Both Treasury and Inland Revenue (IR) advised the Government against removing the ability for investors to deduct interest on their mortgages from their rental incomes.

Treasury said, in a Regulatory Impact Assessment on the Government’s proposed housing policy changes, it didn’t have enough time to do the analysis on the change.

It was first asked for advice on November 18. It provided a response by December 7 and continued developing this advice throughout December and January.

Treasury didn’t include any commentary on interest deductibility in the Assessment and said the Government should hold fire until the work is done.

IR, in the same Assessment, simply said it opposed denying interest deductibility.

Revenue Minister David Parker couldn’t put a figure on what the change would likely cost investors/how much additional tax revenue would be generated. He said it would depend on how the rule was phased in.

Put to Finance Minister Grant Robertson there appeared to be a number of question marks over the impact of the change, he noted the Government was giving itself until October to consult on the specifics of the policy before introducing legislation.

“Behavioural economics is a difficult field and obviously most of what happens from here, with regard to deductibility, relies on behaviours of those who are investors or potential future investors,” he said.

Treasury wanted bright-line test extended to 20 years

As for extending the bright-line test from five to 10 years, Treasury didn’t have time to form a view on this.

Rather, it recommended the test be extended to 20 years.

Under the bright-line test, people who buy and sell investment property within the specified timeframe have to pay income tax on any gains made.

Treasury said: “While tax settings are not the primary driver of problems in the housing market, extending the bright-line test should put downward pressure on house prices in the short to medium term, and provide equity and efficiency benefits in taxing more economic income.

“However, extending the bright-line test may put upward pressure on rents.

“While the extension may result in lock-in effects [encouraging people to hold on to properties they’d be better off selling], the additional costs of these are unclear. The Treasury’s view is that lock-in will not significantly reduce housing utilisation.”

IR opposed extending the bright-line test

IR opposed extending the bright-line test to 20 years, saying it would result in a “substantial” lock-in effect.

“This is likely to impede property from being used in the highest value ways,” it said.

It recognised some investors might pay substantial amounts of tax if they sold properties within 20 years, while those who waited a bit longer would receive tax-free gains.

IR supported keeping rule at five years for new builds

IR suggested continuing to apply a five-year rule to new builds to encourage the building of new houses.

“Such properties are currently subject to the five-year bright-line test under the status quo and building consents are at an all-time high,” it said.

The Government has adopted this recommendation.

Treasury wanted new builds to fall under the 20-year rule

Treasury on the other hand advised against any exemptions being made for new builds.

“An exemption comes with additional administrative and compliance costs, and over time reduces the coherence of the tax system,” it said.

“While increasing housing supply is important, the Treasury considers there are likely to be better ways to directly support supply, for example through an explicit subsidy for developers.

“If the Government does proceed with an exemption, the Treasury prefers that exempt houses remain subject to the 5 year bright-line rule.”

Key figures missing

As for the tax revenue that would be generated from extending the bright-line test to 10 years, Treasury didn’t do this math.

But it said a 20-year rule could see annual tax revenue generated reach the equivalent of 0.2% of Gross Domestic Product by 2035.

IR has been unable to say how much tax has been generated from the existing bright-line test, as these tax payments are lumped in with investors’ other income tax payments.

Treasury told interest.co.nz: "The announced changes involve significant changes to tax settings, that impact the economy through a number of channels – many of the interactions quite complex. To fully analyse these impacts (along with the other contemporaneous components of the package) would have required a longer period of time than was available.

"The complexity in developing advice was intensified by the specialist skillsets needed across several teams within the Treasury, and working across multiple agencies including the Ministry of Housing and Urban Development, IR and the Reserve Bank (on financial stability considerations)."

