The housing market appears to be off to a slow start to summer so far.

The latest figures from property website Realestate.co.nz and the Real Estate Institute of New Zealand (REINZ) show a widening gap between the number of properties being newly listed for sale and the number selling.

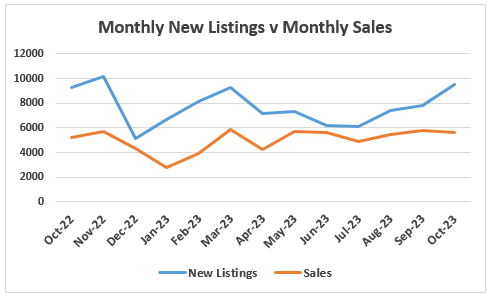

The first graph below clearly shows the trend.

Back in June this year Realestate.co.nz received 6218 new listings of residential properties for sale, while the REINZ recorded 5629 sales in the same month.

That almost closed the gap between listings and sales with the number of sales being just 9.5% lower than the number of listings.

By August new listings began rising strongly, and by October had reached 9529, up 53% compared to June.

But the rise in new listings wasn't matched by a rise in sales, which remained largely flat over the same period.

In fact the 5619 sales recorded by the REINZ in October was 10 properties lower than in June, and 143 properties lower than in September.

As the result, the number of sales went from being 589 less than the number of listings in June, to 3910 less in October.

That is not a good place to be for what many in the real estate industry have been hoping would be a season of recovery for the market this summer.

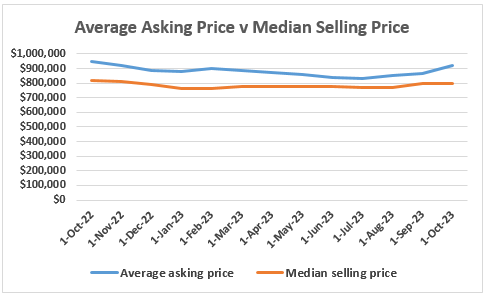

Comparing asking and selling prices tells a similar if less spectacular story.

Realestate.co.nz measures average asking prices for its listings while the REINZ records median selling prices, so the two are not directly comparable, but it is the trends that are important.

Since June, Realestate.co.nz's average asking price has increased from $841,688 to $920,678 in October, up $79,990.

But the REINZ's median selling price has remained almost flat over the same period, rising marginally from $780,000 in June to $795,000 in October.

That has seen the gap between the two more than double, from $61,688 in June to $125,678 in October.

As with sales numbers, the pricing trends do not show the uplift many in the industry had been hoping for.

However it's still early days as far as the summer season goes and things may yet turn around.

But with only around three weeks left until the market eases off for the Christmas break, things will need to happen quickly if we are to see any sign of a recovery this year.

However if current trends continue, then we could see total stock levels rise, properties sitting on the market for longer, the return of the buyer's market and the inevitable downward pressure on prices that produces.

The comment stream on this story is now closed.

- You can have articles like this delivered directly to your inbox via our free Property Newsletter. We send it out 3-5 times a week with all of our property-related news, including auction results, interest rate movements and market commentary and analysis. To start receiving them, register here (it's free) and when approved you can select any of our free email newsletters.

130 Comments

The housing market is similar to the state of Nokia phones... you can try your best to hype it up, but the reality is that it's a slow motion wreck

Recovery?

I usually don't comment on RE threads - predictable and boring. But that word stuck out as assumption writ large.

You are still interested enough to read the article? Most times I go straight to the comments

Nobody should expect a recovery to go in a straight line..... Inevitably, there'll be ups and downs along the way.

Overall, however, the market is much more buoyant than 1 year ago, or 2 years ago.

Notably, house prices remain well above their pre-Covid level 😁 despite the pessimistic predictions of the DGM. ☹️

TTP

When you cannot reconcile with the present why not dredge up the past....

Which in my humble opinion,is why a recovery, would see house prices falling.

