Westpac estimates the introduction of a 10% capital gains tax would see house prices fall by 10.9%.

Its chief economist, Dominick Stephens, has made the call in light of the Government’s Tax Working Group considering a suite of changes to the tax system.

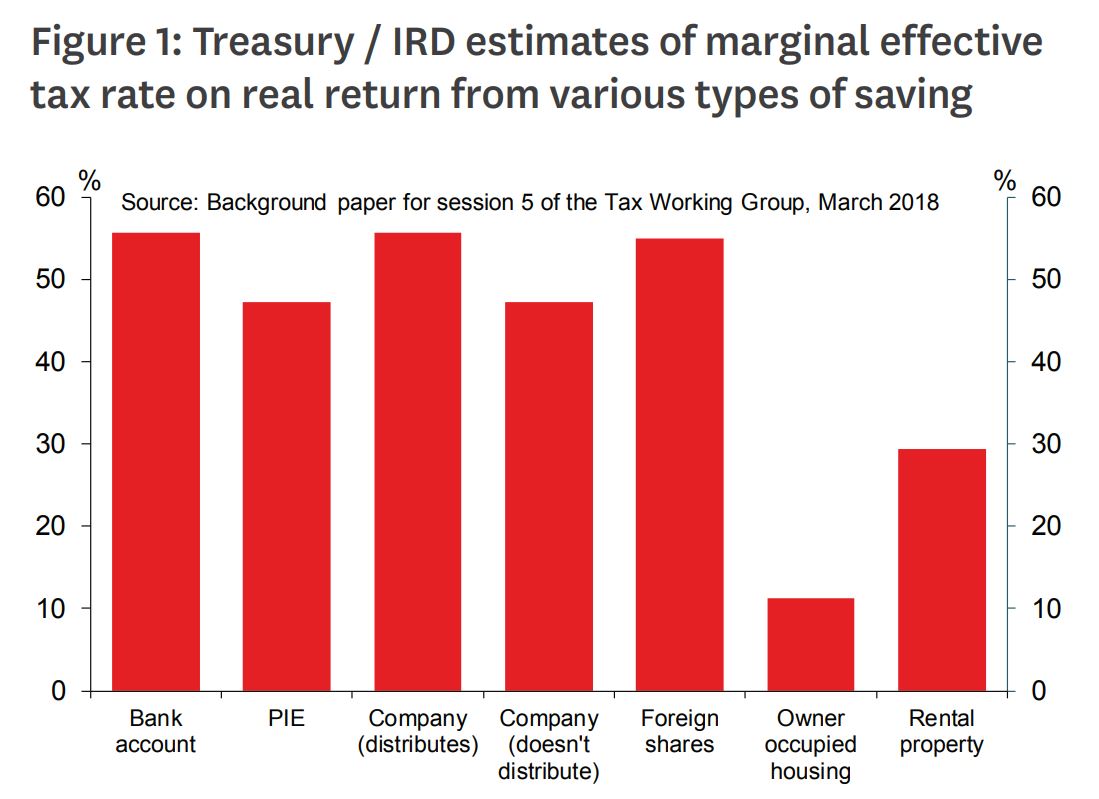

Treasury and the IRD estimate that currently property investors pay 29.4% of their after-inflation returns in tax, whereas bank depositors and owners of dividend-paying shares pay 55.7%.

Stephens’ modelling indicates the introduction of a capital gains tax, which would exclude the family home, would send prices down - not necessarily immediately, but possibly after a period of stagnation.

While this would see the rate of home ownership increase, renters would end up 5.5% higher.

“This extra expense would decrease the amount an investor could pay for a property while still realising a profit,” Stephens says.

"With fewer landlords, rents would rise.

“And with investors willing to pay less for a property, more auctions/tenders would be won by aspiring first homebuyers and the rate of home ownership would rise.”

| Impact on house prices | -10.9% |

| Impact on rents | +5.5% |

| Effect on rate of home ownership | Higher |

Ringfencing

Stephens says it’s difficult to put a figure on the extent to which soon-to-be-implemented rules around ringfencing will affect house prices.

From April 1 next year, the Government is planning to phase out landlords’ abilities to use losses on rental properties to offset tax liabilities from other sources.

Instead, landlords will receive tax credits that can only be used to offset future tax on their property portfolio – rental property tax credits will be “ringfenced”.

| Impact on house prices | 0% to -6% |

| Impact on rents | Up |

| Effect on rate of home ownership | Higher |

Stephens explains: “Ringfencing will not affect investors who have positive cashflow. The higher the leverage over an individual property, the greater the impact of ringfencing will be.

“For an investor running a property portfolio with 65% debt and 35% equity in perpetuity, we estimate that ringfencing will reduce the value of the investment by 6%.

“This seems like a sensible upper bound for the possible impact of ring fencing on house prices, but the actual impact could be smaller.

“After ringfencing comes in, we would expect to see fewer highly-leveraged property investors seeking to buy. This would allow less-leveraged property investors to win auctions/tenders more frequently.

“However, we do not know how far prices would have to fall before the less leveraged buyers enter the market.”

