With the government targeting housing investors and landlords, rental housing has become a bit of a hot topic and it shouldn't be a surprise there have been claims the result will be tenants facing larger rent increases.

However, the analysis of how rents behave in this Raving suggests the government's policies aimed at boosting wages are likely to be more important in offering potential for landlords to put up rents at a faster pace.

By contrast, there is limited if any link between changes in mortgage interest rates and changes in rents. The implication is that the inflationary path the Reserve Bank is currently set on will ultimately be much more painful to landlords and housing investors than the government's policies.

This Raving reveals major discrepancies in rents reported by MBIE and Statistics NZ that can't be explained by the former only covering private rents and the latter including rents for private dwellings and social housing. Despite trying to unravel the large discrepancies I couldn't, which left me in the somewhat uncomfortable position of not knowing how much the private rents reported by MBIE versus the market-wide rents reported by Statistics NZ are providing misleading indications.

The rental bond data reported by MBIE suggests the rate of turnover by tenants has more than halved over the last 25 years. This seems more than is likely which may further add to questions over the rental data reported by MBIE that is based on lodgements with Tenancy Services. But maybe this is what has occurred?

Finally I look at whether rents have increased more or less than incomes. The answer depends hugely on what data are used in the assessment making this topic a goldmine for those wanting to mislead because they are pursuing a political agenda.

Are tenants about to face larger rent increases as a result of Labour's policies?

With the government introducing policies favouring tenants over landlords and making life tougher for housing investors, rental housing has become a hot topic. There have been some suggestions the pace of upside in rents has increased or is about to increase.

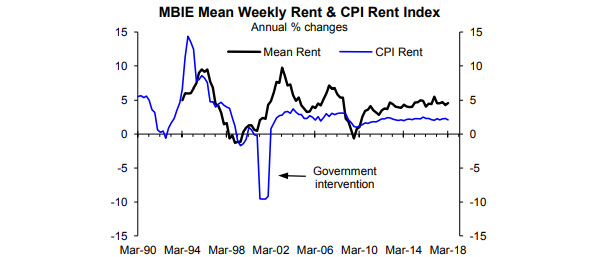

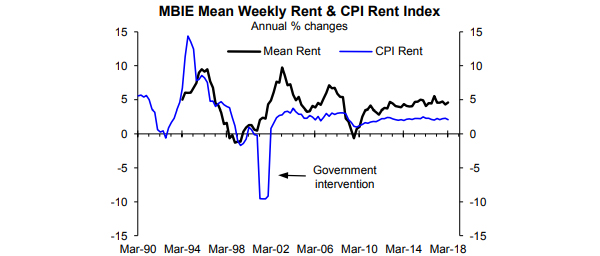

Similar claims that the pace of upside in rents is about to increase have been made on a number of occasions over the last few years especially about Auckland. But based on two national measures the pace of upside in rents has changed little since the 2008/09 recession had a temporary negative impact (chart below). The disparity between how much rents have been increasing based on the mean rents reported by MBIE that are based on bonds lodged with Tenancy Services versus the increases reported by Statistics NZ in the CPI rent component are discussed later.

By putting some people off being landlords and increasing costs for landlords Labour's policies may mean the pace of upside in rents increases a bit but there could be a larger impact from the policies aimed at boosting wages. This is because of the change in the behaviour of rents that has resulted from the new, low inflation environment that started in the early-1990s.

The evolving behaviour of rent inflation

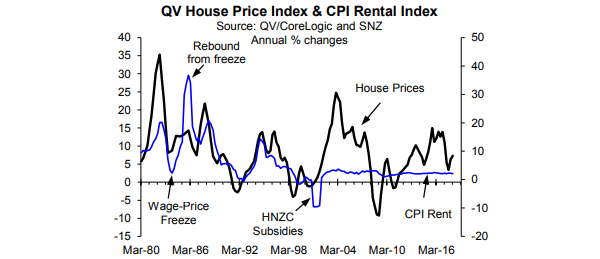

Prior to 2001 rent inflation based on the CPI rent component was quite closely linked to house price inflation if the temporary impact the 1982-84 wageprice freeze on rental inflation is ignored (next chart). However, after 2001 house price inflation continued to experience major cycles while inflation in rents became quite stable.

