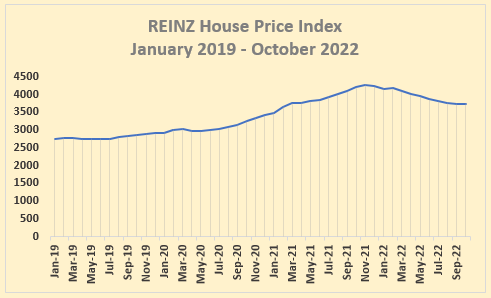

Was October the month in which house prices finally stopped falling after almost a year of steady declines?

The Real Estate Institute of New Zealand's House Price Index (HPI), which is probably the most timely and reliable measure of house price movements we have, because it is based on sales as they become unconditional and is adjusted for differences in the mix of properties sold each month, posted a 0.2% gain across the entire country in October.

That's a marginal increase to be sure and represents more of a flattening trend than an increase in prices. But it reverses the 0.7% decline of the previous month, and brought an end to the 10.9% drop that occurred over the previous 12 months.

That flattening can clearly be seen in the graph below which tracks the monthly movement in the HPI since January 2019.

However one month's figures do not make a trend.

It's too early to know whether October's figures marked the return of an upward swing in house prices, whether they just paused to catch their breath before continuing their downward run, or whether they marked the beginning of a period of price stability.

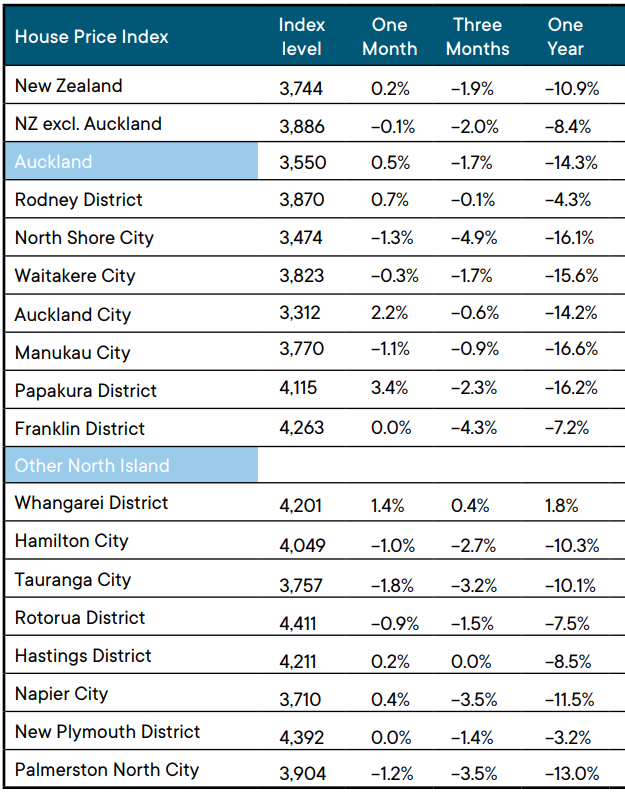

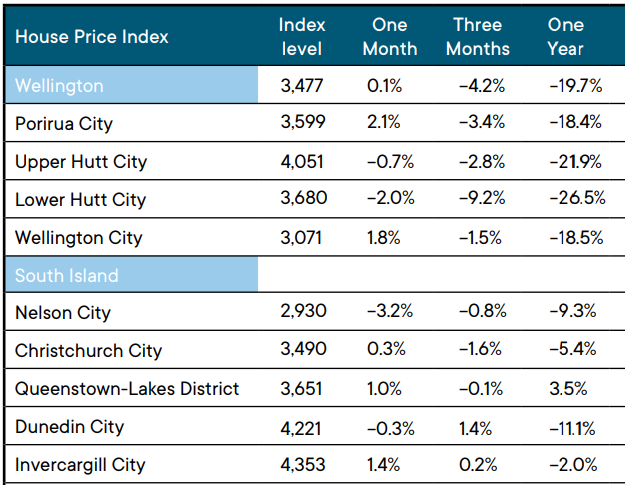

It is probably significant that the HPI increased in the country's three main centres of Auckland +0.5%, Wellington Region +0.1% and Christchurch +0.3% in October, particular as Auckland and Wellington have previously posted some of the biggest price declines.