As for the other types of taxes the Tax Working Group will consider; this is how Westpac expects them to affect house prices:

Property tax, 0.5% (owner/occupier exempt)

- Tax calculated as a percentage of the value of the property, including the land and house - equivalent to the capital value used to determine rates in much of New Zealand.

| Impact on house prices | -10.5% |

| Impact on rents | +5.2% |

| Effect on rate of home ownership | Higher |

Land tax, 1% (owner/occupier exempt)

- Tax levied on only the value of unimproved land on which a dwelling is located.

| Impact on house prices | -9.5% |

| Impact on rents | +4.8% |

| Effect on rate of home ownership | Higher |

Stephens points out: “In our modelling, a 1% land tax has roughly the same impact on house prices as a 0.5% property tax. This is because our calculations are based on the average house, for which about half the value is in the land.

“In reality, properties for which land makes up a greater proportion of the value, such as houses with large sections, would experience a greater percentage decline in price, while apartments would experience a smaller percentage decline.

“Also, Auckland prices would probably fall further than prices elsewhere in New Zealand. This is because land makes up a greater proportion of the value of Auckland properties than in other regions.”

Deemed rate of return, 5%

- Tax aimed at removing the tax advantages property investors have over owner occupiers and over other forms of investment.

For property investors, rental income would not be taxed, and expenses (including interest) would not be tax deductible. Instead, the IRD would assume that investors are earning a 5% return on the equity in their rental properties. Income tax would be levied on that deemed return.

| Impact on house prices | -19.5% |

| Impact on rents | +9.6% |

| Effect on rate of home ownership | Higher |

Top rate of income tax reduced from 33% to 30%

| Impact on house prices | -2.8% |

| Impact on rents | +1.6% |

| Effect on rate of home ownership | Higher |

Stephens explains: “The size of the tax advantage of investing in property depends on the gap between the rates of capital gains tax and income tax. That gap can be closed in two ways – by reducing the rate of income tax, or by increasing the rate of capital gains tax.

“In the past, we have pointed out that increasing the top rate of income tax to 39% in 2000 enhanced the tax incentive for investing in property, and probably contributed to the increase in house prices between then and 2005.

“Reducing the top rate of income tax back to 33% in 2010 probably contributed to the fall in house prices that occurred that year.”

For details on the modelling Westpac used to draw its conclusions, see this note.

125 Comments

No mention of Australian house prices?

Ignore the pending credit crunch in Australia, apparently that’ll have no impact on lending here in New Zealand.

Makes for great headlines and every bank has an economist champing at the bit to get their name in print, but very few (if any) have ever got it right. A common sense investor in the real world can give you better advice and guidance. And this is the problem with our current leaders - all theory and zero reality. God knows what mess this lad's theories might set off.

This is a kooky comment ... “Reducing the top rate of income tax back to 33% in 2010 probably contributed to the fall in house prices that occurred that year.”

.... an admission he really doesn't know, it's just a best guess.

It is all just a guess. If you buy a house, get a 10% gain, sell it and pay 10% on that gain, you still get a 9% gain. Somehow this is going to crash prices by 11% because...

Very very few people would be influenced by this, and not enough to affect house prices, compared to the many laws they have introduced this barely registers.

Good point, 10% is way too low. It should be 33%.

Well, his (adapted) model actually inherently predicts that. So, he sort of has to believe it true.

The only thing he can't get right is the extent of the cross price elasticity.

The model is pretty poor now though. I dare say he has to make liberal usage of his residuals to parameterise his model to anything close to the observed market data now.

I agree, Dominique has become a bit of a lightweight economist really.

More than one statement and selective assumption blows the whole study out of the water ... There is no mention of Supply and Housing stock in this piece - if ignored then numbers are pure speculation !

Every measure of taxing Landlords, in his view, will increase Home ownership ... wonder what will happen to the numbers of renters and homeless people?? ... unless he is naive enough to assume that the Gov will fill the gap and build more accommodation and rentals to house the ones affected. Or he is silly enough to think that people will just sell for lower prices - If that was true we would have seen it in the last 9 months .. but Dominique knows better of course.

This poor economist forgets or simply ignored the fact that more tax on anyone propagates through the society and is More Tax on all the populous ... everyone in the food chain has to pay for that !!

Everywhere CGT was introduced , prices went up and are yet to come down .... We never learn from others, do we? ...

We don't have CGT yet have some of the highest prices in the world....

Wrong. The market (supply and demand) will determine housing prices, not a capital gains tax. Also who cares??? Houses are to be bought with the intention to live in them for 10+ yrs. Anything less and you're losing a fortune to real estate transaction costs.

Only a moron "invests" in single family housing. Way too many costs and headaches to deal with.

Wrong.

Taxes influences the market. That is the point of having taxes. to counter the positive or negative externalities.

Wrong.

Taxes influences the market. That is the point of having taxes. to counter the positive or negative externalities.

So you’re saying that CGT encourages vendors to ask a much higher price for a house than they would in the absence of CGT?

“Yeah man I’d easily get $40k more for this house if there was a capital gains tax”.

Not really so, but in fact sellers will want the buyers to pay ( or share) that CGT tax with them so they will ask for a higher price .. someone should pay the piper ! .. so if everyone does that prices will go up ..

exactly like RE commision that in reality is added to the property actual price ....

do private sellers discount their properties by 50K ? or ask for the full market price for a similar house sold by their neighbour ?