The introduction of large subsidies for Housing NZ tenants in the 2001 March quarter was why annual rent inflation turned temporarily negative in 2001. The CPI rent component includes private sector tenants and tenants of Housing NZ and other social housing providers.

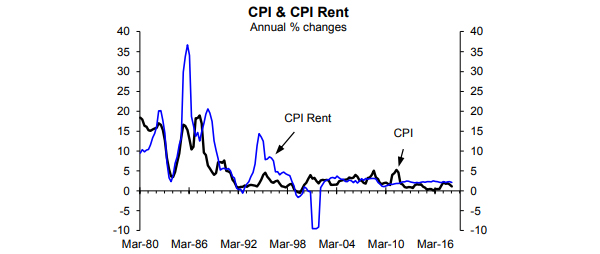

In the 1980s inflation in general was high including for house prices, rents, incomes and prices in general as measured by the CPI as shown in the chart above and the next two charts.

In the 1990s a low CPI inflation error emerged but house prices and rents continued to be largely linked and be much more cyclical than CPI inflation. Rents were still largely linked to house prices as a legacy of the earlier high inflation environment. However, by the time the 2000s boom in house prices arrived, low CPI and income inflation had existed for long enough they had taken over as the major drivers of rent increases; aided by how rents were set for social housing.

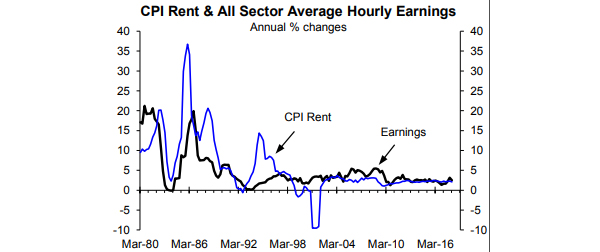

The chart below shows the reasonable link between rent and average hourly earnings inflation in the 1990s with both impacted by the wage-price freeze, the temporary delinking in the 1990s when general and wage price inflation had slowed but rental inflation still seemed to be linked to house price inflation and the subsequent period in which rent increases have largely returned to being linked to growth in average hourly earnings.

It makes sense that there is some link between rent increases and increases in prices in general incomes in part because of how rents on social housing are adjusted.

Based on the 2013 Census there were 453,132 rental properties including private rentals and social housing while based on the MBIE data there were 339,534 active rental bonds in June 2013 that covers just private rentals. At face value in 2013 around 75% of total rental properties measured by the Census rental number were private sector rentals. Qualifications apply to both numbers:

• In the 2013 Censes there were 97,053 households that didn't specify whether their properties were rented or owned, some of which will have been rented.

• It is an offence not to register a bond with Tenancy Services for private rentals but it is possible bonds aren't lodged for some rental properties (e.g. where people are renting from family or friends).

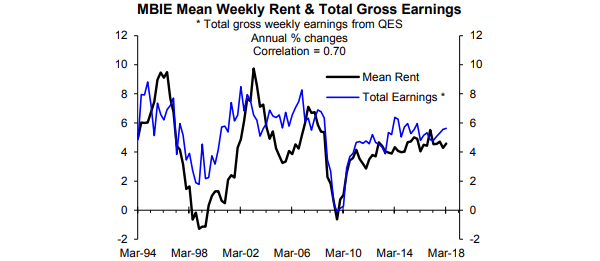

While it makes some sense that rents on social housing are linked to the likes of the CPI and increases in base pay measured by average hourly earnings the rental bond data reported by MBIE suggest that private sector rents have increased well above the level of inflation in the CPI and average hourly earnings. However, the chart below shows that the annual increase in the mean weekly rent reported by MBIE is reasonably closely linked to inflation in average total weekly gross earnings.

The lack of acceleration in private sector rental inflation in recent years most likely reflects a constraint from income growth that hasn't increased based on total gross weekly earnings inflation from the Quarterly Employment Survey. Total earnings include base pay measured by average hourly earnings and bonuses and other worked-related benefits, better reflecting total worker income.

The chart above suggests that the more Labour's policies boost wage and salary incomes the greater scope there will be for private sector landlords to put up rents. Labour's policies to boost especially wages include the 27% increase in the minimum wage over four years, plans for more pay equity deals and policies aimed at giving unions' greater scope to represent workers etc.