But even in Auckland and Wellington, the movements in the HPI were not uniform.

In Auckland the HPI increased in Rodney, the Central Isthmus suburbs and Papakura in October, but declined on the North Shore, Waitakere and Manukau and was unchanged in Franklin.

In the Wellington region the HPI increased in Porirua and Wellington City and declined in Upper and Lower Hutt.

Similar variances can be seen around the rest of the country, as shown in the table below.

November's figures should be telling, because it will be the market's last full month before activity starts to wind down for the Christmas/New Year break.

Indications so far are that sales volumes will remain at low levels compared to previous years and there won't be a lot of movement either way in prices.

But one thing the market is not short of is uncertainty.

There will be more news soon on the interest rate front and it won't be supportive of higher prices.

And many people will be wondering how their household budgets will end up after taking into account rising wages compared to higher inflation. The general economic picture is nothing if not confused.

So up, down or sideways for house prices? At this stage, it's probably too close to call.

The comment stream on this article is now closed.

REINZ House Price Index - October 2022

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

85 Comments

Be quick...

7% Interest Rates This Year, Guaranteed ! - Prophecy Confirmed.

-30% Crash In Home Prices by December , it's a Certainty ! - Prophecy Confirmed.

South Wairarapa District is the First to Break the -30% Barrier, setting the Trend .

This has now Broken the Seal to the Second Scroll. The Prophets Scroll will be released before Christmas.

"All eight Territorial Authorities (TAs) had negative annual median price movements, with South Wairarapa seeing the greatest decrease, down 33.7%, followed by Carterton, down 26.5%."

Of course the spruikers will try to claim it should be for the whole country, but some areas go down while others go up making the average absolutely meaningless, but a fantastic tool to deceive the gullible. This is how the RE Industry claimed the GFC was just a little blip in the radar, when in fact it was devastating . Property drops or increases need to be insular to know what is really going on.

Yes and the lastest QV district specific HPI data shows the large drop is in the upper quartile properties in South Wairarapa which suggests a real drop in the expensive properties, not just more cheap properties selling. Of course this data has lag in it compared to REINZ HPI and there are currently very few properties selling each month in these areas 7 in South Wairarapa and 6 in Carterton for October. Very slim pickings for agents which might explain the really high asking prices as agents “ buy” the listings. Still at least 30% needs to come off in Wairarapa to take off the 50% increase in prices that happened with Covid.

https://www.qv.co.nz/price-index/

House prices increased in October but that doesn't mean it's a trend

And it doesn't mean it's a crash. (Even if the oily DGM insist that the market has collapsed.)

TTP

And it doesn't mean it's a crash. (Even if the oily DGM insist that the market has collapsed.)

TTP

Doesn't mean there's not a crash either. It's just an index. Most people don't have the chops to understand the limitations of longitudinal house price indexes.

Oily DGM? Your absolutely projecting here.

I'm always amused at your comments. They seem designed to get a reaction and I'm sure you have a good laugh at the outcomes. But make no mistake the most oily person on this site is you. I wouldn't trust you and your advice if you were the last agent on earth.

I admire the chutzpah and the relentless commentary, we've all got to make a buck but you are the epitome of a snake oil salesmen and have absolutely no right to impinge on anyone's integrity.

Awful

"And I will smite the winter house with the summer house; and the houses of ivory shall perish, and the great houses shall have an end, saith the Lord." - Amos 3:15 (KJV)

According to the Resource Management Act the smiting of a house is not allowed ... Amos better get his sh*t together because he's in breach of the RMA .

The recovery has begun

Here's the bottom you guys all have been desperately wishing and praying to the gods for. Be quick... ;)

-7

I think you can be pretty confident house prices are not going to stabilise. They will continue the downward trajectory with a great bias to greater falls depending on how quick the economy slows. Mortgage rates at 6% are bad enough let alone get worse.

