Auction activity continued to warm up in the last week of September with a spring lift in activity now clearly evident.

Interest.co.nz monitored 206 auctions around the country in the week of September 23-29, compared to 175 the previous week and 159 the week before that.

Of the 206 properties monitored, sales were achieved on 124 giving an overall sales rate of 60%.

And more are selling at prices above their rating valuation (RV) .

Interest.co.nz was able to match selling prices with RVs on 90% of the properties sold, with 63% selling for more than their RV.

Significantly there were only minimal differences between the Auckland and national figures, with sales achieved on 61% of the Auckland properties auctioned with 57% selling for more than their RVs.

There were also very low numbers of properties that were withdrawn from sale or had their auction postponed, with just two postponements and two withdrawals during the week.

The figures suggest that the market is becoming more buoyant as spring progresses and that Auckland is no longer lagging behind the rest of the country.

Other indicators such as the Quotable Value and Barfoot & Thompson's figures for September also suggest the market is warming up, after what was a fairly miserable winter for residential property.

Details of the individual properties and the results achieved at all of the auctions monitored by interest.co.nz are available on our Residential Auction Results page.

The comment stream on this story is now closed.

You can receive all of our property articles automatically by subscribing to our free email Property Newsletter. This will deliver all of our property-related articles, including auction results and interest rate updates, directly to your in-box 3-5 times a week. We don't share your details with third parties and you can unsubscribe at any time. To subscribe just click on this link, scroll down to "Property email newsletter" and enter your email address.

136 Comments

This situation seems to have been foreseen.

TTP

Thank you Nostradamus.

Right? Number of sales increased as Spring arrived. Who could have predicted that?!

Yeah right whatever TTP

BS and oreo

I note a bit of negativity in your comments.

TTP has been consistent for some time his view and has taken a lot of unwarranted personal insults from those who have equally been AS FREQUENT AND CONSISTENT in posting a contrary view.

How about doing the appropriate - rather than inappropriate - thing now; accept that you may seem to be wrong and be a little bit gracious.

Personally, I think that these are just signs of an upswing and I wait for the REINZ figures, not only this month and next, to be a little more sure. I also think that it is not necessarily certain that this trend will continue into next year. However, there are still drivers in the Auckland market - falling mortgage interest rates, continuing historically high immigration rates, and housing shortages. I also see the likelihood of some increased numbers of property investors returning to the market - albeit reluctantly - due to falling term deposit rates, rising rents, and the possible first signs of some upside in property prices - for the later reason, they will be wanting to be in early rather than when the market has already moved.

P.S. BS and oreo , your comments are consistent with those who don't own property and have regrets. IF you are potential FHB, the likelihood is that first home may just get a little bit more expensive. "Feel lucky?"

What you should do Printer8 is come to Auckland and purchase a home, or a second or third or fourth investment property. You should walk the walk rather than quack constantly. .

What's the beef Cowpat? You seem to be a bit sore - not a good day for some reason? Feeling bitter about some news or something?

As I have posted my wife recently re-entered the property market and purchased a rental so I put my money where my mouth is.

If you know anything about rental property, you will know that yields were around 10% some 10 years ago and now - especially in Auckland - less than 5% As property managers fees are around 10%, it is not rocket science that this really means that rental property really needs to be self-managed. To rent in any distant city is fraught with very high risk - one is not able to readily monitor the property by drive buys, is reliant on expensive tradesmen for simple repairs like changing a washer, and if there is issues, a face-to-face meeting is both difficult and expensive.

If you want to make a meaningful comment then think before you post.

Sounds like you almost figured out why investors have pulled out of the market. And just the other day you almost realised why first home buyers are out, too. You might accidentally turn yourself into a DGM at this rate, printer8.

Cheers GGP

At least I readily acknowledged that I was incorrect in an assumption.

“Drivers”? Try rate of credit growth. Currently , year on year for mortgage debt this rate of growth is NIL

TTP It's painful reading some of the endless negative comments below. Facts are facts we have had 3 years of flat to falling prices and volumes, the market is now moving into a solid position. People are not silly the crash was a DGM's wish nothing else.