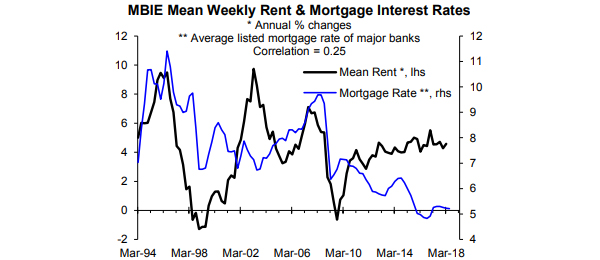

By contrast, there is no clear link between rent inflation and mortgage interest rates (chart below). As covered in our economic and housing reports, the Reserve Bank is set on a path that will cause an inflation problem; ultimately requiring lots of OCR hikes to fix, similar to what occurred last decade.

Interest rates aren't likely to increase as much as over the next several years as they did between 2002 and 2008. But sizeable/painful increases are eventually likely as a result of the Reserve Bank seeming to be set on repeating the mistake it made last decade of allowing labour cost and domestic price inflation problems to develop. This time around it will be encouraged by Labour's policies aimed at boosting wages but also residential building and infrastructure spending.

Why the major discrepancies between the MBIE mean rent and CPI rental component?

As shown in the chart below, since 2002 private sector rent increases as measured by the mean weekly rents reported by MBIE have generally significantly exceeded overall rent increases as measured by the CPI rent component that includes rents on social housing.

Based on the mean rents reported by MBIE for the three months ended March 2018 the average private sector rent increased 4.6% compared to the three months ended March 2017 while the CPI rental component increased only 2.1% over the same period. At face value this suggests that private sector rents must be increasing dramatically more than rents on social housing.

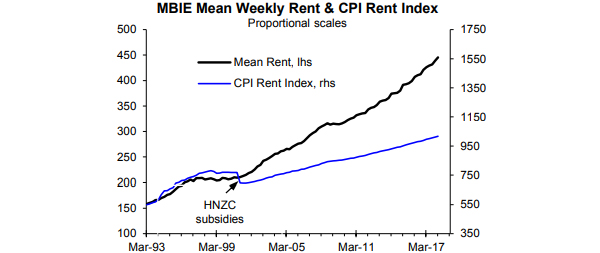

The difference is massive when the cumulative increase in the mean weekly rent is compared with the cumulative increase in the CPI rental component (chart, adjacent column that shows when Housing NZ subsidies impacted).

Excluding the temporary fall in the CPI rent component in the 2001 March quarter caused by large subsidies for Housing NZ tenants, since 2001 the mean rent reported by MBIE has increased on average by 4.5% per annum versus a 2.5% for the CPI rental component (arithmetic not geometric averages). On the basis that social housing makes up 25% of rental housing the implication is that rents on social housing have fallen by an average of 2.2% per annum since 2001. This could occur in one year if Housing NZ increased rental subsidies but there is no way that social housing rents have fallen 2.2% per annum on average since 2001.

The housing rentals component of the CPI includes private and local authority rentals, State rentals, and student accommodation. The CPI housing rentals index measures changes in the rents of all private, local authority, and State houses – not only those for which new tenants have recently been found.

By contrast, the MBIE rental bond data only reflect rents for newly lodged bonds each month for private rentals.

Rent increases for social housing will have been less than those for private sector rentals but it takes much more than this to explain the discrepancy between annual inflation in the mean rents reported by MBIE and in the CPI rental component compiled by Statistics NZ. The difference has meant the mean rent reported by MBIE has increased 46% since 2001 versus a 112% increase in the CPI rent component (chart above).

From year-to-year the mean rents reported by MBIE may overstate how much private sector rents on average increase. Based on the number of new rental bonds lodged with Tenancy Services each year compared to the active number of bonds at the start of the year, in the last year around 42% of tenants changed rental properties. Mean rents only reflect new rental bonds. They should give some reflection of what is happening to private rents at the margin but if sitting tenants on average face smaller rent increases than tenants who change rental properties then the overall increase in private rents will be less than the increase in mean rents for new bond lodgements. Statistics NZ alludes to this potential shortcoming of the mean rents reported by MBIE when it states that the CPI rental component is "not only those [properties] for which new tenants have recently been found."

