House prices may be declining and mortgage interest rates may be rising, but the amount first home buyers are paying to get their own home remains at or near record highs.

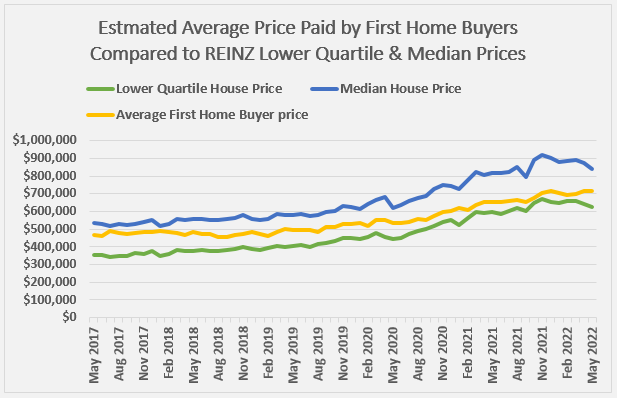

According to the Real Estate Institute of NZ, the national lower quartile selling price peaked at $670,000 in November last year and since then has declined by $42,000, dropping back to $628,000 in May.

Over the same period, interest.co.nz estimates, based on Reserve Bank lending figures, that the average amount paid for homes by first home buyers has increased by $11,000, rising from $705,000 in November last year to $716,000 in May.

However the figures suggest that the recent increase in the amount being paid by first home buyers has been entirely driven by those first home buyers purchasing a home with a low deposit of less than 20%, and consequently a high loan-to-value ratio (LVR) loan.

Between November last year and May this year the estimated average amount paid by first home buyers with a minimum 20% deposit decreased from $702,000 to $697,000, while the estimated average amount paid by first home buyers with less than a 20% deposit increased from $709,000 to $761,000.

Not only are first home buyers with a low deposit paying higher prices on average than their counterparts with a full 20% deposit, they are also borrowing a lot more.

The average mortgage approved in May for first home buyers with less than a 20% deposit was $127,000 more than the average mortgage approved for first home buyers with a minimum 20% deposit.

And low deposit buyers will be paying through the teeth for the privilege. Banks typically charge additional fees and higher interest rates for low equity loans, to reflect the higher level of risk involved.

So low deposit borrowers will almost certainly be facing considerably higher mortgage payments than their counterparts with a full deposit, and because they would also have less equity in their home, they would have less room to restructure their loan if they faced unexpected financial hardship.

The latest Reserve Bank figures show that although the proportion of new mortgages being approved to first home buyers with less than a 20% deposit is lower than it was a year ago, it has been increasing rapidly over the last few months.

In November last year when house prices peaked, low equity loans accounted for 34% of mortgage approvals to first home buyers and that figure had dropped down to 16% in March this year but had risen back up to 30% in May.

That could explain why banks appear to be reining in low equity lending, with the country's two biggest mortgage lenders, ANZ and ASB, both this week announcing a pause on new low equity mortgages.

Although low equity loans make up a relative small proportion of total mortgage lending, at a time when house prices are falling and interest rates are rising, a lot of the risks the banks face are likely to be concentrated in that relatively small number of low equity borrowers.

It may be that banks are simply deciding that the risks associated with those loans are currently not worth the extra business they could bring in.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

66 Comments

FHB should wait if they can. The banks may have done them a favour.

Better to leave NZ for a country where their skills are better valued and housing is treated more as a basic human right.

The estimated cost of servicing an average-sized mortgage in NZ is higher than raising a couple of children for people in their 20s.

Which country upholds housing as a basic human right?

High incomes and guaranteed housing, show me where to go.

I guess you were so keen to reply that you missed the word "more" - some countries are far better at housing their vulnerable. Nobody guarantees you a house but the politicians in some countries fight for the little guy, instead of the lot themselves owning 2.1 houses on average (248 houses between 120 MPs not including ones owned by their partners).

In 2020, Habitat for Humanity reported Japan having 3 homeless for every 100k people in the country and Norway had just over 3k homeless people.

Heard of a country called Singapore and its massive public housing programme that houses more than a-fourth of its population?