Hi "Thinker",

You're more a "misfortune teller" than a thinker.

Given today's headline, I expect that fewer Doom Goblins will surface here to support you.

TTP

Yawn

Despite the fact house prices are currently crashing, Tim insists on filling this forum with the same insane rubbish day after day. "Doom Goblins" are under no obligation to repeatedly post sane counter arguments in response.

RP (the one and only Crash Crusader)

Reverend Retired Poppy - Relentlessly Rebuking the Reprehensible Realtors.

AKA The Reverend.

Yes, its been an exhausting, yet a fruitful journey. The fruit being those who delayed buying. The ones who listened to Tim are "Jam in a sandwich"

The more you say GLOOM the more I see sunshine and unicorns, affordable homes and sanity, must be coming our way.

The Donald Trump of this site.

It's never a straight line in either direction. It wasn't on the way up, and it won't be on the way back down.

The trend is your friend.

Annual changes in house prices and annual changes in mortgage rates have moved in direct opposition since the GFC with matching inflexion points (when one turns negative, the other turns positive). Year on year changes in mortgage rates turned down a month or so ago and house prices may now stabilise or even creep up (the September and October data are exactly as you'd expect based on this hypothesis).

Jfoe, 100% agree with your logic but the mortgage rates have risen all year, plateaued slightly and likely will rise with the next OCR. The FED looks to be in the mood to hike more and so I'm confused by your conclusion. Could you shed some light?

Yes, mortgage rates have risen all year, but the year on year increase hit 100% in June (June 2022 mortgage rate compared to June 2021 mortgage rate). The year on year change in mortgage rates has dropped to 80% since. When this has happened in the past, year on year change in house prices have turned upwards. We'll see! I don't expect mortgage rates to go any more than 50 pts higher. Central banks do actually know that further hikes will achieve nothing positive.

Thanks, Jfoe. Interesting. Are you able to link to a chart somewhere showing the year-on-year change in mortgage rates? It would be helpful to see this.

Sure - I think this chart probably does it (data only back a few years):

Thanks, Jfoe. Appreciated. It will be very interesting to watch mortgage rates vs house prices over the next few months.

Thanks Jfoe - appreciate that. Interesting correlation.

A "creep up" would be an 8 - 10% increase in price to keep up with CPI and/or wage inflation.

Until next time!

All eyes on OCR announcement next week. Over the Summer break I will be watching China to see if they open up.

Heading out on the basis of the October HPI to buy a property would be brave.

It's all to play for.

Agreed. There was also widespread mainstream media coverage of US analysts predicting a "Fed Pivot", which was subsequently shut down in decisive fashion via the Fed chairman.

I suspect there was also some demand brought forward after that announcement, where people looking to buy have seen a drop in prices already, but also now potentially higher rates for longer, and seeking to lock in a lower rate now before they head higher.

But who knows.

Chinas just gone to 5 days in managed isolation, 3 at home.

Which is basically pointless given COVID can incubate for like 2 weeks. Even testing is pretty off now, I tested negative for a day while I clearly had it, then positive. I expect China will just let it go soon, will be out of control probably soon anyway.

To quote the guy who writes at Wolfstreet, "nothing goes to hell in a straight line".

'to heck' Wolf writes.

You should get one of his coffee mugs.

☕

I wish Putin would ...

"It's too early to know whether October's figures marked the return of an upward swing in house prices, whether they just paused to catch their breath before continuing their downward run, or whether they marked the beginning of a period of price stability."

Knowing that interest rates are still going up this year and next year, I cannot fathom how anyone could possibly believe their could be a "return of an upward swing in house prices" !

Property spruikers, self-interested specufestors, real estate agents etc. They probably do not believe themselves in what they are saying, but they desperately need more fools to support the Ponzi.