This can explain why private rents on average most likely increase less in any one year than suggested by the mean rents reported by MBIE. But it is questionable whether it explains all of the large difference in the increase in the mean rents and CPI rent component since 2001. Over time mean rents reported by MBIE should reflect what private tenants in general have experienced in terms of rent increases. It is likely that tenants who don't change property for one or more years end up facing sizeable increases to catch up with current market rents when they do change properties. Over periods of several years and more the mean rents reported by MBIE most likely provide a reasonably accurate indication of how much private sector rents have increased on average.

I am left with a sense of disquiet because I haven't been able to explain to my satisfaction why there is such a large discrepancy between the mean rents reported by MBIE and the CPI rent component.Setting aside my disquiet, to the extent government policies boost the pace of growth in employees' incomes the greater scope there should be for landlords to increase rents. I suspect that this more than landlords responding to government policies aimed at landlords and housing investors will justify some upside in the pace of rental inflation.

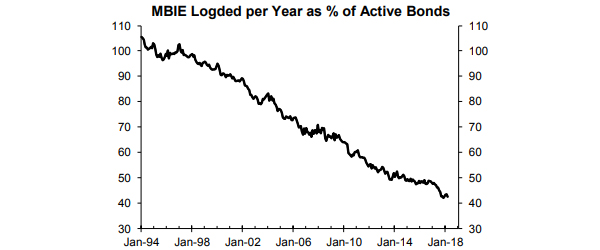

The MBIE data may reveal an interesting evolution in the behaviour by tenants

The percentage of tenants changing properties each year has fallen dramatically since 1994 based on the rental bond data (the next chart). While in the 12 months ended March 2018 there were 161,871 new bonds lodged compared to a total of 380,725 active bonds at the start of the year (i.e. approximately 42% of tenants changed properties) in the 12 months ended March 1994 99,551 bonds were lodged compared to 95,082 active bonds at the start of the year (i.e. there was slightly more than 100% turnover of tenants during the year).

The chart below suggests tenants have become progressively less inclined to change properties over the last 25 years. Having only become a landlord relatively recently I'm not sure if this is what has occurred or whether it reveals something fishy about the rental bond data?

If I had the time I would check the Census data to see if turnover rates by tenants had increased significantly since 1994, assuming it would reveal this. I'm not going to in part because Statistics NZ doesn't make it easy to extract data that covers numerous censuses.

You can tell whatever story you want to depending on the numbers you use

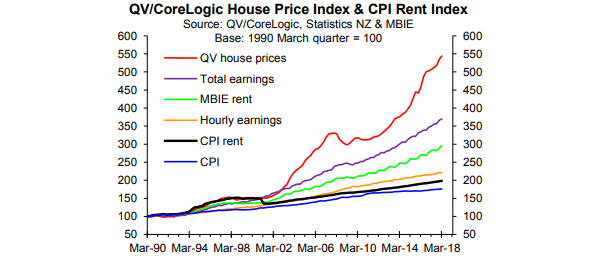

Have rents increased more or less than incomes? It turns out that the answer depends on the data you use (chart below). To have a bit of fun the chart compares how much house prices, incomes, rents and prices in general have increased since 1990 including two measures of incomes and rents. Probably of most important, mean rents reported by MBIE have increased significantly less than average total gross weekly earnings.

42 Comments

Not a mention of the single biggest factor in rent prices? Demand... in the form of immigration.

Yes. However, the past decade has seen a sharp increase in immigration, but not a corresponding increase in rents.

There is however a close relationship (either correlation or causation) between immigration and house sales prices.

Or supply... in the form of new building.

Interesting stuff. I think a discussion of the accommodation supplement would be interesting in that I believe that it is a subsidy of both landlords and employers. Namely that the higher accommodation supplement in Auckland has added to the relocation of industries to Auckland.

What is also interesting is the price elasticity of demand for rentals. My perception is that as rentals went up, people were effective in finding alternative renting options. This is evident by the relatively small increase in rentals in Auckland relative to immigration or house prices. My 'heroic assumption' is that in response to small increases in rentals resulted in more students into small flats, flatmates into FHB houses. boarders into older couple houses etc.

Whether bonds are lodged or not may be influenced by the "background" of the property owner.....

See, I'm not racist.

.

