By Shane Martin & David Norman*

• Many things affect property values in more or less obvious ways.

• Obvious examples are the premium paid for waterfront properties or for larger houses over smaller ones. Of greater interest, however, is how much these attributes contribute to a home’s value – while holding everything else equal.

• Less obvious attributes include location in the “double grammar” zone, which adds about $130,000, and the “goldilocks” factor of location – being neither too close nor too far from certain other amenities.

• Other factors, such as cladding associated with the leaky homes era, lead to a discount in price.

• There are implications for local and central government policy from these findings.

A few months ago, the Chief Economist Unit published a study on the impact of higher-density zoning on housing prices in Auckland. To isolate the impact of increased zoning, we had to account for as many other attributes that add to or subtract from a property’s value.

Though the purpose of that work was to look at how zoning affects property values, the models we developed yielded statistically significant results on how much values change due to other amenities of the property.

Size matters

The average dwelling sold in Auckland over the past eight years was approximately 135 square metres (including integrated garages). Across all of New Zealand, new homes tend to be significantly larger than older homes1. Houses built in the 1970s were typically in the 110-120 square metre range. By 2010, new homes being built were approaching 200 square metres.

Our research unsurprisingly found that bigger homes sell for more money. Across the Auckland Region, each square metre adds approximately 0.3% to the value of a home. On the central Auckland isthmus2, where there is no greenfield development, this corresponds to roughly $4,200. Across all of the non-isthmus Auckland Region, each additional square metre adds about $2,500. These figures are roughly consistent with the marginal cost to build an additional square metre.

On the isthmus, where almost everything is already built up, adding space often necessitates a renovation. Elsewhere in Auckland, where already built houses are competing with new build construction, the premium for extra space is lower. Adding extra space to a house that has not yet been built is cheaper per unit than renovation, and this is reflected in the prices.

Getting in the (school) zone

Anecdotally, “everyone” knows that houses in good school zones are worth more. What constitutes a good school is a value judgment, but as a proxy, income deciles are often used. This is not a perfect measure, and wealthy parents do not guarantee good students and good schools. However, achievement and school decile are correlated3.

Data on school deciles is readily available, so it was straightforward to include in our model of Auckland house prices. Because some homes are zoned to several different schools, we selected the highest decile in-zone school as representing the house’s “school zone”.

We found that across the entire Auckland Region, all else equal, a house in a decile 10 zone would be sold for around $225,000 more than an identical house in a decile 1 zone. This pattern is consistent across the region. On average, each additional decile adds about $22,500 to the price of a home.

There’s also the issue of Auckland’s “doublegrammar” zone – where houses are zoned for both Auckland Grammar and Epsom Girls Grammar. This was accounted for in addition to the decile, and all else equal, houses in this zone are worth an additional $130,000 over and above houses that are not. All told, a home being located in the doublegrammar school zone adds massive value compared to an otherwise identical home zoned for a decile 1 school.

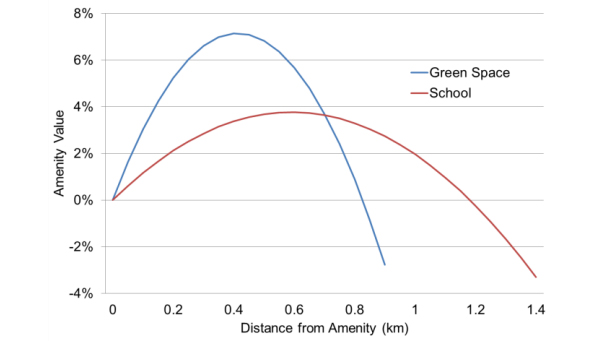

The goldilocks of amenity access

Houses prices are also affected by how near they are to certain amenities. We structured our model so that an optimal distance from certain amenities could be calculated. For many people, the ideal location to certain amenities is not too near, not too far, but just right. Take schools, for example. Schools are loud and subject to lots of car and foot traffic. Most people with children would like to be located a short walk from the school, but not right next door.

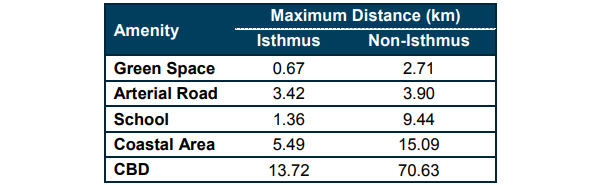

On the isthmus, properties located right next to either schools or green space are valued less than those located a short distance away. For these amenities, there is a “sweet spot” for value – not too close and not too far. Property values are maximised (all else held equal) 410 metres from green space, 590 metres from a school, and as close as possible to the coast (i.e., waterfront).