There are a couple of possible reasons, the first being that interest rates may have reached close to their limit before Reserve Banks cause serious damage to economies so those institutions may pause and wait and see. Secondly in NZ if house buyers judge that there is a reasonable chance that a National/Act coalition will come to power then the likelihood is that owning a house will be less punitive, taking a risk on renting to tenants will be less of a issue (if you can actually move those tenants on if they become troublesome) and therefore houses become a better investment.

When the house price buying boom started it was difficult to find an investment that would return a decent positive nominal return. Now it is difficult to find an investment that will return a decent real return.

Will interest rates stay at elevated levels if the US + World goes into recession?

Given the latest Roy Morgan poll perhaps house prices will start crashing again. I wonder if the poll numbers have something to do with the candidate National selected for the Hamilton West byelection?

Anyone loading up on debt and buying a house right now believing that the house price fall has bottomed out deserves everything they get.

Settled on a place for just under $5M a few months ago, what I got was a very nice property, well constructed house, nice gardens, lap pool, good entertaining areas... puts a smile on my face each time I drive through the electric gates so it's not all doom & gloom, despite having a mortgage for the first time in a while. No regerts

Likewise, not for $5m though. What we got was a 1/4 acre section, 200sqm 4 bedroom 2 bathroom well maintained 1920's property on a leafy street with Rimu flooring throughout, 2 heat pumps, log fire, HRV. Bought with a DTI of ~3.5.

Puts a smile on my face each day I walk out the gate, cross the road -> 300m through the sports field to take my 5 year old to school.

congrats!

I find it strange and confusing when some people kept celebrating a house market crash when they are not even in the market.

Yep most on here revel in the misery of others but still will not buy a house even when their predictions come true, so really the price is irrelevant.

Your are right price is, but debt is relevant.....

Perhaps their only chance to be 'in the market' and live in their own home is for prices to go lower. In that case it would seem logical for them to celebrate to me.

Perhaps they think beyond themselves and have some regard for following generations.

Surely not, the DGM party cannot be over already after all everyone else has been having the time of their lives for over a decade.

Given the massive lag in flow-through of interest rate rises, we probably haven't seen much of what is to unfold yet.

Anyone who's studied control theory knows you don't set your control multiplier too high too soon. No idea if the RB model interest rates and inflation using PID or another system, but I'm sure their math boffins know to stay away from the unstable areas. This applies to the Fed as well.

Whilst I personally disagree with much of what Orr has done over his tenure (and have written for his sacking 3x), what they are doing now is not too far removed from what they need to do. The OCR is likely to go considerably higher, but the system will remain stable whilst it gets there. And that is probably far more important than causing mass panic and an almighty sell-off in a short period of time.

Just sucks for those of us affected mainly by inflation rather than debt servicing costs, but the banks are looking way to exposed to handle the kind of down-turns seen in Japan or Ireland. And there's still no guarantee we won't see that either.

WhoCouldHaveNooed

Patience Carlos125. Patience.

DGM on housing = almost all young people then?

Depends how wealthy your family is.

That Cat did not bounce far...

Dead cat splat

Fool Trap.

Another load of absolute garbage from wet curl Tony on OneRoof today. Why do people pay him?

So, if you do not agree with TA email him and tell him what your opinions are. Let us know what he says, would you.

Lets do some simple analysis...

For a typical NZ household, who had say $60k disposable income to service a mortgage (i.e. total after tax earnings of $120k) in early 2020 when interest rates were 2.5%, they could have borrowed $1.25m.

Lets assume their wages have gone up 10% by end of this year. They can now afford $66k p.a to service a mortgage. However, interest rates are 7%.... By my calculations, they can now only borrow $745k from the bank.

That is a 40% drop in borrowing capacity. This doesn't take into account equity erosion from other assets (KiwiSaver, investment property, own home etc).

This crash is just warming up folks...

It also does not take into account higher Insurance Premiums and Rates. Oh, and The Prophets favourite below.

!0% Interest Rates Next Year, Guaranteed !

And then you could factor in that the typical after-tax earnings of an average NZ household in 2020 was 30% less at $85k* - what's your typical household? Because it's probably not those at $120k after-tax (though they might be the typical purchaser, which is different to the typical household).

