By Greg Ninness

Continuing interest rate falls mean mortgage payments remain affordable for typical first home buyers, even though house prices remain at or near their all time highs, according to interest.co.nz's Home Loan Affordability Reports.

The reports show that the average of the two year fixed mortgage rates charged by the major banks dropped to 2.72% in July after falling for six consecutive months.

Twelve months earlier in July 2019 the average two year fixed rate was 3.81%. And two years ago, in July 2018, it was 4.46%.

That has kept mortgage payments affordable even though the Real Estate Institute of New Zealand's national lower quartile dwelling price has risen from $377,707 in July 2018 to $401,900 in July 2019, and on to $476,000 in July 2020.

So far this year the national lower quartile price peaked at $480,000 in March, dropped back in April and May before climbing back up over June and July to be almost back to its March peak.

Around the country the regional lower quartile prices have more or less followed the same trend and only two regions, Manawatu/Whanganui and Otago, recorded a drop in their lower quartile prices in July compared to June. Three regions, Hawke's Bay, Taranaki and Canterbury, were at record or record equalling highs in their lower quartile prices in July

So overall, prices at the bottom end of the market remain at or near their recent highs, while mortgage interest rates are at record lows.

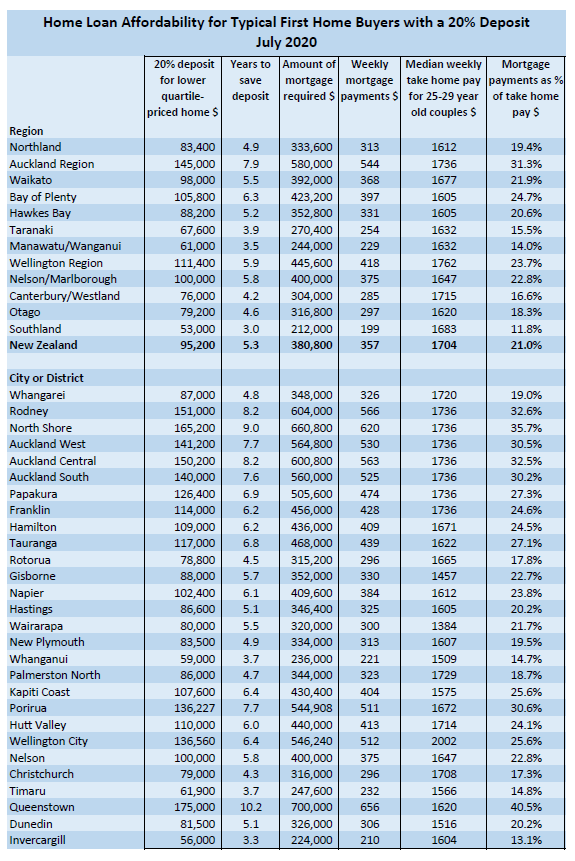

While there are big regional variations in lower quartile prices, which ranged from $725,000 in Auckland to $265,000 in Southland in July, the historically low interest rates are keeping mortgage payments affordable for typical first home buyers in all regions.

With a 20% deposit and a 30 year mortgage at the average two year fixed interest rate, the mortgage payments on a lower quartile-price home would range from about $544 a week in Auckland to $199 in Southland.

If a couple were both working full time at the median rate of pay for 25-29 year olds in their region, those mortgage payments would take up less than a third (31.3%) of their after-tax pay in Auckland and just 11.8% of their after-tax pay in Southland.

Using the same calculations, mortgage payments would take up less than a quarter of take home pay in all regions outside Auckland.

As a rule of thumb, mortgage payments are only considered unaffordable if they take up more than 40% of take home pay, so by that measure, all mortgage payments on lower quartile-priced homes are well within affordable territory for typical first home buyers in all regions of the country.

However with prices so high, scraping together a deposit will remain a challenge for many.

The 20% deposits at July's lower quartile prices ranged from $53,000 in Southland to $145,000 in Auckland.

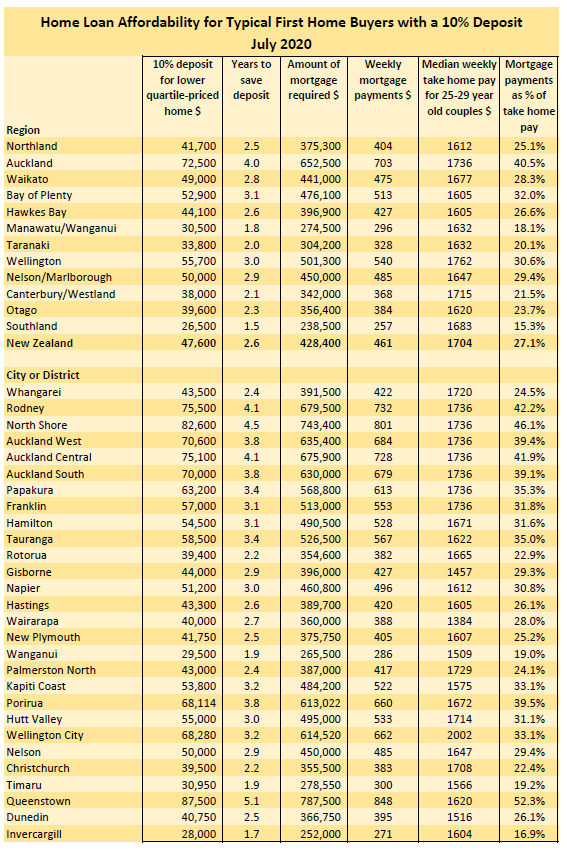

Even 10% deposits would likely be stretch for many people in the higher-priced regions such as Auckland ($72,500), Waikato ($49,000), Bay of Plenty ($52,900), Wellington ($55,700) and Nelson/Marlborough ($50,000).

But interest rates are so low currently that mortgage payments would remain affordable even for typical first home buyers with just a 10% deposit.

With a 10% deposit the mortgage payments on a lower quartile-priced home would remain under a third of after tax pay for typical first home buyers in all regions of the country except Auckland.

Even in Auckland, the mortgage payments would only just cross the threshold into unaffordable territory at 40.5% of take home pay, which would mean household budgets would be starting to get tight for typical first home buyers but they would probably still be manageable.

So it's probably little wonder that first home buyers, many of whom have likely been saving for several years to get a deposit together, are continuing to take the plunge into the housing market, even though economic uncertainties abound in these COVID-troubled times.