These findings have implications for local policy, such as park service provision, and for central government services such as school location.

In the rest of the Auckland Region, the optimal distance from any amenity is basically as close as possible. Of course, since it is possible to be much further from amenities in greater Auckland than on the isthmus, it makes sense that proximity is more valued. On the isthmus, no matter where a property is located, the maximum distance from a school is about a 20 minute walk. In the wider Auckland region, you can be more than 9km from a school.

House values that have sprung a leak

It is well known4 that potential buyers have avoided monolithically clad homes – even ones that are weather tight – because of the leaky homes scandal. Thus, it’s not surprising that these homes have sold at a discount relative to other types of homes.

What is remarkable is that the stigma of monolithically clad homes still persists. Even though the extent of the leaky homes liability has become increasingly clear, many of these homes have been repaired, and testing is available to determine the water tightness of a home, monolithically clad homes have continued to sell at a discount.

Our research suggests that monolithically clad homes across all of Auckland, built in the 1990s or 2000s, still sell for about 15% less than similar homes that don’t look like a “leaky home”. Again, this does not mean that all these houses were actually leaky, or that they were unrepaired. It only means that monolithically clad houses built during this time period have a stigma about them regardless of the quality of construction.

Put another way, two identically sized houses on identically sized sections, next door to one another, would, on average, have a 15% price differential if one of them was monolithically clad. This is equivalent to about $140,000 on an average house in Auckland.

Given the scale of this impact, and the challenge of preventing other examples of building system failure, the policy implication of this finding is clearly for better alignment of risk and responsibility, as we argued in our paper on mandatory building warranties.

Notes:

2. The isthmus is, for these purposes, defined as the area covered by the old Auckland City Council with the exception of Waiheke Island and Great Barrier Island. This is roughly the area from New Lynn to Otahuhu.

4. For example: http://www.nzherald.co.nz/leaky-buildings/news/article.cfm?c_id=562&objectid=10507795 and http://www.nzherald.co.nz/nz/news/article.cfm?c_id=1&objectid=10617051

*Shane Martin is an economist in the chief economist unit & David Norman is chief economist at the Auckland Council. This article was first published here.

62 Comments

Well that's useful. A research study on property values minus any treatment for parameters such as availability of credit, cost of credit, and market distortions from central govt and local govt policy. Real cardigan, slippers, and hot cup of tea stuff.

Affordability, available credit isnt the point of the study.

And why is that? Do those have any relevance to the value of property? The research is trying to isolate the different factors that drive the value of properity. What if the amount of credit is the the largest driver of prices or values?

The effect of credit overtime is revealed in the hedonic coefficients (or, more specifically, the constant in the case that elasticities are the core focus)..

Only if you're modelling the availability of credit (independent) will a coefficient be derived for the value of housing stock (dependent). This research is not modelling availability of credit.

No.

A hedonic regression reveals two things; price, and the elasticity or marginal impacts of variables.

This is based on the observed characteristics of the goods.

In revealing price, it is inherently accounting for the issue of credit expansion. The effect of which can be proxied by the change in hedonic coefficients (in levels) over time.

i.e. as credit expansion increases, so does the marginal impact of characteristics on (nominal) price.

Also, credit is not exogenous in the case of house prices so you would be stupid to put it in any specification with nominal property prices.

Nymad, Can u tell me if I have this right?

Hedonic regression is about the qualities (constituent parts) of a "product" that may influence the demand for that product, and which may result in possible changes in price for that product.

Cheers.

Roelof,

Correct.

A hedonic regression estimates price as a function of the observable attributes of a good. Essentially it assumes that price is the sum of the utility value of all the observed attributes.

So, change the attribute, you change the price by a given factor.

It's important in this case as it sort of highlights why we build certain houses.

In the case that there is a high markup potential in certain attributes, the preference for supply will be to exploit this.

Nymad,... thks

I'd qualify what you have said here..

I don't think it necessarily highlights why we build certain houses.

Take size for example.... I have been told that part of the reason we build bigger houses is because of the high land cost component.. ie. For a given piece of land , a developer will build the biggest house possible , in order to maximise return.

This tendency may well result in "shaping " apparent demand for bigger houses..??

SO... I can see the usefulness of Hedonic regression, and I can also see that the relevant "industry" experience and knowledge is required to get the " full picture " and contextual understanding ..

Ironically you were trying to school people about hedonic indices on another thread.

Now you can't even recognise what the point of hedonic analysis is...

