House prices at the bottom of the market are down by more than $100,000 from last year’s peak in Auckland but have barely moved in Canterbury. This means first home buyers have been hit harder by rising interest rates in some regions and are less affected in others, according to interest.co.nz’s latest Home Loan Affordability Report.

It shows that the Real Estate Institute of New Zealand’s national lower quartile selling price peaked at $670,000 in November last year and has since declined to $630,000 in June this year.

The lower quartile is the price point at which 25% of properties sold each month are below and 75% are above, representing the most affordable segment of the housing market.

Normally a $40,000 decline in the lower quartile price would be good news for first home buyers because it would mean they need less money for a deposit and a smaller mortgage, which would reduce their mortgage payments, all other things being equal.

Unfortunately while house prices have been falling, mortgage interest rates have been rising, and between November last year and June this year the average of the two year fixed rates charged by the major banks increased from 4.08% to 5.43%.

So how would first home buyers have fared in that mix?

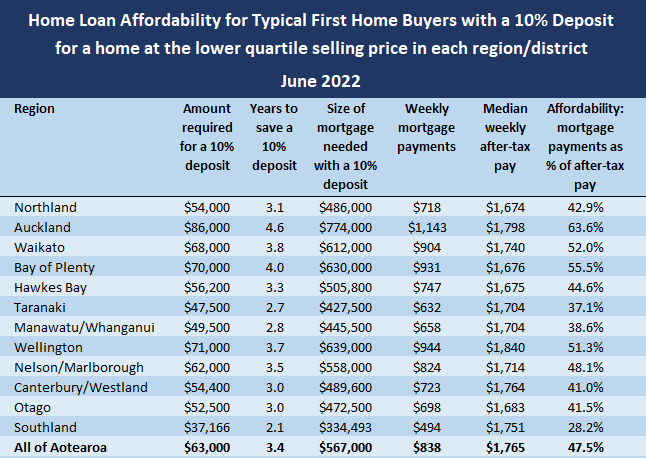

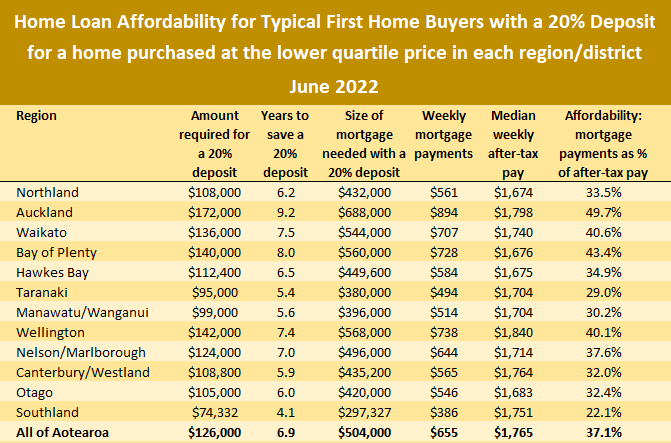

Firstly, the amount they would need for a 20% deposit on a lower quartile-priced home would have declined from $134,000 to $126,000, saving them $8000 (halve those figures for a 10% deposit).

Secondly, the amount they would need to borrow if they had a 20% deposit would reduce from $536,000 to $504,000, reducing the size of their mortgage by $32,000.

If they only had a 10% deposit, the size of their mortgage would have declined from $603,000 to $567,000, down by $36,000.

So far so good – the figures above suggest first home buyers are benefitting from the current market slump.

It’s when you factor in the effect of rising interest rates that things start to get tricky.

If a first home buyer had a deposit of 20% and purchased a home at November’s lower quartile price of $670,000, the mortgage payments on that would have been around $596 a week.

If they had waited until June when the lower quartile price had dropped to $630,000, the mortgage payments would be around $655 a week, up $59 a week even though the amount they would have been borrowing would have declined by $32,000.

If they only had a 10% deposit under the same scenario, the mortgage payments would have risen from about $770 a week to $838, up by $68 a week (allowing for the loadings banks apply to low equity loans).

So it’s swings and roundabouts for first home buyers at the moment.

However the figures in the examples above are based on national house prices, and while changes in mortgage interest rates are the same throughout the country, there have been big regional differences in what has happened to house prices at the bottom of the market.

There have been major price declines in eight regions – Northland, Auckland, Bay of Plenty, Hawke’s Bay, Taranaki, Wellington, Nelson/Marlborough and Otago, where lower quartile prices are down significantly from the peaks of late last year/early this year.

In the other four regions – Waikato, Manawatu/Whanganui, Canterbury and Southland, prices have only dropped slightly from their peaks.

For those regions, there has been more of a flattening of prices at the bottom of the market rather than a significant decline.

The one characteristic of price trends in all regions of the country is that prices are no longer rising.

The difference in price trends so far has had a significant impact on how much mortgage rate increases would have affected first home buyers in different regions.

In the country’s most populous region – Auckland, the lower quartile price peaked at $966,000 in November last year. By June this year it had declined to $860,000, a drop of $106,000 over seven months.

In the Wellington region the lower quartile price peaked at $785,000 in December last year. By June this year it had declined to $710,000, a drop of $75,000 in six months.

But in Canterbury, where prices have merely flattened, the lower quartile price peaked at $550,000 in February/March this year. By June it had only dropped back to $544,000.

What does that that mean for first home buyers?

The amount needed for a 20% deposit on a lower quartile-priced home in Auckland dropped from $193,200 when prices peaked in November last year to $172,000 in June this year, a saving of $21,200.

A 10% deposit declined from $96,600 to $86,000 over the same period, down $10,600.

That meant the amount needed to be borrowed to finance the purchase with a 20% deposit declined from $772,800 in November last year to $688,000 in June, a reduction of $84,800.