The tables below show the main measures of affordability for typical first home buyers throughout the country, and the differences with 10% or 20% deposits.

The comment stream on this story is now closed.

Note: The years to save a deposit figure is based on saving 20% of after-tax pay each week.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

174 Comments

Affordable used to refer to 30% of one earners pay. Now we are told it “is considered “ to be ( by those with an interest in it being this defined of course) as 40% of two earners.

Exactly, since mortgages became unaffordable for most years ago it seems the solution has been to change the meaning of the words we use instead of highlighting the issue.

The language around housing is interesting these days terms like - Housing Ladder (one needs to climb this apparently) --- The banks and realtors marketing departments should be high fiving each other, all the way to the bank.

Sluggy

The term "housing ladder" from my experience has been around and often used for over 50 years.

It is how boomers got to where they are today.

Boomers from RBNZ and Govt will never fight the rest of the boomers, as simple as that.

They got to where they are by purchasing more houses than they could live in. The boomer generation is the property investment generation. I always find it disappointing that my grandfathers generation went to war to fight for and protect the freedom and liberty of our people but the boomer generation then used that freedom to go to war with the next generation in the auction rooms around the country to deprive them of the freedom of owning their own homes. That‘s how we got to where we are today with a little help from your central banker friends perpetuating the unproductive wealth transfer and depriving markets of true freedom. A team of 5 million?, I think not.

Well said. Where is the continued deepening of this rift going to take us? Do they think we're immune from revolution here in New Zealand? This does not even appear to be a consideration.

Depriving future generations a chance at affording home ownership by crowding the market, and then claim to be the saints that provide a roof over their heads because of aforementioned housing affordability (lack of).

And doing so off the back of affordable houses provided to them through the efforts of the preceding post-war generations. Living off the wealth of both preceding and succeeding generations. Destroying the host.

Houses are for nesting; not investing.

No wonder the New Zealand native birthrate is below the level needed to sustain (let alone grow the population) and our leaders feel the need to bring in our replacements to make up the shortfall.

We have only ourselves to blame for electing such leaders.

Agree, they got everyone where we are today.

Yep. If you want to participate you have to shack with up (permanently) with someone who is also earning reasonable money... but not have any interest in children, which will inevitable remove half that capacity for at least a year. God forbid you fall out of love, lose a job, get pregnant, or have to care for a family member... All extremely rare events, of course, that tip that 40% of household income to 80%.

The traditional affordability threshold was a third of pre-tax income. The trouble with that measure is that tax rates can move up or down, increasing or decreasing the amount of cash households have to play with, making a mortgage more or less affordable, but those changes aren't reflected in a pre-tax measure. Which is why interest.co.nz has always used the 40% of after-tax income as the threshold for affordability, since the beginning of the Home Loan Affordability series.

With all due respect 40% is too high.

Singles / couples without children may be able to cope with that but once you have kids that's exceedingly high for many...

When I worked in a bank in the UK Back in the late 1980’s the maximum mortgage you could get was 2.5 times income. London had a separate rating up to 4 x salary. So much more realistic and you could actually pay it off much earlier too.

Which is a fair enough adjustment, but it still doesn't make the measure realistic overall.

I also question the logic of using a *median* income and a *lower quartile* home. I realise it's probably to account for expected wage increases over the course of a career, but I think that expectation might not be realistic in the present day, with wage inflation almost dead.

Household income might I add, which these days the figure consists of twice as many working hours.

I've often read the advice that the limit of affordability was "35% of pre-tax income housing costs" i.e. mortgage, rates and insurance.

Thank you for the clarification Greg, but by any means 40% of after-tax income can be considered affordable. If you really think about it most households bring home two salaries, which are (unfortunately) not usually balanced, if let's say the person earning 40% finds itself unemployed (which in the current environment is not a long shot) that 40% becomes all of the sudden 66.7%, if it is the other way around the mortgage would turn into 100% of the income and become un-serviceable.

I don't know if you've read Elizabeth Warren's 'The Two income Trap' but she makes two points which are relevant here - households in general have not been made better off because more of them have two incomes - it's just bid up the cost of things like accommodation. Also, if your household needs both incomes to pay basic expenses, you double your chances of getting into trouble (as if either one of you loses a job you're screwed, and the other person can't go get a job to help pick up the slack because they already have a job).

Having the fairer sex enter the labour market in the last 60 years has in effect halved labours value vs capital?

And when it stopped being affordable at 25 years, we pushed the goalposts to 30 years.

Rather than addressing the affordability problem and admitting that housing is not only about "ma and pa investor" portfolios.

the country is methodically pushed the way 3rd world went in 90s , With time only "ma and pa" will be able to help their kids to buy a home in 10 years or so , but they don't care, everything is looking great in their eyes. IF something is happening you don't like , there will be always covid/lockdown/canabis/ flag change/etc topics raised in the news so that you have something else to worry about

"If a couple were both working full time at the median rate of pay for 25-29 year olds in their region, those mortgage payments would take up less than a third (31.3%) of their after-tax pay in Auckland and just 11.8% of their after-tax pay in Southland"

The key point here is that in the majority of cases two full-time incomes are required to service the loan in Auckland without untoward mortgage stress. Based on the recent number of deferrals/interest only applications, many are currenly in this delemma. My brother (cop) and wife (hotel manager) find themselves in this position when my brother's wife had her hours cut by 60% with a $600k mortage still to pay.

"If a couple were both working full time at the median rate of pay"

That's going to be a b##dy big IF!

It was harder in the 70's and 80's! We even had to work on Saturdays to 12, just got to pub before the All Blacks test at 2.30. Lovely wife used to have a roast cooking when we staggered home.

...yeah they gave up the right to be queen of the home to become a slaves to the workforce. It was a great partnership for 90% of relationships (and their kids).

Look at the mental lifestyle of a couple now!

So true..some comments on the lock down was relief as the first time people hard a chance to stop and look at "modern" life and go WTF? Also spenders of time with their partner..

And a lot of people saying either "My kids are great, it's insane I don't spend more time with them"... or alternatively, "I didn't realise they were such little s**ts, their poor teacher"... I've actually heard both.

