Property website Trade Me Property recorded its biggest ever drop in average asking prices in May, while the number of properties listed for sale on the site surges.

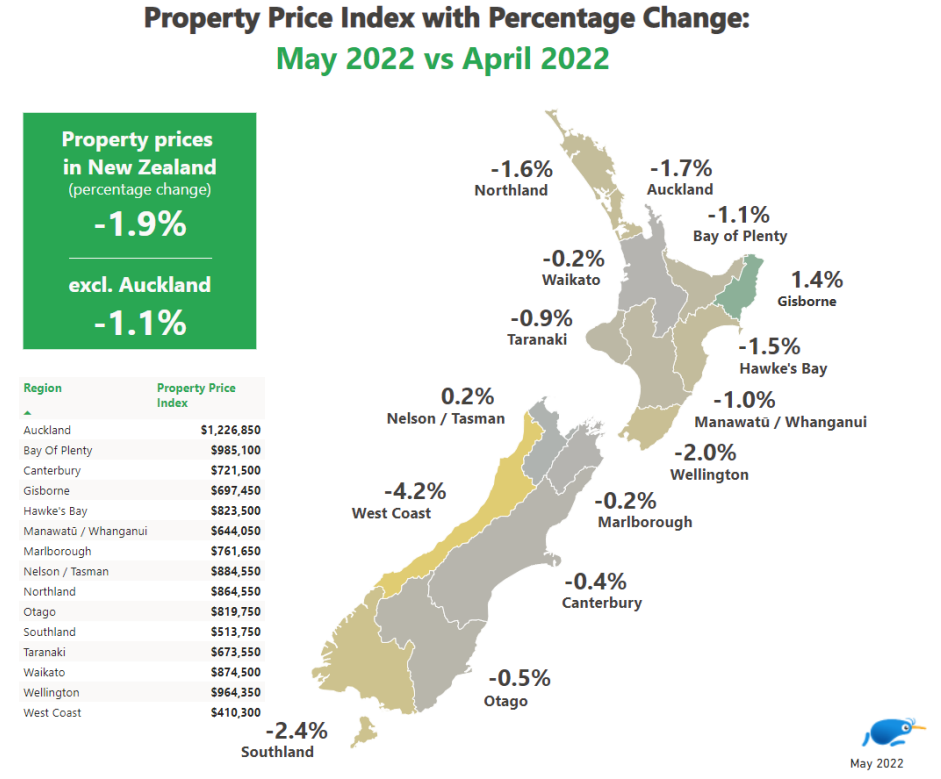

According to the Trade Me Property Price Index, the average asking price of residential properties listed for sale on the site was $949,700 over the three months to the end of May. That's down 1.9% compared to the three months to the end of April.

That was the largest month-on-month decline the website has ever recorded.

"Often prices cool a little as we go into the colder months, but last month's data is beyond anything we've seen in previous years," Trade Me Property Sales Director Gavin Lloyd said.

"The whole market is in flux and we're seeing this in every corner of the country," he said.

The biggest asking price decline was on the West Coast where it was down 4.2% for the month, while the smallest declines were in Waikato, Nelson/Tasman and Marlborough at -0.2%.

It was also significant that the average asking price declined by 0.4% in Canterbury, where prices have been particularly resilient until recently.

The first chart below shows the average asking prices throughout New Zealand and their monthly percentage declines.