Yeah, some life realities are bitter indeed.

Read up on tax theory Eco Bird.

Ironically you accuse Stephens of being a poor economist, however you appear to have no idea how ad valorem tax works in a Marshallian system.

No, apparently I don't ... !! lol

Some of us chose to leave tax theories to those who indulge in fantasy world and academic research ... others, who don't know how ad valorem tax works, have a stake in the game and a finger on the pulse ! ...

They just watch and read the "Ooops, we got it wrong statements " and justifications of what happened in due course.

Eco Bird, when your Bank Manager performs a regular financial health check on you, will you call him/her a lazy and spoilt guarantee seeker like you called me ;-)

My bank manager RP, he/she is my business partner ...

You are just a lazy and spoilt guarantee seeker trolling about thinks you admitted that you know nothing about ,,, you often make it clear to all and sundry that you want everything for granted and preaching to others to follow your investment "lifestyle".

I hope you , at least, notice that difference !! :)

"My bank manager RP, he/she is my business partner" Iol, that would present a conflict of interest and imply you're the recipient of liar loans. For once, what you say finally makes sense. Yes, lets all shine a light to your investment lifestyle shall we - NOT!

lol .. poor RP !!

MYOB and stick to your TD, and stay away from things you do not understand.. lol

Eco Bird, yeah - nah, to the contrary. Its crystal clear. You're merely a symptom of the froth. Readers can always count on there being loads of "highly intelligent" dribble in your comments ha-ha :)

I'll now leave you in peace so you can dry yourself off.

Well said Echo Bird. My bank manager, lawyer, Valuer, Re agent etc are also all my business partners. Few understand that we create a team and we're responsible for our team to perform

Yvil, as I don't need any of these. I will willingly plead ignorance to knowing what it must be like to want to pay these people's salaries. It's no wonder property junkies are demanding some return on their gambling escapades.

In your depression scenario, such cosey relationships with Bank Managers can turn quite nasty. At the end of the day, your bank is a professional Landlord managing their security. They expect you, by every legal means possible to guarantee repayment of the loan.

Ha ha, your bank manager is NOT your business partner. You are his customer and a source of revenue (and possibly also of grief) and if needs be they will throw you under the bus to make sure the banks interests are met. The bank is your friend, but only your fair weather friend. You are not a team, the bank is the residual risk holders in your properties and if needs be they will take control to protect their interests. If you become a risk to their business they will leave you at the side of the road, bleeding. The loyalty you have shown your bank will not buy you a cent of credit. You and eco bird are so sweet and innocent...you are bubble fodder

lol, I hope both RP and yourself feel much better after venting your venum ..haha, obviously you do not understand what business is ( maybe apart from selling things on TradeMe or behind a trade counter).

But your comments show others how disconnected both of you are from the real world

enough said ...lol

Well, I’ve worked in and for banks for 20 years and I’m worried about you, your thinking of how banks work bothers me...at your time of life, you can’t afford any major setbacks....take care

Well thanks, you have worked in and for banks , but you didn't quite work with Banks bobster ...not every customer is the same for the banks - I hope you learned that at least from your time spent with them.

we have been with them on the highs and lows for over 20 years, your theory about buses and left bleeding on the side of the road is just fantasy.

Take care.

Eco Bird, I also worked in banking 11 years from late 80s to late 90s. Trust me, your bank ain't your friend or your "business partner" So get real. I witnessed things I never thought was possible when the tide went out. I have trade shares, profited from some well managed funds and paid plenty of tax. I know when it's time to call it a day. This might help calm your nerves; https://www.whitcoulls.co.nz/bookkeeping-for-dummies-second-australian-…

Retired Poppy, I knew you were an ex-banker. It takes one to spot another fellow colleague who has worked in the industry. Your comments fall on deaf ears unfortunately. Sometimes it is better to save your sanity and just wait on the sidelines for opportunities. Why tip off the sheep? It's too much like hard work for no pay.

But that’s the point, right? You’ve only ever seen them in bubble mode? Well, that’s over now. GFC didn’t count cos the Aussie banks saved us, next time they’ll be ones holding the knife.

I had a dream about you last night (really)...I was in Koh Samui, it was boxing day, you were standing on the beach in your gold speedos (you looked GREAT) and the tide went out.....way out....and you looked really confused, you couldn’t understand what was happening....and then the tsunami appeared...but you said “I don’t see a tsunami, I don’t even know what a tsunami looks like, I’ve never see one”, and then you said “well I see the tsunami but I am really good at swimming in tsunamis”, and then the tsunami hit you, and you swam but then I realised you had never really seem a tsunami before... and you ended up losing your gold speedos....it’s just the kind of guy I am...

That dream was kinda like a metaphor....I can see what’s coming, but you can’t, and I don’t want you to lose your gold Speedo’s...for everyone’s sake...

haha, nightmares are horrible aren't they? ...

You assume that me, or some of us, are wearing loose speedos and are up to our ears in debt ... you are wrong... Not every investor is reckless.

In the event of such tsunami it will be a nude party and everyone will lose his shirt - that includeds you too ...

Be optimistic without taking a lot of risk, know the rules of the game and how to play ... hiding in a cave is not the answer.

thank you for your concern though...