Rastus I agree with you. I always found the feminist zeal to become a 9-5 corporate drone perplexing, I was more than happy to trade with my wife but she wasn't having a bar of it. Of course this was going to support higher house prices rather than an increase in disposable income. To all the newly empowered female corporate leaders reading, enjoy the stress, missing your kids key life events, work travel, narcissistic managers and end of year reviews - I'm off to F45 and then lunch with the boys!

Nonsense. You come across as blaming women for this. Most people don't want to become drones, or deal with any of the negatives you mention. They want freedom to choose to work, to be equally involved and represented in the decision making, to contribute to society and to have the same economic advantages and possibilities that men are afforded in the workplace. Without this as an option, they have almost no prospect of having this same independence and freedom of choice in the course of their life. They should be able to have this on their own, and not be entirely dependent on their husband for economic security etc. One income should be enough, giving both partners the choice to have more time for their family. Women seeking to have this same independence, is not to blame for our current situation in which two incomes are needed to service massive debt. It should not have to be one or the other. We should perfectly well be able to have the same independence afforded to both men and women, alongside one income being able to support a family.

The world has moved on. If your family unit cannot financially compete with other more cohesive and productive family units, you're fresh outta luck.

yes but inflation eroded the debt. Not any more

Covid is destroying incomes. It's great mortgage rates are lower but if you have already had or expect wage cuts or job losses this isnt going to help.

You're only telling part of the story. Covid destroying incomes also means that people don't reach for that 'nice to have' product at the supermarket. Did you ever think about how many trade-up, added value FMCG products there are in a typical NZ supermarket? To give you some perspective, the assortments are greater than in a country like Japan.

Now why is this relevant? All those 'nice to haves' actually sell quite well when there is a healthy economy, particularly a credit-driven, asset bubble economy. Times like this, it's a different story. There are only a few scenarios here: revenues and margins fall and incomes and employment fall. Many of the businesses that support the 'nice to have' part of the economy are already running close to the bone. There are mortgages, houses behind these businesses too.

You should get the idea that the bubble economy feeds off itself. Now when you're faced with the situation that we have now, the negative feedback loop kicks into gear. Many NZers are not really aware of this yet.

People are not reproducing because house prices are too high to raise a family and both adults have to work. Do the specuvestors really hate NZ or does their greed simply outway any moral compass they perhaps once had?

#1 reason we've decided not to have kids.

Same, we just can't afford to have one person not working.

And over time this would stabilise things, except we go and import our population growth instead.

Got to keep wages low and New Zealanders out of those job opportunities.

I don't blame the specuvestors, as greedy as many of them are.

I blame successive governments for totally failing to address the issue in any meaningful way. Hopeless.

Aren't most govts representative of those specuvestors?

The majority of home owners are specuvestors?

They try but the specuvestors shriek hysterically every time solutions are proposed. Then they back off.

Meanwhile the wages of the young are taken to fund the retirement of specuvestors even while housing is turned from a means of stability in NZ society into specuvestors' money tree.

But who voted them in, year after year?

I lot of the adult population (60-70% plus) either own homes or are on state housing. When the maths is stacked way there's little hope.

I think the specuvestors love NZ because the RBNZ and the banks allow them to be as greedy as they like with no real consequences if the s..t hits the fan.

Whatever one thinks is an "affordable" level, as long as potential FHB have required deposit, have security of income and job, are able to meet the bank's lending requirements, are confident that they can service the mortgage, and have a house in mind they have little to fear.

RBNZ statements regarding the likely future of the OCR suggests that next year that mortgage rates are likely to be lower so those fixing for a year payments are possibly likely to be lower.

As there is always a degree of uncertainty in life, they need to be prudent and start look to pay that mortgage down as soon as possible.

RBNZ figures show that FHB are currently active in recent months. In the last three years 79,305 mortgages have been granted to FHB - that about 145,000 FHBs.

RBNZ figures show that FHB are currently active in recent months. In the last three years 79,305 mortgages have been granted to FHB - that about 145,000 FHBs.

Yes. Many of these people buyers will have been thrown into a kind of financial battle through no fault of their own. What they thought was a 'prudent' and socially inclusive decision to buy a house may end up causing them endless misery.

J.C.

' . . . to buy a house may end up causing them endless misery."

It seems that 145,000 FHB disagree with you.

It seems that 145,000 FHB disagree with you.

Really? Do you call each of them to check on how they're feeling?

J.C LOL very good comeback

Many of these FHB probably had the choice of paying 2/3rds of a single wage earners pay packet on rent, or 2/3rds on a mortgage with additional thrown at rates and insurance for the premium of "secure tenure". Congratulations to them.

That's a hell of a lot of prerequsites you list there P8

Albert

Same criteria I used over 40 years ago. Some things don't change.

As there is always a degree of uncertainty in life, they need to be prudent and start look to pay that mortgage down as soon as possible.

Prudence is a quality missing from much of the housing market. My mortgage broker said there is a rapidly rising trend of couples who are hell-bent on buying houses to the full extent of their creditworthiness. Those earning median incomes wish to live in bigger homes overlooking the bay and the financial system is here to take full advantage of this greed.

By doing away with LVR requirements, I wonder if RBNZ has stimulated subprime lending in NZ.

Lot of 'if's' in that first paragraph mate!

A large number of very big ifs.

Of course it's safe to borrow if you have a large, bulletproof income and don't borrow too much! A tautology.

The point is how few people that actually applies to.

Given this article appears to be a followup to last weeks, as I wrote last week , a 25-29 year old couple in similar circumstance , who rented the ten years from June 2010 thru June 2020, the first five year period sharing, having invested the equivalent housing deposit equally in bank deposits and a New Zealand growth fund, would have been financially better off than those who chose to purchase their first home in June 2010, whether with a ten or twenty percent deposit.

Given this article appears to be a followup to last weeks, as I wrote last week , a 25-29 year old couple in similar circumstance , who rented the ten years from June 2010 thru June 2020, the first five year period sharing, having invested the equivalent housing deposit equally in bank deposits and a New Zealand growth fund, would have been financially better off than those who chose to purchase their first home in June 2010, whether with a ten or twenty percent deposit.

Doesn't surprise me. They probably would have been better off renting and investing everything into the Smartshares FNZ (Top 50) ETF.

The Auckland house price index (from Interest.co) has doubled in Auckland over the last 10y. With a 20% deposit, that is a 500% ROE - can you explain to me how some term deposits and an NZ growth fund get to be an annual ROE of 50%??? (uncompounded).