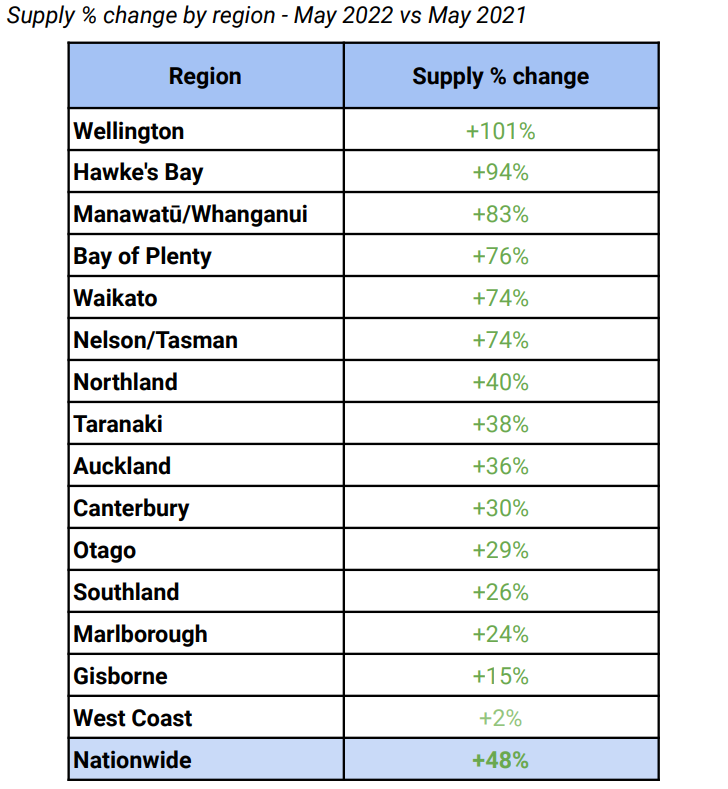

At the same time asking prices have been falling, the number of properties available for sale on Trade Me Property has skyrocketed, with total listings at the end of May up 48% compared to a year earlier.

The biggest increase in listings was in the Wellington region where they more than doubled, while the smallest increase was on the West Coast where listings were up just 2%.

The second table below shows the annual percentage increase in listings in all regions.

The comment stream on this article is now closed.

Trade Me Property

Total Residential Property Listings on Trade Me Property

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

133 Comments

That's going to make a lot of people happy on this site.

Only happy that commercial reality is finally going to apply after more than a decade of it not.The speculation driven disconnect of asset prices from income has been of almost biblical in its scale. Accordingly any speculators who literally loose their shirts in the next 48 months have no one to blame but themselves.

You would have to be a particular kind of crazy not to celebrate one of life's basic necessities becoming cheaper.

I dont even feel like cheaper is the correct term ... just a sensible % of your childs income.

Hail the Queen for some good news.

I take it that it's going to be a gloomy day for you... may it continue

Why may this be Yvil ? .....if property prices keep falling, some builders/contractors etc on new builds, will lose their profit margin or sell at a loss ....they then won't be able to pay their debtors ......then these parties will be forced to off load staff .....inflation will keep rising in this far away land at the bottom of the world .....unemployment will rise ....more businesses would be forced to close (so many have already with covid) .....standard of living drops etc etc ....... why would this make anyone "happy" ?

The rebalancing process is necessary. The govt can keep the build rate up by backstopping demand.

Hardly ....I hope the govt can step and take over these building projects and keep these people employed .....but as economic conditions get tougher, the banks increase their "stress" interest rate for mortgages....so makes it harder for first home buyers.

Indeed, government employing these builders absolutely seems the best approach. Kiwibuild might finally have builders with which to build.

These builders that stopped getting competitive quotes for inputs and started taking kickbacks for loyalty to one brand/colour????fletchers/carters….blue/green who cares

serves many of them right….

I know a chap who got the gm role for a merchant out west….that one merchant/outlet was paying out a million dollars a year in “loyalty payments”

the end user contracting a builder doesn’t see these kickbacks

and it’s allowed the distributors of the products to become very inefficient

Ah yes that is so, very much so. Lots and lots of backs to be scratched and options to exploit. Whole environment is corrupt. Overheard in a car park a builder yelling into his phone yes,yes realised he had underquoted for all the glazing so then was to reduce the glass to cheaper specs and will get it back that way. The customer will never know the difference.