The amount that would need to be borrowed with a 10% deposit declined from $869,400 in November last year to $774,000 in June this year, down by $95,400.

But with mortgage interest rates rising from 4.08% to 5.43% over that time, how would that have affected mortgage payments?

Based on the figures above, they would have increased from about $859 a week in November last year to $894 in June this year, for buyers with a 20% deposit, an increase of $35 a week.

For buyers with a 10% deposit, the mortgage payments would have increased from around $1,111 a week to $1,143 a week, up by $32 a week.

So the trend for first home buyers in Auckland where prices have dropped substantially since they peaked late last year, is that they now need less money for a deposit and a smaller mortgage to buy a lower quartile-priced home, but will be facing slighter higher mortgage payments.

What about in Canterbury where prices have merely flattened?

Not surprisingly, the amount needed for a 20% deposit on a lower quartile-priced home in Canterbury has barely changed, dropping from $110,000 at the March peak to $108,800 in June, down by just $1200, while the amount needed for a 10% deposit is down by just $600 over the same period.

The size of the corresponding mortgages have dropped from $440,000 to $435,200 with a 20% deposit and from $495,000 to $489,600 with a 10% deposit.

Over the same three month period from March to June the average of the two year fixed mortgage rates increased from 4.41% to 5.43%, which pushed up the mortgage payments from $509 a week to $565 a week (+$56) with a 20% deposit, and from $656 to $723 (+$67) a week with a 10% deposit.

That means first home buyers in Canterbury are so far getting very little benefit in terms of the amount they need for a deposit and the amount they need to borrow, but are getting hit harder by rising interest rates.

But that doesn’t mean first home buyers are better off in Auckland than Canterbury.

Auckland remains a hideously expensive place for first home buyers and it’s likely that even with the most recent price falls in the region, first home buyers on average wages are probably still priced out of the market.

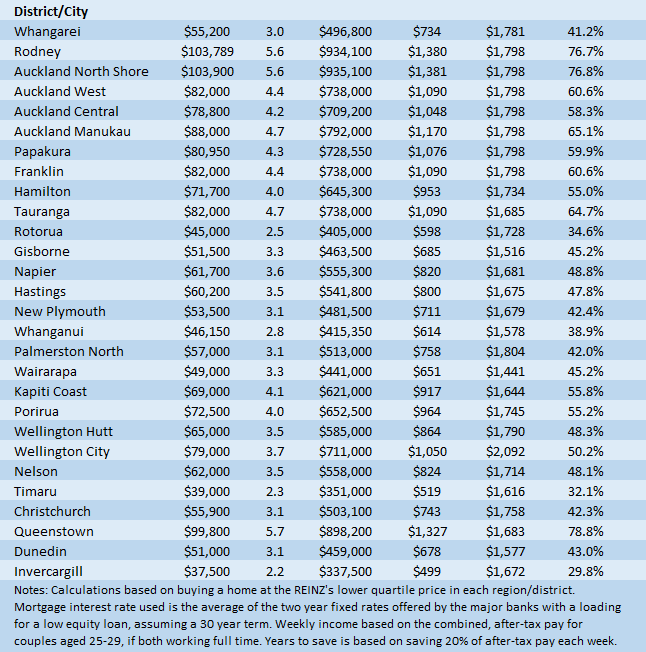

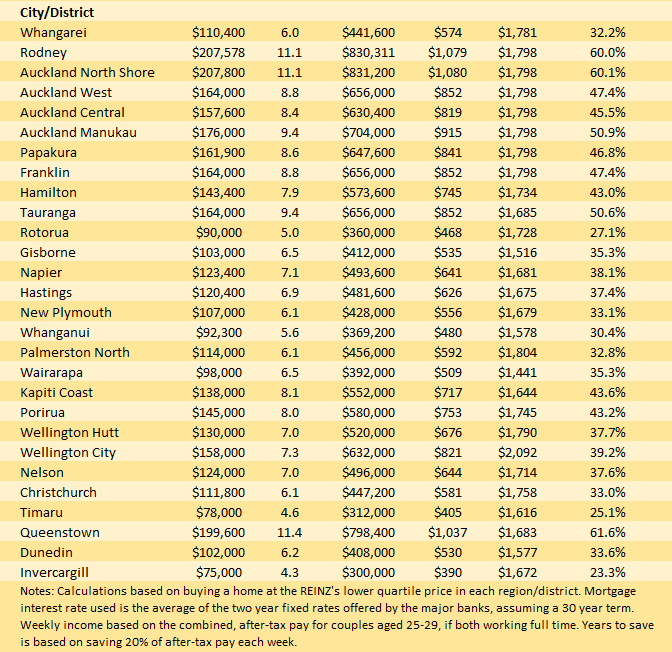

The tables below show the main affordability measures for typical first home buyers in all main urban districts, with either a 10% or 20% deposit:

The comment stream on this story is now closed.

*This article was first published in our email for paying subscribers. See here for more details and how to subscribe.

148 Comments

Hutt Valley Market Update 18th July

Whilst I dont track the Auckland market. I can comment in regards to FHB's - starting to see more sales in the past few weeks with the majority of sales under the 750K range. Those who have read my previous reports would note that the bottom end of the market has been stagnant with very few sales for most of the year now starting to see it move - but not without some hefty price reductions first.

I've written a little bit more about those price reductions in the "market valuations" section below

Current Market Listings

545 houses on the market- Down 22 on last week . I predicted a couple of months ago that I thought listings would drop to the mid 500’s by end July and this seems to have delivered. I do expect listings to come back with a roar in mid August as Spring selling season approaches, I think we will also see a number of houses that have been delisted returning to the market as sellers hope more people will go looking for a house.

We have now had 5 months of less than 100 houses been sold in the hutt valley – making the average number of houses sold each week 25. This is well down on last year where 40 houses were selling a week and at the peak in March 2021 50 houses a week were selling.