Not sure what this research paper has to do with hedonic indexes. There is no explanation of the methodology.

This is literally the basis for how they are estimated.

1st step: estimate a hedonic specification.

2nd step: estimate an index based on prices estimated from the hedonic coefficients.

3rd step: show everyone the pretty constant quality and mix index you have created.

In their own words:

To determine the value of upzoning a property, we used four years of housing data. Data includes information about the sale (price, date) and the property (when it was built, parcel size, dwelling size, garage spaces, views, decks, construction material and so on).

We then merged this data with information on zoning before and after the implementation of the UP, as well as the distance of the property from various amenities (green space, main roads, schools, coast,and CBD), which created a profile of each property sold between 2013 and 2016. In all, we were able to successfully profile almost 110,000 residential property sales. We did not include properties in the

CBD as these are not comparable to properties elsewhere in Auckland.

It all depends on the the independent variables used. All I'm saying is that the availability of credit and cost of credit is not used, therefore it's unclear whether or not this research has any strong relevance. It proves and quantifies some factors such as close to amenities may impact the value, but that has limited meaning if it's not actually the primary diver of value.

Again, see my comment above.

The method they use is literally the basis for creating hedonic indices.

Credit expansion is captured in the price variable structure. To put some arbitrary measure of it in a standard hedonic specification is pointless because it isn't an exogenous hedonic factor.

The relevance is in question, but not from your argument's perspective.

Obviously dependent on whether you take the perspective of Rosen (1974) or Pakes (2003) will have a big impact on the interpretability of the hedonic coefficients. This is getting out of the scope of understanding here, though.

The method they use is literally the basis for creating hedonic indices

How do you know? The methodology isn't stated, except for what I posted about. There are many kinds of regression models that could be applied here. The objective is to understand the relative impact of the independent variables on values.

It doesn't matter.

As you say, they are estimating hedonic coefficients ( relative impact of the independent variables on values).

Hedonic coefficients are the basis for hedonic indices.

A linear / logistic regression can do what is achieved here. Building a hedonic index is not necessarily the answer.

Have you ever done regression before?

A linear / logistic regression

I can only assume that you mean in an OLS/MoM context?

But, yes. Correct.

And what would that give you?

Perhaps a vector of estimated hedonic coefficients?

Obviously the logged coefficients will be interpretted as elasticities, though. But that is beside the point.

Have you ever done regression before?

I know for a fact you have no idea about regression methodology (which is evident from your misunderstanding), so don't throw stones.

All linear regression is based on least squares. A "linear regression" does not give "hedonic coefficients". A hedonic regression would.

And yes, I have used regression analysis in a professional context -- supply chain analysis, segmentation, and conjoint studies for demand analysis. I don't claim to be an expert, but I will not try to talk about what I don't understand, much like it appears you're doing.

You said, A linear / logistic regression.

Obviously because you are so smart you would realise that in the loose term of 'logistic' regression you normally refer to binary response models like logit/probit/tobit.

Obviously just because you know the model, it doesn't mean you understand it.

This is evident in your linguistic terminology.

All linear regression is based on least squares. A "linear regression" does not give "hedonic coefficients". A hedonic regression would.

Again.

A hedonic model is almost 100% of the time estimated with OLS.

Again, because you are so smart you might be able to understand why - Gauss Markov, and simplicity being the main reasons.

You are just confusing yourself. A hedonic regression isn't a type of econometric methodology. It is simply the application of economic data to an OLS context.

As for your regressions. They must be absolutely garbage.

You are advocating the usage of endogenous variables and if you fail to understand the basic mechanics and setup of the models, there is no way that you can be estimating variances correctly.

Hes mistaken what the study aims to achive which is estimate the relative contribution of certain factors to the price. His point more broadly is still correct just unrelated, credit is the main factor driving overall values, but is probably not a major factor in the relative price of two properties in the same credit market.

Hes mistaken what the study aims to achive which is estimate the relative contribution of certain factors to the price. His point more broadly is still correct just unrelated, credit is the main factor driving overall values, but is probably not a major factor in the relative price of two properties in the same credit market.

Well that depends. For example, assume in the case of a property crash where the prices (proxy for value) in areas such as Remuera fall more than in Glenfield, what does that say about the validity of the research? If proximity to good schools and amenities, then that would mean that the relative fall in values should be greater in places such as Glenfield, etc.

Again, you are misinterpreting.

Price isn't and exogenous variable in this case. The exogenous shock doesn't impact prices directly. It impacts exogenous variables that are correlated with prices.