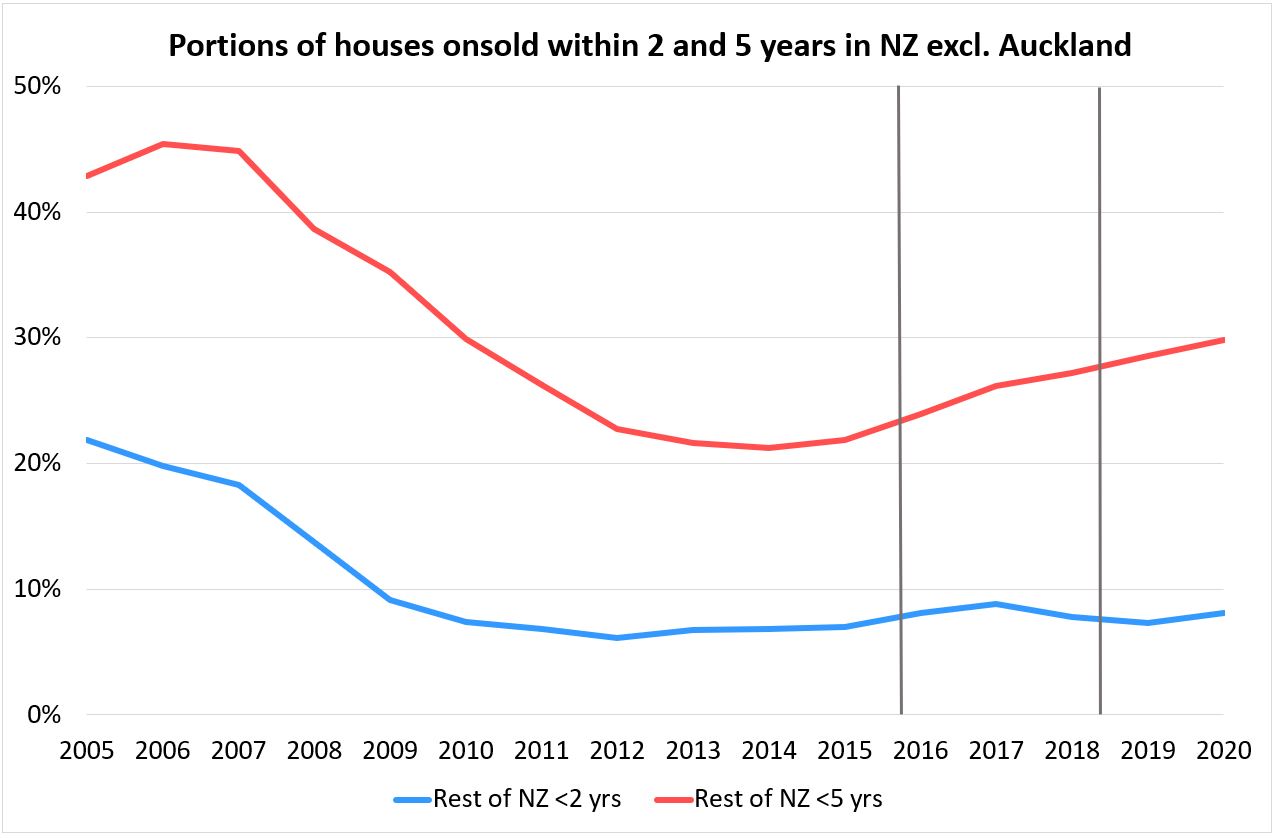

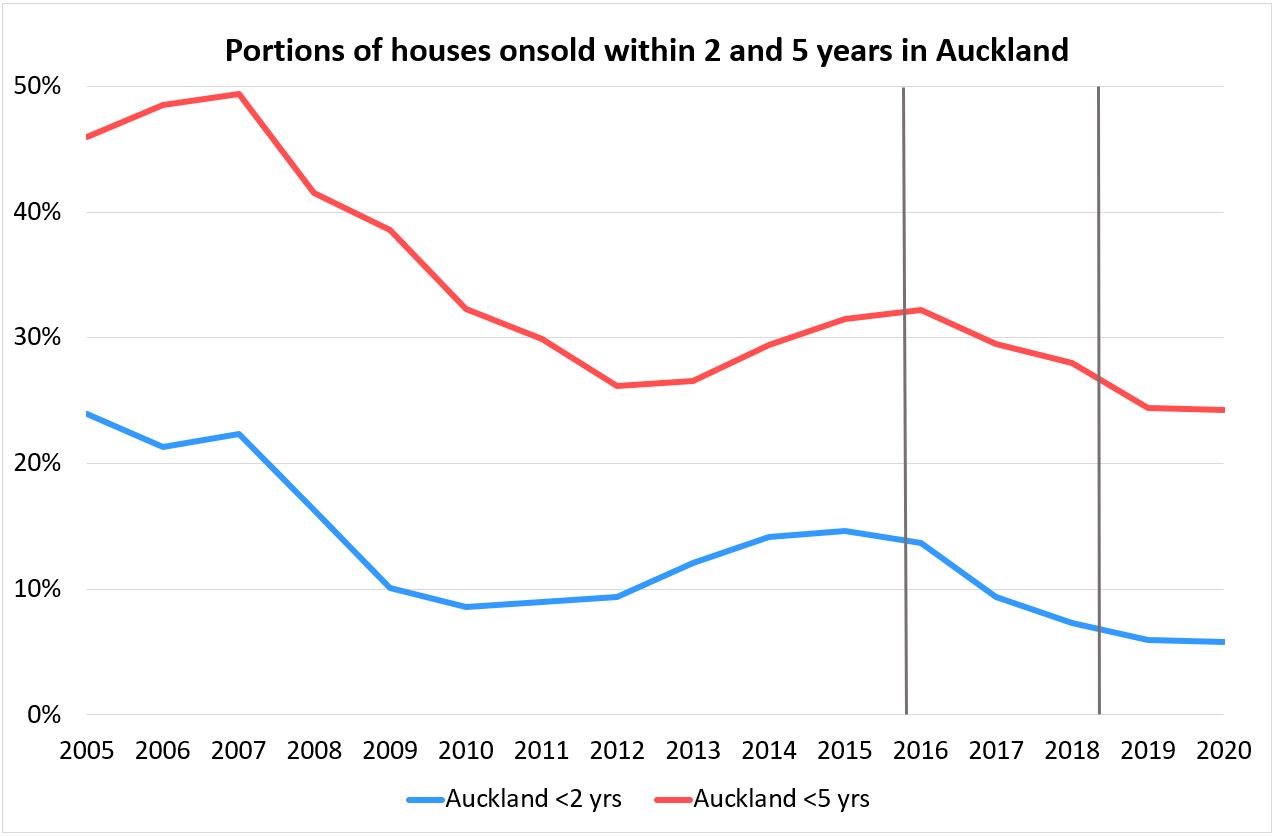

Impact of bright-line test to date

CoreLogic data provided to interest.co.nz shows the bright-line test (introduced by the National-led Government at two years, and extended by the Coalition Government to five years) has to date reduced the portion of house flipping.

However flipping activity has been picking up beyond Auckland, presumably as capital gains have been attractive enough for people to look through bright-line rules.

131 Comments

That's interesting. So the change was an unadvised political gesture then.

It's a bit of a gamble - there could be unintended consequences. But I say good on them for acting fast - prices are rising so much they needed to try and break the mindset behind the galloping prices.

fast -- five years shouting about the crisis and now in 4th year of government ... fast you say -- hell hate to think what you mean by considered!

Yep I do wish they'd done more sooner and I hope there is a lot more coming in their forthcoming supply side announcements.

They could have rolled out the interest rate deductions a few months ago but I don't know if it would have been politically feasible to do before prices really started taking off about September last year.

Given where we're at now though, I'm glad they didn't wait for a full analysis of the effects of the interest rate deductions change.

They did Kiwibuild- oops massive failure so lets screw the housing market up better this time by more idiotic interventions. Your like the government, you don't seem to know the difference between Investors{ long term Rental providers} and speculators who buy and flip without ever renting them out. The latter are already paying taxes on such gains.

To take away interest deductions for boni fida investors will only exacerbate housing supply issues. Watch investors and speculators walk away from deals now that they have previously entered into with developers. Gonna get real messy

Act in haste Repent at leisure, and the repentance will be a bitter result for many.

I wish someone would advice the RBNZ to start increasing the OCR, even by just 25 basis points and see how just that slows the investors. Then again Orr would repeatedly choose to ignore this advice. This one change will definitely tilt the balance more than anything.