545 houses on the market with 25 a week selling means there is 22 weeks stock on the market. Down on the 26 weeks SOH recorded in April but very high for this time of the year.

House Price Reduction

299 houses have a listed price – this is down 22 on last week

69% of the houses listed with a price have reduced their price since listing

The average markdown has increased to 98K.

Of those that have listed prices (pool 299) -59 have reduced their prices by 100K

13 have reduced their prices by over 200K, 6 have reduced their prices by 300K and 2 now has reduced their price by 400K with the biggest reduction been 425K (a total 25% reduction)

The data continues to show the majority of houses listed are under 900K. The Median house price for all 545 listings is now 800K. (Down 30K from a couple of weeks ago and the lowest Median in the last year)

Market Valuations

The latest QV valuations (valuations by QV which are updated every month and give an approximation of a houses value) have dropped $180K since Jan for the Hutt. This is interesting because new RV ratings are due to be calculated in Sept and released in Nov. A number of people who bought in the last 12 months are going to find their house is worth a lot less than what they paid for it.

As for homes.co.nz valuations – some massive drops in the last round of updates released last week.

- Woburn (the Hutts most expensive suburb) – average house price dropped 90K in value in June alone and is down 240K from $1.65M (in Feb 22) to $1.41M

- Petone – dropped 50K in value in June and is down $180K from $1.19M to $1.01M and will drop below $1M this month.

- Wainuiomata (the Huhts cheapest suburb and attractive to investors and FHB’s) – dropped 35K in value in June and is down $140K from $870K in Feb to $730K

Houses sold vs houses removed

My records show 233 houses listed with a Price have sold YTD (up 10 from last week).

I have records of a further 210 houses (up 19 from last week) that have been removed from the market unsold YTD.

28 of those houses removed from the market have been listed on the rental market.

Length of time on the Market

- 412 houses have been on the market for over 30 days - 76% (last week it was 413)

- 283 houses have been on the market for over 60 days - 52% (last week it was 295)

- 199 houses have been on the market for over 90 days – 37% (last week was 208)

- 123 houses have been on the market for over 120 days - 22% (last week was 118)

- 75 of the houses have been on the market for over 150 days - 14%

The number of houses on the market over 60 days is now over 50%. This has risen from 32% of houses in mid March (one in three), 1 in 3 houses have now been on the market more than 3 months , 1 in 5 have been on the market over 4 months and 1 in 7 have been on the market over 5 months.

Rental Market

This week the rental market has 209 properties for rent up 87 on this time last year, – when just 122 houses were for rent.

Average rental price reduction is $53 a week. There continues to be around 10-15 listings a week which are new builds and some attractive rental prices with one discounting its listing price from $750 to $650 to rent it, it’s a 3 bedroom 2 bathroom townhouse in Petone so some good rental prices for renters at the moment. Possibly the best rental market in the last 10 years – not so good for landlords

At the moment the percentage of properties listed at $650 is 39% still well below the 53% of houses listed over $650 on the 23rd March.

I was born and raised in the Hutt Valley. My parents still live there. I flatted there when I was at university. My wife and I are educated, with postgraduate degrees, and I have a six-figure income (my wife is off work to focus on the pre-school kids). I'd like to raise my family there, but it's too expensive. This is a nice analysis, but $650/w for a rental is just eye-wateringly expensive, and that's what you consider a good price at the lowish end. It feels like a punch in the stomach that I can't afford to raise my family in the same place I grew up; an inter-generational backwards step.

On a similar note for Auckland. What do you suppose is the annual household income required to make Auckland feel "affordable" to a family? $400k?

Probably 250K minimum, but more like 300K.

I think it depends on the amount of equity you have, I would not live here in AKL unless I had the equity I do, would probably be in CHCH

lots in the press of AKLers selling to head south.

Yeah good point. If you have lots of equity, then arguably 150K is more than enough to have a pretty comfortable life.

Let's assume 500k equity, 2 adults + 2 kids, looking for a decent 4br say ~220+ m2. I'll restrict myself to the shore because I know it well enough.

If you're talking about the far parts of beach haven/glenfield/greenhithe, you might be able to get something for $1.5m. So that's a $1m mortgage. Current P+I repayments about 9%, so $90k a year in mortgage costs. Bank test rates are nudging 8%, so P+I test ~11% = $110k pa. So probably something like $225k gross to make it workable, and that's with no contingency for rate rises (or other problems).

Median type suburbs, say northcote-forrest hill-albany, probably more like $1.8m. Now you've got a $1.3m mortgage, currently $120k pa to service with testing at $143k. Probably need $300k gross, again without a lot in the way of contingency.

Top third of suburbs, say northcote point-bayswater-devonport-takapuna and up the bays, probably $2.1m. Our hypothetical family still has enough equity to stay low LVR. Current servicing $144k pa, test $176k pa. At least $350k gross.

Obviously more equity helps. But it's not pretty if you're talking about current prices + current interest rates.

Avo on toast for Xmases and b'days only

It is all so mindblowingly stupid.

What a stupid waste of life, waste of time, waste of energy, to be stuck paying off such a huge mortgage.

And all because our corrupt governments thought that high house prices were "a good problem to have" and our corrupt RBNZ was pushing "the wealth effect".

It is all going to look even more stupid when house prices crater, like they did in Ireland (but faster).

What a stupid waste of life, waste of time, waste of energy, to be stuck paying off such a huge mortgage.

While I tend to agree with you, the vast majority does not. I have no evidence to support that though. It's just the feedback from the BBQ and water cooler chatter.

I can't believe how docile people are.

They accept debt slavery without even a complaint. Our parents could pay off a house in 20 years on one income. We just happily accept so much less.