This is why we need a mandatory industry insurance scheme instead of the taxpayer always having to clean up. But it's also why the industry is completely uninsurable and can never hope to be underwritten.

It is just the beginning.

Yes, it has not really started yet. But once it does start, it is going to be unstoppable, and it will continue until houses come down to justifiable/sustainable levels. There is a looong way down until prices reach a sustainable level.

And what price in your eyes is sustainable for a lets say a 100m2 house in an average Auckland suburb?

Large UK cities like Birmingham and Manchester have average property prices of ~$500k NZD. Perhaps NZ properties should be a little more expensive due to how inefficient our construction is and the earthquake standards required etc, so maybe $600k average?

Of course if you talk to people in the UK they think their prices are too high and many are predicting falls there too, so I may be being too generous.

I was thinking 450k for a modest house in, say, Mt Roskill.

lol, I guess its good to have a dream.

I woudnt even want to pay that for a place in Mt Roskill.

No, at that price even with a far bigger drop in the market than I expect will evenuate it would be a complete gut and rebuild job, I can see why you wouldn't want to go near it. Might even be better to feed it to an excavator and start from scratch.

3-4 Times main earners income and 50% of partner especially if likely to produce children so houses $4-600K.

The average USA house price is USD375k so also NZD600k

And that figure is after huge recent price increases which will most likely drop off as the full extent of this economic shambles comes to fruition

In Birmingham and Manchester you would be getting an old small terrace (attached) house with no off street parking and a postage stamp section on average I reckon. Maybe we are about a 20% drop to get that?

On the other hand, you would likely be getting a double-brick solid home with cavity wall insulation, a foot of insulation in the roof, PVC double glazed windows and central heating. Long lasting and not much maintenance required.

My house in the UK in a similar city has off-street parking and a large section, currently selling for the equivalent of $350k NZD.

Jimbo - Try this one - https://www.harveyscott.co.uk/properties/15461356/sales - uk wages roughly on a par pound to dollar, Stockport is a middle income suburb of Stockport 10 miles out of Manchester so easy commute train/bus or car with plenty of local shops and public amenities and comparable to Avonhead Christchurch. NZ property prices well out of step with incomes so will fall substantially.

What is an average property in Birmingham or Manchester? If it's an attached townhouse with barely any section then no thank you!

Sounds like the sort of thing on offer in Auckland nowadays

Isn't justifiable/sustainable all relative to interest rates?

700-800K

Winter will see these declines snow ball.

TimeToPanic

I see what you did there.

With home prices up @60% over the last two years, this doesn't even register.

566 Brand New Terraced or Town Houses listed for sale in Auckland on Trademe as of today. Some are still under construction. But this number will grow week by week. Prices for these homes still seem to be detached from reality IMHO. You can rent an equivalent or better property for less than the cost of servicing the mortgage.

On track for a 50 to 60% correction from the all time highs based on debt to income ratio. Good-bye credit cycle , hello economic cycle.

Yes, the time has come to pay the piper. Prices will halve in real terms, and this was unavoidable and just a question of time. It is time for specufestors to finally learn the big lesson that housing, like all investment vehicles, can go down as well as up. Considering how crazily overvalues NZ housing has become in the last few years, a big market correction is well overdue and beneficial to the real economy in the longer term.

Market forces and economic fundamentals will reassert themselves, there is no doubt about it, and the RBNZ can do very little about it.

They could move the inflation target band to 4-6% and cut the OCR.

The problem with this is it would seriously erode the integrity of our currency. The govt needs the NZD to be respected by the population of NZ has a means of exchange & a store of value.

If all OECD central banks act in concert. Then none of them need fear an outsize currency devaluation. As it was with the Covid induced money printing. The corporations of the world need to know that persistent 4-6% inflation will be tolerated. Profits can be maintained. They will have the confidence to raise pay rates to match inflation knowing they will not be left holding the bag of elevated payroll costs if the higher interest rates succeed in destroying demand.