The property clock points to a upturn next year.

With slightly lower prices, lower interest rates, bigger population, ever increasing construction costs, a few more years of savings and collapse in TD's it's a no brainer that the market will strengthen.

The DGM's will of course point to our falling GDP figures ( helped a lot by having this COL in Government ) and the multiple issues overseas so an improving market should not be happening !

Well these things have never stopped it before, well done being a lone voice of common sense TTP !

The property clock and historical trends are valuable indicators, but dare mention that here and you're sure to be accused of being stuck looking in the rear view mirror. Those hoping for a crash see no need to learn from the past because "this time is different".

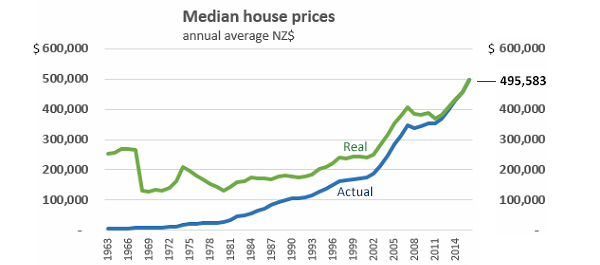

In nominal terms, NZ property has risen every decade since records began in 1963. I'd love a DGM to explain to me why "this time is different" https://ibb.co/Tk67H9k

Show data for 1984-93 then. Risen is a weasel word. Does it mean real rise after inflation?

No, nominal explicitly means excluding inflation.

1984-93 https://ibb.co/GtFSWnf

Remember, inflation eats away at the mortgage.

Many thanks for that data.

I know inflation was v high in mid 80s esp

So I would have to work out real increase

{kind=link}

I purchase a house in 1984 for the median price of $56,615. I take out an 80% mortgage of $45,292. I earn the average annual income of $14,820, so the mortgage is 3 times my salary. In 1993 I sell the house for the median price of $115,813. Due to wage inflation over this period, my wage is now the median of $28,931.31, so I can now pay off the mortgage in just 1.5 years instead of 3 years. And that's even if I was on interest only and not paying down the mortgage at all over that period. In relative terms, my mortgage has halved, so even though the house value may not have increased in real terms, I'm still much better off.

Remember that the interest rate was around 14% back then. That means you paid about $6339.48 each year for 10 years, so a total of, say $60,000. You then sold the house for a gain of (115,813-45292)=$70,521. So you made a total gain of about $10,000 in nominal terms. Pretty sure a term deposit would have beat that.

No, you haven't factored in the proportionately high rent you would otherwise been paying over that period, which more or less cancels out the proportionally high interest. I'll happily pay 10% interest if annual rent is 10% of the value of my house.

Yep. Realised that right after my comment. I have no idea what rent was but that sounds right. Agree with what you're saying, then.

We can find common ground on one thing at least!

Ha, yes.

I actually do want to apologise for that earlier nonsense. The coin flip thing was 90% a joke but I gradually backed myself into defending it as though I was being serious, so I regret that spiralling into such a long back and forth.

As for the 1984 example, it sure makes me wish we could go back to a 3.0 price/income ratio where you could save up your deposit within a year!

For sure, we can agree on that as well, a deposit in a year would be very nice indeed.

It's still doable, I bought at 3 x my salary in Masterton a couple of years back. Just don't expect to live anywhere near your place of work.

Why did you have to resort to a loan shark if earning four times median wage, purchasing price only three times income, and subject to first home buyer low deposit requirements? Good on you regardless.

Sorry I don’t follow your comment? I don’t earn 4x Median wage.

My bad, I misinterpreted this comment. Thought you were Mr Money Bags earning 4x median wage.

Ah I see! No money bags here unfortunately!

Can you please explain to me how property prices will boom again during a recession (potential financial crisis)? I'm asking unironically. I was too young in 2008 (and not living in NZ) to experience the direct effects of recession.

House prices don't boom during a recession. DGMs throwing some really tough questions at me today, go easy guys, please.