Last time I checked, I was a person, I have raised complaints ;)

Still here?...this must be the longest good bye evfer!

I'm still on the internet, yes.

Where are you going?

I think most people are very risk averse. A house is a security blanket and helps people avoid asking themselves what they should do with their lives. The whole debt slavery set up precludes most from doing much else except work to fund the debt.

Its considered safe, and a sure thing here in Godzone.

At the bottom of all that rubbish economic and monetary policy of the last decades that's caused this stupid situation is speculator entitlement mentality. The same thing you see when anyone seeks to change policy, e.g. to implement a CGT. Whining, shrieking entitlement to feeling wealthy by passing huge debts to following generations.

It's not stupid at all Fitzgerald. What are your options, live with parents, rent? Renting = No pet's, kid's can't paint their room's, rent reviews, having to move. All so unsettling for a young family. Yes the first years are a grind, but find me a person who did this and regretted it after 10 years. I'll wait.

Taleb's turkey: "Show me another turkey here at Bob's Thanksgiving Turkey Farm that regrets living here. I'll wait."

Ask me again in 5 years time and I'll show you hundreds of thousands of people who regretted it.

We don't need to have such high house prices. Other countries have better priced houses. We just pay too much because of poor policy, corrupt central bankers and stupidity.

Dp

Firtzgerald,

'It is all so mindblowingly stupid.

What a stupid waste of life, waste of time, waste of energy, to be stuck paying off such a huge mortgage.'

You summarised my feelings, wish I could like this twice.

I was about to make a similar comment. It's all well and good to drop $800k on a two bedroom shoebox.

Need space for kids? Good luck.

Mortgage payments are usually not much more than rent. If a family saves deposit while renting then a mortgage has to be a breeze, even with the usual extra costs of ownership.

Yeah, but rents are too high. They eat up too much income. NZ rent-to-income ratios are much higher than almost every other country.

A friend of mine rents in central Melbourne for $420 per week for a large (~80sqm), new 2 bedroom apartment. Even with falling rents in Auckland CBD there's no comparison.

Not many couples making 400 k a year. This has to change and only way is housing market crash which has started and will pick up speed as rates climb. Anyone over leveraged will be watching deposit disappear and soon be in negative equity no other way to sort out mess from last five years fiasco.

I was born in Christchurch & moved to the Hutt Valley mid High School.

When I had one income, was paying rent, had young kids & a modest 10% deposit, we moved back to Christchurch & bought our first home, stayed for 5 years until we had enough equity to buy back in Wgtn. It was a good place to raise young kids, larger section, a lot of free outdoor space/parks, cheap & good public transport, cycling easy...

I know that it will depend on your job situation however good houses are still a third less in Christchurch, same as they were 45 years ago

House prices are 10 years behind, society is 20 years behind.

Sounds like paradise.

I hadn't been back to Christchurch since the earthquakes until a couple of years ago when we started looking at property & spent a bit of time there periodically.

While the rebuilding is still got a long way to go the potential is there for a really good vibrant walkable CBD (say within the 4 Avenues). I also noticed peoples optimism & positivity were more present than Wgtn & the Hutt which have spent at least a decade now going back to the gloomy dodgy environment they were in the 1990s (dysfunctional city councils in both). I live in the Wgtn Eastern suburbs and hardly ever go into town since the Central library closed.

ChCh "Society" back when I lived there in the 1960s & 1980's was a very stuck up, rigid & close minded place. I sense that the earthquakes & the mosque shooting have broken a few barriers between people.

Great points.

If I didn’t have such an established life for our kids in Auckland I would definitely consider ChCh.

There are some folks in the internet who would argue that Christchurch is too "anglo Saxon", therefore you are a racialist for considering moving there.

As nouns the difference between racist and racialist

is that racist is a person who believes a particular race is superior to others while racialist is a believer or advocate of racialism, a theory that race determines human capabilities.

Some "folks in the Internet" should get a life.

See that Hosking article in the Herald talking up Christchurch? the photo was a nice street with a tram and barely a car in sight. Remember the outrage from Hosking when they turned one of the 5 lanes of Hobson Street into a cycle lane!

It's people like Hosking that are poison to democracy. A charismatic little man with a big mouth who is an expert on everything.

Your description sounds like a historic figure dominant through the 1930’s and early ‘40s…

The reason i use $650 as my measure for a rental price is this is the price where it becomes cheaper to buy than rent (at $650 a week – someone can borrow $550 000 at 4.5% - average FHB loan is currently $548 000).

$650 a week in rent is also the point at which the average hutt valley house price (currently at $800K ) will produce a rental yield of about 4.2% - anything under 4% in a market where capital gains are difficult to achieve starts to become an unattractive yield (especially when you can get 3-4% interest on a1 year term deposit)

For Lower Hutt which has always been one of NZ's more expensive rental markets (because of lack of stock) the amount of rental listings over $650 is declining - currently 39% are listed over $650 and the amount of new builds coming to the market is dragging the price of rentals down where renters can now get a decent townhouse for average rent ie $650 - when 12 months ago they would have been paying $700-$800 a week for a similar property.

There was article about an agency on one roof.They had 90 listings shown, but another 50 off the list but available.

do you see or know of this in the hutt?

Great Analysis as usual. Are many of the properties that were removed from the market now being presented as rentals?

28 of listings this year have been removed from the market and listed as rentals.

10 of these were listed in June - none in July so far.

"Average rent reduction is $53 per week" has anyone told Seymour and Luxon this. They said that Labours rule changes (Healthy homes, CCFA, removal of tax deductibility etc) would increase rents and that was a justification for reversing them. If Labours' changes are having a positive effect for the average kiwi, surely they should remain? Unless National and Act are only there for landlords rather than first home buyers and tenants. How many landlords are there? I hope for their sake there are enough votes in it for them.