With a 20% deposit, that is a 500% ROE

Meh. Furphy.

If you disagree, counter. An emoji has more substance than your reply.

My reply is to illustrate the laziness of the idea of an ROE of 500% based on a house deposit and an index.

In the context of Cowpats illustration, it is entirely appropriate. How is it it lazy, do you dispute the calculation? There will be many real world examples that show this is probably conservative.

Or is failing to accept this some form of coping mechanism for you?

OK Te Kooti. You have at your disposal on this website .

1/The median national lower quartile home June 2010 thru June 2020, as illustrated last week

2/A mortgage repayment milestone calculator, 25 years , using the most common fixed rate, the 2 year ( if you want , go variable). You have historical average mortgage rates whether they applied to our FHB is mute.

3/Bank deposits, similarly on 2 years , taxed for our rental couple.

4/National rents 2010-20120 , our couple prefer a 3 bed home shared for the first five followed by a 2 bed, go it alone . They prefer the median national rent, as opposed to lower quartile. Their rent of course is increased each year..

4/.Stats NZ will provide you with household rates/insurance weekly or annually .(Insurance of course varies tremendously) Stats NZ also provide general maintenance costs. (Our home owners, never had to re roof or undertake any substantial repairs, that's too much of a banana ) If you want throw in an acceptable weekly number.

5/ Fisher funds or similar will provide you a chart/history for a basic New Zealand based growth fund. ( our rental couple did not buy Apple/Tesla shares) ( I used Fisher as it popped up on the site)

6/ The difference between rents/ mortgage is invested, again fifty percent in bank deposit/ 50 percent share/investment fund. To make it interesting, an international growth fund.

7/ Our home owners enjoy the value of the increase of their first lower quartile home,their principal repayment and retain of course their deposit (although I am a little short of Mr Ninnes's calculation ) and on moving up the ladder would they be better off in financial terms than the rental couple, all other things being equal.

Let's simplify it - I will give you $10k per annum for rates, insurance, maintenance etc on a a $1m house over 10 years

A) $200k House deposit ($1m house), $100k additional expenses = $900k profit at T+10y

B) $200k Invested - $100k Fisher Funds (400% growth) = $400k and $100k term deposit (10y compounded) = $100k So $500k

I will concede that the Fisher Funds has done very well, but still it is $900k vs $500k, you get to live in your own house and not move (worth a lot). The trick here is the leverage of course.

You appear to have forgotten, in your simplified study 1. The principal paid by home owner during those 10 years , which now reverts to rental couple,and 2/ the difference between mortgage interest on 800K and rent, reinvested .3/ Yes a home owner gets to stay in their 'own' home, paint the fence, mow the grass ,put a light bulb in, rental couple enjoys time to do other things, and moves if neighbours play music too loud. 3/.If its 10K for rates insurance/maintenance, the difference becomes very large .

I don't follow your logic in 1. If the mortgage is p&i then there will be additional savings by owner occupiers. I don't believe a house is cheaper to rent than an interest only loan. 2. is the same as one - a mortgage is higher due to paying off debt which is savings. 3. I included in my numbers, I took $100k out of the end sale.

Fisher Funds has performed better than house prices and would easily win but for the leverage, but that's always been the trade with housing.

The goalposts seem to be changing. In June 2010 you purchase 1 million dollar home with 200000 deposit, a 2 year fixed repayment mortgage at 7.19 percent. In the first 2 years your repayments are $68,912 each year. After 2 years (3.08 percent of the principal has been dealt with) Rental couple share median Auckland 3 bed at 460 per week, their annual rent outgoings Y1 $11960 and Y2 $12870 In the first two years the difference is $112,994, which they have reinvested in further bank deposits and an investment fund. At Y3, mortgage now 5.5 percent and so forth

Xero shares 10 years ago $6....now $101...but hey some here said it was only accounting software that anyone could copy.

Tesla up nearly that much in scarcely over a year. The "new normal" is a strange beast.

That's great Cowpat. It just goes to show that buying a house is not the only game in town. There are alternatives that can be quite lucrative.

Zachary, always alternatives. Cheers.

Except we kept that cash ready for a house purchase and our parents kept telling us a fundamental rule is to only invest in the sharemarket after buying a house.

A 30 year mortgage is nuts, mine was always a 15 year plan. You want to be aiming for 20 to 25 max, the extra weekly amount of a few dollars slashes years off your mortgage.The low interest rates now allow you to smash it, or is it now the low rates that are the problem ? people cannot be bothered to pay it off. I used to be on 8.6% and you sure want to pay that off as fast as possible.

I agree. At the time of getting our mortgage sorted, the bank gave us the required fortnightly payment but we had enough spare left over each pay to make additional principal payments and chose to do so. As it sits now, we've cut our 30 year term down to 24 years and set to re-fix our interest rate in October at 1%~ less than it is at the moment. Thinking we might even add more to our fortnightly payments to further pay off our debt.

Just because the mortgage is nominally structured for 30 years doesn't mean you take anywhere near that long to pay it off. Ours was structured for 25 or 30 but will be gone in about 10. But you might as well keep the mandatory repayments low, just in case.

Our employment is secure for the medium term and we do also put cash away to have on hand, but yes you raise a valuable point that is often overlooked when trying to reduce debt.

Why not keep it at 30 years and put your extra savings into an investment that earns more than 2.5%?

Tax treatment makes this harder to pull off. e.g. the 2.5% that you're "earning" by paying off the debt is after tax, and risk free. (Well, beyond the risk you already took in the purchase).

Takes a modicum of financial literacy to think like this

Unfortunately, not all that common around here to understand WACC

I want a jetboat this summer being the priority investment currently. Whats your alternative suggestion for a 2.5%+ investment?

Bitcoin

How? I always ask for advice here from those in the know but never get any guidance? What wallet to use, how to buy etc.

Buy a Ledger Nano X (online, directly from ledger.com) as a cold wallet (offline storage). Takes a while to arrive. Buy crypto from https://easycrypto.ai/nz/ -- can be direct debited straight from your bank a/c. That's what I did anyway. Pretty painless. Start with a small amount to test it before doing a bigger chunk .

Thanks mate definitely going to look at this tonight.