* Source: https://www.stats.govt.nz/information-releases/household-income-and-hou…

Yes a 40% drop aligns with the present value of discounted cash flows (using NPV) if inflation rises on the cash flows at a rate of 8%, while the discount rate rises from 3% to 8%.

I would agree, but after decades of math of finance (yield actually mattering) not meaning a damn as people chased speculative gain, who knows. One thing for sure, future generations will study this period and there will be a whole pile of "how not to..." written about.

Housing stock building up in Auckland 10% more over last two months. As rates keep raising prices will tumble.

One does not have to be economist or an expert to know where the market is and heading.

Really ? I wouldn't want to make a call at present and stake my life on it. Russia just dropped a couple of missiles on Poland by mistake, seriously anything could happen in the near future.

Let me guess... Poland should roll over and let Russia win?

Brock,

That's highly distasteful/offensive. Conduct that's uncalled for.

Many people here will have friends/family living in Poland - and communications with them are becoming disrupted.

I urge you to withdraw your comment.

TTP

Brock was making a satirical reference to way some commenters have a habit of licking Putin's boots.

Dropping missiles on a foreign sovereign country is not a mistake. Its somewhere between incompetence, and an act of war.

Hanlons Razor

I think this is just a bit correction for the price which applies to almost all assets price.

Assets price is not something that goes one way up or one way down, there will be some corrections in between. The reason is that assets holders always have price expectations, in an down trend scenario, when selling price is reaching or going below their expectations, they normally would hold off selling their assets as long as possible, which causes price goes up and down a bit, then when the market corrects their expectations, the price continues to drop again.

So I wouldn't call it an end of a year of steady declines personally, especially when we are not out of woods yet.

If the HPI results are not already bad enough, he goes onto say - "That being the case, you aren't going to see house prices go anywhere but down, in our minds, still over the next 12 months or so."

But then goes onto say -

"In better news, Olsen did not believe a housing crash was on the horizon."

Olsen is described as "A leading economist"

I have other words to describe Olsen, and its NOT "A leading economist" ( Do these people actually get paid ? )

None of them picked and called the top ... just sayin.....

Don't expect any of them to manage to call the bottom....

I sold Nov 21....

This is not the bottom you fool!

FHB here, sitting on the sidelines waiting to buy a reasonably priced home that doesn’t evaporate my life savings.

I have a question about the HPI data. It seems that all data must go into some nationwide database that then gets accessed by RE platforms (homes.co.nz, OneRoof, realestate.co.nz etc) as they all seem to update at the same time. I’ve noticed that ‘Recent Sales’ prices are often listed as TBC or Unknown for any sale that wasn’t an auction (public data anyway?), for all my properties on my watch list even 6 months+ later after being sold.

Does the HPI data rely on agents inputting the sales price into some database? Its as if RE agents desperately want to hide any house sale that sells below valuations, therefore skewing the house price data…

Maybe I’m being facetious, but REINZ is surely as corrupt as the RE agents that built this Ponzi scheme.

"Maybe I’m being facetious, but REINZ is surely as corrupt as the RE agents that built this Ponzi scheme. "

As The Prophet Would Always Say - Whatever The Vested Interest Say - Believe The Opposite !

Yes things have changed on the RE sites, the last few years prices were published as soon as the contract on the property went unconditional, I think to keep driving prices up. Now all our sales except for a few new builds ( these are still achieving good money in my area) are no longer published. We are finding that prior sales data and RVs are being taken down from the pages on some properties for sale also. I don’t think the Homes website uses HPI or any other official RE data ( I could be wrong). Homes can b3 accessed and changed by local agents, changing prices and removing bits of data. Homes has been manipulated by agents so much ( agents are able to go in and make a “ market appraisal” on any property thus altering the algorithm generated valuation) and sales volumes are now so low in our area that the Homes values are now nowhere near what houses are actually selling for. The house estimate graphs are still ticking up every two weeks with last years price rises - they are showing no drop at all over the past three years. I suspect that sales prices are not being put in as when I find out the prices and check back into Homes the property specific house estimate graph has not corrected to the sales price on the sales date.