The answer is pretty straight forward CJ

The reaction to the GFC by central banks (including RBNZ) was to cut cash rates significantly as well as the US and some others were involved in QE or “printing money”. The purpose of this was to stimulate the economies. This meant interest rates became very low meaning cheap money was readily available (borrowing) so investors put money into assets chiefly houses and shares. Both of these increased significantly as especially cumulative causation added further fuel.

With the current global economic issues central banks are - whether rightly or not - again employing the same measures (e.g. RBNZ OCR cuts).

Some will argue that this is not sustainable; and others that this is possible with some central banks having already gone negative.

The RBNZ seems to want to support the housing market (as well as exporters) as the effect of a declining housing market will have a negative effect on the wider economy - people will be less likely to spend. Equally the RBNZ will not want to see rapid house inflation hence it will be controlling that through both the OCR and LVR - however 2 to 3% house inflation seems acceptable to them.

Property prices wont boom again during a recession.The unemployment rate will be increasing. That means more and more people will find it hard to find job. And there will be some people losing their jobs too.That will force people to sell theirs for more cashflow or to pay off their morgage. When more houses are on the market, but the demands are few. The will push housing price down.Yes, the interest rate will be low. But keep in mind that even it's hitting zero interest, you still need to pay off the morgage. Without sustainable income, there will be people couldn't afford to keep their houses. That being said, at the moment, we haven't got that stage yet. That's why the housing price is flat at the moment, people are still willing to invest into houses, thanks to the low interest. However, if lowering OCR can not stimulate our economy too much, unless if there is solution for this, we will continue to head down to that path. I dont think it was an actual recession for New Zealand during 2008 as back then we still have a huge OCR margin to drop. NZ economy can come back up pretty fast. But now with 1% OCR, who knows when there is a actually recession, how we gonna go through that?

FYI, here a similar chart up from 1970 to 2005. If in 2005, a chartist had extrapolated the price history at that point to determine their future price expectation, it most likely would have continued upwards.

http://www.doctorhousingbubble.com/wp-content/uploads/2009/09/1975-05_m…

{kind=link}

After 2005 it changed. That's how chartists can get caught out.

What is important are that the reported facts, irrespective of ones outlook can be relied upon,

"There were also very low numbers of properties that were withdrawn from sale or had their auction postponed, with just two postponements and two withdrawals during the week."

For the period 23-29 September Barfoots alone had 2 postponed and 4 withdrawn auctions

https://www.interest.co.nz/property/101928/sales-were-achieved-more-hal….

"The property clock"

Say. No. More.

A robust and well-reasoned argument cmat, well done.

I'm just struggling on where to start with "the property clock points to..." - it is such a robust & well-reasoned statement in of itself.

Tell me more about it:

- Where is it pointing right now? 1pm? What can I interpret from that?

- Does the clock only report in nominal terms?

- Does the property clock operate in a vacuum or is it correlated to something? Anything?... or just a metronomic clock, not influenced by anything other than its own rhythm?

- Is the property clock international or only set to the NZ time zone?

It's in the Church, and it's 3 o'clock. Remember, prices at 7 o'clock will be twice as high as at... uh... 0 o'clock (7am?).

My point is simply that the cycle exists - are you denying this? I can admit that gravity exists without an in-depth understanding of why it exists. Roughly 5 years from peak to trough, roughly 10 years from peak to peak. The Auckland market was at 12 o'clock in late 2017, previous 12 o'clock was mid 2007, mid 1996 before that.

12 o'clock in 2017 puts 6 o'clock something like 2021/22. NZ normally experiences a plateau or modest fall between peaks, not a crash. Yes, nominal terms. Doesn't operate in a vacuum, influenced by a million different market factors, who knows. Yes, NZ time zone ([UTC+12] Auckland, Wellington).

I just flipped a coin 4 times and it landed heads all 4 times. Based on this and no further information, I believe it is fair to conclude I will land heads every single time from now on, to the end of time, no matter how many times I flip the coin. I don't have an in-depth understanding of why that would be, but it is impossible to deny the pattern of something happening 4 times in a row.

If you think market trends are as random as a coin toss, I don't think there is any helping you. Failure to learn from the past is willful ignorance.

I thought the basis of your confidence was that it happened 4 times in a row? So what's the difference?