Hardware wallets are definitely the way to go (Ledger). If you want to play around with the technology a bit for fun you can get something like “pillar” app on your phone for free. Same principle as ledgers you will be given a backup phrase to write down in case you lose your phone. You’ll be able to see receiving address etc. Just a good introduction into the technology. BitPrime is not to bad for buying in NZ.

Yea I've signed up to bitprime so once I've sorted a wallet i'll look there also. Appreciate the feedback

I reckon there's a reasonable chance the jetboat would turn out to be a better "investment"!

Are you saying it's wise to bet against technology?. What stocks are driving the stock market now?.

Got to have a diverse portfolio. At least a boat is a tangible, physical asset I guess

Sorry, I just noticed Pillar haven’t integrated a bitcoin yet (coming soon). Looks like just Ethereum and Ethereum based tokens at the moment.

Buy a Ledger Nano X (online, directly from ledger.com) as a cold wallet (offline storage). Takes a while to arrive. Buy crypto from https://easycrypto.ai/nz/ -- can be direct debited straight from your bank a/c.

Don't mess up your recovery phrase with nano. I have before. Frightening experience. Janine from easycrypto had an interview on TV with Duncan Garner. Waste of time really. I don't use easycrypto and I'd imagine the volume in a country like NZ is low.

What setup do you use JC for bitcoin?

I buy Bitcoin through Japanese exchange Bitbank. I also use Independent Reserve in Australia, but ony for onboarding.

Yep, well I'd definitely take others' advice over mine. I'm a noob and feeling my way. Re easycrypto, I appreciated being able to speak to someone on the phone -- spoke to Janine. She was fine. I know I can sell through them. KYC was very easy. I've been careful with the recovery phrases. Hope that's all OK. Purchase-wise I've just stuck to Bitcoin, Etherium and Cardano. De-Fi seems great, but I'm a bit of a sook. Not keen to get burned.

Local Bitcoins.com...easy to buy

Also VIMBA ..pretty good local service if you wan to buy via a Kiwi Co (why go offshore)?

Yea true. I need to research on how the transactions work for cryptocurrency also.

Good feedback team I appreciate it

I have long term used Kraken because it has proven itself extremely secure and reliable.

Until you are on an exchange that is hacked or goes dark just at the moment you want access most, you will not appreciate the value of secure and reliable.

I also use bitprime.co.nz to purchase and sell crypto currency. Based in Christchurch I believe. I think they add about 6% fee to your purchase , but when you sell you get full price. I either use the online wallet called Exodus to store crypto, which you can download for free, but I also have a few nano ledgers (offline storage usb). What many people don't understand its that you can buy a fraction of a bitcoin or any other crypto ..Bitcoin is worth somewhere around $11,500USD, but you can purchase a minumum of $100 worth. Youll need to register with who ever youre buying crypto from (in my case Bitprime). Once you purchased your crypto, youll be asked to provide your exodus wallet address or nano ledger address (series of numbers) for the token, then they will send you your crypto. .....www.bitprime.co.nz. /. https://www.youtube.com/watch?v=SxgVml8MjIg (how to use and setup exodus wallet)

The thing about paying off your mortgage faster is that you get a guaranteed after tax return equivalent to the interest rate. There is zero risk to it. Any other suggestion on here has risk. Also, taking investment advice on internet forums is probably not a great way to decide what to put your hard earned into - including mine.

It's one thing to service it, another to pay it off. Many people are now having to borrow so much they will never be able pay it off before their job becomes obsolete.

It's the high principal amount that is the problem. Many are most likely borrowing max amount over max term leaving little room for extra repayments, especially if they're attempting to maintain some sense of balanced lifestyle rather than being hermits in their own home so as to pay down eye bulging ass puckering debt faster.

3 years in, we just upped the payments and dropped the interest rate so now tracking at 13 years (down from 25). Easy to do when your mortgage is equivalent to a house deposit in Auckland though.

It's really not worth paying it off now. A few quick calcs based on a $500k mortgage for 30years, and paying (or not borrowing) $20k lump sum at the beginning.

At 8.5% you save 9x what you paid in the lump sum in extra interest, and if you keep your payments the same, that reduces your loan term by 4.5years.

At 2.5% that $20k payment saves you $21.5k in interest, and reduces your term by 1.75years. So saving yourself barely more than dollar for dollar, and those dollars aren't due till 2048.. Adjust for 28 years of inflation, those dollars won't buy you much. Why pay it off any faster than needed?

Wife and I (FHBs) are looking at putting in an offer on our potential first home for $1.2 million in a few weeks. I keep seeing a lot of comments calling FHB crazy or stupid, so I'm don't mind answering questions for any of you wondering "what the Hell are they thinking?!".

Colleague just bought his first home for approx $3 mio in Mission Bay. Family are in Hong Kong. I think this is a sign they may be returning.

IMO, it's only crazy if you dont meet the following criteria;

DTI lower than 4 (decent deposit would help), rock solid job security for both, house is in very good condition e.g. warm, secure, no renovations needed, you will be owner occupier.

In your humble opinion, for sure

Some buyers always look for renovation and/or value-add potential

And/or are expecting career growth (i.e. tradie finishing their apprenticeship)

Etc....

Guess desk jockeys and keyboard warriors might be a bit different, so understand your point, but surely they could pick up a paint brush, landscape or google DIY improvements on Youtube, do a bit of work.

Point is to seek and hunt for under-value and then add as much value as you can.

IMHO

So a tradie finishing their apprenticeship is buying a 1.2 million dollar house, adding value to it and youtubing DIY ideas?

Seems that you sir are the keyboard warrior

Well my portfolios a bit bigger than that now, but yeah that’s broadly how I started off

Didn’t actually finish my apprenticeship, as could hire licensed tradies cheaper.

It’s not rocket science

Take the tips and advice, I’m not trying to troll you.

Edit: (the YouTube thing was for you if you’re stuck)

Investments take a lot of time and patience

I’ve also had enormous good and bad luck over the last 20 years

Trick is to maximise or capitalise on the good luck and try and minimise or reduce the bad luck.

Not saying it’s all easy, it can be darned tough sometimes, but that makes the rewards even more rewarding

Wishing you all the best for your future

YouTube for DIY advice is invaluable.

AvE for life advice.

Good on you.

Do tell northman46!... only then we can assess your relative sanity or insanity ;-)

It's hard to write without going on an emotional long monologue.