Aussie banks didn't save us - government legislation stopping them investing in crap bonds did. Otherwise we would have been in the same mess as the US. Don't think for even part of 1 second that your banker is your friend.

Eco Bird, if you can manage to stay off your Bankers monthly AQ (Asset Quality) list, then you are doing well and you may just manage to keep your Banker Buddy from throwing you under the bus. There is no job worse than a banker having to make calls to their customers on their AQ portfolio list! A banker would much rather spend their time selling more debt to new customers and making their big bonus for the year.

TainuiBabe,

What are the quantitative and qualitative criteria that would land a borrower on the Bankers monthly AQ (Asset Quality) list?

For retail borrowers:

1) minimum bank credit exposure? 1.5mn? 2mn? 3mn?

2) near or breach maximum allowable LVR by bank? what level is this? 80% 90%

For business and commercial borrowers:

1) minimum bank credit exposure level - what level exposure? 2mn? 3mn? 5mn?

2) near or breach of maximum allowable LVR covenant as per lending agreement - what level? 65%, 70%, 80%? other ??

3) near or breach of interest coverage ratio covenant as per lending agreement - what level? 150%, 125%, 110%, 105%, other ??

Trust me when I say that your Banker is NOT your friend if your property values start to decline in a turning market. Bankers always reprice their asset books in a bear market and you can expect a call to book your next financial review sometime in the next few months.

And what is New there TB? ... we all know that and cut our cloth to suit accordingly ... you seem to be surprised !! and you sound like letting out a secret lol... we all get financial reviews periodically depending on our leverage and the books are constantly reevaluated in both Bear and Bull markets albeit for different reasons ....what is New? .. the tsunami is coming in few months ? ... well great that would bring excellent opportunities .

Some people had that " Call " in 2008 and everyone worked around the crisis smoothly .... today many businesses I know have that "health check" call on their businesses every 3 months to make sure that things are still running " adequately " and the loan is safe.

I am not sure why are you guys so concerned about people who mind their own business and have a totally different risk profile than yours ? ...do you think we are dumb ..lol ??..or you are super clever and need to warn us from the evil Banks ?

Not sure Why are you dishing out so many doomsday predictions and creating the fear of God in investors or buyers minds and hearts ... markets go up and down --- what's new?.. or is it the DGM attitude dominating your life ? Surely it couldn't be envy , God Forbid!

No one said My Banker is my Friend !!.... he is my Business Partner, he/she has a job to do and rules to follow ... and we know what they are and we keep each other happy ...most of the time! to run our business smoothly.

We are not sheep to be tipped or otherwise, as you put it TB !!.....BTW that comment was very rude and disappointing !!

We operate businesses with the help of Banks and other professionals as Yvil mentioned above just like any other business .... and usually the buck stops with the business owner / manager .. so every investor owe it to himself to be prudent and secure his business against potential risks and consistently run his solvency test scenarios and act accordingly.

If every business stops borrowing or payback his bank ASAP out of the fear that heavens might fall next week / month / year, and bankers will come knocking on doors, then we might as well all shut shop and go bush, live on spuds, watercrest, and carrots under a tree (mortgage free) !! --- the first to head that expedition would be the people who will lose their jobs and then their houses ...

How many SME businesses, employing thousands of kiwis, you reckon are open because banks have lent them money based on personal guarantees ( which means their family home is at stake if they muck it up) ?? .... few tens or hundreds of thousands maybe? .... will they all close down too when their house prices drop and get on the QA list ?

If it's not your cuppa guys, do not drink it, and please spare us the preaching just because one day you worked in/for a bank and became clear voyants of late !

thank you

Firstly CGT is not on prime residence and much higher CTG in other countries where it has always been the norm have run away house inflation .

Will it happen at Auction too?

Of course it will, it is about price expectation and market values - the details and breakdown of that value is dissolved in one price.

do you see anyone selling his house voluntarily at 50 -100K less than the market ( unless they are desperate..) ?.. of course - Not.

Housing = long term place to live, with very high transaction and maintenance costs.

Investment = liquid, produces income, expectation of increase in value coupled with risk.

{kind=link}

I have never voted in my life until last year, when I thought it would be worthwhile in order to make a change. Always thought politics was for the gullible. I have been proven correct. Never again!

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12…

I agree, another lot over promised and are under delivering as always. Round we go.

Labour, so desperate to come back in power, clearly had no idea what they were talking about when making those promises. For god sakes, Labour voters should've known better at the very beginning when Jacinda decided to join forces with Winston as to what a disappointment this government would be.

And still less disappointing that the previous government.

At least they are doing something

I find a lot of people are saying “at least they’re doing something” now. What if it’s counter productive? Why not say “I think what they’re doing is benificial?” Do you prefer action over good outcomes?

It's a coping mechanism for them.

I really despise the "Us" vs "Them" mentality in US politics, I would hope that NZ and MMP it would be less about choosing sides and more about doing what is right for the country. Opinions may vary, but it shouldn't be a team sport.

You can support a party but still be critical of them.

Ring fencing tax losses + capital gains tax.

And now we hear that the govt may allow overseas investors to buy but only if they do not live in it. Why would they buy if on the other hand the govt were to introduce these policies which will reduce the future value of property?

I know its different parties saying these things but of the govt were to enact everything, then it is sending out a very confusing message.