The main difference between market/economic patterns and a coin toss is that a coin toss is random, whereas market/economic patterns are not. Your coin analogy is an exceedingly poor one.

Market patterns absolutely have an element of randomness. The only reason you consider it predictable is that it happened 4 times in a row.

What I'm trying to highlight to you is that something happening 4 times in a row actually tells you nothing, because even something as purely random as a coin toss can happen 4 times in a row.

An element of randomness does not mean the economy and market patterns are as random as a coin toss. Your coin analogy is useless. And I didn't say it has only happened four times in a row, I just gave the dates of the last three years that the NZ housing market was at 12 o'clock. Go look at the historic data yourself.

Your stupid clock worked 4 times in a row, that's why you're using it. You didn't *say* that explicitly, but your clock works in 10-year cycles and you clearly only care about the last 40 years, so you don't need to say it, I can infer.

New Zealand property prices are affected by millions of factors outside of anyone's control - that is randomness. It doesn't matter if it's equally random to a coin toss. The point is that when things are random, what happened in the past doesn't matter. You can understand that for the coin toss, clearly, but for some reason it escapes you when it comes to property prices.

If you are simple enough to think that market patterns are just random fluctuations, I only hope that you entrust your finances to a competent adviser instead of taking it on yourself, as your acumen leaves much to be desired.

I didn't say it was *just* random fluctuations, DD. I think any financial adviser would gladly agree with me that "past performance doesn't guarantee future results". Apparently you don't, so I guess we can agree to disagree.

Hi Due Diligence,

With respect, I think the problem you're encountering in your dialogue with GGP is that GGP doesn't actually know what the words "random" and "analogy" mean.

Thus, I recommend that if you want to make progress with GGP, use only one-syllable words - such as "toss" and "coin".

TTP

Sound advice, cheers.

Excellent. A lesson on probability from a man who doesn't know the difference between "can't rule it out" and "every likelihood it will happen".

Hi GGP,

If you want to hang onto my every word (akin to a child hanging on to his/her mother's apron strings) then you're welcome to do so.

But most people understand the gist/thrust of my messages here perfectly well.

TTP

Maybe you can go by the gist/thrust of what I'm saying, instead of hanging on to my exact understanding of the word "analogy" and "random", akin to a child hanging on to his/her mother's apron strings.

Hi GGP,

With all due respect, you're mimicking me again.......

Time you learned to think for yourself.

TTP

I'm mocking, not mimicking. I know the spelling is similar, but they are different words. I suppose that can be hard to grasp when you're used to only understanding the thrust/gist of any given statement.

Hi GGP,

Some simple advice for you:

When you're in a hole, stop digging.

TTP

Don't worry, TTP's not the smartest brain around.

Hi Fritz,

Please note that it's not about being smart.......

It's about commonsense and good judgement - both of which yourself and GGP lack.

TTP

Did some ultimate auth hand down this celestial timer?

anyone with half an eye on global events can see its far from a no brainer.

"The property clock points to a upturn next year."

The recession clock points to a downturn next year.

Facts and realism are rational not negative

Ha ha. You guys are brilliant comedy value. Do you sit next to each other in the same quiet RE agency office?

So what were the figures for the same week in 2017 and 2018? Is it just the usual seasonal effect, or is it slower or faster than normal?

Scrolled down through Greg's old articles, found this one from about a year ago: https://www.interest.co.nz/property/96116/prices-ranged-595000-325-mill…

It's only about Barfoot auction results, but it looks like there weren't general auction result articles last year, or maybe another contributor wrote them if there were. Barfoot managed 57 sales in Auckland on that week last year. This week this year, there are 84 sold total, from all agencies. So unless Barfoot has 2/3 of the market, it looks like fewer properties were sold at auction compared to last year. Higher rate of success, but seemingly entirely just due to fewer properties being brought to auction.

I think we were at about 35% this time last year?

35% of how many that went up?

Im not sure, you could probably search 'auction sales' and page back to Oct 2018 and find out.