Overall, however, the market is much more buoyant than 1 year ago, or 2 years ago

Lol when hyping the market is more important than facts

2 years ago was 2021 and the market was at its peak

Hi danicriss,

The records show very clearly that the market went into sharp decline from November 2021. In other words, the boom/buoyancy ended and the downward correction began.

TTP

NZ house sales volume from: https://www.interest.co.nz/charts/real-estate/volumes-sold-reinz

October 2021: 7486

November 2021: 8644

Not even a decline let alone a "sharp" one. The Actual records show this Very Clearly.

TTP, you've already been fined for dishonesty in your business dealings, good to see you are at least being consistent and bringing that dishonesty to the comment section.

The records show that November 2021 marked the end of the boom. The housing market declined after that.

No point you trying you (and your DGM cronies) attempting to mislead and deceive well-informed people.

November 2021 is well-documented as the month/year that the market turned.

TTP

Hahaha the cojones on this guy ‘attempting to mislead and deceive well-informed people’

i don’t know how you lie straight in bed at night.

Good to see you're up to your old shenanigans of changing your comment after your lies are exposed.

Housing busts don't go in a straight line either, TTP. I think the jury is still out on what is gonna happen going forward.

Nokia was Nokia back the days because there wasn't iPhone in place. if housing market is Nokia, what is the iPhone to it?

iphone appeals mainly to younger generation. In this context; it's Australia!

but Australia was always there, and hardly a game changer.

Bitcoin, give it another 5-10 years to reach scarcity race levels

Well built, energy efficient, high density townhouses and apartments in convenient locations. FAR preferable to younger generations. Just a matter of time.

I’m sticking with my BlackBerry.

TTP

Good chat with a banker contact last week. He confirmed they were more or less in extend and pretend mode. They were letting people breach debt covenant ratios with little action. Any farmers not meeting generally interest only payments were green flagged to sail on if they even hinted at mental health issues.

He did say they were actively reducing their own operating overheads at levels surprising staff, especially as they were announcing record profits. Its almost like they are batten down the hatches for something...

He did say they were actively reducing their own operating overheads at levels surprising staff, especially as they were announcing record profits

At the ANZ earnings announcement to staff, Shayne Elliott mentioned that they would be letting people go. Someone mentioned it to me. He has one of those offshore jobs in South-East Asia. Not quite sure what it is he does. My feeling is that there probably is overpaid deadwood working in the banks.

A lot of companies went on a hiring spree to get extra bods on board to cope with the surge in demand over the Covid period. Now that they are no longer doing that level of business, those people can be let go.

I wonder if they'll let the chief economists and associated functions go... There's some overpaid deadwood... Maybe a chairman...

"Good chat with a banker contact last week"

Just out of interest, what type of lender were they with?

1) top 5 bank lender

2) other bank lender

3) non bank lender

One of the Aussie 4, mid level commercial manager.

Averageman,

Thank you for sharing that intelligence.

"He confirmed they were more or less in extend and pretend mode. They were letting people breach debt covenant ratios with little action. "

Seems like a lot of loan forbearance at the moment by the banks. Did they mention

1) how long are the banks extending and pretending?

2) under what circumstances the bank would stop extending and pretending?

I did ask, but not being openly discussed at his level. Just noises about branch closures, and redundancies due to low lending volumes.

I did ask, but not being openly discussed at his level. Just noises about branch closures, and redundancies due to low lending volumes.

ANZ - IT functions being outsourced to India. NAB - IT functions and innovation outsourced to Vietnam.

NZ banks have been outsourcing functions to overseas locations for decades now.

"He confirmed they were more or less in extend and pretend mode. They were letting people breach debt covenant ratios with little action. "

Averageman,

Did you get a sense of the magnitude of the loan value or loan book that the bank was extending and pretending? Did the commercial manager think they were comparable to the GFC in 2008- 2010 period?