For us it's affordable. We're fortunate with our careers (no help from "bank of Mum of Dad"). Work's looking stable and we've saved a large deposit while trying to get on the ladder. Deposit is 1/3 of the house, DTI is 3, enough savings on top to survive a year unemployed, and we can afford it if one of us loses a job.

We've been trying to buy for 5 years and have always gone for the typical FHB homes. But they're brutal. We compete against FHBs and their parents, investors, bored Boomers looking for a project and the down-sizers. This house doesn't make sense for those people. That's why our reasoning of why so expensive for a first house. Plus it's perfect long term. It could serve us for 20 years, probably longer.

Like other FHBs, time is running out too. We're in our 30s. We need to make a start at having our own family. Covid hasn't delivered the promised crash. The RBNZ has signalled they'll do all they can to keep the gravy train going. Houses have almost doubled during our house hunt. Regardless, we have to pay someone to have a house, why not the bank rather than my landlord? (who once called us his "cash cow"). Another year renting is another $30k down the pan.

I wonder if lock down has emphasised the problems with renting too. For us, the small space, cold, damp, mould, and being powerless to do anything about it. Plus like many others, getting into growing food and gardening.

In which case, I don't think you are even remotely crazy.

We made a similar decision when we purchased. We have two kids. Had been moved on twice by landlords selling from under us over the previous 3 years and just emotional/psychologically couldn't handle not having a home anymore.

These reports are good. Thanks for putting the time to do them.

Also worth keeping in mind that banks are stress testing first home buyers at something like 5% - 6%, so those that are able to get into the market are enjoying low interest rates at the moment, but are also well placed to cope when interest rates do eventually go up. But this will likely be so far in the future that by that point their incomes will likely be considerably higher (even just due to wage inflation, let alone career advancement) and their loan balance will be substantively lower due to the repayments they’ve been making. Tough to get the deposit together though. Should increase the amount that can be taken from KiwiSaver for this.

when interest rates do eventually go up......incomes will likely be considerably higher

Middle NZ needs to lose this unfounded Nostradamus twaddle.

At best when interest rates do "eventually" go up, all it'll probably do is morph a standard table mortgage structure in such a way that the interest portion of your repayments never decrease over time. Go to refix in 2 years time, the interest rate has gone up a couple of percent. Either increase the payment amount or extend the term just to keep on target.

Yes, I think it is likely that notably higher interest rates are many years away. It is likely that first home buyers will have higher incomes in years to come than they do today, both due to wage inflation and career progression.

I don’t know what part of my comment you disagree with. You think it isn’t likely that incomes will be higher in the future?

The current issue isn’t whether there’s risk of interest rates going up its whether one or both partners have an income to service the loan.

All else being equal lower interest rates mean the average person is willing to pay more for the same house (with more debt). Thus property prices move higher, "affordability" remains the same and leverage every increasingly eye-watering.

Hmm correct me if my perception is off but buying a home doesn't make financial sense unless you enable capital gains.

$600k @2.55% over 30 years = $850k total.

Assuming an unchanged price at the end, 30 years and $850k plus to own a home?

I don't understand why we accept "that's the way we've always done it". It appears extremely uneconomic, unproductive and inefficient. Not to mention the flow on effects to future generations.

In addition, lending money into existence via homes does not appear to be a solid foundation for a resilient or "sustainable" economy. Seems more a pillar of sand and we keep piling on more sand.

meh...

Your perception may be a little bit off.

The interest component is what probably has to be compared with a like for like rent , during that same period. ( After all, the choice is between owning vs renting )

eg. $600000 @ 2.5% is 15 000 x 30 ys = 450,000 ( interest only loan ) throw in $10,000 /yr for ins/rates =300, 000

Rent at $500/ wk is $750, 000

AND... then a key assumption one has to make is the growth in rents over that time.. ie. If I dont buy , how much rent will I be paying in 30 yrs time.

eg. $500 compounded at 2% = $670 at yr 15 and $ 900/ wk by yr 30.

I think there are compelling reasons to buy a home vs renting

2 key reasons that this might continue into the future ( rent increases ) , is to do with the nature of our fiat monetary system (Monetary inflation ) ), and the second key point is to do with the locational value of Land.

In a growing economy ( population and GDP ) economic gains and infrastructure gains, get appropriated into the utility value of land.

In my view, the only things that will change this relationship is a radical change in the nature of our Monetary system and/or a radical change in our taxation system..... I only see this happening in a Great Depression like event.. ( which is possible )

I do agree with ur sentiment though... A lifetime of debt ( 30 yr mortgage ) is kinda enslaving , and is something I'm glad I never had to consider.

The alternative of being a lifetime renter is also something I dont like the idea of either..

ALSO...mortgage interest rates at 2.5% ..is akin to a transfer of wealth from savers to borrowers.. gift of the RBNZ

Roelof, so what your saying ,in your example ,is that after 30 years , on an interest only mortgage you own the home.

Cowpat.. is that what u think I said ??

For the sake of simplicity I calculated the total interest based on interest only loan.

For me, paying off the mortgage itself, becomes a way to save , a store of real value.

Throw on top of that , the impact of monetary inflation on asset prices, and the choice between owning vs renting became pretty

clear for me.

Interesting figures, but the goalposts have changed with regards to risk as well. We've travelled a long way since December. What banks expect in terms of servicing the loan is not what it was then - savings have to be from income (not debt, not necessarily equity for rural), and I've had some banks insist that they will only lend on certain types of houses (larger than 50 sq m - Kiwibank - not a transportable, minimum of 3 rooms etc). Extraordinary really - only willing to lend if I accept conditions not just on capacity to service but if I accept their conditions on what I'm borrowing for..

I've experienced this too. Been waiting almost a month on an application so far and already had disputes with the bank due to half the deposit stemming from a severance payment. Sad part is that I can easily afford the payments but the banks are being pretty fussy. Apparently we've got an offer coming but still waiting on that.

Awesome. So with such high mortgage debt they just need interest rates to stay at these record low levels for about another 20 years in order for the mortgage to remain affordable. I see no issue here.

The boomers will look after them...

Imagine what could be achieved if all this time spent complaining and blaming circumstances was put towards improving one's own life!

So after selling and making an eye watering tax free profit Yvil I assume you are buying up again? Or are you holding off...watching the FHB tumble off the cliff?

It's not a profit unless it was a second property, he was downsizing or moving somewhere cheaper. Even with the last two it is only a %. If he was selling to upgrade then he's actually lost money relatively.