That would cause an inflationary spiral, they would probably end up needing even higher interest rates.

Following last weeks USA inflation the Fed may move up 0.75% this week. Orr will need to consider NZ OCR next move up 1% or NZD fx will deteriorate even further, driving up NZ inflation massively (roughly half NZ economy is tradeables).

I agree Jimbo, historically interest rates need to be 2-2.5% above inflation to curtail so 8% inflation = 10.5% = interest with tax taking the difference to leave you square net.

Westie....they should have just set the target band to -5 to -10 back in 2020 and then we wouldn't have needed to print any money back then and created the mess now....

Does that sound like a solid idea?

Orr if they had just looked at NZ inflation (the stuff we can control) then they also wouldn't have needed to print any money back then and created the mess now

In March 2020 the RBNZ and government did a multitude of things all at once on the mere expectation of asset prices falling. When asset prices began rising they feigned ignorance for as long as they possibly could. At what stage of an actual asset price decline will they intervene again to stabilise ? Crown limos and your own 757 to jet around the world in can be very addictive. The press gallery love it as well. Better than the daily Covid briefings in the Beehive.

"In March 2020 the RBNZ and government did a multitude of things all at once on the mere expectation of asset prices falling"

The outcome was that they prevented asset prices from falling. But it was from the forecast deflation that they responded to (not directly asset prices...although we all know its correlated right?)

Likewise now, the reverse is that we have inflation which they are responding to and falling asset prices is the result of discounting future cash flows with higher denominators.

The outcome was that already stupid house prices rose 20% in 2020 and another 28% in 2021.

Yes that was the result of fighting deflation.

Now we are fighting inflation.

Prices will fall - a bit (20% max) but COSTS of new houses are going up considerably over the next year - so NEW house prices are not going to drop, because they simply can't - material, labour & admin costs. But there could be a situation where very few new houses are built for a few years.

By this time next year, you basic cost of $3,500 / sqm will be $4,500 - $5,000. But the houses will actually be better.

Sounds familiar??

What about the land....of which there is plenty of around the country....and isn't directly impacted by inflation costs like materials and labour.

Yes, land prices are where the falls will show up. I had shares in CDI.NZX which is a property developer with a large landbank and a wad of cash in the bank. They are down ~30% in the last few months which implies a significant fall in the value of their land.

I see Fletcher are now down ~40% from their peak a year ago so there is likely some truth that building rates will fall significantly, too. Either that or the market is suspecting the current high margins in building will not persist (or more likely, some combination of the two).

Prices react to supply/demand and as demand falls price is the elastic andif builders try and maintain cost per sq m at even $3500 so a modest 150 sq m house will have a build costs of $525k plus land so close to $1 million say $800k to be generous less $200 k deposit (good luck with that or Bank of Mum & Dad have helped) so borrowing $600k BNZ 3 year 25 year term will cost $3945 a month - $47346 PA out of net income = Gross income over $100k and little or any discretionery disposable income = misery but at least a roof over your head.Conclusion Mr Builder & Suppliers reduce costs/profits, increase productivity lest the Bank sells you assets to repay your debt, the perfect storm has just arrived.

definitely more listings in whangarei but no sign of a drop in price expectation,except maybe in the area around where the new kainga ora complex is being built.

This is the perfect place for singautim to post his/her Hutt valley report

It's just start, if market can go north for 40 straight years, than the possibility of going south for at least 5 years should be expected.

Have never owned any property other than my own home. How the market goes up or down is therefore scarcely relevant. My property sits relative to the market, as boats in the harbour, up and down on the tides. Imagine that there is not a small percentage of similar households in NZ. Guess being like that should make me sleep better, but it doesn’t seem to though.

Yes, but to be more precise, the swings in the housing market are is only scarcely relevant if you also don't have a mortgage and the house you own is sufficient for your needs and is not a store of wealth for when you downsize in retirement etc.