The bank knows the second there is any whiff of information that could push the population to panic then she's all over. People would pull their money, housing foreclosures would be rocketing and all would speed up exponentially as the news spread and contagion to other sectors. Even in the hardest of times, a bank would rather lose money for a while than lose everything.

This is eventually going to throw a spanner in the works of the Rest Home Industry and others.

I was looking recently at an over 50s village. Own the property, pay an annual fee, get any cap gains- but loose 20% as a 'fee' to the body when you sell up (4% per annum to max 20%)

All these models will be based on assumed never ending gains.

Can they suck it up if the growth has gone?

No. But new models will fill the gap.

I think you may be confusing rest homes with retirement villages. The example you have given suggests a retirement village. Some retirement villages have a rest home attached to them, some do not. But most rest homes are separate from retirement villages and unlike retirement villages, most are not dependent on their residents having access to capital from the sale of a house, so gyrations in the housing market make little difference to them.

Nope, no confusion.

Rest homes was one ref (eg Rymans)

Second ref was retirement village (eg Cambridge Oaks)

Different models but both models rely on increasing property prices.

Both will be affected...but how. If the gains go, do the fees need to go up to cover the lower cap gains?

Remember time shares...when the fees got so high the 'week' could be purchase for a $. Diff beast but then again...

Neither will be "effected" by this, but will be definitely affected.

I have put your advice int effect by editing. :)

Ryman is a retirement village company that also operates rest homes.

I knew someone who used to own a rest home and there was essentially no money in it. Retirement villages are another thing entirely, espailly if they are a license to occupy. But looking at retirement company shares, they haven't been doing very well in the last few years, because of the house price crash and rising interest rates. We were told the housing market had starting increasing again. But even if they flatline until 2030, that is still a fall when factoring in inflation.

Hi Greg,

It's a bit like the DGM - who confuse crashes with recoveries.

TTP

Hey TTP, you and the DGMs could take up gardening together. They provide the manure while you're having a dig....

Hey TTP

Are you sure it's not like someone who instigated a shady deal to control prices, hanging out on a Property forum just to mock folks who think property prices in NZ are way off base?

https://comcom.govt.nz/__data/assets/pdf_file/0023/69530/Commerce-Commi…

Price fixing doesn't seem to be behaviour befitting a person who is trustworthy, has high integrity or has high quality character.

People choose their behaviour and actions which leads their reputation.

When trust is lost, it is extremely difficult to regain.

Fool me once, shame on you. Fool me twice, shame on me.

With falling prices the younger generation Recover ability to buy a house without such massive debt, which is good

Hi Speedmax,

The problem is that house prices don't fall for long.......

Most of the time house prices rise - and at a faster rate than they fall.

But never mind, a peaceful society, education, health and wellbeing are all at least as important as home ownership.

TTP

The problem is that house prices don't fall for long.......

Most of the time house prices rise - and at a faster rate than they fall

Yawn.

They have been falling for 2 years now. Especially when you take inflation into account.

Given high interest lending rates stay elevated for another 12 to 24 months then we are looking at a *likely* 5 year period of house price falls.

Keep in mind that home prices have to increase by 6% annually to simply catch up to inflation. To see a REAL increase in value they would need to be increasing at 10%pa. Otherwise your equity continues to lose buying power.

This is eventually going to throw a spanner in the works of the Rest Home Industry and others.

The property ponzi and the retirement home industry go hand-in-hand. I don't know which is the bigger rort but I'm leaning towards the latter.

The retirement industry will be fine. Their growth hasn't gone - we have an aging population increasingly going into retirement still with debt.

So we will see pensioners who need equity, sell their houses, pay off the remaining mortgage and go into a retirement village. The impact will come through the increasing supply of their properties. No doubt this will release more housing for the ever increasing population.