Edit: super tough to reply when you change your post 5 times in as many minutes.

Im not actually aware of many places governments uphold housing as a basic human right.

Japan's level of homelessness has almost nothing to do with the quality of social welfare afforded by the state.

Without capital gains of course they are not. Surely this is basic banking 101..?

Kneecap the "new entrants" to the market, while there are plenty of anecdotes of people trying to exit the market (Investor Facebook Chat Group).

One that made me laugh the other day though: "I'm so over this market". First offer fell through due to roof, so they replaced the roof, now second offer fell through due to builders report.

Landlord Website trying to bring some positive news........forgetting that for any activity need $$$$$ and BIG profit

https://www.landlords.co.nz/article/976520440/rules-for-massive-residen…

These changes are laying the groundwork for the next 30-50 years of demographic shifts.

Thanks for the link Carinaz, a very good article indeed

Says only economy in NZ is housing.

Spends disproportionate amount of time on property and investment sites.

Makes sense. If you watch nothing but kitten videos on YouTube, that's all you end up seeing.

Pa1nter, please read comment below, even Bernard Hickey......

Truth at time is painful !

Even on this website, check what news and articles are published most of the time and why because housing is the only economy in NZ - directly or indirectly.

Bernard Hickey too confirms, what many here have been commenting that only economy in NZ is Housing (Everything is Housing - Thanks to Politicians). RBNZ and Government have happily allowed themselves to be pushed in a corner where are forced (seems that are being blackmailed) to promote housing ponzi as can than justify their action of supporting the monster - HOUSING PONZI ( is anyone still allergic to the word Ponzi).

Newsletter / email from Bernard Hickey

"TLDR: We don’t have an economy. We have a housing market with bits tacked on. That’s evident again in a fresh set of data and news below this morning that emphasises how the economy, our health system, our tax system, our infrastructure deficit and all levels of Government and politics are held hostage by a too-big-to-fail housing market in the grip of home-owning median voters who can’t see any other way."

Inheritance and capital gains tax would sort most of that out and reduce intergenerational wealth buildups. Except... if you think people opposed capital gains taxes wait until you see the reaction to an inheritance tax.

I have argued for inheritance tax a few times on this site and can confirm - everyone seems to hate it. It seems to be a visceral disgust rather than a logical consideration of how best to raise tax from a population.

Maybe it's just a crappy idea? Maybe given that you've got 70 years of someone being alive to tax them, hitting them with the door on the way out seems like a less-than-ideal way of taxing people? Maybe not reforming the other taxes we have on the books to be effective and just falling back on something ideologically convenient is a crappy way to run a tax system?

This is the kind of thing I mean. Always considered as an additional burden rather than a way to distribute the burden away from workers where it currently sits.

It does shed a lot of light on how hard NZers must think it is for someone without a head start to succeed in society. Perhaps it would be more popular if we truly had the egalitarian society we sometimes claim to have?

The burden falling on workers is not due to mum & dad not getting taxed on their death. It is due to

- Corporate tax rates being lower than personal tax rates.

- Loopholes that allow corporates and high net worth individuals to minimise tax that aren't feasible for workers.

Ultimately all taxes (Inheritance, CGT, Gift, Land tax, etc...) fall to the worker to pay, as they can never "minimise" it.

All this talk is about rejigging tax to make it "fairer" but every change I hear is just changing the way to tax an individual. We need to change the system and tax corporates, trusts, and other non-human entities. So that we don't have to tax the individual.

And corporate taxes end up being paid by the consumer, usually the same person as the worker. It's all coming from the same ultimate source.

The trick is taxing in a way that isn't too objectionable, is relatively fair (which is subjective), and that incentivizes things that society thinks are 'good', or at least doesn't discourage them.

For example, income tax discourages productive work as you keep less of the proceeds. Capital gains tax discourages hoarding assets which don't produce an income. Inheritance tax discourages people from holding onto more money than they need to fund their retirements. Corporate taxes discourage companies from setting up shop in NZ. Land tax would encourage productive use of land.

Each has pros and cons and I don't see inheritance tax as being more objectionable than the taxes we have become accustomed to.