It's not his job, he's fighting as hard as he can to keep us employed. The answer is building houses but in the meantime, I also think NZ needs investors to pay a CGT on annual capital profits. Treasury/IRD can figure out the appropriate rate. The interest deductibility change means you are paying taxes even when you make losses, and that introduces unnecessary risks and taxes the cash flow rather than the capital gain. However, I do think the max LVR should be respected in relation to deductibility of interest, deducting 100% against a max 60-80% LVR is absurd.

(double post)

Proud of our government for standing up to the bureaucracy (deep state?).

Agree. There are probably rental properties out there built 50+ years ago that have supposedly never made a cent of profit (as they are always sold to someone with a big mortgage who deducts the interest). They can make up as much crap as they want about it being fair because that is how it applies to all businesses or whatever, but realistically it is not in any way fair and needs to be changed whether IR or Treasury like it.

I'm sure banks pay tax on the profits from large investor mortgages. It is a money go round. Someone pays tax somewhere.

This has brought a few smiles to my face today. Great herald article with the usual property spruikers complaining bitterly and saying it’s crazy. If they are that scared it just might work.

Yes it could backfire and rents could go up, but we know that doing nothing to avoid unintended consequences is just not working.

Indeed Jimbo. + the articles of bank economists going on about negative consequences - “chilling effects”. Hopefully everyone can see through those.

Whilst I was hoping for more , it’s genuinely the most any government has done in the last 20 years.

Can you tell us all how many new builds will occur as a result of changes?. Also, is envy your middle or second name

The absolute boar's nest that is housing in this country went way, way beyond "envy" a long time ago. It has to be fixed.

I'm mid twenties - have had capital gain off a house I owned in my early twenties. Not naïve enough to think that I did anything to deserve it - so no envy here. I'd guess more new builds? Seems to be stabilising the market around the lower quartile - everything else should hopefully drop.