I'm picking 4 and 5 bedroom homes will hold value and become more popular as many opt to live together instead of drainig the family wealth into the vampire industry of retirement villages. Seems to be a trend around where I'm at anecdotally

Rest homes have nothing to do with the property market. Beds are paid for by the Govt at $1350 a week. Even the rest homes contained within a retirement village like Ryman or Summerset fund their occupants through the Govt not through the house sale (unless you want to pay extra for a premium room). They take any patient that is funded, and not just people who were living in their retirement village before they became ill. This is one of the reasons why the Govt is amending the Retirement Village laws, because the retirement village operators promise people who buy in to it that they can easily move in to the rest home part, but they can't because the rest home is full of public patients.

Ryman do prioritise their current residents. Just been through this, although it's still a minefield because the local DHB has to approve the 'move'. If you have aging parents their house/unit/apartment value does matter because that cash is needed to fund the resthome fees, $7,000 per month (until the Govt subsidy kicks in).

They may prioritise them over the public if they have beds available, but the problem is when there are no beds available. Then Ryman et al say "we will move you to one of our other rest homes" which defeats the whole point of being in a village where you want continuity of social interaction with your friends. Its not like they kick a public patient out of their bed and then give it to a village occupant. If a retirement village occupant is moving in to the rest home property prices dont matter at all, their house has long been sold to pay for the original right to occupy licence.

NZ Housing market

Optimist: The glass is half full

Pessimist: The glass is half empty

Realist: contaminated water, drink (buy) at your own risks..

Brilliant

Optimists: speculators

Pessimist: ?

Realist: DGM's

Optimists would also include those with their vested financial self interests.

They need to instill confidence for people to buy.

*chortle*

Chicken little is a realist?

The glass is two times too big.

Average vs median.

Would be nice if apples were being compared with apples.

What would also be nice to see is the median length of time the properties were on the market.

Brutal economics.

600k mortgage @ 2.5% 550 wk or 28.5k per year to service 30 year P&I. Takes the first 34k of a gross annual salary.

600k mortgage @ 8.35% (low equity premium rate) 1100 wk or 57 k per year to service 30 year P&I. Takes the first 74k of a gross annual salary.

How much does the same house cost per year to rent? You need around 5% annual property value increase to be in the same position as someone renting the equivalent property and you are on the hook for rates, insurance and repairs. Pray you keep your job and your relationship otherwise its bailing out with no parachute.

You forgot taxes.

"600k mortgage @ 2.5% 550 wk or 28.5k per year to service 30 year P&I. Takes the first 34k of a gross annual salary. "

28.5k per year after allowing for income rises of say 10% is $31,350 per annum for debt service

$31,350 debt payments at a 8.35% mortgage rate on P&I is borrowing power of $341,589 - that is a reduction in borrowing power of 43% less than the $600,000 borrowing power at a 2.5% mortgage interest rate.

I see the upward (immigration, potential changes in policies) and downward pressures (OCR) having been pretty evenly balanced of late. The market looks patchy to me (high end, turn key doing OK, apartments not so much) depending on type of property and location (region to region) so month to month we're seeing little compelling evidence of either a crash, or a revival. Data spikes rather than momentum.

My hopes that when the OCR is tweaked down the RBNZ institute the DTI to stop a take off occurring as this has the potential to break the stalemate. Happy with CPI increases in property value but not the nonsense we saw in 2021 again.

I've been watching AKLD apartments in my area ..absolutely dead ... mainly due to vendors having unrealistic sky high expectations. No idea what these landlords are smoking ... would like some though ..

Its not boom times

There is normally a growing gap between new listings and new sales at this time of year. It closes again by January.

...then prices will start falling by late February.

We shall see. I'm still picking a flatline through 2024 and Auckland rents to go up 7.5%. interest rates will start dropping 2025. If landlords and property developers have kept their heads above water thus far they are probably going to be ok.

If landlords and property developers have kept their heads above water thus far they are probably going to be ok.

What are you basing that on considering there's still a lot of debt being refixed at higher rates?