If people think 1 - 2% falls month on month is miniscule, Ireland dropped between 6 and 9% in their first year of their property bubble burst and went on to be down 70%.

But we're not Ireland so it'll be okay.

Correct.

We just need to keep retiring farm land and planting pine trees.

Everything is going to work out fine.

This is a very important point. When various housing bubbles burst (US, Japan, Ireland, Spain) monthly falls rarely exceeded 1.5% per month … only Ireland saw falls of 2% per month and that was 18 months into the housing correction.

A lot of people have scoffed at the current falls as “insignificant”, or that the market is “resilient”. In context of other bubbles, NZ HPI falls of 2% per month points to a very sharp correction.

There is no guarantee price falls will continue for months/years (as per other examples) but looking at the current macro environment, I wouldn’t want to bet my life savings against it.

Very true. There's heaps of "pfft 2% is nothing" comments on Stuff.

Trevor Mallard is going to Ireland. First their housing crash, now this. The 'luck of the Irish' has well and truly run out.

The Evil Union has already screwed the ROI over just wait till the EU collapses and Ireland discovers just how the British thank them for their nasty divisive policies over Brexit. Irelands new national anthem will be Dont cry for me ROI ()Republic of idiots) and do enjoy the Mallard.

NZ house market and economy generally are very similar to Ireland in 2006. Results in housing market will be similar. Fortunately NZ banks are better capitalised so less likely to bankrupt the State and require IMF intervention. The next several years will be rough but that merely reflects the scale of correction required. Long term benefits will make it worthwhile

The asking price is down but still not selling, who would pay a million plus for a 3 bedroom box in Auckland on a tiny piece of land. NZD tanking making inflation even higher, rates climbing all this will add up to a major meltdown in house prices. Some building companies already insolvent, over leveraged will be huge financial trouble some look like trying to get out quickly at a loss but who will catch the falling knife.

November was the time to sell the townhouse on a postage stamp and move as a cashed up buyer to provincial towns and buying a McMansion on a paddock. Here's to all those who made the right call.

This is going to unravel a lot faster than anyone thought. The question is, is our central bank ready, or will they panic and over-reach to keep retail demand at a level that can sustain employment?

I think the real question is going to be whether its the RBNZ or the Govt that hits the panic button first. I can't see the govt sitting back and doing nothing as the economy and employment go down in flames..

I can see them doing something - which will make everything a lot worse because they do not understand or accept the economic consequences of their own actions. Look at their track record over the last 4.5 years.

Orr/RBNZ pumping up the OCR is the only way out. Wait for the "cure is worse than the disease" moans, some of us have been here before.

Grant Robertson is trying to rush through the property market insurance scheme to keep people paying their mortgages and the banks in gravy should employment fall. On the taxpayer, of course.

With average 3 bedroom house price in Auckland being 12 x average wage couples income not much RBNZ or Government can do but watch prices crash.

Come on guys, have some perspective:

Homeowners told: Don't worry about price drops, you've still made money

https://i.stuff.co.nz/life-style/homed/real-estate/128947057/homeowners…

Here's another "know a guy" story.

Person I know, number of investment properties. One property bought in ~2014. Tried renting it earlier in the year, couldn't shift it (wouldn't accept a lower rent offer). Tried selling the property in May (last month) and got an offer 1.8 times what was originally paid for the property. Turned it down as it wasn't as high as what a nearby property sold for in October 2021. Putting it back on the rental market, rental market has since dropped. At the end of the day, it will still make money when it comes time to sell. It is difficult to reason with blind greed.

Yeah, I think buyers should make offers at about max 20% more than the 2017 valuations.

Absolutely. Very good ball park for where buyers should be right now. If you are paying more than 2017 valuations x 1.2 then you are not getting a deal.

Something along those lines for sure. I was thinking what would I be considering if I were in the buyers market today...

