The current lack of capital gains for residential property is not just reducing opportunities for new investors, it may also prompt existing investors who have held their properties for many years to see if they could get better returns elsewhere.

Last week interest.co.nz looked at the indicative rental yields and cash flows that could be available to prospective residential property investors, based on median rents and lower quartile selling prices.

This showed how difficult it would likely be for investors to find a property that could provide a reasonable cash flow if they were purchasing the property with a mortgage.

However, there's a much larger group of existing rental property owners, who are in a very different situation.

They will have owned their properties for many years and many will likely have little or no debt on their investment.

In most cases they will have seen the value of their properties increase substantially since they purchased them and are likely also receiving a healthy rental income from them.

In short, they will be sitting pretty.

However, the market is changing.

Capital gains have virtually dried up. See the interactive graph below which shows monthly movements in the Real Estate Institute of New Zealand's median selling price at both the national and regional levels.

At the same time demand for rental properties from prospective tenants is soft while supply is up, putting downward pressure on rents.

To top things off, the cost of outgoings such as rates, insurance and maintenance costs are rising.

All of which adds to uncertainty about future earnings prospects.

So it may be a good time for established investors to consider whether having their money tied up in a rental property is the best use for it, and whether they could get better returns elsewhere.

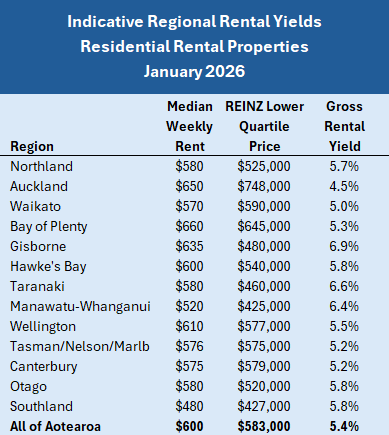

The table below shows the median rents in each region, based on bonds received by Tenancy Services, compared to the REINZ's lower quartile selling price in each region. That enables an indicative gross rental yield to be calculated for each region around the country.

In most regions this gives indicative gross rental yields of between 5% and 6%. The outliers are Gisborne 6.9%, Taranaki 6.6% and Manawatu/Whanganui 6.4%. The only region with an indicative yield below 5% is Auckland at 4.5%.

If you shop around you can get 4.5% on a bank term deposit, for a three year term, which goes up to almost 5% if it's a PIE fund.

That suggests rental properties in most regions, with the notable exception of Auckland, are likely providing a better return that bank term deposits.

However, when making that comparison, investors need to consider that the rental yield figures are gross, which means they would need to estimate the effect expenses such as rates, insurance, maintenance and other property management costs, as well as loss of rental income from periods of vacancy, would have on their returns.

These costs have the potential push down returns considerably, and in low yielding regions such as Auckland, Waikato, Bay of Plenty, Nelson/Marlborough and Canterbury, investors may find they can get better returns by selling their property and reinvesting in something that provides a better return.

In some cases, this could be achieved simply by putting the money in the bank.

However, as poor as the returns may be, this is unlikely to result in a rush for the exists from existing, long term property investors.

As long as their property is not causing them any major problems and they continue to receive a regular income from it, human nature being what it is they more likely to keep their money in a market they know well and are comfortable with, even if the returns have become relatively modest, rather than venture into unknown territory.

But for those on the outside of the market looking for a potential investment, the poor returns could be a major stumbling block to finding something suitable.

The comment stream on this article is now closed.

Median price - REINZ

Select chart tabs

31 Comments

But but...they are all worth at least 2021 specu bubble prices. And as things tighten further...who is going to buy them?

🍿

Unless everyone heads for the doors and the sales prices plummet.

Often people value a group of assets as the recent marginal sales prices times amount of stock. But in a crash scenario not everyone can realise that marginal price. Equally true for gold, crypto, real estate

"make", Greg?

Wrong word.

Turtle

turtle

turtle

.....

"Capital gains have virtually dried up"

Many people were saying the same thing in 2013. 5 years later, the HPI had lifted around 50%. Property goes through cycles and we've been here before. Property is a good long term inflation hedge. Stay in the market and don't be sucked in by all the investment property-bashing comments.

WORST INFLATION HEDGE IN HISTORY, since the paradym shift after 2021.