The change in some exogenous factor(s) (these hedonic factors) impacts prices in this framework, not the other way around.

Price or value would be the dependent variable in this model. It has to be.

Exactly - it's the endogenous variable.

So it isn't okay to talk about the impacts of a price crash.

What you talk about are the factors that influence the exogenous variables to instigate a price crash.

OK, I see your point. "Endogenous" as the "dependent". I still say that this research is fluffy under the assumption that a credit-driven asset bubble is in full flight. Intuitively, we already know that houses near good schools have higher value. However, that does not validate any quantifiable driver. Furthermore, it does not explain the impact of a credit-driven bubble on the independent variables.

Again.

It does likely factor the impact of credit.

Credit isn't likely to be impacting the marginal utility of the specific exogenous variables in the case that 'affordability' isn't changing. In the case that a normalised measure of value (such as affordability) was changing drastically, we could assume that the marginal effects of certain characteristics was changing too.

Sure, credit expansion is increasing nominal prices (or, you could argue that the relationship is endogenous - prices are increasing credit expansion). However, this will be captured in the constant of the specification.

OK, I see your point. "Endogenous" as the "dependent". I still say that this research is fluffy under the assumption that a credit-driven asset bubble is in full flight. Intuitively, we already know that houses near good schools have higher value. However, that does not validate any quantifiable driver. Furthermore, it does not explain the impact of a credit-driven bubble on the independent variables.

Obviously just because you know the model, it doesn't mean you understand it.

No I don't know the model because it's not explicitly stated in the 2-page pdf.

A hedonic model is almost 100% of the time estimated with OLS.

Least squares is the basis of linear regression. You're not baffling me in any way.

As for your regressions. They must be absolutely garbage.

Whatever you say. Seems to have worked though and have been far more insightful that you rambling on about what appears to be something you have have a sketchy understanding of.

Obviously just because you know the model, it doesn't mean you understand it.

That was with direct reference to your confused terminology. Not the methodology of the research here.

Seems to have worked though and have been far more insightful that you rambling on about what appears to be something you have have a sketchy understanding of.

If my understanding is sketchy...I'm sorry, but I hate to say what that implies about yours.

Obviously this isn't a congregating place for econometricians (unfortunately), but if it were, they would be taking my side in this discussion.

Nothing is confused. I know exactly what I'm talking about. If I didn't understand what I was talking about, I would say quite openly. I will think you will find that linear regression is the basis of econometrics. You may disagree,but I'm not going to battle you about it.

Humm yes quality is certainly an issue considering that most properties in NZ are glorified sheds. It always fascinated me that you could get a mortgage without a building report, even after the leaky homes scandal. And people would regularly risk not bothering to get a full building inspection before buying even with a shoddy property.

No way could you do that in the UK, you wouldn't even dream of taking that kind of risk there.

I think you'll find that during asset bubbles, almost anything is expensive -- regardless of "quality" -- relative to income.

Yeah too bad that AKL bubble is now deflating.

It is certainly my observation that large, good quality houses in good locations are continuing to get exceptional prices. Properties in the three to four million range seem to have no difficulty selling. I am surprised that there are so many buyers for these sorts of properties.

Size and quality is even trumping location for some buyers.

It is certainly my observation that large, good quality houses in good locations are continuing to get exceptional prices. Properties in the three to four million range seem to have no difficulty selling. I am surprised that there are so many buyers for these sorts of properties.

Size and quality is even trumping location for some buyers.

Yep. A house on Hurstmere Road gets a better price than on Onewa Road, but the research is not about the likelihood of houses selling.

Isn't it about the likelihood of properties selling in a way though? Instead of location. location, location it is now quality, size and location. It reads to me as an advisory for property investment. Focus on these three things rather than just location. Worst house in the street principle may no longer apply due to the increasing gap between 'haves and have nots' and changing demographics.

A year or so ago I thought that it was pretty risky buying a two million dollar house, now I see that it was a gamble that paid off.

Buying a $2 mio house is only risky depending on your aversion to losing some or part of $2 mio.

" I am surprised that there are so many buyers for these sorts of properties."

seriously? have you been living in a cave on an isolated island for the last 10 years?

The gulf between the haves and have nots is at record levels

https://www.radionz.co.nz/news/national/307458/10-percent-richest-kiwis…

So how many people working in the council are we paying to do this stuff? Like work out that bigger houses sell for more? 10? 20?

And leaky homes sell for less than non-leaky homes. It seems the objective is to quantify the value of upzoning a property.