First, where are interest rates heading? What are swaps and OCR doing for the next ~3months (short term time frame to keep the price adjustment as relevant to now as possible). Draw back through the history of swaps and OCR to find the last time things were at this level. Make a couple of broad assumptions based on median income and median house prices at that time. Adjust forward for both wage and CPI inflation. Compare the value against current median price and that might be the current price drop. There's no exact science. Best we can do is look back to when conditions were similar.

Unless you brought your 1st home in late 2021 early 2022. In which case the value of your home has probably dropped more than your deposit. So you effectively now have a net worth of zero. As the debt on your house is probably of a similar amount to what the home is worth on the market. Welcome to Mr Orr's casino!

Soft landing?

I think it will be a hard landing this time.

Very curious to see the REINZ figures this week!

Waiting patiently...

Is there a way to check when its out? Seems to vary between 12th and 18th of the month.

They seem to like releasing on a Thursday.

Just check this URL to see if it's released: https://www.reinz.co.nz/residential-property-data-gallery

They'll be out at 9am tomorrow (Wednesday).

Thanks Greg! Is this a super secret squirrel time you get each month or is there somewhere where we can find this out? :)

I'm picking HPI in Auckland to be down 13-14% down from peak.

To misquote the bitcoin squad:

- House prices double every 7 years

- House prices might stagnate for a while, while wages catch up

- House prices are dropping but you're still ahead

- ?

1 house = 1 house

Just don't mention the maintenance and rates and insurance = 1 house

- You just need to zoom out further

- Something something dollar cost averaging

Lots of chat on BTC tanking, not so much on the NZD which everyone holds?....

I don't hold NZ dollars. Foreign shares, gold and silver is the way to go.

After that blow off top in housing, it was clear that the NZ dollar was on its way down the toilet. More falls to come.

Dow Jones and Nazdac fell substantially today so hope you don't have US shares and can exit others ASAP - bonds down - the perfect storm has arrived many will drown NZ will get wet possibly soaked.

"Often prices cool a little as we go into the colder months, but last month's data is beyond anything we've seen in previous years,"

Above will be the new norm for it is not the end of two year bull run but end of two/three decade of Bull run.

Many hoping and believe that in NZ any slowdown in property market is shallow and short are in for surprise. When has it ever happened before that housing market is on the edge of crash and interest rates have just started to move up.

Government and central bank under the guise of pandemic has created a perfect receipe for disaster with no control as the only thing they knew is to print and throw cheap money.....high dose was given and was good while it lasted.

I mean the only out for the RBNZ/Govt is to alter the CPI target and kickstart another LSAP programme to drive down yeilds again.

would you really be surprised to see that happen ?

HAving worked for the banks for many years, I personally cant see more than a 20% drop. Any more than that and banks will be too exposed. They "own" the government, and will drop rates on their own accord before house prices drop more than that.

Posted a couple questions on this broader topic over the last couple of days. I think the relationship between NZ economy, Australian owned banks and NZ central bank will play out interestingly over the next couple of years. I don't think that RBNZ would mind exposing Australian owned banks for their risky lending over the last couple of years - and may even buy back bad debt, or at least transfer the debt internally. The question is (third time same question haha), in this scenario, does buying bad debt or bailing out a bank which is owned and operated in Australia stimulate the economy, and if so would it be the NZ economy or the Australian economy? Who owns who in that scenario?

That financial genius( idiot) Cullen missed the chance to buy The National Bank through the Cullen fund achieving some measure of retail interest rate control whilst profits would remain in NZ. I doubt Grunter has the gumption and knowledge to even start a defenceive policy to shelter NZ from the worst of the coming perfect storm. We are about to see creative destruction in action and hopefully The Greens/Maori Party are so destroyed and Labour marginalised politically for a decade or three.