Couldn't look before, was working on site with a crappy connection. Search didn't show up an equivalent report for all the auctions Int.co.nz monitored, only a story on B&T auctions .. https://www.interest.co.nz/property/96116/prices-ranged-595000-325-mill…

So I searched int.co.nz database. Last week of September (24th to 30th) last year there were 109 sales from 294 auctions. And from what I can see, that sales figure only includes those that sold under the hammer or prior, not those that sold immediately after (No "Sold Post" entries) So not a significant increase in sales, likely the same or lower once you include the ones that probably sold post last year, just a huge decrease in the number going to auction. Evidence doesn't support "market taking off" as TTP is yet again trying to infer.

That is the strangest thing about these threads.

It's all a few of the same old folk insisting that equivocal statements of "can't be ruled out" actually meant "will take off", along with figures that have been declared to show that but actually show very little when broken out into their constituent parts. Prices that are down YoY are declared up, one of the three lowest September volumes (IIRC) in the last decade or so is declared to be the market taking off...While MikeKirk's breakdown of actual results suggests performance vs. CV wasn't great (see below).

September doesn't seem to be telling us a whole lot of much at all. At least not enough to declare that "can't be ruled out" actually was "will take off" and actually has been proven in any way.

Much ado about nothing.

Reality is, still low auction sale numbers in Auckland with those selling are having to sell at more realistic prices. Remember property will always sell if it at the right price. :)

Hi CJ099,

Notably, "the right price" is above RV in most cases - as reported by Greg Ninness today.

TTP

43% sold below RV, must have been a lot of pain for those vendors (says the DGMers with a glint in their eye and a lick of their lips).

Hi HeavyG,

Sorry - but that's absolute rubbish!

Given the magnitude of increase in house values over the last several decades, many of that 43% will have done mighty well.

HeavyG - you (and the other DGM minnows here) are wasting your time trying to pull the wool over people's eyes.

TTP

@ttp: It's in the above the million mark where prices start to struggle even for Auckland. And we're certainly not seem much selling in or above the multi million mark. Below the million mark - prices are a bit more stable due to much lower mortgage rates so people can borrow more.

RV in Auckland is 2 years old. You call 57% "most cases" - be careful with that, as it might trigger a voilent reaction in some National voters.

First page of successful auction results in Auckland gives a total of 21 properties where there is both a sales price and a CV. 12 were below CV and 9 above. Total CV was $21,885,000 and total sales price was $21,979,500. So in total, sales prices were $94,500 higher than CVs, meaning each house gained $4,500 in value on average.

Now, let's remove all the results that mention "renovation" or "weathertightness" in the ad. This removes 5 Glamorgan Drive, which was "newly renovated", 8 Intrepid Place, which was "tastefully modernised", 99 Queen Street, which was "exceptionally renovated", 151 Arran Road, which had a "Stunning makeover", 2 Matangi Road, which had a "fully renovated" bathroom, and 3 Whitaker Place, which has weathertightness issues. 6 properties were removed, leaving us with 15.

Now the total sales price comes to $15,906,000, and the total CVs comes to $16,410,000. That is, CVs were, in total, $500,000 higher than sales prices, meaning each property on average lost about $30,000.

Neat analysis, ive often thought renovations are accidentally part of the long term historical growth estimate as well.

nice.

Don't let rational and intelligent analysis get in the way of the Spruiker Narrative!

Good analysis GGP. And yes the an average value lost of about $30,000, sounds about right. Even more interesting when auctions are meant to fetch the best price. Sill REA's could help Sellers by reducing the commission rates, that will give them more price wiggle room. :)

So all the houses that sold were purchased by the vendors at their current CV amount. Amazing!

Just to get it straight (1) Majority of houses selling below CV is a loss (2) Majority of houses selling above CV is a loss. You're right, the spruikers are damned either way.

"So all the houses that sold were purchased by the vendors at their current CV amount. Amazing!"

Who said that??

"Just to get it straight (1) Majority of houses selling below CV is a loss (2) Majority of houses selling above CV is a loss. You're right, the spruikers are damned either way."

Who said that??

Good analysis.

I note that a report Barfoot put out yesterday with all the sales in my area.

They went to the trouble of putting "n/a" for the CV of any property with weathertightness issues but failed to do the same, or disclose, that a property had been renovated.