Actually it pretty useful.

eg if the value ppl add to a property per sqm is $4200, if you are extending your property at $3200 sqm them you are making around a 25% profit margin. If its $2400 and the cost to build is $3200 its not such a great idea.

or ppl dont want to be too close to schools but 1/2km is considered ideal due to noise so when design and location is considered factoring that in might help with planning and improve outcomes.

Also sometimes its useful to prove the assumptions being made are actually sound and quantified.

Yes, I thought it was a really useful bit of research. It quantifies and confirms many of the things that we expect, thus taking them from hearsay and rumour, subject to much argument and discussion, to useful evidence. I particularly like the bit about it being cheaper to add extra space to a house that hasn't been built yet.

And think of the local GDP generated by all the earnest 'research' that went into this: many meetings over lattes in the locality, site visits and tiki tours to ensure that paper impressions matched on-the-ground-reality, hosted visits to open homes, and why, look, it's Christmas already, and isn't that the Tea-Person with the 10 am trolley. Let's reconvene in February and get some sorta paper out to show the managers we actually Do Useful Stuff here.

Amazing how much traction stigmas get. The monolithic cladding described in the article may well be avoided in Auckland but in other parts of the country people can't get enough of them; and these are places with a similar climate to Auckland.

If you have worked on fixing one you wouldnt be. Bad ones repair costs are not far off new construction.

Yes,why would you risk it...drive on by,plenty of others to choose from

Stating the obvious here. Apart from 'leaky' homes. Some of the chilly bins are poorly built as well as being leaky and sell at far more than a 15% discount. I know of one 240m house on a prime coastal section that has a $250,000 improved value in the latest CVs. That would be more like $700,000 if it was brick or wood. Auckland Council arbitrarily wrote down monolithic home values in the 2011 CV round. It wasn't widely reported. Here's a link:

http://photos.harcourts.co.nz/Harcourts.Public.WebTemplates/763/Files/V…

No great insights here. However, we should consider the relationship between council assets and property values more. For instance, why does the council agree to put a new library in a new subdivision without a contribution from the developer - who gains thousands from each section sale as a result/

Heard of development contributions?

Wow. Leaky cladding sells for less, desirable public school zone and coastal and or open space (parks) aspect sell for more. Hope this didnt cost to much to put together, though probably valuable for setting rates, and thus the rates hike in everyones immediate future.

Would suggest the dgz premium could have been 130k years ago but not today. Arrival of overseas buyers has probably made it 8-10x that hence the radically change demographic in those schools. A visit to New Market Primary will underline that.

I assume as the CV is set on similar homes selling price? and this research in effect is also based on that that there shouldn't be a significant change in rates.

If your zoned intensification is higher in the new plan you will pay more rates. Ultimately this forces owners sitting on hi-rise land to sell and move on. Having a hi rise on your northern boundary is never any fun.They also generally get a pretty big cheque from the developer.

Tough crowd to please. I enjoyed reading their insights, even though I knew there was a link between price and the various variables.

The point isn't about proving the link. It's about quantifying the link.

Great for me, 274m2 house incl double garage, 4 bedrooms with timber weatherboard in Old Greenhithe. 400m from a playing fields and 1km to school. Happy days.

""On the isthmus, properties located right next to either schools or green space are valued less than those located a short distance away."". This puzzled me. I can understand the attraction of living adjacent to water (a) view (b) no chance of something ugly being built to block view. I treat green space the same way - I have a long boundary next to regenerating bush and wouldn't swap it for a fortune. It has long puzzled me that houses backing on to our domain have no premium over houses on the other side of the road. In fact this study claims being over the road adds value!

Similarly with schools - lucky Auckland has schools which are about 80% green fields (unlike the UK where they were sold by dumb politicians). They have the same advantage of view and unable to block view and the minor disadvantage of noise during school breaks - that is daytime especially lunchtime on working days only. I used to live near a school and work from home - it is astonishing how loud a playground can be but just wait 15 minutes and silence returns.

"Auckland property's value is influenced by size, school zone, amenity access and cladding just as much as location"

School zone & amanity access IS part of the "location"

OMG just found out last night this DGZ character bungalow sold for $2.6mil earlier this month. It has a 2017 CV of $2.3mil - it just proves that school zone, house size, cladding, amenity access & location are all equally important ;-)

http://rwepsom.co.nz/properties/sold-residential/auckland-city/remuera-…

Get rid of school zoning.

Where schools are oversubscribed parents can bid for places.

The excess funds generated (ie. less taxpayer subsidy for the oversubscribed schools) can go to the poorer schools to balance up the performance.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.