Carry on.

She's got my vote, and I didn't vote for her last time. I was waiting for her to actually do something to help the country and make the 'brave' decisions that all others have failed to do. At last I have some hope that we will become a country that cares about ALL its citizens again.

Be interesting to see if she slashes immigration when the borders open.

I agree with you Jimbo, however, wish it had been done months ago. I hope that the Reserve Bank now does their part (in May) as house prices are still unaffordable.

When you break an egg - you reach for another.. Labour have done well pushing through the bureaucracy. I don't imagine it was easy!

The Bright-Line-Test is always contentious, yet is being applied in such a way as to incentivize new builds. 20 years has merit. Further piecemeal extensions to the BLT may happen.

Everybody knew it was going up to 10 year today. As always, Judith Collins was her disingenuous, tangential self - pathetic.

Judith Collins is in no position to critizise Labour over this . She was part of the Key Government when people were sleeping in cars and garages. She surely is a hypercrate.

How many bottles of beer can you fit in a hypercrate?

Two dozen ? ... a regular crate holds 12 bottles of 750 ml each ... does Judith Collins get on the turps .... cool !

You can never fill up a hypercrate

Hypercrate = a whole brewery

Will be interesting to see where National goes from here policy wise. Will they campaign on reversing these tax changes? Can they actually gain votes from that? Can’t have that many PIs can we?

You may remember Simon Bridges campaigned on reversing the healthy-home-legislation, rental reforms and the florigen-buyers-ban?

When it came to 'drug reform', National's Simeon Brown bot was a few modules short of an operating-system. Last week Gerry Brownlee wasn't sure how many houses he owned.

National continuously come off out-of-sync and touch. They're like that can-of-peaches at the back of your pantry.. anything has to be more appealing. Where did this can come from anyway? Why is it here? Has it past its' best-before-date? Do peaches come in blue?

Hahaha

Funny

Yeah I don't know what planet the bureaucrats were on not supporting new build exemptions.

Probably more 'tax simplicity' dogmatic nonsense.

Quite hilarious. The government creates bureaucratic groups to form conclusions about specific parts of the economy or government. It then ignores those conclusions (Tax Working Group).

The government then waits for advice from agencies about what should be done. They give advice or ask them to wait, the government takes their advice, then does their own thing anyway.

Just goes to show you all the bureaucracy and waiting around for advice is pretty meaningless, they are just stalling for time and are going to do what they think anyway (which is the bare minimum required).

NZ is a representative democracy not a technocratcy. Our elected representatives can ignore the advice of so called "experts" if they wish. Besides the experts often contradict one another, look at economists.

Jacinda got quite firey in the press conference when questioned around the magnitude of the interest deductions changes. This must be why...

"these tax payments are lumped in with investors’ other income tax payments."

No analysis... How dumb are the bureaucrats

Or maybe clever? They don't want us to know?

I'll call it now- interest deductibility will end up being removed off the table come Oct. Putting it on the table now will scare lots of investors off - allow the market to reset and for RBNZ to ban interest only loans. By Oct the govt will see how far the amrket has fallen and then turn around and go we have changed our mind after consultation as this move would be out of alignment with every other tax investment rule with interest.

The other reason why this will occur is tax rules are rarely made effective half way through the year- they always start at the beginning of the tax year - otherwise they become extremely messy to comply with and even messier to audit.

Nah, don't think so. They've had quite a long time to make decisions on these policies. They don't want to ruin their reputations.

ikimpaul...exactly that did cross my mind as well. And bear in mind the threats and extreme bullying they will suffer at the hands of the property lobby.

You've nailed it I think. Policy announcement is basically "jawboning"with 6 months up their sleeve. If prices drop 15% in short order (as I think they will), they'll shelve the policy and call it a win. If prices keep rising, they retain the option to implement.

I doubt it. They will lose even more credibility.

It's the classic opening gambit.. Never ask for what you want. Go high then settle for 50 cents on the dollar.. At least I hope that's the case.. Paying tax on an already negatively geared rental doesnt make a lot of sense.. At least I can rest easy in the knowledge that labour will look after me in my retirement now that they have stolen my prospective retirement income... Hmmmmmmm

Here are a few things to that cross my mind,

1.) FHB's dream of upgrading to their dream home from their first are dashed.

2.) Rent will increase as well as homelessness.

3.) The slow down would mean councils will start to starve for infrastructure funding.

4.) Businesses and trades that are dependent on the prospering property market will go under.

5.) Credit will tighten as risk had substantially increased becoming another slap on FHBs.

6.) The special wage subsidies in lieu of COVID is drying up with a potential of increasing unemployment.

7.) Businesses are becoming more uncertain what's next from the government and investments are suspended.