The thing is a consumer has a choice not to buy. A worker can't just not work.

What is "More money than they need"? What if you die early? Example: Breadwinner dies at 60. Partner then has to survive off that "inheritence". If that was taxed at 30% they would likely be destitute well before their time. What about Breadwinner dies at 50 or even 40?. Do you then tax the life inheritence that will be used to feed the two school kids that just lost a parent?

You also have the issue forming, where inheritence is likely to be a mortgage rather than cash. So what exactly are you taxing?

Yeah, it's always weird to read posts about how bad taxes on various other things are - e.g. land or capital gains - while the elephant in the room gets to go almost universally unmentioned: how ridiculously bad an idea it therefore is to tax productive work the hardest of all. As it makes no economic sense it can only be driven by the entitlement mentality of some who held sway over policy.

I'm with you MFD. Makes complete sense to me unless you want to move increasingly towards neo-feudalism and away from meritocracy

Sure let's all be poor problem solved.

Inheritance tax only acts to make the recipients poorer, not anyone who has actually earned their money. Can you honestly look at the world and think it's the trust fund kids who most need protecting?

Those "trust fund kids" are protected from any form of inheritence via the trust. I mean that was reason 1 and 2 as to why trusts boomed back in the 80s/90s.

- Hide the money before going into aged care.

- Protect the money so that the kids still got it.

As I said earlier. You aren't saving the worker from being taxed. You are only changing the timing around when they get taxed.

Inheritance tax would push a society closer to being meritocratic. The problem is most folk don't actually want a meritocratic society, they want to push their kids ahead of others.

Indeed, the Scrooge McDucks come out in force, quacking about "double taxation" as if that doesn't happen everywhere anyway. Intergenerational wealth buildup resulting in huge wealth inequality has knocked over empires quite a few times before, so we should be doing everything we can to prevent it. Instead people resort to their base greed instincts.

Just give everyone $10k through a CBDC 'Matariki account' and everything will be sweet...

I love a roaring inflation fire... More gas, more gas!

Not if it goes towards the 5% balance owing on the mortgage.

As soon as its announced watch the revolving credit balances.. new spa pool goes on the revolving credit, a month later $10k comes off the revolving credit.

Or its $10k off the balance already on the mortgage for the Tesla/Ranger/Jetskis, so the payments on that drop by $40/week, and that money ends up being spent somewhere else.

And those that don't have a mortgage?

It would be inflationary,

So much for people thinking FHBs would benefit from a drop in house prices… It will probably get worse as NZ enters a recession an FHB's lose their jobs.

Agreed, FHB's are actually far better off in a rising market where there is job security, prospect of capital gains and banks are lending. All things equal, mortgage repayments don't really change under either sceanrio - higher prices/lower rates means more of your mortgage payment goes to repay the loan and less on interest and vice versa.

The coming recession just bakes in another generation of renters, great for us.

Yes, them and over-leveraged property investors are both going to get choked out of the market if unemployment starts ticking up.

Another thing people don't mention too often is divorce/break up. FHBs are often in new(ish) relationships, still on their first marriage, etc. Having a house in negative equity (or one that is taking a long time to sell) is another complication to the misery of dividing up assets.

Not just an after-the-fact complication, also contributor to the stress on a relationship.

Yep - and then the mortgage payments are so high they can't afford to move out and rent another place... More than once I've heard of couples staying in the same house but living separate lives for this reason.

I'm still on my first marriage, been so for a very long time and I intend to keep it that way

I'd rather be on my first marriage and my umpteenth house, than on my first house and my umpteenth marriage

I think it's the middle managers that are at risk of losing job this time round not the FHB, in my industry anyway. Youngsters seem to be able to do twice as much for less money.

Land and Build package.....be aware as worst is to come specially if have not chosen Big builder (though even they can go burst but probability is less).

Happening in Australia...

Why “are first home buyers with a low deposit paying higher prices on average than their counterparts with a full 20% deposit, they are also borrowing a lot more.”? The house price is the house price whether you are putting in 10 or 20% equity. Yes the borrowing amount goes up on a 10% deposit but the house price doesn’t. Is this due to the Govt policy driving low equity First home buyers to new builds and developers capturing the buyers ability to access KiwiSaver amounts etc If so then borrowing less and buying a lower price “used” home may be better and probably give the buyer a back yard as well!