MMP is really a joke. In the 2014 election there were 3 parties that made it in with less than 1/120th of the total votes (local or party vote). Act coat tailed in, Maori Party got the special vote and Peter Dunne Gerry-Mandered his way in.

Yet two other parties which would have secured multiple seats did not get in because of the 5% rule.

Every. Single. Party in parliament in the last few decades has either been one of the big two, or founded by ex-MPs of the big two.

It's no wonder we have so many vested interests in the beehive. Any outsiders are kept out under a fear driven rule originating from Germany.

Our system sucks almost as bad as the US. Every 3 years I have to vote for the "least bad" rather than who I actually want to vote for.

The two big parties hug so close to the center anyway, people are just voting for their favorite colour and trying to use the negatives of the opposition party's previous term as a justification for their vote.

Breaking it down though, if Labour were to fail to deliver on key areas such as KiwiBuild that would leave a Labour voter in exactly the same position as a National voter who voted for National based on John Key's campaigning. At worst.

Which means its a bit rich to see people who will excuse any failure from National and continue to do so after

nine years criticising Labour voters for taking a wait and see approach after 9 months.

Am I surprised by such hypocrisy? Not in the slight, teensy-weensy bit.

To your first point, can we all just admit labour and national are mostly just the same with a different colour. National got in on the back of a housing crisis under labour (100% price increase from memory), now labour are in on the back of national’s housing crisis. Two sides of the same coin.

If anything’s hypocritical I think it’s expecting either labour or national to change anything substantial. We will keep going round in circles until we lose our political dogma and look at the real causes of housing crises.

Agree they are very similar in that they are both very socialist but generally favour slightly different recipients.

However, by very nature National is conservative and this tends more toward inaction than action. Labour is more likely to take radical action - e.g. the 1980s economic liberalisation when Labour was more economically right-wing than National was.

I think we're hitting the point where we do need to take more radical approaches to things because cruising along has only made things worse, and we're hitting real crisis points. Thus, though I didn't vote for Labour I do hope they back themselves and get things done, as yet more years of inaction and pretending crises don't exist will not do NZ any good.

It will require democratic pressure, obviously. I'd advocate for positive pressure - pressure on them to get things done - rather than just more mews and squeals of indignation from the Collection of Whingers. (Though in the case of threats to their tax-free gravy train it may be understandable.)

What was written on the box when people voted Labour was transformational change versus National which said modified status quo.

If Labour do not live up to that message on housing then quite rightly there will be a huge amount of dissatisfaction.

Ipsos the polling company recently reported housing affordability is the issue that most concerns the public -for all income groups, both sexes and all ages except for the retired where health care pushed housing into second place.

For Jacinda, Phil and Grant their route to political success is quite clear -deliver on the public expectation that they transform the housing market.

Wow, revisionist much? Did Labour campaign on ‘Rogernomics’? I see it as an opportunity taken by Roger Douglas, not a Labour party policy platform per se. The voters as a whole, at least those in a comfortable position, don’t vote for change. That will continue for decades to come. COL supporters have been sold a pup. It’s amusing reading the justification from their supporters. The more things change the more they remain the same and the Golden rule continues to apply i.e. those with the Gold make the rules.

So your argument against Labour being more likely to take radical action than National is not arguing that they haven't got that track record, just that they didn't necessarily campaign on that radical action in one particular instance? They were campaigning against Muldoon's sit and do nothing but freeze things, obviously.

Neato. Gymnastics much?

Well put. I agree for change a more radical approach in relation to removing cumbersome regulation, removing tax advantages etc but not government trying to become builders. Got to fix the cause not the symptoms.

I take it your a top voter then ;)

I would pick a group of idle politicians over these current bunch of liars and hustlers any day.

Interest.co.nz should do a list of Labour's promises vs policies to clarify just the magnitude of 180s this government has done. They not only do something vastly different from promised but also provide false justification for it and short-change their voters for morons.

Agreed and seconded.

What has been disappointing ?

I’m in a similar boat, I voted National 3 times because I had a man crush on John Key with his gorgeous smile. This time around I voted Labour because they promised some real good things but I’m not impressed. If after 3 years there’s nothing to show for it then I’ll probably vote the New Zealand People’s Party or something.

You are the perfect voter then.

The way that article reads to me is that the legislatoin will stop developers ramping up the costs of a developement. But then I guess that's what you get when your economy is based on houses. Makes it seem a good idea to me.

@redcows , you need a lesson in economics ........... developers dont "ramp up the costs " , the costs are what they are

* Land prices in Auckland are influenced by supply constraints and coucnil rules and requirements and DC Levies and $20k for a water meter

** Materials prices are set by an oligopoly , effectively with Fletcher Group as the price maker and everyone else as the price makers

*** Rampant migration of over 2000 new faces every week is a major problem pushing up demand

**** Wage rates so out of control that someone with a paint brush is charged out at the same rate as a young GP earns in his first year as a Doctor .

Things are out of control , and Developers are simply not part of the causes .

Did you mean Fletcher as the price maker and everyone else as the "price takers"?

not sure what is wrong with the amended bill..

we cannot shut out foreign investment, I think this is a win win for both parties..

if we criticized the previous government for being polarizing, how can we expect the COL to be the same.. that was the whole point of consultation.. get feedback and work for the betterment for all..