The 35% of households did not get what they want at the expense of the 65% and this may be well and truly the final nail to mark the end of the economic cycle in NZ.

"FHB's dream of upgrading to their dream home from their first are dashed..."

LOL

LOL

LOL

Under-40s are despairing of ever owning a property at all, they're not dreaming of an upgrade... And none of this affects your own dwelling, for which you never have been able to claim tax deductions. Poor, poor effort.

He’s right - people usually either invest or spend. Where investment gives little return they then spend. People who would have used equity / cash to buy an investment property instead use that money to buy a bigger house. The difference between house prices starts to spread - lots of $2 million properties , lots of 750 k properties and not much in between - Sydney is a classic example of this

Ah CWBW. You do make me laugh.

8) Residential investors will kick up a stink and pretend they care about FHB's/trades/productive business/rents, when they are just concerned about their own back pocket.

So they should , they are the ones taking all the risk. Example- tenant misses rent payment and thus so does landlord, the bank goes after the landlord not tenant and credit rating warning issued.

And you think thats fair?

So they should , they are the ones taking all the risk. Example- tenant misses rent payment and thus so does landlord, the bank goes after the landlord not tenant and credit rating warning issued.

And you think thats fair?

1) as above - this is clearly nonsensical.

2) It's possible rents will increase, but remember those missing out on profit because of high leverage are competing in the same market with others with no leverage who are unaffected. You cannot just increase rents unilaterally unless the weight of the market is doing the same.

3) If councils saw development as a profit centre they would be encouraging building. The opposite seems to be the case.

4) Perhaps. This is part of a necessary rebalancing - the housing market and its appendices have become a monster

5) The RBNZ is still pumping money in - I wouldn't worry about credit availability. Unless you think house prices will fall more than 20%, existing equity rules will suffice.

6) Perhaps, but irrelevant.

7) The companies I'm invested in seem to be ploughing on with investments - OCA are raising capital today, the power companies are building power stations like there's no tomorrow. The share market is still booming.

Wow, there is a lot of gumpf in this comments section but this takes the cake! You don't get 'prosperity' from selling the same stuff back and forward for increasing prices. Bring on the 'end of the economic cycle' (read - a fairer system for all).

Why should anyone listen to Treasury? They're consistently wrong, and consistently toe an ideological line that is out of step with observable reality. Absolutely weaponised tool of the status quo.

Correct. Treasury seems to have done NIL by way of analysis on all fronts. "Treasury said, in a Regulatory Impact Assessment on the Government’s proposed housing policy changes, it didn’t have enough time to do the analysis on the change." ....." As for extending the bright-line test from five to 10 years, Treasury didn’t have time to form a view on this."

Wonder whether they are just sitting there collecting fat salaries & happy with status quo. Unproductive input, if any, to be expected from Treasury. No surprises then why government pushed ahead with measures on their own

It seems crazy that Treasury hasn't been given enough time to assess the new policy. It suggests that the Government has been dreaming this stuff up independently or it was never in their heads at all until a couple of months ago. Surely they've had 4 years to address the issue (it's not new) and properly assess this policy.

Where is Winston Peters when we need him?

I'm sure he's enjoying a single malt, with a grin from ear to ear.

should treat every house in nz as the same ,no deductions at all but give tax credit to business employment also r&d credits to increase smart business and so on so we dont need to import people in huge amounts. also train our over 55 years old nzers there is plenty of them able bodied.use the resources we already have here and get rid of welfare unless you are vulnerable part of society, we all here together act like it.

Agree with the first comment rj, but then you kinda lose the plot a bit.

I say, you can have your interest deductions so long as you are paying commercial interest rates, but you can't have both.

If this government does not listen or consider any advise than why does Jacinda Arden every time comes up with that we are waiting for advise ( Everyone know now that it means not interested and is said mjust to deffer /avoid/delay).

https://www.nzherald.co.nz/nz/government-officials-advised-ministers-ag…

Another example is interest only loan, though RBNZ and Government have been in touch with each other and in discussion for ages, still Jacinda said waiting for advise from RBNZ on DTI and Interest Only loan..

What is Mr Orr waiting for before advising Jacinda and also is it not that RBNZ already asked DTI from government much earlier, so why the wait and what advise. Also Mr Orr said that he does not need any permission to ban interest Only loan and can go ahead anytime, so again why the wait and what for.

Why no is grinding the government on it and also Mr Orr. Perfect time to introduce after taking the first step today.

I'm betting the waiting is to see if todays changes calm housing market between now and May. Because they don't want to high tackle the market, just slow it down. My guess anyway

I've worked in the central agencies and it does take a while to pull a piece of advice together that is well thought through and that the people that matter feel comfortable about - a lot of parties to gather views from, eyes need to pass over it, edits, checking back, then up the chain to the seniors who will present it, all while other things (some urgent) are going on.