REINZ data is the best most up to date data, it is released just a few weeks after the end of each month. It is based on unconditional contracts that occurred in the previous month, so is very current data. It is official data and the REINZ HPI is what the RBNZ uses for its analysis. Look at the HPI, but also keep track of volumes etc on the monthly report for your area.

https://www.reinz.co.nz/residential-property-data-gallery

i also use the QV and Core Logic tools to check local data ( my area has tiny sales volumes), but you need to remember that this data is based on settlements so is a few months out of date

https://www.qv.co.nz/price-index/

this is useful though to drill down to your area, it shows the movements in the upper and lower quartile ( I presume that you will be looking in the lower quartile as a first home buyer) as at present differing priced bracketed houses are decreasing at different rates.

Always remember that agents are not on your side, they are on the side of the sellers. So take their advice with a grain of salt, I am often shocked at purchasers earnestly taking price advice from the selling agent.

I am looking to purchase and am constantly watching, but think it’s too soon for me to buy as most vendors in my area haven’t accepted to drop in the market yet and are still hoping to find a buyer who will pay last years prices, it may be a bit better in your area in the lower quartile houses. I guess you will be juggling house price against estimated interest rate cost also.

Best of luck, good you are keeping an eye on Interest it has the best articles and I find the comments really helpful.

Thanks Nellbell! Really useful information.

I often wonder what specific properties get sold for rather than area averages. Seems very dishonest for RE platforms to publish sales prices when they’re increasing, and hide them when they’re decreasing. Their job should be to present the factual data regardless of market direction.

Good to know that REINZ, QV and Core Logic are reliable sources of data.

One place you may find what a property sold for is propertyvalue.co.nz BUT look in both the About section as well as the Property History timeline. We've found it may Sold: sale price not available on the timeline, but if you look in the About section the sale price may be recorded along with the date of sale. We're using it to track property prices in an area we're interested in buying in and sales prices are not always there but enough for it to be useful to us.

QV.co.nz, Oneroof and propertyvalue.co.nz are sites that publish sale prices, but not until settlement has occurred I think :)

Don't really get this. There's always a seasonal bounce. This one appears to be anaemic?

There's likely to be a few people that have waited for spring. They've been successful in holding in and seeing prices drop, but it's time to buy and get in with life.

Economically there is nothing to think that the trend is house prices has reached a floor. The lag for interest rate increases and people coming off fixed rates is still there. But it will happen.

Inflation is with us, wage rises have happened, inflation is still with us and businesses can only pay so much. Then we will see the retraction of spending.

This has the possibility of years to play out. At least 2. Asset prices are going down people, get used to it. To say that it's too close to call is pretty ridiculous.

Low unemployment rate, a reasonably stable economy, record year on year wage increases, rising interest rates. If one of these 4 walls falls over, that's when things will get interesting.

And as we know, the RB is planning to skittle the first 3 :(

If house sale volumes are down (by 30%+ since last yr) then a higher portion of the houses on the market would be new builds. They are a higher price cf with older houses. Could this be responsible for the increase HPI?

Digital currency "Bitcoin" is cooked, housing is the next on the list.

Not TTP...

My oh my, what a surprise ;)

Keep posting my doomsday dreamers. Wishing for everyone to lose their wealth is one thing, but karma always comes back around to bite you.

For the record, before COVID, interest rates were already at 6%, and housing prices were going up at that time as well. So to say that these level of interest rates will "crash" a market, its absurd. Only if interest rates go to double-digits will that happen. That won't happen as the govt has vested interest, and on top of that, inflation trends shows signs of easing (especially with the recent US inflation data which shows a downtrend has started). You don't feel interest rate hike impacts until 6-12 months out. Similar to when we dropped interest rates to close to 0%, we didn't feel it until 6 months out. So all the hikes we did in the last 3-6 will start coming into play now.

Enjoy!

-7

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.