Email them. I wrote to 7HL. Someone in his office at least clears his inbox, and if there are enough messages the same you might actually see something come out of it. I'm not naive, but writing was better than complaining on the internet.

My message was"

Here are some policy changes that will win more votes than they lose, and actually match National's traditional values.

- Stick up for homeowners, not landlords. There are more votes from centre right people going begging on this point than you'd retain from landlords. As a symbol of good will, sell your rental properties on the open market. (Did you know that on some internet forums you're known as "7 houses Luxon"?)

- Focus National's business policies on small and medium business owners. There are more votes here than for bigger businesses. Many people working for big businesses want to start their own business.

- Stop relying on immigration to boost GDP. This puts strain on accommodation and services. Some is needed for skilled workers, but the definition of 'skilled' has not been what most New Zealanders think it is. Again, more votes in here than its corollary.

- Put up a population policy to a referendum and pledge to abide by it, within reason. This will steal at least half NZ First's votes. New Zealand's population has doubled in 30 years based almost entirely on immigration. No government has ever asked the public what level they want, resulting in too much change, too quickly. Definite vote winner, and in the public interest. After all, politicians owe it to people already here to improve their lives, not those not here yet.

-Articulate foreign policy clearly, not reactively. Appreciating things are delicate, a few issues I see as important are:

- Chinese expansion into and militarisation of the South China Sea

- Support for the State of Israel's right to exist and right to self defence while condemning human rights abuses

- Support for the Pacific, especially with regards to climate change.

- Stand up for free speech. This is what swung my vote for ACT - National looked weak on free speech 2020, on top of the above issues. The erosion of free speech in NZ is a clear and present danger. There are no monopolies in the marketplace of ideas.

- Eliminate the 5% threshold. This was part of National's downfall - not enough mates despite winning the popular vote. Sure some fruit loops might get in, but even fruit loops deserve representation in the House.

I might write something similar to Seymour but tailor it to broad church libertarianism that benefits NZers not pure church libertarianism that benefits (who exactly?)

Be careful with this stat

The rent reductions i refer to is the difference between the rental price the property lists at and the last rental price (before the property is delisted - I'm assuming when it delists the property is rented for that last price) So as per my article a new build in Petone listed at $750 and its current listed rental price (it is still on the market) is now $650 so this property has a rental reduction of $100.

This doesnt mean the cost of renting in the Hutt Valley is lower than it was this time last year. Although I suspect it may be slightly cheaper to rent or at least on par with last year - but i dont have data on this.

A property can have a rental reduction ie the rent asked decreases the longer its on the market for lots of reasons. The most common reasons will be

1. Ambitious landlords who think their property is worth more to rent than the market thinks - or the landlord might need a certain amount of rent to make repayments/ cover costs etc.

2. An oversupply of properties - more properties coming onto the market for rent vs the demand for properties in that area mean landlords need to lower rents to make their property more attractive to renters. - I suspect this is the actual driver of rent reduction in Lower hutt- the number of rentals is at a record high and double this time last year.

I am worried about the economic disaster that seems to be unfolding, on a global scale actually. Relatives have been trying to sell property in China, sold after 3 months. This must be engineered, as it is global, and our central bankers cannot be so stupid not to foresee what deflationary asset collapse will mean. Some people here seem to think they can benefit from this collapse, as prima facie it seems to favor renters. I genuinely don't think that many people will be able to benefit from the outright economic collapse at hand. There will be massive economic hardship, akin to 1929-1932. Apparently, the plan is to create a severe crisis so the masses will cry for even more central control. This is truly scary, we already have a 'pandemic', a European war about to escalate into a world war, a 'vaccination' campaign that is experimental in nature and based on genetic manipulation (in the West at least). How much more?

God defend New Zealand!

> Auckland remains a hideously expensive place <strike>for first home buyers</strike>

Fixed that for you.

Good try, but the strike tag doesn't appear to be supported here.

Let's see if the < s > or <del> tag has the desired effect...

<p><s>strikethrough test</s></p>

<p><del>strikethrough test</del></p>

edit: hmm, nope. I'll leave this here for you to read. 10 points to Gryffindor if you work out how to do it

I wonder if this works: <b style="text-decoration:line-through;">Test</b>

Nope :P (tried span, p ,font, b). LOL, back to work I <b>go</b> (b test for sanity).

Looks like the editor takes plain text, then converts it automagically.

Yeah I spent 5 minutes trying to get it to work and then gave up and left it. The "About text formats" link (below, right when you're editing) says strike is supported, but I can't get any of them to work so I'm obviously doing something wrong.

All you've done wrong is give up so quickly... never say die!

<html>

<head>

<style>

p1 {

text-decoration: line-through;

}

</style>

</head>

<body>

<p1>Strikethrough Test 3</p1>

</body>

</html>

Edit: Hmm, nope

True, really needs an average of 1.1 not 1.4, and a median of 900k not 1.05. Nothing new here, incomes dont match the house prices. The townhouse explosion could help the median.

I'd love to see half of what you point at, actually :D...

Auckland remains a hideously expensive place f̶o̶r̶ ̶f̶i̶r̶s̶t̶ ̶h̶o̶m̶e̶ ̶b̶u̶y̶e̶r̶s̶

How about the $3m to $5m buyers, how are they fairing?

*Only* $1143 pw for a lower quartile home in Auckland, with a 10% deposit. Sarc on.

I'm glad you have avoided 'vanilla' language in your description of this. Because it IS truly horrendous.

Successive governments over the last 20 years should hang their heads in shame.

Slow Hand Claps.....

Let's look at what a FHB would face in buying a 2 bed shoebox in the middle of nowhere, in a lower value location...

Purchase Price 750K

10% deposit = 75K

Mortgage = 675K

30 year mortgage @ say 5.5% = $884

Throw in insurances, body corp, rates (all things not needed when renting), and that's an outlay of towards $1000 per week on housing.