It is absolutely instinctive for people in orgs like Big T to make those papers as well researched and as well argued as is possible for them.

They can't just magic up a nicely crafted piece or work because this shambles (inequality, basically) has been brewing since the 80s.

I say this in the full knowledge that nobody is interested at the moment in hearing excuses for highly paid bureaucrats, given the years of denial and delay that has covered us in hyperbubbles.

The government had failed miserably in creating an environment to increase the supply of affordable housing and rental accommodation. The situation has got considerably worse in the last 3 years under Labour.

Failure of Kiwibuild to increase supply, excessive emergency housing costs, ineffective changes to Reserve Bank Act resulting in lower interest rates than necessary, huge expansionary monetary policy resulting in excessive savings in NZ bank accounts and ineffective tax planning by government has led to this knee jerk reaction to implement policies that the Reserve Bank, Treasury & IRD cannot agree on.

If Labour were on top of their game, they should have campaigned on extending the Bright Line Test to 10 years and removing the tax deductibility of interest on rental properties.

Both of these policies will result in the government collecting a lot of extra “new” tax from property owners.

Effectively these are new property taxes that the government will be collecting and they should take responsibility for not disclosing this at the last election. Any trust built up has now evaporated.

Business needs certainty in tax rules and not knee-jerk reaction to introducing new policy without getting appropriate consultation from all the experts rather than an inept government who have had little training in financial management.

At a minimum the “new property tax” income streams should have been costed to find out what financial and social benefits it will bring to NZ.

Has the business community been given sufficient time to plan for the proposed tax changes and how fair are the rules compared to other types of investment?

I believe it will result in a windfall for lawyers and accountants because the tax system is just getting more complex.

This is just the start of of the property tax collection. The government has borrowed too much money and in future it will not be able to collect sufficient income tax to pay interest bills and its annual expenses.

Rather than invest in long-term infrastructure the government has wasted too much money fighting fires such as emergency housing and inefficient social spending.

I guess the Government felt like something had to be done and that's fair enough.

There will be unintended consequences, the majority of rentals are privately owned by Mum and Dad investors. With interest rates moving up soon, rates increasing, the lack of deductibility of interest will be seen as a tax on Mum and Dad investors and it appears they are being the scapegoat here.

Multiple Government housing polices are at the core of the problem here along with cheap interest rates and poor TD rates.

Unfortunately the poor old renter will face the ultimate cost here.

The 10 year brightline extension to 10 years means a percentage of the market will not come onto the market further complicating availability.

The very people Labour appear to want to help get caught in the crossfire, just like the changes to the tenancy act with regard to evicting tenants.

It is no surprise that the emergency housing list has increased 5 fold, these people are now not wanted by the private rental sector as under the new rules they are potentially liabilities !

Fair comment Shoreman. Sad but true. The real balancing act is going to be around increasing the supply of subsidised housing at the bottom end, and shifting the 'intermediate renters' (a class unknown before the 1990's) back onto the home ownership treadmill.

Hey, if landlords get stupid about rent hikes there's a new policy for that too.. Rent freeze or caps on percentage of increase and such. Seems theyre not exactly scared to tinker on rental policy judging by heatpumps, 3 months notice etc etc

Easy ways to get around stupid policies like that.

Its about time we helped sons and daughters into their first homes rather than mums and dads into rental investments, dont you think?

What about humble retirees who have had their income on term deposits slashed and burned? There are anecdotal stories from banks of people 80+ turning up wanting a mortgage approval so they can try to buy something to help support their retirement. There are no winners in this monetary environment (apart from the elite) and the ongoing demographic warfare that you’re participating in is ultimately unhelpful to resolving the problems we face as a society.

That's what we and a lot of other people we know are already doing.

Interest rates up soon? In October last year the Reserve Bank's Chief Economist. Young Ha mentioned that house prices falling would be a "worse case Scenario" which could not be afforded during the Covid recovery. Following yesterday's announcement and the chatter now that house prices could go down, I won't be surprised if the RB cut the OCR again.

Golly there are a lot of Labour shills on this thread. Rents will increase by between forty and one hundred percent (over four years) as a result of removal of interest tax deduction. Little short of an ongoing divisive financial disaster for most of NZ's renters. This isn't anything to celebrate. Many of our tenants have lived in their homes for over ten years. I had no intention of increasing rents, and I haven't done so in years. However this new policy leaves me no choice.

As above.. Rent freeze time then. The beatings will continue until morale improves

Dave Mederato maybe its time to invest your money elsewhere and let young kiwis have a chance at home ownership

You clearly no nothing about economics. Also you can expect more labour than national trolls after the results of the last election.