That's simply not true, and you know it.

Go and read up on what happened to the over leveraged in the 1930s, the 1970s (20% debt) and after 1987. Debt unsupported by income was by far the worst investment.

Perhaps your truth is a bit blinkered.

Property is a good long term inflation hedge

I am not sure this is true if you buy now at these low yielding values. And the fact that the new plan in Auckland opens up 1.6mil new titles. As you say we will see, place your bets Banzai.......

Investing in property isn't a bet if you're in it for the long term. On the flip side, short term bets on gold is most definitely gambling - don't let anyone tell you otherwise.

It is a bet. If the ratio of houses to population increases, prices will almost certainly go down. There is every chance this could happen if population growth stalls and/or building activity continues or increases.

In saying that there is no such thing as a safe investment, and property is still one of the safer ones.

Some people get really caught up in the difference between gambling, investing and saving, to me it's all on the same spectrum. Doesn't mean it's bad so long as the odds are in your favour, the position on the spectrum just affects your stake size and diversification needs. At one end of the spectrum there is huge risk from volatility and at the other end there is huge risk of seeing your money wasted away by inflation.

Property is somewhere on the safer/less rewarding end of the spectrum, depending on the market, leverage, (lack of) diversification etc.

Risk (and return) with property is leverage. And you can't dollar cost average your way into the market - you are either out or all in (often with 10% of your own money and 90% of the banks).

Hence it seems that once people buy into the market, they become spokespeople for it and try to talk prices up (even in the face of the worst possible probabilities of price increases).

Yes, a highly leverage property is much higher risk than a small position in a highly speculative stock, in my book. There's people out there who would balk at me sticking a few grand on a risky company when they're susceptible to a relatively routine ~20% market correction in one small residential real estate market wiping out their whole net worth or leaving them underwater. If my investment goes bust it's no biggie, there's plenty of others.

On the flip side, short term bets on gold is most definitely gambling - don't let anyone tell you otherwise.

Got a bit of a surprise to see PMGOLD up 4.2% and ETPMAG (silver proxy) up 10% on the ASX on opening. These are crypto-esque moves.

I think the Ponzi is far more manipulated than the sheeple fully understand, It's basically the mechanism by which the money supply increases. Empirically (the Anglosphere since the 1990s): mortgage lending has become the dominant application of that mechanism and thus a de facto driver of money and credit growth, with clear implications for house prices and macro-financial stability.

Miners up on possible less diesel disruption since Trump confefe on a deal.

GDX up 8% this morning.

Short positions on gold and silver being obliterated.

- Survivorship bias / hindsight bias

- False equivalence

- Appeal to past performance

- Thought-terminating cliché

I believe that had a lot to do with Chinese capital flowing into Auckland, which was restricted by China in 2016 and the foreign buyer ban 2018.

Where do you suppose the capital will come from this time?

I had a long-held, no mortgage rental property in Mount Maunganui which by chance, I sold pretty much at the top of the market. By reinvesting most of the proceeds in a combination of government stock, local authority funding agency and dividend paying equities, I significantly increased the net income with the added bonus of it being hassle free.

I would think that for many landlords, the balance will have swung even further since then.

Well played.

Not sure how old you are but for those who are keen to step onto a cruise ship for a few months, cashing in on their rentals seems like an attractive option. You can get mostly steady income and no nasty surprises from the property managers, or the latest "1/100 year" weather event that seem to be hitting every few years

Government stock is cash , you can lend it if required as margin for a loan as well

IT Guy,

Why I would but risk-free government stock-as an income producing asset and then contemplate using it as collateral for a loan beats me, but each to his own I suppose.

its how many immigrants satisfy investment requirements

rolande,

Nearly 81. I much preferred tramping to the thought of a cruise, but cancer has stopped that. I am in fact looking at a possible cruise to the Marquesas to see what it would be like.

Buying any property in the hope that it will make money because the market is going up is not investing, it's gambling. If you want to make good money in property, you have to understand how to create value.

Your accountant prompted you to say that to the IRD?

The old saying was 'the best time to buy a property was yesterday' but that seems to have fallen out of vogue with the debt gamblers.

doubles every 10 years smells old as well

Honest question, have you always thought that, or is this new thinking/comment for you?

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.