Yes. Investors can buy in the gap between what a FHB can afford for a second-hand vs a new build - so they can both out-bid FHBs and pay less, on top of which they secure the property much faster than the FHB, thus take lower risk. It's a shame, really.

Also, if the FHBs have the disposable income over-and-above rent to save the deposit (instead of using equity), chances are their on a bit of coin and thus capable of servicing a more expensive mortgage, than the investor reliant on rental income.

"Investors can buy in the gap between what a FHB can afford for a second-hand vs a new build - so they can both out-bid FHBs and pay less, on top of which they secure the property much faster than the FHB, thus take lower risk."

How ???

Provided they meet the criteria: a couple has access to an extra $10,000 FHB grant towards their deposit for a new build, over an existing house.

Obviously, that wont necessarily increase their mortgage gap 10x, but (from RBNZ stats) it quite possibly will allow them to opt in to a new build for $50-70,000 more than they can spend on an existing house.

This means, an investor could out-price an FHB on an existing home - which they then settle in, say, 6 weeks. The FHB, on the other hand, having experienced this a few times, gives up on an existing house and goes with an off-the-plans build, for a few tens of thousands more, which might take 18+ months to settle. (As has been noted many times, serviceability for the most part has not been FHB's main problem until the recent extreme prices).

A concrete example: one FHB (couple, $40,000 deposit sans grant), one investor($110,000 deposit), one second hand house, one new build.

The FHB can bid up to $500,000 towards the second hand house. But they can spend up to $600,000 for the new build.

The investor, meanwhile, can only go up to $550,000. But that doesn't matter - they can out-bid the FHB couple with ease.

Assuming each just slightly out-prices the other for the respective builds: the investor gets a second hand home for $510,000 with a balance owing of $400,000, whilst the FHB gets a new build for $560,000 with a balance owing of $500,000 -> or 25% more (ignoring for the moment that the investor was unlikely to bid more than what they were able to acquire the second hand house for, and the builder probably wasn't going to drop the going price). On top of this, the investor has a more favourable interest rate and may possibly be on interest only, meaning their debt is not just smaller but cheaper to service, dollar for dollar.

So, both have acquired houses. The investor have out-bid the FHB on the existing home (and if they're cheeky, rented it out to them afterwards - I've seen this happen!), but paid less for their house than the FHB. The investor also had the house settle much much quicker than the FHB, so acquire it as a security sooner. Nevermind the exposure the FHB also has to the builder/build going bust, or invoking a sunset clause, all while they're continuing to pay rent and thus still exposed to the risk of having their current home sold out from under them. A lot more can happen in the new build settlement time frame than the existing home settlement time frame.

Which is why I think it's a shame so many FHBs have felt they needed to go the off-the-pans approach, just to get onto the property ladder - since they're purchasing for security, which is achieved much faster with a second hand house.

What is the impact on that analysis of the investor not getting to deduct its interest payouts on the used house whereas they can on the new one?

That is a great question.

It's now a matter of choice:

If the investor foregoes the second hand home for the new build, now the FHB also get to choose if they will out-bid them or not - and it could go either way. From a security perspective, I would think the FHB would take the immediately available second hand house - or at least, they have the choice to.

But if the investor is willing to wear the extra serviceability costs, and targets the second hand house, the FHB have no choice. And that has been the landscape of the market for many years until very recently.

[Note this simplistic analysis ignores the effect having one house selling first has on the price of the other - the assumption being that if sold second, the new build had a fixed floor derived from building costs etc.; whereas the second hand house will be sold for a negotiated price between seller and buyer. But the maximum possible offer for the second-hand house will be whatever it takes the investor to outbid the FHB.]

So first home buyers with low deposits are paying more today than 6 months ago and also paying much higher interest rates… Unbelievable! Surely there has to be some personal responsibility taken, if they can't service the mortgage in the future

Is anyone going to take responsibility for pumping the market so high that it's put FHB's in a precarious position where they have had to over extend themselves?