Based on another comment you’ve made, you don’t know much about economics or tax either. Play the argument, not the person.

That's okay, your tenants will eventually find new landlords who aren't leveraged to their eyeballs so don't share the same inclination to increase the rent. 5000 first home buyer purchases are made every month, maybe a few of those buyers leave rental properties vacant for your valuable tenants?

Get this. I've been in this business since 1990. Since before it became trendy. Haven't bought a property in many years, and definitely not mortgaged to the eyeballs. If I can see the outcome of this policy, then maybe you should listen.

Lol.

Go ahead and increase your rents.

Nobody is going to pay them.

What Brock said. Put the rent up 100% and see what happens. Then tell us about it.

So you've been in business since 1990, you're not mortgaged to the eyeballs, yet mortgage deductibility is a huge thing for you and you have no choice (your words) but to impose this onto your loyal tenants?

Will they though? Do you think a Landlord that is not leveraged to the eyeballs got to that position by taking on a cost they could just pass? Just like when GST increased from 12.5% to 15% you didn't see vendors dropping their price to offset the difference, it just gets added to the price.

Unfortunately I think we will just see the same here.

Until new net houses come to market the shortage works this way - Landlord sells rental with 3-4 occupants - FHB purchases and two occupy ex rental so one new homeless person enters the market for less rentals - supply & demand. Stop Immigration, stop bureacratic interference and obstruction by draconian legislation change and you just may see an improvement, otherwise its BAU.

You are sorely mistaken, rents literally cannot increase more than people can afford. Furthermore we are finally building more dwellings than is needed by population increase. Bringing rents up to market rent is one thing. Thinking market rent is going to double is some sort of sad landlord delusion/wet dream.

Are you aware NZ is already 80,000 dwellings short of demand? 80,000. And that’s now with an immigration freeze.

The government “hopes” to build 130,000 in wait for it...20 years

Well 80,000 is as good a guess as any I suppose but yes I am aware there is a shortage and I am also aware the private sector is finally eating into it after 10 years of increasing build rate.

The reality is no one knows if we have a housing shortage and certainly not to an exact figure. If you stated we have a deficit of 80k affordable homes then yes you could well be on to something.

Have you ever had 150 people apply for a single property?

No but I’ve rented several properties and never had any problem getting one... property I recently moved into I was the second person to apply for it and got it.

So why do we have thousands in Govt(Taxpayer) funded Motels etc?

People will have to afford it. Just like people had to afford the increase in prices of goods and services when GST went up to 15%. The tax gets passed on. The wealthy don't pay, the poor people do, thats how it has and always will work unfortunately.

Median rent in NZ is about $500 per week. Average salary after tax is approx $1000 per week. Not quite apples-with-apples, but I think close enough to show any claim that rents can double in a few years (barring any huge events like natural disasters or significant inflation) is absolutely crazy.

https://www.interest.co.nz/charts/real-estate/median-rents-nz

https://www.salaries.co.nz/cd/tax-calculator/average-wage

Of course you have a choice, you could always sell one of your houses for a start!

20-year bright-line test would have been definitely much better. But the extension to 10 years is better than nothing, as a first timid step.

Fortunr - There are no bad ideas here but increasing the brightline test removes a percentage of properties off the market for that time making availability worse..

With the current 5 year brightline most investors are happy to wait out that time and improve their properties and have the opportunity to sell and/or change their property mix etc.

With it going to 10 years it is too long for most people so many will change from property investors to speculators and just pay the tax, adding more fuel to the market.

We are at this point because of poor Government policy over decades and very low interest rates.

Removing interest deductions will increase costs that will to some extent be passed to the renter.

Tinkering around the edges creates distortions that Labour seems ignorant of.

If the Government believe tinkering around with the supply side will fix the problem then what about a immigration freeze until the market is back in balance ??

Extension to 10 years only applies to properties purchased from this weekend. If someone was purchasing with intention to sell in 5-10 years they may no longer proceed, freeing the property up for a non speculator?

Agree on immigration freeze...

Would have been better to have put a stamp duty on investor purchases make the barriers higher from the start.

Not increase their expenses which will just get passed on to renters. Those who can’t afford to rent on the market get put into already under supplied HNZ stock so will join the waitlist in motels a massive government cost.

Are their any other businesses that are taxed as a percentage of their turnover rather than on their profits?

Is there any other business that exploits people based on their basic need for shelter? Housing should be considered along the lines of education and healthcare, it is an essential public need. Its not the same as a business leasing cars for example.

That's why we have public housing. Don't want to pay market rent, there's always state sponsored housing.

It's the same reason why most people choose public health rather than to pay for private health.

And then there's private schools and public school.

Yes and with all things public they are bursting at the seams and a massive cost to government

There is no silver bullet. But good on Arden for making this courageous move. This could be a scarecrow policy, we will soon find out!