The average mortgage rate for borrowers in NZ is now 5.53%. Most of the refixing from the crazy low rates of 2020-21 has already happened.

"Most of the refixing from the crazy low rates of 2020-21 has already happened"

The key questions are:

1) how much of that interest rate re-fixing is on extend and pretend terms by the lenders?

2) how many of these borrowers on extend and pretend terms will be able to hold on until they are no longer in cashflow stress?

extend and pretend

I have never heard that phrase before. It rhymes well and sounds good, but what does it mean

Mentioned earlier. Speaks to the banks allowing stressed debtors to have extended terms an or interest only, and then ignore default or miss interest repayment covenants. All the while making record profits. Not unlike a drug dealer allowing you extended credit to keep you hooked.

Isn't that known as a mortgage holiday which was commonly handed out during covid. In the end, you still have interest upon interest so not that many householders truly used it

The issue there being that if they can never pay the debt back, then giving the user a hiding and the user bailing still leaves a real debt and nothing gained. Then comes the dealers debt to their dealer

Most have already refixed at higher rates once, but many of those were in 2022 at rates lower than today. They will be in for another significant bump refining in 24. Interest rate pressure will keep increasing for another year yet

The average mortgage rate for borrowers in NZ is now 5.53%

So half the market have yet to refix to current rates.

https://datawrapper.dwcdn.net/mXAfw/1/

There's a huge amount of mortgage volume that's due to roll over in the next ~12 months still, that was on lower interest rates. Even people who fixed for 1 year are facing a jump from ~5.7% to ~7.3%, but anyone on 2-3 years are going to be facing a huge sticker shock, from 3% and lower to ~7.3%. Only about half of the pain of refixing has occurred.

The big question is how many had it all in one basket. Many split their mortgages into 2 or 3 blocks to help weather the changes over time and lower the impact in one hit. This, plus the fixed periods will delay the pain out longer than Australia who have mostly an immediate effect due to the level of floating mortgages.

If landlords and property developers have kept their heads above water thus far they are probably going to be ok

This is not how the market works. Some can keep their head above water but the ones that matter are the ones who can't. If there's too many of those they will drive the market

It's the same in reverse. It's like saying "if everyone keep their cool and understand houses are overpriced then prices will stay put". How did that work 10 years or 2 years ago? The market is driven by the few who flinch, not by those who keep their cool

I also see prices pretty flat over 2024.

perhaps ticking up at least 7-8% over 2025 once retail interest rates are circa 5.5%.

Some of us were sceptical of the green shoots narrative. Looks like that scepticism was justified.

Your Dr can now prescribe "green shoots".... s/he cannot help you with your cash flow negative investment property though.

That's why he's called Dr Feelgood and not Dr Yieldgood, after all.

Hi Greg,

Can you help me understand the rationale for restricting new comments by readers on some articles?

Like this one - https://www.interest.co.nz/property/125263/number-residential-propertie…

Thank you in advance.

I close the comment stream on the property articles after 3-7 days. That's because the comments need to be actively monitored and if the comment stream was left open indefinitely we would need a team of people just to monitor the articles. It is very rare for a comment thread to still be active after 3 days.

Get an AI bot

I now find I cannot even use the words "dead cat bounce" or "Suckers Rally" to describe the last three months because prices are not even rising. It appears to be flatlining price wise with a growing bloat of listings.

Come Autumn 2024, prices will follow the same track as last Autumn - down.

Funny how we never get an apology from the DGM's when they are wrong, still its a bit like the end of the world, you will be right one day, just keep on thinking doom.

Imagine thinking you're owed an apology because someone had a differing opinion than you on the internet.

Is it just a "differing opinion" or "crap advice", depends if you take it I guess, some people here block comments from certain posters from the get go, no need to wait for that apology.

Well the majority of readers know full well the value of your advice and it’s laughable.

You aren’t influencing anyone.

The only person I've ever seen acknowledge they were wrong on these pages is HouseMouse.