Over $900k capital gain in 7 years and he "lost money"? You should hear what you guys sound like.... Entitled greed ! Future generations will judge harshly.

Yes Yvil is under the impression he worked hard for that profit.

Breathe FB.... hear me out. He needs to live somewhere, he wants to buy back into Ponsonby as I understand it, which means all the "profit" is going to go back into buying what he already had. It can't be considered profit in that case, only if he wants to buy cheaper.

That seems a bit nuts, though. You seem to be saying that whether I make a profit on something doesn't depend on whether I sell it for more than I bought it for - even if I sell it for close to 1 million more than I bought it for. Whether I make a profit depends on what I choose to spend that money on a year or so down the line. Doubt the taxman would accept that you didn't make a profit because you're (maybe) planning on blowing all the money next year.

Really underlines why the tax base change is needed. Incentivise productive working (doing, making, helping) thru a lower tax rate, and disincentivize idle dept base land speculation thru a universal land tax paid quarterly. Yes house prices will take a hit, but you need a decent wage to pay the mortgage and it will be offset by your reduction in income tax.

Your chance to make a difference for yourself is approaching, and if your under 35 the odds of fleeing to Aussie or the UK are off the table at the moment. Check out TOPs policy's.

Totally agree.

But never going to happen.

Averageman.. New money ( credit growth ) may enter an economy via the housing mkt , but after that it flows... One result of that is that Capital Formation has never been easier.

A company like Rocket Labs would have struggled to get off the ground 20-30 yrs ago.

I personally thinks TOPs policies are a little bit flakey... They say it is evidence based but I suspect it is simply their attempt to justify things.

eg. a tax on an imaginary income, in regards to the TOP policy in forcing house prices down. ( not hard to find research that supports ones view, especially in regards to economics )

In the Next breath TOP wants to do Money printing to address Covid 19 stuff..

The “economists” at TOP are like doctors of the 19th century - those who consulted them were statistically more likely to die than if they hadn’t.

They don’t live in the real world - taxation of imaginary income, race-based resource allocation and taxation, spraying helicopter money around like there’s no tomorrow.

Totally disagree.

But never going to happen.

I’m under 35. I own my home, but TOP’s irrational land tax would turn me into a tenant paying rent to a government landlord. Prospective first home buyers are unlikely to be convinced by the idea of having to pay perpetual rent on the property they hope to one day purchase.

Why do you 'totally disagree'?

It is totally distortionary, and unfair, that people who work, build and run businesses etc get punished in terms of taxation rather than people who speculate on housing.

Land is subject to the same tax requirements as other assets. There is no “loophole” or tax advantage enjoyed by land.

But if you believe this, you should be advocating for an extension of the bright-line test for CGT, not the insane land tax based on imputed (imaginary) income proposed by TOP. The existing 5 year bright-line test actually represents a tax disadvantage incurred by land that does not apply to other assets.

Meanwhile in Australia, “CBA had increased it’s hardship and collections team from 650 to 1700 people and is using better data tools to assess customer circumstances. More then 30% of customers with deferred loans have less than 20% equity in their property”

Just observing.

Interesting to note the change in post comments over the past few months.

In March - April it was bubble burst, 50% fall, and the one that I reckon was a classic that summed many comments up: “buy a house and everyone will be pointing and laughing at you . . You will be officially stoopied”.

However most of the comments today are moaning “can’t afford”, “how can someone afford a house”, and quite a few boomer envy comments . . . and the FHB envy comments that they are miserable, as prevailing view is that house prices are seeing upside and the existing mortgage is likely going to be less this time next year.

But just observing. :)

Yes, but your engaging in some kind of "I bet x will happen" with other commentators. It's mindless and not really constructive. The reality is somewhat different. You don't know how bubbles unwind and it is common behavior before most bubbles collapse to deny the existence of a bubble or that it could potentially unwind.

Furthermore, if you were really interested in sentiment analysis, you wouldn't be trawling the comments of interest.co.nz You would be using more sophisticated tools across the internet. So you're really engaging in a game of one-uspmanship about something you have no real ability to predict. That might sound harsh, but let's be honest, this is the reality.

JC... When something is labeled a "bubble" for over 10 yrs then, in my view, its questionable whether it has even been in a bubble.

Not sure what you mean by "sentiment" analysis. ?

NZ housing was in more of a bubble, and more vulnerable, pre GFC ( 15% credit growth era ) than it has been since.

Also...Auckland real estate has been sideways for last 2-3 yrs.

First question is.. How do you define a bubble and what metrics would you use.?

The last big bubble I lived thru, and was a part of, was the NZ sharemarket before the crash in 1987.. ( I leant what "animal spirits" meant )

Well there you go. If you don't know what a bubble is, you cannot deny its existence. So claiming that the last big bubble you lived through was pre-1987 is a false claim because you don't know if you're living in a bubble now. And this is the recurring theme of bubbles: most people don't actually think that a bubble exists.

You did not answer the question as how you define a bubble. What metrics do you use? e.g. for housing, the price of a house compared to median family income?

In my personal opinion the term bubble suggests a massively fragile situation that can pop any second, thus it has to be quite short term, it has reached a point that it will deflate any second now. That is different to cycles where every boom is followed by a bust. You cannot say we have had a bubble for 10 years. You can say that we have had conditions over the past 10 years that has to end in a bubble.

And from the conventional view point of valuation, I agree with you, the greater the dissonance between cash flows and PV of investments and assets the greater the probability that we are heading toward an unsustainable bubble or we may already be there.

Robert Shiller says that bubbles cannot be easily defined by metrics. Each bubble is different. What he does say is the common element of bubbles is 'irrational exuberance'. This essentially means human attitudes and behavior that drives asset prices higher than the fundamentals justify. You should read the book 'Irrational Exuberance.'

Furthermore, housing bubbles do not pop overnight. They can't because the volume of transactions is too low.

I kind of think that discussions around 'bubbles' are moot.

What we do know is that housing is very expensive, relative to incomes, in Auckland especially, and NZ more generally.

The high house price to income ratios create greater fragility, because households become more sensitive to issues arising from loss of income. But, it must be remembered, most of the house owning population are not so highly stretched. So that limits the fragility.