This is one area where the property industry is highly misleading.

Often, once a property sell, the listing will become non-discoverable too (you can't even search it on TradeMe) - so there is no way of knowing if it was a renovated property.

Then in comparable sales analysis they'll include all the renovated properties in the area to show SP/CV multiple uplift.

https://issuu.com/barfootsuburbsales/docs/st_heliers_kohi_mag_template_…

Even then, they report on page 5 that the median sale price was almost $200,000 lower than the median CV. And that they sold 20% fewer properties than last year. Better not call that a "loss", though, as that might upset HeavyG.

Yeah exactly right - *even then*, the stats on the first couple of pages tell a sad tale for a 'premium' area of Auckland.

Mary brought her home in West Auckland in 2008 for $350,000, in 2017 the house was assessed a rateable value of $950,000, in September 2019 Mary sold her house for $900,000 making a $50,000 loss.

This is what you guys sound like.

It's almost like we're talking about how the price has moved the last 2 years, rather than the last 10 years.

I think we can all agree the price has gone up in the last 10 years. Does that satisfy you?

A bit too petulant for my liking, try again.

Not just the last 10 years. NZ house prices have gone up in nominal terms every 10 years since records began in 1963. But that's mostly just coincidence based on random chance, so it doesn't really tell us anything at all about what prices are likely to do in the future. We need not pay attention to that data - the next 10 years could just as likely "be different" [sarcasm] .

I think prices are likely to go up in the future, especially on nominal terms and especially on a long enough timeline. Not because it happened in the past but because the population is increasing and we are still very slow at building new houses, plus inflation will always keep pushing it up if we're just looking at nominal values.

What happened in the past is a reflection of the above. It is not *itself* an indicator of what will happen in the future.

Nope.

I'm not looking backwards. Mary made money. Good for Mary.

I'm looking at how you assess value in the market *NOW*.

In an up-market Real Estate agents are all too happy to use SP/CV to determine value - and when I say determine, I mean the recent high watermark is referenced ad nauseum as a peg for market value.

How often did we hear "prices are trading at x% above CV in x suburb".

Now we have a lot of obfuscation around that metric.

If houses were trading at 1.1x CV 3 years ago and now it's 0.90x then that is a material change.

Obviously no one want to quote the low water mark.

And no one wants to be honest about where the average lies - They'll include renos to manipulate the avg/median.

Don't get me wrong, it's always been a terrible metric, but it's the only thing we have - and if it was good for the goose in an up-market then its good for the gander in a slow market.

Indeed. Most stuff on Hibiscus Coast is selling 3-7% below asking price. Most stuff is orig put on market above CV. Which is not a good procedure to follow when assessing market price in current environment

By saying houses are trading at 1.1xCV versus 0.90xCV do you mean if CV had been $100k and the HPI/Median (whatever you are using for "trading at") was $110k and 3 later is $90k? Why wouldn't you just say that e.g. the HPI dropped from $110k to $90k over 3 years? Why would the CV matter?

The discussion above used CV as the measurement and then did some cherry picking to produce an average price below the CV followed by a Eureka! Sellers have made a loss. Pointless exercise with zero value.

And the best argument you come it with is "real estate agents do the same dumb shit so why can't we?...". SMH

Nobody was saying sellers made a loss. We're just looking at whether the market is going up or down since 2017, when the CVs were decided.

Because HPI is only reported at a Ward level, which is often a very large area comprising disparate suburbs.

It's obviously a great metric, the best by a long way, but hard to apply to individual properties.

I'm not saying sellers make a 'loss' - I'm saying prices have pulled back from where they were 3 years ago, some more than others.

If some Vendor says their particular property is worth $2.5m and it hasn't been on the market for 25 years then how am I, as a potential purchaser, expected to objectively assess that as reasonable fair value???

How can I apply HPI to arrive at fair value for that particular property?

How would *you* apply HPI to arrive at fair value if *you* were a purchaser???

No one had an issue with parroting CV ratios 3 years ago - why have you got such a problem with it now?