I think you guys classify him as a DGM even though he's pretty neutral to my eye.

I forgot what you call the other camp, but it seems far more common for the "NZ is diffrunt brigade" to redefine the meaning of words rather than acknowledge this "correction" is cutting a bit deeper than predicted..

I am assuming the difference in QV's upward trajectory in house 'values' and the flatline in REINZ average sales price data is down to a larger proportion of lower quartile houses being sold in the current climate. First home buyers are making a bigger proportion of purchases than normal so I assume that is in the lower quartile range.

How can they expect any increase to house prices when interest rates are rising and are at more normal levels. The price of a house is tied to what someone can afford to pay / mortgage someone can afford to service.

Agreed. Sellers and agents on greed hold as long as the banks enable avoidance of what the market can actually pay at today's interest rates. What will force the banks to price debt to real market affordability and income fundamentals?

"How can they expect any increase to house prices when interest rates are rising and are at more normal levels"

Many property investors use long term historical averages of house price growth in determining their future expectations on house price growth. Capital growth forecasts used are in the 4-6% p.a range.

A number of property investors believe that mortgage interest rates have peaked and are expecting mortgage interest rates to decline.

Here are the 1 year mortgage interest rate forecasts currently used by one company of property promoters in their calculations

Oct 2023: 7.2%

Oct 2024: 6.6%

Oct 2025: 6.0%

Oct 2026: 5.0%

Oct 2027: 4.5%

Also interesting to see a former high profile property promoter who owned up to 60 odd investment properties sell his entire portfolio in 2020. There has been no indication he is buying existing properties at the moment. He is currently developing some property - unsure if it is land subdivision, townhouses or apartments.

Could we be following in Australia's footsteps with a double dip, with a short lived spring upswing, with a lack of inventory, followed by a flood of listings, a lack of finance qualified buyers, and another downswing in values as affordability and inflation bites?

Spot on I’d say

Likely. I predicted a flooding of listings this spring, and it has been somewhat less than I thought, however still plenty in my region and at 52 days to sell there's no sign it is picking up.

"As the result, the number of sales went from being 589 less than the number of listings in June, to 3910 less in October."

Greenshoots™

I’m just here for the Retired-Poppy comments. 🍿

And TTP, Swifter..

Interesting numbers. I reckon agents have been pushing unrealistic expectations onto hopeful vendors through their appraisals...

First rule of Listings, we don't talk about lack of listings. Second rule of Listings, say anything to get listings.

Reality sucks.

The facts are people just can’t or don’t want to pay over inflated price’s. I believe average income earners have no chance of purchasing a property in Auckland from scratch,younger generations also will find it hard to own a house many are leaving for other countries. With rates now at 7-8% average wage couple needs 8 x income mortgage to buy house in Auckland for this reason the next phase of crash will happen. Also as more people refinance and weekly mortgage payments go up 70 to 90% only a matter of time before defaults and deadline sales are the norm.

The facts are people aren't willing to accept undervalued offers, there just aren't enough in deep poo for them to move the market.

With the current immigration levels there's a going to be a ton of demand for rentals, just did a trademe search for 2+ bedrooms between $550-$900/week in Auckland City and only 32 results (excluding apartments). Edit: trademe had retained a filter, there's only about 400.

There are bugger all facing a 70% increase in payments, only a small number fixed for >3 years when rates were at the bottom, most have already adjusted to the first rate hike, no signs of a crash inbound.

Why would you exclude apartments?

Becuase they are horrid shoeboxes.

That's a very old fashioned Kiwi attitude. All the immigrants that are coming in don't share those views and will be quite happy to live in an apartment. I think you have excluded them to try to make your point. Add the apartments to your figures and see if the point still stands.