Just enforce normal tax. It the property has had one cent of tax offset applied its a rental and it collects 33% on sale (or some sort of withholding tax for long term hold). If its part of a portfolio then all properties are effected.

and gst too.

That's capital gains tax, and in most countries it is normal.

Just enforce normal tax. It the property has had one cent of tax offset applied its a rental and it collects 33% on sale (or some sort of withholding tax for long term hold). If its part of a portfolio then all properties are effected.

Why calculate based on a 10% capital gains tax? That would put New Zealand in a similar situation to Australia where the CGT is discounted by 50%.

Should they not just be calculating it based on marginal tax rate? Even this calculation at 10% highlights how vulnerable the New Zealand housing market is.

He's an 'economist'. My experience in countries with capital gain taxes is people are inclined to hang on to houses longer and trade on same market if they do sell. Investors are extra sure to hang in there as long as the return is okay, unless you get them to revalue every year and pay the tax , treat capital gain as income, if it's only when they sell incentive is to become a long term landlord or set up a company and trade shares. Asset taxes are better.

The 1% land tax has same effect and simplier, why not?

Land tax is not as fair though. A capital gains tax is a tax on profit. It is unfair for some forms of profit not to be taxed when other forms of profit are. Why work a PAYE paying job when you can make capital gains from housing and pay zero tax? Who will pay for education and health and super if we are all just trading houses with each other and not paying tax?

The problem is a land banker will just sit on their land for decades or put it in a trust waiting for the next tax loophole.

Omitted in the above is the observation Dominc made on radio that the increase in rentier voter by number over the home owner was going to have an impact on govt policy (or words to that effect). Main stream accepting change is inevitable perhaps?

Yes and there was another point he made on radio that prices may just flatten out rather than actually fall. Having a punt both ways like having your cake and eating it, is appearing to give answers but just fence sitting

What is shocking to me is the overtaxing of savings. No wonder we are a poor country and falling further behind, what with our overpriced cold damp chicken shacks and all. Perhaps a halving of tax on income from savings would solve our long standing problem of flogging off the country to others.

The marginal effective tax rate on rentals seems about right to me, maybe 5% too high.

Westpac are simply wrong ............. there is nowhere on earth that a new or additional TAX has ever brought the price of something down .

Its oxymoronic to even suggest that house prices will fall on any sustained basis

The price of used houses in Auckland is simply a function of the replacement costs of building new houses and those costs are not about to miraculously come down anytime soon .

What may happen is some investors will exit the market because of the new tax but with almost 100,000 new non-Kiwis arriving here 365 days as migrants , those properties will simply be snapped up by new migrants ( Mostly from China )

Yip Boatman -lets keep it simple.

Remove taxes and impediments on building houses. That is the simple and easy way to bring down house prices. Because as you say Boatman -the price of used houses is simply a function of the replacement costs of building new houses.

I have a few hundred sentences expanding on this point on my website. But that is the gist.

https://medium.com/land-buildings-identity-and-values/why-tax-house-bui…

"The price of used houses in Auckland is simply a function of the replacement costs of building new houses" - what so land is free now? Care to give me some of yours?

I think that Boatman included land costs as part of total building costs for new houses -at least that was my assumption.

The price of existing housing is set by the price of new housing.

Much like the price of old cars is set by the price of new cars.....

It is quite simple....

Perhaps we should clear this up further as both of these explanations aren't entirely accurate.

The price of used 'houses' (or improvements) is a function of the cost of replacement (depreciated by some nominal amount) and the net of extensive and intensive land value (the effective cost of development).

The price of property (including intensive development) is a function of amenity value of land (intensive price), implicit taxation (cost of developing), and some depreciated replacement construction cost.

Old cars are a lot cheaper than new cars. Yet with housing the price of an old house is almost the same as the price of a new house. This is because the value is actually in the land and not so much the house. Its land values that need to come down. One of many small steps to achieving that is to decrease speculation by making the tax system fairer.

Fair enough -but it is a small step. The big steps are about removing the excessive costs in creating buildable spaces.

Agree. Maybe a tax on investors could offset the removal of tax and contributions from new dwellings?

Increasing taxation?

Why would you want to raise rents during a housing crisis?

That doesn't do anything to stimulate the capital that we need for development.

The simplest approach is to liberalise the planning restrictions - some work has been done with the AUP. As Brendon often points out, there is a substantial amount more that could be done, also.

Who says rents will rise? Isn't it more likely for house prices to drop and the rental yield after tax to stay the same? If people can afford to pay more in rent, why aren't landlords charging more now?

No.

Surely the rental market isn't purely inelastic - so rents will have to rise. A signal as perfect as a tax will ensure that at least some of the burden is realised in increased rents.

Rising rents mean increasing yield - upwards pressure on prices.

Rising rents means less savings - lower capital accumulation in the economy because it is being sucked up by non productive housing.

Less domestic capital accumulation means higher development costs.

Mmmm. Sort of.

We know that the intensive price of land in Auckland is relatively cheap.

The extensive price is huge, though - indicating that there is a huge amount of development cost capitalised into the land value.

Hence why I further refined the definitions supplied. Like you many people simply assume that land cost is representative only of the amenity value, relative to some scarcity constraints.