Until then, I shall continue having a laugh at the herald ‘journalists’ and opinion piece authors.

Comment of the day for me from Ashley Church: "The consequences of this are huge and will dramatically increase the tax bill to the average investor, at a time when most landlords are already losing money on the day to day operation of their investment." So if they are losing money on their investment what are they in it for?...

You mustn't have been around long. Property investors get in the game for the love of providing a roof over another person's head and the warm fuzzies they get for helping their fellow humans.

Making a minute loss from year to year is irrelevant when you frame it in that bigger context (and there was something about capital gains of 100k a year for the last few years, but that's definitely not an important part of the picture...)

Just informed tenants that rent is going up by 30%. Not well received but Labour government to blame I am afraid. Sad as they are nice family.

Is that a joke or for real?

Yes. I'd just signed off 6 letters on my desk this morning.

All of them begins with "As you may be aware..." and ends with "Yours truly."

I'm betting, given that the changes don't come into effect until Oct 1st, and the whole purpose was to get speculative investors to sell, that if that doesn't look like happening in a few months, AND especially if it looks like the cost is just being added to rents as many are saying they are going to do, then the Govt. will step in with further measures to stop this.

Basically, they are saying to investors, if you can't stomach the increase internally, then sell up, putting your house on the market for a FHB. And just as importantly, if you can stomach it, then don't take advantage.

Sounds like they will have to implement further measures.

Is that to make up for the huge reductions you have been making all the time, as interest rates went through the floor???

B727... so hopefully the unoccupied sin tax on empty houses in urban areas is in the pipeline and you are budgeting to pay the extra tax on your empty rental.

What I don't get about bright line test is whether or not it's being enforced. Bit pointless arguing about whether it's 5/10 or 20 years when they don't even have the data on who is currently paying. Surely they can disclose the amount of capital gain tax revenue currently being received?

So will peoples baches cop all these changes?

Most baches exceed a 10-20 year investment, and keeping in mind if you held it before now you only needed to hold it for 5 years max.

The interest deduction issue is only a concern if you Air BnB it.

Can anybody tell me why all those new laws come into effect 4 days before year end? All those new regulations always start on odd days in March. It is a nightmare for accountants.

And secondly, thank you, we now have one of the highest CGT taxes in the OECD, effectively mainly taxed at 33% or 39%. So far I have been a really good landlord, kept up with maintenance and always keep the rent in the lowest quartile. This will change now and I will always increase the rent to the maximum. Renters you can thank Labour for this. I know who I not vote for next time. Being a landlord is a business like all the other businesses but they can still deduct interest as a cost. The laws in this country are really odd. Why not building more affordable houses like Labour has promised? Only enough supply will stop house prices from rising, not this money making scheme. I will certainly keep buying houses or building them but the rent I charge will go up significantly and I will hold on to them for longer.

There really are a lot of low IQ posts around about how landlords dictate the rent instead of the market.

Please tell us all about how you slashed the rent you charged when interest rates were dropped to almost zero.

I agree, I wonder how many weeks of not finding a tenant before they decide to meet the market in terms of rent.

Don't feel bad raising rents, it's government driven inflation- there's nothing we can do about it.

Haha whats the government got to do with it? I thought you are running a business? can't you do it without a big fat subsidy?

What a lot of landlords never seem to be able to get their heads around, is that the country overall is much better off is a large percentage of people own their owns, and aren't having to pay weekly rent.

Then it was 100% the right thing to do if the Treasury disagreed with it.

Hahaha nice comment

Question / Hypothetical situation here.

Say you buy a rental and you plan on selling it in <10 years, surely it now becomes in your best interest to do as little maintenance on it as possible. If you decide to spend 100k on a renovation to make it nicer, you'll pay tax to earn the money to pay for it and pay interest on the money borrowed to do the same, but you'll get stung 33/39% for the value added to the property. Surely this encourages slumlording.

Improvements are still an expense against the investment and get deducted from the overall profit before tax is applied.

The only change is regarding the deduction of mortgage interest to your yearly accounts

If you are happy getting bottom dollar for your house when you sell it maybe, seems like a cutting off your nose to spite your face philosophy.

The leader of this country held one real job, demonstrating pots and pans at Farmers. This government has no regard for businesses and the people who contribute to this burgeoning debt.

Property investors, and mainly the highly leveraged ones were definitely making government debt worse, by getting a subsidy to get rich, while pricing out owner occupiers from buying houses.

Deductibility of interest could prove problematic- we have a strong body of case law that says that interest is a legitimate cost of doing business. Would the new proposals survive a judicial review? Expect to see that part quietly dropped before October.

As long as they don'y change the law so that residential properties can't be owned by businesses.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.