For a shoebox in the middle of nowhere, in a low value location.....

Just rent it to the government for social housing - problem solved.

Yeah, but think about the pride of being a home owner :P

And once mortgage rates are 7%, that will be $1036 per week, plus insurance, rates, body corp

Not hard to see why or how demand for new build townhouses is falling off a cliff…taking the residential construction sector with it

Yeah, I have a mate who bought an AKL shitbox a year ago, and he's a builder. Talk about having all your eggs in one disintegrating basket.

Note too that 750k is the exception rather than the rule. Most townhouses in low value locations are advertised for early 800’s…

Also note those prices made a bit more sense with interest rates at 2.5%. It is very likely that prices will come down more to match the new interest rates.

yep, although Given construction costs, developers won’t be able to bring them down much more without getting more than minimal profit. But they might simply have to accept that reality.

Some may just be looking to escape without a loss.

Stage three of the boom and bust cycle.

Stage 1. Make as much profit as we can screw out of the system.

Stage 2. Make a profit commensurate with the risk.

Stage 3. Make enough profit to not incur a loss.

Stage 4. Make as small a loss as possible so we can survive until the good times return.

Stage 5. Cash up everything so the banks don't have to and keep the credit rating.

Stage 6. To hell with everyone, thank God for the family trust.

Nice. Maybe edging closer to halfway between stages 3 and 4???

Yes, that movement between stages 3 and 4 is a slow and reluctant mental shift, but when they finally look around and see others starting to bail, then it's a rush for the exits.

The answer is simple.

Rent for a bit and watch from the sidelines as the whole corrupt ponzi burns to the ground.

It would appear that climate change is your only hope for that to happen.

...and hope you still have a job as the ripple effect wipes out anything that relies on discretionary spending?

A mortgage does not confer job security.

No but pretending that property crashing and burning will have no spillover effects and that people on the sidelines currently will be in a position to buy is sort of only telling half the story.

People on the sidelines are standing further from the fan.

Regardless of whether or not they will be in a position to buy, they are much more likely to dodge the excrement splatter.

Anyone who has been through a downturn before knows we will all come out the other side fine so what if your house is only worth half of what it was a couple of years ago in the end a 50% to 70% crash is only way most of the population will be able to have own home. GV27 why would this no be good for New Zealand most people want to see kids and grandkids grow up with hope of having own home and not talking via FaceTime to some far of land.

I'm not saying it won't be good in that regard. I need a more affordable option for my next family home so I'm on board with that side of it.

I'm just not going to pretend there isn't a downside; and this whole country is set up on the presumption people will spend more than they earn. If people stop doing that, it will come to a grinding halt. That's going to affect everyone in some way. Yes, house prices might be much cheaper, but that doesn't mean that you'll have a job with which to pay for an affordable house. The young and older workers tend to bear the brunt of downturns disproportionately, remember.

Bang on. And its not just the kids we want the best young teachers, nurses, doctors, engineers to stay and others in to want to come here.

Why on earth would they move somewhere where they cant afford a decent home for their families.

It is a visible, sad lazinees and greed - of older investors, lazy/thick governments and rbnz who have driven our prices sky high they should be ashamed.

I agree. You are getting some interest on your saving and house prices are going down.

Leave.go to London, Sydney ,KL,NY. And a hundred other amazing places….my advice is to the young ones is go see the world.

three years in London or twenty in Dennemora…..it’s a no brainer

things that can’t last forever don’t.

✈️ ✅

Don't underestimate the will of those in power who have portfolios to try to use taxpayer funds and government and monetary policy to protect their own wealth at a cost to many other Kiwis.

Absolutely. The Ponzi is a black hole, and all of NZ's resources are within the event horizon.

Would anyone advise kids to buy a cheap house in Auckland stuck in run down area helicopters flying over head most weekend cars stolen. 30 years paying $ 1100 a week just enough money left over beans on toast every night can’t have kids because if you lose one wage for a few months you will lose your house. This is why young couples are going to Aussie would be crazy to even try buying In Auckland. It is so good to see this housing market tanking give it two years and the market will be more affordable for them as it is youngsters have already lost almost three years of their life’s with covid.

You forgot the ram-raids, more trendy these days!

How about a bit of homicide thrown in here and there for good measure

On a full moon the place is like a zoo with no cages. It won’t be long before people start community gangs to keep streets save.

In real-estate speak, west auckland is full of "character".

Haha

’Bohemian’

Maybe people can live a Gangsta fantasy

Ow yeah - vibrant.

We weren't advised to do this - but this effectively what we did. We purchased our first home in Henderson in 2013 for $440k. We had never ventured into West Auckland except to play high school sports against Kelston/Massey. Quite the experience...

110 square metres of floor area on a cross lease section....not a flash street, but we lived in the house for 7 years. We tidied up the small gardens, tidied up the fencing which we paid for (no point asking the neighbours...), new carpets, repainted interior and exterior etc. We sold up in 2020 for almost $850k and purchased a house north of Auckland - 200 square metres of floor area, 2.5 acres for $900k. Requires a bit of work.

"Kids" shouldn't be buying their first home in Pt Chev. Start small, and have a goal to live in Pt Chev in 20 years?

I live in that general area so I feel qualified to comment. You've almost got the nub of the problem, but the Pt Chev bit is irrelevant. Your Henderson cross-lease section now requires a $170K deposit, and it's now an even bigger mess from a congestion and social issues perspective. So you now not only have to save up a $170K deposit and pay down the mortgage on the rest as interest rates rise, but you also have to hope like hell that prices keep rising at stupid levels to ever be able to afford anywhere else.