Is anything much sold on the cost plus a %? I would suggest that the price of most things these days are set at what the market will bear and have no relation to overheads/costs unless its negative in which case no one provides it. So by and large I simply dont think landlords can put up rents by much until wages go up. In fact I suspect that rents are at best going to be stagnant for years. The best thing the Govn can do then is ring fence the losses that can be claimed as tax relief and make "landlords" bail out and sell to FHBs.

Rents are constrained by h'hold income. The greater the proportion of income allocated to rent, the less is "spent" into the economy without income growth or greater consumer debt. Income growth is flat-lining while consumer debt is probably pushing its limits.

Ahhh. Rodney's monthly misadventures in correlation.

I am left with a sense of disquiet because I haven't been able to explain to my satisfaction why there is such a large discrepancy between the mean rents reported by MBIE and the CPI rent component.

Not really rocket science.

These things measure different things - the word mean in the MBIE data should be one big hint.

The MBIE data is not of constant quality or mix and is measuring new lodgements only. Estimating inflation based on this is a fools game. (They do release data by SAU - given the huge amount of spatial dependence in housing markets, this might be an elementary way of somewhat stratifying the data)

The CPI rate of inflation is constant quality and mix.

This is why the figures don't reconcile (or the discrepancy for social housing doesn't explain the difference).

You sure about that nymad.?

CPI rent may be better quality of like for like rental properties, but it is a smaller sample size.

CPI rent seems to be calculated based on a "survey"...( sample size of 9000 rentals approx. )

http://archive.stats.govt.nz/browse_for_stats/economic_indicators/CPI_i…

I'd say the MBIE data based method as probably being more relevant , in regards to rental price "inflation ".

This rings true with my anecdotal experience as a landlord.

When my mortgage interest rates rise or my costs go up for some other reason (like the gardener increasing his rates), I wouldn't increase the rent to cover this - I wear the cost. I generally only increase the rent when a new tenancy begins, and my gut feeling is that the rental rate I achieve is determined mostly by what tenants in the market can afford to pay, not the costs that I'm incurring as a landlord.

In theory, Labour's policies will increase incomes. Given that rents have followed income for the last 25 years, I think we are going to see a sharper up-tick in rents.

In theory, Labour's policies will increase incomes. Given that rents have followed income for the last 25 years, I think we are going to see a sharper up-tick in rents.

Do you want to elaborate on why govt policies will increase incomes? Labour are really not much different from National in their myopic focus on constraining public debt. How does that relate to increased incomes?

When you legislate an increase to the minimum wage some one on the minimum wage will have an increased income...

So how does increased minimum wages translate into higher rents? You're talking about the most cash-strapped h'holds in society. Furthermore, assuming that increased minimum wage does impact rents, to what extent do you think it will enable landlords to increase rents?

Renters in the market compete with each other for a scarce resource, being rental accommodation. Their incomes determine how much they can afford to pay. When their collective incomes rise, they can afford to pay more, and because they are competing with others who can also now afford more, they push rental prices up.

Minimum wage increases will increase entry level property rents. Income rises at the other end of the spectrum will increase the price of high-end rentals.

Did you see the graph in the article showing that rents rise and fall with income?

Sweet if we don’t want rents to go up then lower the minimum wage/

Minimum wage increases will increase entry level property rents. Income rises at the other end of the spectrum will increase the price of high-end rentals.

Really? How do you know? To what extent will an increase in min wage impact rents? Listen. I will answer that for you: "you don't know." You're spinning a narrative that you think makes sense.

Did you see the graph in the article showing that rents rise and fall with income?

Yes. But so what? I would argue that the relationship might be different if I were only looking at minimum wage earners.

OK. Glad you saw the graph, but a shame you dont understand it.

OK. Glad you saw the graph, but a shame you dont understand it.

The graph has nothing to do with the increase in rents or incomes for minimum wage earners. It is an aggregate of all rents and incomes. That's almost as meaningless as suggesting that if the CPI increases 1%, the cost of living for all h'holds increases 1%.

Why the fixation with minimum wage? My original post was that labour’s policies are likely to increase wages (mean and median) and that rents will follow, as has been the case for the last 25 years. My comment that rents are likely to rise seems to have struck a nerve...

But since you asked the question - Minimum wage earners rent houses at the cheaper end of the spectrum, so it is the rents of lower-end properties that would be affected most by an increase in minimum wage. But Labour’s policies won’t just affect minimum wage earners.