People will be able to pay extra for awhile but many will just get to far behind the million dollar mortgage went from 950 per week to 1750 many of these people could just afford the 950 this would be why 1 in 10 are selling at loss and the market is starting to get flooded with people trying to get out. Pragmatist most investors left the market a long time ago it would be crazy to invest 1.2 million for average house to rent out for a 900 per week do the numbers make 46800 per annum less costs even if you invest into term deposits you get 72000. Hope you are not advising people to invest in rentals at this point many places are already down 20% from highs.

I'm not advising anyone to do anything, except ignore the interest doomies.

32??????

I just searched and got 491 (excluding apartments, but why exclude them?)

Ah, stupid website had retained a suburb filter that it should have cleared. Apartments excluded becuase screw that, Who'd actually want to live in one.

Perhaps people looking for a roof over their heads? Wild guess I know.

Recently saw a FB listing for a rental where pets would be negotiable. 106 messages on the post and can't imagine the number the landlord got privately. All sorts from families who are moving to or recently moved to the city, immigrants, families who have had to move each year for years on end, the works.

I want to and do live in one. Some reasons: double-glazing throughout, fully insulated, ventilation in every room with temperate fresh air supply, necessities and services (hospital, supermarket, education (uni)), a handful of top Auckland restaurants, access to the motorway, public transport systems, my commute to and from work, are all within a 15-minute drive. My weekends are not spent on jobs around my home. The body corporate is well-run and the common areas are well-maintained and cleaned daily.

The psychology around selling at a loss is interesting too. On a very small scale ($1-2k) I feel it acutely when I look at a few of my worst stock picks and can't make myself sell them, but no doubt loss aversion applies right up the investment scale.

From Investopedia: The fear of realizing a loss can cripple an investor, prompting them to hold onto a losing investment long after it should have been sold or to offload winning stocks too soon—a cognitive bias known as the disposition effect. Rookies often make the mistake of hoping a stock will bounce back, against all evidence to the contrary, because losses lead to more extreme emotional responses than gains.

Smart money reaches the exit first, hence why so many traded up and also sold off rentals through the boom in recent years.

Sals need to have a denominator

Which is total housing stock

Which is never mentioned

Stock has risen in Auckland for instance by about 15000 pa last 6 years. So if sales are lower than last year, they are in fact worse because the metric of sales as a % of total stock is not given

i keep saying this

Good point Mike.

Primary determinant of sales and price direction: cost of credit. Followed by mortgage stress test. Even as inflation falls real rates rise. So market credit continues to tighten

Hence watch real interest rate taking account of inflation. This is why sales not increasing and in Auckland are lower than in 2008-09

Inflation is still way above 2% narrative it’s not coming down just not climbing as much.

Mortgage stress + other have to sell reasons

house prices have flat lined for the last 4 months, that is fine shares and kiwisaver made hardly any inroads either, some articles state property prices up and then they are down. lets see what happens I am feeling optimistic that shares and houses will soon start going up again. Anyway what is DGM's?

The following people are labelled as DGMs:

- Those who want hard-working, young Kiwis to be able to afford to buy houses in which they can raise young families;

- Those who want house prices to fall so we no longer have one of the highest income-to-house price ratios in the world;

- Those who are worried about rising crime levels and increasing homelessness and believe that affordable house prices will bring more stability to society;

I’m not really sure why, but DGM stands for ‘Doom and gloom merchant’. The opposite of DGMs are people like 7-house Luxon who primarily seems to care about whether his property portfolio is bringing him more luxury, privilege, overseas holidays, etc (and the same for his mates with regards to their portfolios).

Considering your name is 'safeashouses', my guess is you're not a DGM?

I'd say anything that allows people to have financially stable future and a family is best for society. It just so happens that house prices are the biggest drain on the ability to do this unless you're in somewhere with semi-affordable housing. Sure people would like to be rich, but they don't always want that for the reasons you think, considering pressures today dictate that if they want to buy a house that they HAVE to have:

1./ A partner

2./ Both high paying jobs

3./ No hope of children for many years still even if they are early 30's

4./ All of the above and/or parents willing to help them towards a deposit or something towards the house

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.