The fragility has also been strengthened by things such as rapid lowering of mortgage rates. It must be remembered that even 2 years ago mortgages rates were north of 4%. NZ has had the luxury in the last 12 months of being able to cut the OCR significantly. Most other countries couldn't. That strengthened our fragility.

But that fragility still needs something to break it. Many people thought covid would crack the fragility. For some, the glass *bubble* would explode - 50% house price *crash*. For others, like myself, it would be significant cracks in the glass bubble - 10-15% price falls.

Thus far, the market has been resilient. A veneer of *strength* is apparent, but it's only masking a profound underlying fragility.

The RBNZ and Govt have used up a lot of their ammo - most of it (noting we will probably go to a negative OCR). That has *saved'* the housing market - for now. But my expending that ammo, we have become even more fragile.

I predicted last year that sometime before 2022/2023, the market in NZ will crash by 20-25%. I'm not so confident on that timeframe, now, but I think there's a better than even chance that it will crash by 2025. It's likely that an economic or natural event will hit us by then, and we won't have the ammo left to deal with it.

Fritz,

I like what u have written.

If u reread it you will see that there was never fragility.

ÀND .. u also alluded to why this is so.

Govt and Central banks r the 2 most powerful economic forces that there are .

The GFC response , by other nations , created the playbook that NZ was always going to follow.

I also agree that 2025-26 might be a timeframe to watch.

The last 10 yrs of houses prices in nz has more to do with Govt and central bank actions, in my view, than it does with the idea of " irrational exuberance" ... " Bubbles".

We may enter a bubble , as a final blow off. I don't know.

Maybe banks will start doing ninja loans ??

That's like me saying do you know what a cloaca is, because if not you might be one

House price index? This graph is really scary....

https://www.economist.com/graphic-detail/2017/03/09/global-house-prices

J.C.

You amuse me. You have been claiming for considerable time regarding a bubble burst - so when is this going to happen??? You seem to be expecting people to put their live on hold rather than getting on with it.

You seem to be just happy to scaremonger with this ongoing wishy-washy unsubstantiated claim people "don't know how bubbles unwind and it is common behavior before most bubbles collapse to deny the existence of a bubble or that it could potentially unwind."

As for accountability, you posted that people who make predictions "run the risk of being perceived as frauds or con artists into the future". So what's your beef against outing those posters who make these unsubstantiated claims which prove unsurprisingly being false? It would appear that it is simply those who were to be the "frauds" weren't, and the dgm bubble burst claimants you sided with are proving to be the frauds.

If posters know that they are likely to be held to unsubstantiated claims then they would put a little more consideration into their posts and the quality of comments would greatly improve.

The guy is a broken record. The crash is always just around the corner, you wait and see. His sort have been saying the same thing on this site for close to a decade now.

But how do you know that the bubble burst claimants are frauds. As of today that may appear to be the case but maybe in the future they could be correct. As I've said here before, if things do turn for the worst ,I just hope that people like yourself who are happy to gloat at the moment will have the good grace to say that they indeed got it wrong. I have also said many times on here that I have no idea what will happen into the future. Things might crash and burn or they may not. History tells us that house prices would increase under normal circumstances, but I for one don't think these times are normal. But I sure don't get on here and talk down to people who think things could turn sour. It comes across as arrogance from someone who has made money out of property. Everyone has a right to express what they think. Saying things won't crash and burn is just as unsubstantiated a claim as saying things will boom, in my very humble opinion of course.

But how do you know that the bubble burst claimants are frauds.

Do you think Robert Shiller was a fraud or a respected economist / academic? If your answer is the latter, good for you. Shiller was famously accused of making claims about bubbles. He did nothing of the sort beyond saying that there was evidence that a bubble could exist. It turns out he was right when the bubble burst in spectacular fashion. Before the bubble burst, the media suggested that people who had listen to Shiller would potentially have lost market gains his views had prevented them from investing. The difference between Shiller and most people is that he understands probability and its impacts.

Yes J.C, I happen to agree with you. I was talking to P8 who seems to think that making a prediction that doesn't align with his is unsubstantiated which I can't quite fathom. I certainly don't think Shiller is a fraud and wasn't alluding to that.

You have been claiming for considerable time regarding a bubble burst

You just wrote that becuase you're a troll sensing that I'm not a fraud / charlatan who goes around pretending I know the future of house prices.

The guy is a broken record. The crash is always just around the corner, you wait and see.

Another troll in action. I'm afraid your inanity doesn't push any buttons.

JC

Your decision to believe whatever you wish.

It is really pleasing to see 145,000 FHB getting on with their life appreciating the social and financial security of homeownership. They have little to fear from a shock - whether it be at the personal level or wider economy - by being prudent.

. . . and I have no concerns calling out unsubstantiated scaremongering claims.

For you, you have an unfailing belief in Shiller as he called the USA burst in the GFC. Given the subprime market that existed there that was not surprising; however while a downturn in the NZ market, no such bubble burst occurred here.

Given the subprime market that existed there that was not surprising;

I see. Every Tom, Dick and Harry knew about the subprime issues. Got it.

40% of two earners is "affordable" ? What a sick joke.

When the housing Ponzi collapses (and it is not an if, but a when) it is going to be potentially catastrophic. The higher you go, the bigger the mess when you fall.

My only hope is that, when this happens, the ones to suffer won't be the latest FHB's, but the speculators.

I am afraid though that, like in any Ponzi scheme, the last to jump onboard will be the ones mostly affected, sadly.

'40% of two earners is "affordable" ? What a sick joke'

Agree, It's not clear to me why the authors perpetuate this nonsense.

What's more, it's not just about whether it is affordable now - its got to be affordable for 30 years. And I bet not many people spend 30 years as part of a couple that collectively earns at least 2x the median income for that entire period.

What's worse again is at best case interest rates stay flat (as well as inflation) for 30 years so wages stagnate, no inflating the debt burden away. If interest rates do go up, then yes we'll have inflation and wages will rise but whatever income gains are to be had will like be offset by an increase in the servicing costs of the mortgage.

Really like the wind-swept and interesting pic.

Looks like an upmarket version of the retirement garage I hope to find out there somewhere. First year, in goes the shelter belt along the south and west boundaries. Peace at last.

.

RBNZ will likely follow the US and let inflation run ahead of target in the future. I guess when that will be is anyone's guess but as assets become more inflated they will need to be curbed somehow. Looks like a win win for the banks when interest rates increase

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.