Still not convinced you understand the table, I.e the reasons for the correlation between wages and rents.

Labour have run on a policy platform of increasing wages. This article mentions a couple of specific policies -

"Labour's policies to boost especially wages include the 27% increase in the minimum wage over four years, plans for more pay equity deals and policies aimed at giving unions' greater scope to represent workers etc."

I said that IN THEORY Labour's policies will increase incomes, which is true. Whether they will be successful remains to be seen.

National and Labour's wage policies are like chalk and cheese.

Rodney makes it a bit complex for himself, and with all those graphics.

I agree with Steven. Costs have not much at all to do with it. Whatever your cost basis you charge what you can get. Many decades ago when I was dumb enough to deal with private tenants it went like this. I charged a high rent and still got tenants in. But then I found tenants were in trouble with the high rent and needed to exit. Painful process.

So then I cut back the rental a bit, still got tenants in, and they stayed. Much more fun.

Point is that what the 'right' rent had no relationship to the costs I had.

As an aside, a hotel room in Queenstown that cost you $200 a night three years ago can now cost you $350. Nobody suggests that the owners costs have near doubled

But the data he uses is rather interesting. So last graph, I shows clearly rents do not follow QV (house price inflation) but the renters income. The Q is then that increasing gap points at decreasing viability of being a Landlord ergo the only thing that makes sense tehse days is chasing capital gains.

This also means then that increasing the accommodation supplement just puts more money in landlords and then banks pockets. Bitch to be a renter in the lower echelon of course. that is a clear pointer to the Green's (if no one else) that handing out more accommodation supplement will go straight into the speculators and banks coffers even making house prices rise. So if you really want to spend the money to make things better for poor ppl, better to put the money into HNZ taking more ppl out of the trap and giving the Govn an asset.

Indeed. Rents don't go up much without incomes to pay for it. What "population growth" (the current platitude for mass immigration) does instead is drive down living standards as people cram together like sardines.

It would have been hilarious watching these astute investors pay way over the top for properties with absymal rental yields if they weren't just nullifying their lousy investments by avoiding income tax.

Thank God the CoW (coalition of winners) is shutting down that particular rort.

I hope so.

Hi Rodney

Thanks for the article, interesting as usual.

Statistics New Zealand has an elaborate procedure for collecting private rents. it collects all the rents within about 350 meshblock regions up and down the country. Landlords are regularly surveyed, and if they increase rents within a tenancy, or between two tenancies, this is captured.

As far as I understand, if there is a new rental property in the meshblock, the property is included in the sample, but its initial rent is not included; just changes in the rent. Thus if there are 30 rental properties in a meshblock and the average rent is $400 and the rent on the new property was $500, this "one-off" increase in aveage rents is ignored; but all subsequent rent increses in the 31 rental properties are included.

I am not 100% sure if this is correct, but you might want to check it out. I think the crucuail issue would be whether for a particular house any rent increases that occur when landlord 1 sells to landlord 2 are included in the CPI. If they are not, the SNZ series might systematically record lower than true rates of inflation (assuming landlord 2 does not significntly improve the property when he or she purchases it and raises the rent).

This procedure, which seems reasonable, could explain some of the difference between SNZ and MBIE rental series, although it seems a stretch to believe it would be a lot of the difference. It would be important if rental properties changed ownership a lot, and the rent for these new rentals were substantially higher than the price of existing rentals.

Andrew

Andrew,

anecdotally, my experience is that quite a few landlords charge market rent on first letting their property, and then , as the tenant turns out to be decent and longstaying, the landlord will only increase the rent incrementally . ( lagging actual mkt rents ).

If this is somewhat true , then it is possible that the meshblock survey method used to determine CPI rent might not properly reflect rental inflation, in the same way that MBIE method that monitors actual rents of new rental contracts.( which one would think would be at mkt determined rents.???? )

Good grief - what would ever happen if we ever reverted back to 2002 equivalencies.

In terms of rentals - I've always gone about 10% below market (how "market" is determined is irrelevant for me) - happy tenants for many years, happy me.

For me, I'm either low or no borrowings - in a general sense costs don't matter - what matters, again - happy tenants, happy me.