As Brendon says, the key is to mitigating this deadweight loss incurred through a lack of liberal building regulations. The cost of which is represented in what you assume as 'land' cost, and not only the explicit cost of construction.

Yes, the fact that we are free to choose whether to buy a Toyota, Audi or Porsche, Hatchback, Station Wagon, or SUV, makes cars accessible for almost everyone.

But the fact that a developer is required by the council to build a high spec mansion with lots of parking and a 50 year guarantee makes housing much less accessible.

The amenity costs are not constant either. Wrt intensification master planning a bigger site means more housing units can be accommodated with less loss of amenity value compared to what multiple individual plots doing their own thing could achieve -even if total size was same as the one big site.

This means master planned sites have more upzoning gains -which could be split between higher developer profits and more houses/ lower prices/better quality for buyers. As well some of those higher profits could be returned back to the original land owners to incentivise their agreement to the scheme. So a triple win scenario!

That is the basis for my Master Planned Block proposal .

https://medium.com/land-buildings-identity-and-values/can-great-design-…

Yes, loss of amenity value is decreasing in scale for (well designed) new developments.

Unfortunately it is the inverse for existing developments in the same area - they are facing marginal decrease in amenity value wrt intensification. That's the balance that must be struck and the core issue as to why we have such restrictive planning.

I agree entirely that if we put the right incentives in place, master planning is the way to go.

However...

The big issue we face is that although in theory we could construct master planned developments, there are too many private obstacles for a reasonable developer - obtaining a whole block of properties from individual land owners, huge uncertainty in construction inflation, planning process.

It is not unreasonable to expect that such a development could take 10 years to achieve given these constraints.

I wonder how long it is taking the likes of Ngai Tahu Property to build a residential block in Hobsonville. Is it really taking 10 years? It would certainly take a few years though.

Also my master planned blocks could be done on a smaller scale -say half block -0.5 hectares with 10 existing houses becoming maybe 50 residences. It could still be quite effective at a slightly smaller scale.

For the wider neighbourhood there are pluses and minuses amenity wise by having an inclusive mindset to welcoming more neighbours. More people means more commercial outlets, better public transport, more ratepayers to fund more public services. But also more difficulty parking, roads might be more congested -these could be addressed by congestion charging of road and parking spaces which could be spent improving local amenities though.....

The Ngai Tahu case is more unique, though, being greenfields.

I was talking about planned development areas in the likes of the upzoned Te Atatu areas.

Smaller scale, yes.

Again, though, 10 existing properties to purchase and amalgamate?

I just think that that sort of co-ordination is the exception. For instance, you must find clustered low intensity property to start with which is quite difficult.

Those owners must also be willing to sell at a reasonable price for the developed which is severely hindered by the huge lock in effect that over priced property maintains in a flat to falling market.

Honestly, I can't see it happening.

Greenfields, yes. But we can only provide so much clustered density with our current infrastructural constraints.

Nope. The price of houses is all about the availability of credit. Watch the prices drop as the credit squeeze tightens. All your other theories are just side shows arond the edges...

a credit crunch combined with an urgent need for liquidity by a large number of property owners likely results in lower prices (as the property market is relatively illiquid in a credit crunch scenario).

The banks are appearing very anxious at present. Westpac with a whinge today, ANZ yesterday on foreign buyers. How fragile their lending positions must be. If they had leant prudently on sensible income multiples perhaps there would be less requirement for lobbying government policy now. Nothing to worry about with NZ's banks?

Jenee . your teaser on the home page is misleading , one needs to read exactly what the economist said ............. it seems he holds the view that ringfencing of losses is more likely to cause prices to fall as over-geared investors exit , than a CGT would

"Treasury and the IRD estimate that currently property investors pay 29.4% of their after-inflation returns in tax" - really? How? Why?

If I bought a house 10 years ago for $500k and I sell it now for $1 mil, I've made $500k profit tax free. I must have paid almost $1 mil in tax from rent to have paid 29.4% in total!

Who comes up with this rubbish?

If IRD will tax landlords on the assumption that their return is 5% from rents - then bring it On !!

Rents will be adjusted accordingly upwards to prove them right .. afterall IRD cannot get it wrong , can they?

The right hand doesn't know what the left hand is doing in this CoLs and dreamers - So far, it sounds like a dog's breakfast to me !! Diluted Bills, contradicting messages to the outside, failed promises and have no clue what to do next, spending money inappropriately and Tax,Tax,Tax ...

Good luck for 2020

But currently lots of rental properties make a loss. Why would anyone invest in something that makes a loss? Or is it actually making a gain that is hidden as a loss?

Like Amazon, Xero and 101 other companies that don't make a profit in their early years?

It is quite a simple concept:

You buy a house which may be negatively geared, chip away at the mortgage (usually doing overtime on your day job, putting extra cash into it, not going out pissing up all your money every weekend) and over time also hope to get some rental increases. Over 5 or 10 years your negatively geared property becomes positively geared as you lower the mortgage costs and you start paying taxes on your profit.

The fact that in the past few years speculators have been able to buy, hold for a few months or a couple of years and flick on at huge profit does not make them property investors. All landlords/property investors I know are in it for the long haul

Craig

"Top rate of income tax reduced from 33% to 30%" - this will just put more money in rich peoples pockets - which will go where exactly? No way a tax decrease will drop house prices!

