drivers of cutting the OCR? They seem a bit conflicted.

RS, are you sure the RBNZ cited falling house prices as the reason to cut interest rates? I think the reason given had more to do with low inflation and a lot of economic headwinds both locally and internationally

"The outlook for household spending was discussed with regard to the assumed dampening impact of soft house price inflation. Some members noted lower mortgage rates could contribute to a stronger pick-up in house price inflation, which could support consumption. Other members noted that house price inflation could remain weak, for example if net immigration continued to decline relative to the number of new houses being constructed."

One thing is for certain though is that 50%!of Auckland’s first home buyers will be on beans on toast after mortgage, rates, insurance costs - given DTI’s are on post tax income, can’t see much left there to support the consumer economy. Similar situation will exist for the tenants who are paying the mortgages of the later investors... not a lot left after the beans are paid for. Anyone seeing an uptick in the number of coffee shops for sale in the Super City?

From article above - "The ratios are based on gross (pre-tax) income."

Not as the but I recalled Adrian Orr discussing as one of the factors.

I'd need to go back and re-watch the coverage to find the exact quote and time.

Interesting that the 'over 6' figure in Auckland has dropped away substantially, far more of a drop than any fall in price.

I suspect that could be because the really impatient FHBers who couldn't hold on have dried up. I (29) know of a few people my age who took on collosal mortgages between 2016-18, because they got caught up in the market FOMO. Conversely I don't know a single person who has bought a first house in the past 18 months. Very small sample size naturally, but the numbers in this article seem to support it.

Auckland has effectively run out of suckers...

Hi milky one. There are probably far fewer parents today prepared to stump up the deposit money than there would have been 2 years ago. Most should be telling their kids that there is no need to rush now, let it slide and we can talk about the deposit later when overall commitment is less. If they aren’t thinking like that then they are either dumb, or being irresponsible with their kids future.

When we were young we could budget on an increased income to help blow off the mediocre mortgage. Globalization now means wage increases are toast, the rest of the world will do our job for 50 cents an hour.

So good luck with the 30 year mortgage based on the old order.

"In Auckland, almost half of first home buyer debt was at a DTI over five. It’s high, but it’s not at an extraordinarily high level..."

I think we all know, including the RBNZ, that this will seem very high if/when the housing market starts tanking from this high level, along with a shock from the global economy, which is likely why they are already throwing the kitchen sink at the OCR. If we head to recession territory and unemployment rises, watch out. The whole situation seems unsustainable but all they can do is keep going - lower rates, more FHBs, debt.

Why do they call it DTI and not LTI? the "D"ebt is the same as the "L"oan, isn't it?

maybe if you shout Toby Fiennes morning tea, he might consider your request :)

From the RBNZ press release

“For example, by comparing DTI figures with loan to valuation data, we can better understand risks from households with a combination of large loans relative to the value of their property, and large loans relative to their income.”

I would suggest that they’ve woken up to what DFA have been suggesting for some time, that for some households there is ‘a combination of large loans’

I believe in Australia there are households with total exposure more like 8-9 times gross household income. (Some apportioned as interest only, some as repayment to get the total borrowing ability higher) and keep the credit excesses going.

"5+ DTI. Not great. Not terrible"

they stopped with 5+, what is the actual number

At the end of 2018, 15% of new mortgages were between 5-6 household income. 23% were in excess of 6 times. See DFA ‘Unnatural Acts from the RBNZ’ - they quote the matrix used by the RBNZ in last November’s financial stability report. The issue is not just confined to first home buyers but also those chasing the Joneses on second move up.

I really want to be able to give this more than just the one like.

I think you might have been the only one who got it. :)

I’m assuming we’re talking household incomes? If so, our debt to income was 1.5x when we bought in 2017.

Way to go NZD

Has anybody else noticed that Homes.co.nz has started adding 'sold' red dots from a year ago instead of just the last 6 months. This is very telling and very cynical. This now gives the impression more houses have sold than actually have and the prices look higher for sold prices because they were higher a year ago. The last gasps of a failing housing market. Just accept it housing industry, the bubble has burst. Live with it. Give the young and the poor a chance for once. This greedy club has been going on for far too long.

Nice catch. What a bunch of sneaky so and sos.

The North Shore of Auckland is a sea of recently sold red dots on Homes.co.nz. The ones I randomly checked were sold between Sept and Oct 2018. Gosh the RE industry is in real trouble if they've become this desperate.

I did notice that the other day, a place near ours was still showing as recently sold (October 2018).

Gee that's really cheesy and desperate.

Maybe they red dot their last 20 sales

Ha ha

Also: so many of the recent sales which are actually from the past few months are "price unavailable".

Message to all First Time Home Buyers "Wait for the market to bottom out" it is falling both here in Auckland and else where in NZ. Do not pay higher than the 2017 RV price and negotiate lower if you can.

Make sure you only pay for what you can afford!

"Negotiate lower" ... Good strategy. Once you have bought your first home you are definitely on the ladder and building equity.

Except like now in Auckland when you are on the road to negative equity :/

Then take off those negative nancy glasses you might be able to see better

Yea Glitzy, just stand on your head. Then you will see that your equity is actually going up.

Its not yet falling "elsewhere in New Zealand" its still rising. Currently I'm only focused on Tauranga but most people selling are still extrapolating the RV's from over a year ago to big increases in asking prices and property sales have hit a brick wall. Starting to see some at below the RV and they are still not moving. My watchlist is growing on Trade-Me but very little is dropping off it over time. Perhaps one annoying thing is when they do its "withdrawn" rather than either withdrawn or "sold". Does anyone know if "sold" is even an option to sellers ?

"withdrawn by seller" on TM is the only option. You have to look elsewhere to find out if it's actually sold, or taken off the market.

Looking up the agency's listing (on their website) is often a good indication. Usually if it's sold, they will proudly trumpet that.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.