Private school kids buying houses in inner-city gentrified suburbs are a crappy outlier and not a great reason to overlook the fact that the thing you benefited is kind of the reason we have a problem.

It's a fair point you raise - it did only work realistically because of the capital gain we made, however we certainly weren't guaranteed the capital gain when we took a punt to buy in an area well and truly out of our comfort zone. We were terrified that we were buying at the peak of the market back in 2013, and people were telling us that we were crazy to be paying that much for a house on a cross-lease section in Henderson.

In hindsight we would have been better off buying the $800k house in Northcote (probably worth $1.5m today), but I was uncomfortable with a mortgage of $800k for a first home back then. I guess I'm of the view that I don't see prices tanking massively, and over the long-run prices will rise, however not to the extent of the last couple of decades. I'm just saying that FHB's might need to buy outside of an area they were born/raised to get on the ladder.

"Lower your expectations and move further out"?

We've been down this road, it ends up with people having to buy outside Auckland and commuting into it, and the development around the fringes adds a premium to the formerly outer suburbs that are now more centralised. It's simply not a sustainable argument, either financially or from a quality of life point of view.

But you say "I was uncomfortable with a mortgage of $800k" to get a much better house, but now they have to stretch to 800k just to buy something crap.

I was in a similar situation to you, but our mortgage repayments weren't that crazy, we could still afford to go to the pub or eat avo on toast, and were also able to put some extra in after a few years of pay rises and pay it off quicker. Now I think it will be a long hard slog giving away almost all your income just to get that undesired Henderson house. At least now we have some inflation to help out though.

Don’t rate your comment. At all. Sorry.

You can see my calcs on this page. Even ‘starting small’ and buying a really tiny 2 bedroom townhouse on a ‘postage stamp’ in a low value location is unaffordable to anyone who doesn’t earn at least an upper middle household income (say 150-180k).

Your comment is good in theory, and maybe was valid 10 years ago, or possibly even 5 years ago.

But certainly not in 2022. But maybe in 2023 (if prices fall 30%?)

Who said the kids were trying to buy their first home in Pt Chev? The usual "below the belt" comments from team out-of-touch.

Also, why did you need 110sqm of floor area as a first home? I made do with 80sqm in 2017.

Do you have kids NZdan? That's why we needed 110sqm. I've got several mates who refuse to look anywhere else but the North Shore - they are still renting. Pt Chev was a generalisation, but you get my drift.

Yes I do.

Team out-of-touch is apt. Only about 5-10 years out.

Not having a dig at you, but that $440k house cross-lease house is now priced at well over a million.

Kids don't have a chance these days.

Exactly. And apologies to USkiwi for my blunt comment. But I think it’s justified.

Don't worry, I don't take it personally. I've just looked at the house on propertyvalue.co.nz - it is saying high-end $920k, low-end $820k. It is a myth that every house in Auckland is over $1m. We are only in our second house and I'm not yet 35 - I'm hoping I'm not that far out of touch.

Let’s assume 875k. Plug a 725k mortgage into a mortgage calculator and see what that spits out at 5.5% over 30 years…

So professional "kids" earning good money in demanding jobs and contributing lots to society should be raising their kids in crappy neighbourhoods so that boomers can live comfortable, privileged lives in the areas with good schools? OK, thanks. Nevermind.

Now, knuckle down and pay those folks' pensions.

Loving these comments

Beats paying off a boomers mortgage on their 3rd rental property. Don’t get me wrong, we were pretty frustrated that after 7 years qualifying in our profession we still couldn’t purchase a house in the area we preferred. I think where our generation will differ - born in 88, is that we won’t get rich via rental properties like the last generation.

I hear you, USKiwi. Horribly frustrating situation - and good on you for doing what you could to make the best of a bad situation.

Don't worry, both the American and Chinese property implosion will spread massive contagion to us. Especially the Chinese. I'm surprised their economic plight whether accurate or not isn't referenced more both here and on MSM, given they are our biggest export customer.

Nah, a Chinese bust could never happen! X, Audaxes and Keith reckon China is well on its way to dominant power status!!!

I charted the NZ house price index from 1991 until pre-pandemic values and added an exponential trendline at 6.136% annual increases. This trend intersects HPI multiple times and for multiple periods is very, very close to actual HPI. Its shows peak HPI is 30.6% higher than the extrapolated trend which requires a 23.6% correction to return. Previous peaks above trend are Jun 2007 of 20.9% and Sept 2016 of 7% with corrections below Jun 1993 -11.7% then return along trend untill Sep 2001 -20.9% and Jun 2012 -10.8%. This current peak was the highest by far from our trend line in 30+ years. Even if we correct back to our existing trendline which is possible we still face an issue, incomes have not kept up anywhere near 6%+ annual increases. Buying entry level next year when we see peak house price crash, people on good and great incomes will be paying most of their income for the rest of their lives and not able to pay down their mortgages enough to upgrade significantly. This is even taking to account mortgage rates returning to current levels from however high they will peak next year.

I would love to see this. Too bad there's no easy way to share it on here.

https://pasteboard.co/xvTnHkXDwDv4.jpg

{kind=link}

I have not made a presentation style graph, I used this for my own reference.

Nice! So a fall of around 20% would bring the HPI back in line?

Somewhere near that takes us back to that trend from the peak. However, if we overshoot it could be more.

Also to consider is that we knew the housing market was in a bubble even before pandemic pressure was applied.

The culture of safe as houses investing in property and factors like stimulus and rediculous interest rates for prolonged periods means we could well correct to an intrinsic or fundamental value and anywhere in between.

Good points, Juzz. Markets seem to prefer overcorrecting, as opposed to just correcting. I think the market is bound to overshoot on the way down, which will be great if you ask me. The future for house prices will be interesting, no doubt.

Yup. Anyone who has bought in the last two years is poked. They're either rekt or stuck. And they're meant to smile because this is a 'good thing'.