One becomes a landlord to invest ones money with the aim of growing it with investment returns. Landlords are often seen as the devil but property investment is a business at the end of the day. It is not a charity. Tenants on the other hand are often painted as the innocent victim.

This mentally is completely irrational and simply puts emotion into any analysis of rental markets. Once we treat landlors like business owners, as you would a dairy owner selling icecream, then we will have more balanced & informed views of the rental market.

Okey dokey, then let's make sure for a kick off, as per any other business you pay commercial interest rates and let's make sure you are subject to the consumer goods act, and let's make sure that you can't just decide to "unsell" your goods to anyone in the form of arbitrary evictions.

That'll do for starters.

Oh and definitely let's stop subsidizing this business via a specific benefit for landlords, the accommodation top up.

To decrease rents and increase wages for the working poor simply reintroduce land taxes to increase efficient use of land, and reduce income taxes at the low end for low income earners or decrease GST.

The previous government reduced taxes in just the bottom 2 tax brackets. The current government repealed that legislation because it was a tax cut for the rich...

The previous government removed the top 39% bracket for the wealthy and simultaneously increased GST. They loaded up the poor.

Current government does not care about that, they only repealed the tax cut that applied to the bottom 2 tax brackets. If we compare ourselves internationally to successful countries with a similar population you might find that our marginal tax rate at $70,000 is almost 5x that of our rivals (Singapore). Their top tax band isn’t hit until you start earning over $320,000 and even then it is closer to our second lowest tax bracket than any other bracket.

0

Singapore can because they don't have social welfare. Downside of the low tax rate is no financial safety net. Also no superannuation but they have a similar scheme to kiwisaver called cpf, which has a combined employee/employer contribution totalling 35.5% vs kiwisaver 6%.

That's the difference between looking at headline figures and actually understanding how our "rivals" operate though, I'm not sure Saddr01 cares about the actual facts, just the low tax rate.

For example their sovereign fund that keeps their taxes low is partly because the Singapore govt owns or partially owns a massive chunk of domestic businesses that operate in Singapore.

According to US Dept. state reports 6 of the GLCs (Government Linked Corporations) accounts for around 17% of the total capitalization of the Singapore Stock Exchange - https://www.state.gov/e/eb/rls/othr/ics/2012/191233.htm

They buy shares at market price when they add them to their sovereign wealth fund & certainly do not raise taxes to increase the size of their wealth fund.

The cpf like KiwiSaver is just mandatory savings, not a tax. It is still your own money which you can eventually use as you please.

There are more houses to rent available in Wellington, than there are houses to buy (many of the houses now available to rent, were previously listed for sale for many months and didn't sell). Several houses that have been available to rent have been sitting vacant for several months, and a few have since reduced their weekly rent (but still no takers). Of course none of that is captured in the sales data, as these properties were withdrawn from sale.

Landlords in Wellington almost ALL upped their rent this year after the media made a big fuss about shortages, however, the shortages only seem to occur at a particular time of year. Early Jan, everyone is on holiday but students suddenly start looking for properties before the start of term. And of course every year, this is when the media decided to report that Wellington has a rental massive crisis, even though the crisis disappears after a few weeks.

This year, after the media headlines about "queues around the block" landlords across Wellington put rents up. But this has simply resulted in their properties remaining vacant.

The only way this makes sense to me is that rental levels are attached to affordability, and no amount of media fluffing will change that. As a landlord if you overprice your rental, you will just have it sit empty so you have to eventually meet the market.

dp

There are a number of errors in the article. Firstly MBIE rents are based on new bonds lodged. There is a significant difference between what shows up on Trade Me rents and MBIE. MBIE even goes to the effort of publishing a rebuttal of TM figures. MBIE rents are lower than actual for new rentals. Secondly it takes a bit of digging to find the true meaning of Social housing on the stats department site. Social housing consists of Housing NZ and city council housing such as pensioner housing. Only 40000 of HNZ stock are let at IRRS rates. The remainder are let at market rates. Of the 500,000 private rentals only 200,000 receive Accommodation subsidy. The impact of AS is not as much as some would have us believe. The science of supply and demand should take into account the time lag between causal events and outcomes. The biggest single event in rental housing over the last decade was the change of depreciation rules. This imposed an additional one billion dollars of tax each and every year. That tax change made a lot of properties unprofitable and caused less properties to be brought to the market than was required to meet demand.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.