Or am I just supposed to roll over and pay $2.5m because $2.5m is what they're asking and the property clock and 10 year cycles and lower interest rates and whatever... so it must be worth $2.5m??

Seems to be a little spruiky news going on. Remember nothing falls in a straight line.

What about a brick? That falls in a straight line.

And then it hits rock bottom ? Boom boom.

Well I’m surprised!

I fail to see how you can describe a “market” as buoyant when Auckland new listings are 22% down on last September. I also note you do not state how many were auctioned in equivalent week of last year.

Barfoots sale rise was accounted for by more apartment sales in City Centre. Finally, in order to compare two sets of figures one needs to be informed of denominator. That is, the total stock and % of that which was put up for sale and then what proportion of that sold. As stock is rising fast in Auckland it is not fair nor accurate to compare sales without laying out the numbers requested herein.. for instance we are told stock added in Auckland is about 12000 pa for last year. But this is ignored when making sales statements and opinions on those sales totals.

It would be nice if a contributor could please identify the elements needed to show a healthy market v a poor market. Listings, sales , price might well be minimum requirements? NOT price alone. On that score 2019 shows listings and sales at 2017 levels and prices at 2016 level. Buoyant?

It's pretty simple. Above 50% auction clearance rates = bouyant market. Below 50% auction clearance rates = rainy week.

MikeKirk, are you still a real estate agent?

Pretty boring.

Are you a robot

What is boring about asking if you are still a real estate agent, as you said you were before?

Why can you not answer the question?

The reason is MikeKirk, is that you are not an agent at all!

No agent in NZ would have a viewpoint like you do!!!!!

Takes all of 30 seconds on Google to see that he is still a real estate agent.

So, is Mike Kirk an agent, currently?

Question hasn’t been answered by anyone.

Says there is an agent that was with First National but doesn’t appear that he is currently a real estate agent, unless you can say otherwise?

With his attitude to real estate you can see why he is no longer one!!!

https://telosgroup.co.nz/team/mike-kirk/

Whether or not it's the same Mike Kirk I can't say, but seems like it matches.

Correct my friend.

Nice to see someone has capability in research method.

Some parties seem to assume that all of a profession think the same, speak the same and behave the same.

pretty limited perspective.

Look on linked in and see my work experience.

Political economy is in my blood.

Check the register.

Also, it is not attitude to RE, it is attitude to FACTS and objectivity v convenient thinking and seeing things as they are, not as one might wish them to be. You do not seem to be able to counter anything I present with what might approach an argument based on facts.

You begin to sound like Trump and his "birther" trope on Obama.

Mike Kirk you may well have tried being an agent for Telos Group First National, but you clearly are not any longer!

You are not showing as an agent for the Telos Group!

for some reason now you are bitter and twisted about property.

No real estate agent in Auckland would speak the way you do!!

No real estate agent in Auckland would speak the way you do!!

You may be right there...in one narrow sense. Mike Kirk seems to be providing quantitative and qualitative analysis of sales number and what houses are selling. Agents don't seem to typically provide that level of robust analysis.

I had an agent try to tell me that "lots more apartment developments are going on right now, so the apartment market is really poised for strong capital gains", as one example.

https://i.imgur.com/oxgbrOQ.png

{kind=link}

Hope this helps tm2

What date was that GGP?

He clearly was with the Telos Group at Silverdale according to his registration this year!!!!

He no longer is an agent with them, according to their website.

I can understand why he is no longer an agent, as no agent that talks the way he does would be engaged with any worthwhile real estate firm.

No half sensible vendor would ever engage his services with the way he presents!

I took that screenshot right before I posted it. He's still on there right now. I don't really know what else to do to help you out here. Maybe get new glasses? Read the list slower?

Bollacks.

Read who the sales agents are at Telos Group And he is not down as a current sales person!!!!!

No Mike Kirk there now!!!

Read the current information available GGP!!!

GGP you say he is a salesperson at Telos Group, please provide evidence that he is selling properties with property references etc.!!!!!!

Funny that Mr Kirk has not responded by saying that he is still employed as an agent with Telos Group, because he clearly isn’t!!

https://telosgroup.co.nz/team/mike-kirk/

What do you see on this page?