Firstly, dropping interest rates won't necessarily stop price falls. I lived through the GFC in the US and prices continued to fall as interest rates dropped. Why? Because once falling prices are in the psychology of buyers, nobody wants to be the person who steps in first and gets their fingers cut off by the falling knife. Unfortunately, because of past events in NZ, we assume that falling interest rates = higher house price with 100% correlation (this isn't true).

Secondly, are you implying that our retail banks control inflation and funding rates? (which it could be argued they do, by creating money via debt creation....) Can you imagine how fraudulent it will look if inflation is at 10% and our retail banks say, 'bugger it, we're dropping rates to protect our over inflated residential property lending portfolio'. If anything, if financial theory is correct, as the likelihood of debt default increases, so should the premium for lending to risky debtors. I.e. rates should go higher as default risk increases...its just that we've been living in lala land the last 20 years where as the risk of default as increased, we've dropped interest rates....meaning we have provided even more debt to people who otherwise wouldn't have been credit worthy borrowers.

If inflation shows up (which is a reasonable prospect as demand in the economy drops), sure, I can see them dropping rates along with that. But I doubt they will do it while swap rates are still rising.

(And are you saying that banks would fraudulently rig the swap rate market in order to save the housing market?)

Yea a good point, 2009 -> 2021 gradual easing coincided well with house prices as it was going with the trend. Can't say they have no impact, access to credit and all of that jazz, but the scenario in Japan following the peak was the same again. Interest rates were dropped but by then it was too late and prices plummeted. Number of other factors at play then as well but stating the obvious that interest rate fluctuations are not 1:1 with house prices.

Worldwide, I don't think we have much reason to believe banks won't act unethically - or threaten governments - to make more or lose less money.

Really? Did you not follow the Oz banking Royal Commission enquiry a few years ago? Same banks.

Possibly misread my comment?

Definitely misread your comment, my apologies

None necessary :)

Don't think it is plausible that banks can lower mortgage rates to keep bubbles alive unless they're willing to significantly compromise their profits in doing so. Banks simply can't fight offshore bond markets for their funding.

Bear Stearns

When were we getting that deposit insurance scheme again?

Where's TTP aka "taking the p*ss" to allay all our fears of this "indestructable" NZ property market ???

Searching for doom goblins (lol) under his bed that have been whispering scary things to him at night about falling house prices

Good.

Long may they fall.

DTI in line with the rest of the world next please.

Would hate to have used "fake" money -equity - to have over leveraged into a handful of investment properties in the prior 12 to 24mths. Interest rates are rising quickly from historical lows and capital gain looking less likely in the short term. Will be a bumpy ride over the next 3 to 5 years if your in long term - where does the extra cash come from to pay mortgages??

TimeToPanic

"Long may they fall."

Too bad about the legitimate owner occupiers who face financial ruin? Or just acceptable collateral damage, just like they were on the way up?

The alternative is throwing more and more younger generations under the bus to protect those who have been put at risk by greed encapsulated in the last decades' politicians and central bankers. If there are real tears not crocodile tears, the government could always use the Aussie New Liberals' jubilee approach to help renters and owners without unduly bailing out speculators (as has been the approach to date).

TBH I think that's inevitable at this point, but contingent on a competent government response, which I'm not sure we'll get. The collapse in discretionary spend will be too great if we just expect OO to cop it yet again, and will further underline NZ as being a place where you pay through the nose for not being born before the 1980s and actually trying to get by on a salary/wage - even the professional ones that used to be a slam dunk for a middle-class life.

I'm not sure what my way out would be if I end up in negative equity. But keeping things on an even-keel is hard enough at the best of times with how hard getting by is day-to-day, and this country seems pretty average at mental health support. Consequences seem predictable at this point.

Might be time to start popularising the Aussie New Libs approach, eh. Puts the social pressure on to not just bail out the usual suspects who've been bailed out to date, but to let speculators bear the risk of their speculation while assisting those who bore the cost of speculators' greed.