I mean yes, if you're on the outer looking in. But if you took the people we trust with our financial system (PM/RBNZ Govt/Finance Minister) at their word and did your best to secure a home for your family (even if you did the sensible thing and bought a modest starter home) then you're in trouble.

WIld swings in house prices and interest rates only work for a very small group: those who can downsize or those who are mortgage free and looking to invest. Guess what demographic that tends to mean will win out again.

Its about 160,000 houses of which I suspect a fair number were investors. They don't have anyone but themselves to blame if they thought those super low interest rates were here for ever.

I'm sure these people didn't give any thought to those who were living on their interest payments.

Yes anyone who bought in the last two years is facing varying degrees of unpleasantness. We as a country voted for a party that stated prior to the election that they knew about the housing problem and were choosing to protect existing homeowners rather than remedy the problem. I'm not advocating for them or their "opposition" but to their credit on this issue, Judith made it clear that we needed to act on it.

Many people who are mortgage free will be looking at retirement, now with inflation, they are looking at losses in savings and other investments and increased cost of living while transitioning to a fixed income.

Those looking to invest will no longer see property as the infallible investment it once was, they will be limited by equity requirements, rental requirements, tax deductions... and so on.

Hopefully, we will see investment strategies shift towards productive enterprises that will stimulate and sustain our economy. Rather than creating wealth inequities.

https://www.youtube.com/watch?v=452XjnaHr1A&ab_channel=GuilhermeBarbosa

Very interesting comment. Thanks, Juzz.

Post it in https://www.reddit.com/r/PersonalFinanceNZ/

Done

It would be great to put the interest rates on the same graph. Then we would see a major driver of the 6% pa trend line.

Then extrapolate interest rates, which should allow you to extrapolate prices.

I have such a chart at my disposal CPI vs OCR from march 1988 and HPI overlayed from March 1990. As that is the dataset available, I'd like to have previous years and maybe I'll look into sourcing those because I believe there is some valuable info from the 70s.

I will post up a chart tomorrow, I think possibly a log-adjusted HPI vs linear CPI & OCR may be easier to interpret.

I think there are more factors involved to make predictions, demographics play a big part that gives me a reason to be bearish on housing over the next decade. However who knows what policies, if any are used to intervene as our banks are predominantly offshore so bailouts would be a very hard pill for voters to swallow. Will we see a reversal in CCCFA or an early reduction in OCR? who knows

so the quoted median income is household income, not personal income.

Everything is terrible. Always.

It really does go to show that a 10% deposit really does not cut the mustard - it's buying pain for yourself and

10% should be fine next year

Good luck to the government on its Kiwibuild Reset (Mark 4?)

haha

Very telling that there have been no articles on it! It seems even the media ignore anything that Megan announces about housing.

Are you expecting a cheerleading squad because the thing that was meant to give us 100K houses is going to now give us the infrastructure to build 8K houses? Frankly I'd consider not having more coverage about this to be the PR win of the century for the government.

Not talking about the infrastructure stuff. Talking about the quite large increases to house price caps for the scheme that were announced on…Tuesday night.

Just thought it Interesting / curious as to the lack of articles.

Of course the changes will make jack all difference because of the rising cost of finance.

Heh. I looked at the new income caps and though to myself: the people smart enough to be on the new income caps are smart enough to wait. FOMO fades when you see prices falling more than your deposit in a few months, and staying renting is far cheaper than having a mortgage. Especially as every new abode listed on the market lessens the likelihood of your landlord successfully selling out from under you, in the race to the bottom.

Probably somebody else has pointed this out but the extra cost to service the mortgage is only for 2 years. Then both hypothetical families get the same rate.

The difference between them after that, is the amount they paid for their homes. It seems to me this is a decent trade off for less debt and is likely to get better and better while we have high inflation, almost irrespective of the interest rate.

Absolutely, I would stress test myself at 12% mortgage rates (albeit a very tight budget). If we see double-digit rates next year and low prices then it is a good trade-off for high-income first-home buyers. Fix for a year, maybe two, and then the tough times are behind you.

This article says it all: https://www.oneroof.co.nz/news/41857

“I would be gutted if it happened in our street. People don’t want to live next to terrace housing. Especially if they’re paying $4m.” No one is really protecting “special character” or whatever else, they are just plain NIMBYs who are being sponsored by a disgraceful council. This is just utter corruption the likes of which we don’t normally see in this country.

So the government have told Auckland council to allow density everywhere, and the council have said ok but not near the centre because it is so precious and rich and “character”. Have the government accepted that? If I was the government my counter offer would be 30 stories everywhere within 5km of city, because Auckland Council are obviously taking the piss.

Tumeke Mackerel the inside out city.

I can tell you now that 100% the government will be submitting on the plan change and demanding that the ‘special character’ overlay be removed, in its entirety.

I hope so. It’s outrageous that Devonport was excluded from the intensification. It’s perfectly situated for a ferry ride to the CBD.

Amazing the NIMBY entitlement mentality should apparently overrule issues of pollution / emissions, economic sustainability (maintaining sprawl) and congestion from more sprawl. Messed up.

Yeah the transport plan doesn’t quite match the housing plan.

I think they will find the metro tube needs customers to be economically run.

Replacing fifty busses from my eden between 7-9 am won’t do it

That’ll devalue the area for sure, guess no more “Beverley Hills”.

Flat in West Auckland, enquiries over $800,000

2 Beds,1 Bath,1 Living area, 88m² Floor, 132m² Land, 1 Off-street parking

Enough space for a young family, but how about the cars, ride an electric bike or what.

Will immigration increase, yes from those countries suffering from poverty/corrupted governments/authoritarian regimes. No from developed countries where one can choose where to live and work. Can't think of a young bright lad working in farms.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.