GGP, geez, he had a ticket with them, but clearly he is no longer selling for them.

That is an old article when he was there!!!!

Which part of Mike Kirk no longer sells real estate for Telos Group don’t you understand?

He is now not a salesperson with Telos, he clearly has left them and is now a bitter ex agent!!!!

Thanks GGP.

But clearly it's not worth wasting good seed on barren pasture as far as he is concerned.

How is it possible to be, as he puts it "bitter and twisted" re property? It is an inanimate object.

Not bothering to respond further to him.

I was door knocking for 3 hours last Sunday in Stanmore Bay.

Which I did for good of my health of course

dp

Mike, so you are saying that you are still selling real estate for Telos Group?

If you are why are you not down as being a salesperson for them on their website??

Can you please give us a reference to your current listings please, because I believe you are having us on about being a current real estate agent?

You door knock on a Sunday afternoon looking for listings?

You are having us all on Mike!!!

Simple solution. On Monday, call up the Telos Office and ask to speak to Mike Kirk. We shall see what they say and see if this conspiracy of Mike Kirk being one of their agents goes all the way to the top. Their number is here: https://telosgroup.co.nz/contact/

GGP, Mike Kirk is clearly not an agent with Telos Group anymore, or he would have his profile on their website.

Yes he was with them but for some reason he no longer is and for him to claim that he is a current agent with them is a lie!

Note that he has not confirmed that he is still with them.

He needs to come clean and state that he is no longer a real estate agent but a former failed one!

He did confirm he's with them earlier up in the comment chain? Like I said, all you have to do is call on Monday and see what happens.

Think Mike should take that as a complement.

"It would be nice if a contributor could please identify the elements needed to show a healthy market v a poor market"

Here's a market indicator of a buyers market vs sellers market.

Wow...days to sell in Auckland look "buoyant". Definitely an upward trend line there.

For the Auckland market - since June 2018, each month has recorded the highest number of "days to sell" for that respective month compared to the same month each year since the GFC in 2009.

I'm hearing of property vendors who have been unable to sell their property after a period and taking it off the market to relist with another agent. I believe that this effectively resets the starting date of days to sell.

In a downward price market, vendors are slow to lower their price expectations, so are unwilling to accept lower prices from buyers. Hence the longer days to sell.

A vendor signs up for a 3 month commitment with an agent, (however this may now be more negotiable given current market conditions). If a vendor sells before this period expires, then the vendor may be subject to paying 2 sets of commissions - one to the first agent, and another to the second agent. Not sure what happens when you change agents within the same firm such as Barfoot and Thompson. Other firms are franchise businesses.

Look at this newly completed apartment - its been listed for sale since December (that's about 9-10 months)

If a vendor takes his property off the market prior to the 90 days, he can not relist with another another agent within that 90 day or listing period.

The vendor would be pretty dumb to do this unless he has an agreement from the first agent releasing them from the listing which would be pretty rare, and why would they.

Should the buyer be introduced to the property by the first agent and contract signed up by the 2nd agent, then a second commission is also likely to have to be paid.

A listing contract is a contract and vendors need to be very careful what they do when listing their property for sale.

Yes. And sales trend shows lower for 3 m than 7m when comparing to 2018, for most areas although apartment sales improved in this measure last 2 m

Prediction: other than Auckland City and Waitakere City sales in Sept 19 will be virtually identical to Sept 17.

Auckland residential sales in Sept 17 were 1706.

Albany Ward were 188

Rodney were 178

NSC were 311

Auckland City were 526 (apartment sales improvement means these will be up )

Waitakere City were 299 (these will rise quite a bit = FHB)

I will revisit when REINZ announce the results next week

Prices go down, sales go up. People are shocked. More at 11.

GGP, Mike Kirk did not confirm that he was still with Telos Group.

He said check the register.

It shows that Mike Kirk registered with Telos Group as an agent in March and it will lapse if he doesn’t renew his license next March.

Mike Kirk is not a practicing agent with Telos Group at the moment at all, so is an ex.

Agent.

No successful agent would ever have a mindset to real estate that he has.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.