Simple question: "Do you live in the house?" If so, give access to a state-underwritten FLP to let you ZIRP or LIRP the balance of your mortgage while your wages catch up - to give you a shot are maybe a retirement, or even a family.

If you bought an investment property, and were expecting the taxpayer to underwrite your interest-driven cashflow loss while you banked a tax-free gain or were just going to wear the brightline because it was worth it anyway, then that's on you. But it's time to stop pretending specuvestors and owner-occupiers are the same and have the same capacity to wear a loss of this size.

Seller are still in denial, the asking price doesn't reflect the full picture of what is to come. We are definitely for a big fall, not a soft landing. However, this is not going to be the Armageddon that they are trying to tell us. If you bought last year and you intend to live in your house and not sell, the price will be back in 10-15 years and you will have enjoyed your own house. I feel no sympathy for whoever bought last year in order to speculate with all the scarcity of houses that we had. So, at the end is not all that bad.

Banks have to fund, they cannot just drop rates unless RBNZ extend their Funding for lending printer , this is possible if we see funding dry up but not yet ….. buckle up Dorothy Kansas is going bye bye

Big equities crash here will do more damage then housing correction IMHO will mean everyone’s KiwiSaver is smashed

Our idiot leaders will now bring in a capital gains tax so that the theiving class can offset their losses..

They wouldn't have to allow capital losses to be claimable.

Realising the benefit of a deferred loss is an invitation to speculate for gain, otherwise it's worthless.

I did say "idiot leaders". Neither Orr nor Robertson have got anything right over the past 2.5 years and should have let the bubble go at the start of Covid, they had the perfect excuse. National were probably even worse busting their lungs with all the blowing into the bubble that they did. We should of had a capital gains tax as soon as labour came to power. It was voted for after all. If we had that, and hadn't bailed the property investors out with the rest's money during covid... things would be a lot better now.. .Now we are going to get a huge crash... and the debt is on the books. Just shockingly incompetent management.

We should of had a capital gains tax as soon as labour came to power. It was voted for after all.

It wasn't voted for. Labour dropped CGT policy like a hot potato when they saw the polling data well before the election. If they'd stuck with the policy it would have been Bill and friends presiding over the disastrous Covid response.

She created a working group when she came to power and only rejected their recommendation in 2019 under pressure from Peters: https://www.stuff.co.nz/business/112010254/government-to-make-statement…

Reading these comments makes me depressed, some of you guys are the 'glass-half-full' type

So what if the house prices drop, question is what are you going to do with that information?

One persons crisis is another persons opportunity...

Some of us are now primarily concerned with keeping a roof over our family's heads. The mood has shifted away from property investors who think being alive at a certain time makes them business geniuses.

A couple of interesting graphics to look at.

https://www.macrotrends.net/countries/IRL/ireland/gdp-per-capita

https://www.stats.govt.nz/tools/which-industries-contributed-to-new-zea…

"owner occupied property operation" am I understanding that correctly that they count not paying someone else rent as increasing "product".

Hamish - very interesting info. Shows how dependent the NZ economy is on property (the construction industry, real estate services, property investment etc). A downturn in residential property will have a really big negative impact on economic growth and could induce a recessionary spiral that will be hard to pull out of.

This is barely minimum - squeezed some bubbles out of recent two year gain, people still making hundreds of thousands. Some property in Rolleston marked price reduced need to sell etc, still more than 200k above their purchase price 2 years ago (which only 500k). Price need to go back to 2015 level to give young generation hope.

This is what you get when the experts at the Reserve Bank make useless predictions. Here are the last three 1 years rates I have had. 3.2%, 1.94% and 4.3% and all came with cash. The RBNZ poured fuel on a fire and it blew up in their faces. If you average 1.94% and 4.3% you get 3.12%. I don't see the end of the world, but prices from the ultra low interest period will be a thing of the past. The 2017 valuations predate Covid and are five years old and might be a starting point.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.