Waiting for politicians and bankers to take responsibility may require some special patience... in fact I am not sure they know the word 'sorry' or 'accountable' any more (if ever).

Nobody has put them in a precarious situation stop blaming other people.

Well said Carlos! But it's so much easier to blame others, rather than look at ourselves

I agree - we are all responsible for managing our risk and educating ourselves about risk. Basically we dug our own holes or built our own palace.

That said - the consequence for FHBs of a bad investment will be felt by the FHB - whereas (unfairly) the consequence of bad decisions by the government and reserve bank leaders will not be felt by those individuals- but ought to be (else where is the incentive for the next leaders?)

Not all FHB are financial savvy folk like us on here. Just like I'm not savvy with electrical work, which is why I use an electrician and pay good money for it. Shouldn't the same apply to banks?

They make good money out of lending, so should bear responsibility in issuing the loans. Especially if in 12 months time they more than double the interest rate. Could the banks not see this coming? Billion dollar profits and they can't even forecast where their own lending costs will be in 12 months time?

You make a good point Dan, I reiterate the proposition tI made numerous times before: Let's include budgeting in the school curriculum. I know some people have a problem talking about money, but that's exactly what need to be taught from a young age. Firstly to debunk the myth that "money is the root of all evil" then secondly to learn to manage finances and understand simple, basic budgeting.

The Govt doesn't want citizens being good with money... clearly why it isn't taught in schools

idk, at least in my opinion (as someone who has worked in schools and in finance), most budgeting and personal finance courses are a load of crap anyway. A majority of people’s money problems are caused by deeper issues than not knowing how to create a basic spreadsheet and add up receipts. These include:

- being easily convinced by sales people/advertising/peer pressure to buy things

- having an enormous void inside them than can only be filled by consuming

- the inability to cook

- over-reliance on parents/partner for financial support

- having too much pride to ride a bike, take the bus, or be seen walking

- having insecurities and thinking that <insert product here> will fix them

- being bored easily (lacking curiosity) and thinking that holiday to <insert place here> is the only solution

- not understanding the probabilities relevant to most popular forms of gambling

- falling for ‘investment opportunities’ on Instagram

- etc etc

These things need to be taught in other ways. But definitely there should be some education about economic cycles and the reality of debt, things like that. It's hard teaching finance stuff to people who don't have money though, thats why most people don't start thinking about it until their 30's.

This is an amazingly useful list - thanks! I have two kids and am making notes so I can share with them. You have my respect!

Economics and Accounting aren't taught in schools these days?

But if everyone, or at least alot more people, were financially literate there would be more looking at central banks and government and asking WTAF.

Can't have that.

I had a go at my bank rep (as well as Labour & RBNZ) for encouraging and enabling what I considered to be socially irresponsible lending. Their response? Blamed the punters for keeping on paying silly money - and then implicitly also blamed Labour. Yep, pretty much 'nothing to do with us at all'.

Interesting to see what is happening to NZ property market from the UK given how inflated the bubble was in NZ Im surprised its taken this long although the UK is not immune and market is softening a bit over here too although we are a higher wage economy which makes a big differnce. Im thinking of returning to NZ with family in tow with Brexit, Ukraine War and terrible Tory government lifestyle change is attractive but NZ seems to have a fair few problems crime, crazy living costs being away for 17 years maybe I just have rose tinted glasses. I would have no or low mortgage in Auckland and be a highly paid professional but is it worth it should I be looking at Australia instead?

I am lucky to have married into an NZ family and my kids have grandparents and cousins here. If it wasn’t for the family connection I am not sure if I would choose here over the UK. I miss UK pubs and beer. In NZ you can have any beer as long it’s IPA. NZ has great beaches and generally friendly people but there is no longer a functioning state education system and it’s best not to need healthcare. Having said that, the UK weather is crap, the NHS is collapsing and inflation is 9%.Australia is either flooding or on fire. Perhaps NZ is not so bad after all.

In NZ you can have any beer as long it’s IPA.

So much. Hard to find good brown ales on tap these days.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.