As Boatman says taxing anything more will never reduce a value of something!

Michael Cullen has had his day in the sun and it wasn’t that sunny.

A CGT will push house prices further away from first home buyers and will bring in very little extra tax.

It is mainly an Auckland problem so why don’t they limit it to Aucklandif it is such a Problem?

By that theory we should have some of the cheapest houses/rents in the world as we are one of the few countries that doesn't have a CGT.

Nonsense. That assumes very little of the price of housing is due to speculative demand based on an expectation of capital gains, or the nature of NZ housing as a good place to park and/or launder money.

IF those things are very large factors in the price of NZ housing then disincentivising them and making NZ houses all about homes instead would cause the price to fall.

For once I agree with you The Boy. Capital gains is certainly not a problem in Christchurch. If anything it is the opposite as values surely but steadily decrease down there along with rents. Well at least Labour is doing something which is far more already than National ever did.

Let's also remember these bank guys are not independent economists giving impartial advice. What they are paid to do is to advocate for policy settings that enable banks to sell more mortgages and make more profits. This might coincide with what's good for the wider society -i.e. by fixing the housing crisis. But it probably doesn't...

It's highly implausible that a 10% capital gains tax would lead to a 10.9% fall in aggregate house prices. For a start, the majority of residential dwellings are owner occupied and unaffected. Then, I don't believe the prospect of paying 10% on any gain would deter an investor (and of course any losses recorded can offset future gains). Lastly, if rents were to increase, this offsets some of the CGT anyway.

For FHB, CGT is a long awaited Xmas present!

Ha, different to what happened in Australia when they bought a CGT in. The lack of people wanting to sell put prices up.

If a CGT is such a panacea for property prices then why hasn’t it made a difference to prices in Australia, Canada, Sweden, UK?

How do you know it has not? ie without it prices could be even worse.

So no evidence from Westpac that their projections have come to reality in other countries who have implemented a similar tax?

Interesting article by Westpac but far too theoretical in my opinion. House prices are determined by many, many different factors, therefore the estimated impact from the various tax changes on house prices are really just an unverifiable guesstimate.

"Westpac estimates the introduction of a 10% capital gains tax would see house prices fall by 10.9%"

The 5 year bright-line test IS a capital gains tax that is already in place and currently taxed at 33% , so is the government proposi proposing to lower the tax on CGT from 33% to 10%?

I am not sure why people are complaining about house prices going down.

I you were too silly to do you calculations and thought that everyone will keep on paying top dollar for shacks... well I hope that you learnt your lesson, did not get burnt too badly and move on.

For investors (entry level and seasoned) an affordable loan makes far more sense, you can have your rent at a good price and still make money. When it comes to the crunch... your tenants can still afford the rent and you will not have to top up your mortgage on the property.

For FHB's and people only wanting one house in which they can retire... shouldn't it be fair that they can pay off the house and still have savings left over so that they are not a burden on society later on?

Everyone seem to want to win the lotto these days and they hope to do it in one stroke.

If your wish is taking away from someone else... it is time to take a long hard look at your values.

If landlords make a loss on their rental properties, then what are they in it for ?? If its not capital gains,surely they are not in it for charity ?

Economists (with the exception of Tony at BNZ) can really put out some weird stuff. "10% CGT would result in 10.9%drop in price"- WOW. These same economists were claiming high, in fact very high, interest rates were almost around the corner in 2010.

All that talk in 2010 sucked me in to a 4 year fixed at 6.8, then a 25k break fee charge we didn't take up hahaha. Scam alert! Did you also get caught out?

Nice in theory Dominick. But theories often fail to live up to the hype in the real world. Care to list all the countries where this taxation has successfully reduced house prices? All you are doing is encouraging the very inept and envious Cullen to come up with some really nasty taxes to 'screw the rich pricks'. Don't be the one to be responsible for that, your reputation will not survive it.

New Zealand successfully used land tax to break up large land banks and get land into the hands of average New Zealanders. The UK also used land tax (and estate tax) to do similar. Both played a big part in eventually increasing home ownership among the unwashed masses like yourself.

Not a lot of discussion on the 'Deemed rate of Income' version.

Another option may be say 4% on the gross capital value as this would encourage lower financing.

Dominick Stephens has made a pretty safe prediction in one sense. No one will ever know how much a CGT might have impacted prices. There are many variables in the mix and the affects of none can be isolated out and quantified.

Prices are determined by supply and demand. I feel Stephens has failed to convincingly show how a new CGT would impact either demand or supply. There seems to be a wide-spread acceptance among some that demand would be negatively impacted and so would negatively impact prices. I'm not convinced demand would be negatively impacted. There would not be any fewer persons needing houses and they would not need houses any less than they do now. Turnover could be negatively impacted since a tax payable on sale could be a reason to delay or avoid selling, however this would only affect a small part of the market since traders and those owning investment properties for less than 5 years are already required to pay tax on capital gains and owner occupiers will be exempt.

If a CGT will not negatively impact prices, then what could be the true reason for the CoL potentially introducing one? Could the answer be that it's just another opportunity to increae the tax base - naked perverse socialist ambition.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.