International credit ratings agency Fitch is predicting New Zealand will record nominal annual house price growth of 3% over the next two years.

Fitch says this in the New Zealand section of its Global Housing and Mortgage Outlook - 2019 report, which is authored by Fitch's Sydney-based director Chris Stankovski.

Below are Stankovski's comments on the NZ housing market in full. These come ahead of the release of the Real Estate Institute of New Zealand’s December residential sales data on Thursday morning.

The last REINZ monthly data showed November's national median house price was a record high $575,000, which was up 6.5% year-on-year. Excluding Auckland, the national median house price was $485,000, up 7.8% year-on-year. In contrast REINZ said Auckland’s median house price dropped 1.5% to $867,000 in the year to November.

Fitch estimates NZ recorded 2.5% house price growth in 2018.

Fitch expects lower home price growth in New Zealand driven by restrictions on loan-to-value ratios

Home Prices Cooling as Government Restrictions Temper Demand

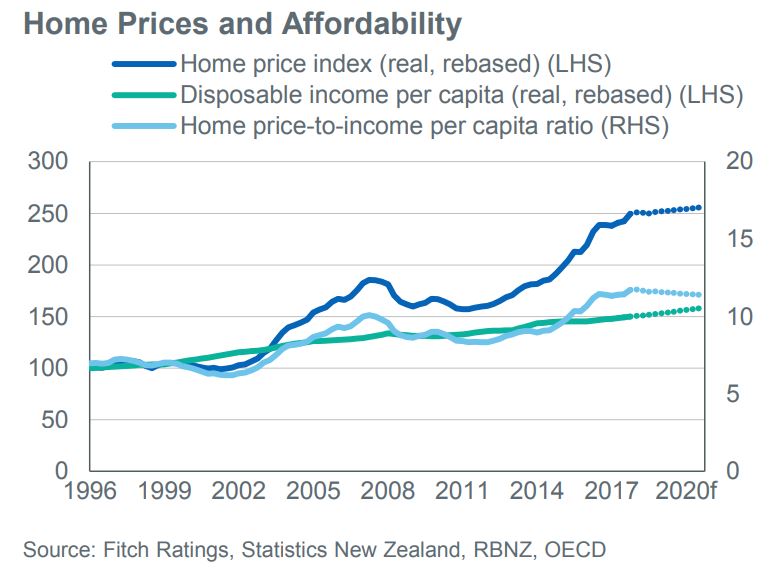

Fitch expects annual home price growth of 3% over the next two years down from 14% in 2016. Demand for housing in New Zealand is expected to weaken as credit lending restrictions will continue to keep the number of first-time buyers and investors low. Although New Zealand’s high household debt levels (at 93% of GDP as of 2Q18) place downward pressure on prices, supply remains constrained, which along with strong, above trend economic growth and stable mortgage rates, will keep home price growth positive.

In October 2018, the government banned non-residents from buying existing homes with the aim of improving affordability, although Australians and Singaporeans are exempt due to free-trade deals. Fitch believes this will have a limited impact on national prices as it is estimated that fewer than 3% of homes are sold to foreign buyers. However, we expect Auckland to be affected, as the percentage of sales to foreign buyers is about 20%. Fitch expects Auckland to continue to post lower growth than other regions in 2019 with price falls likely.

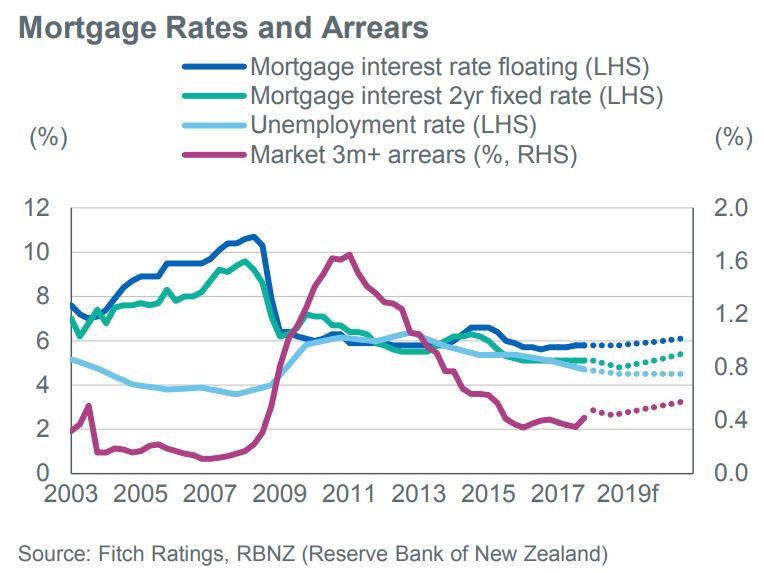

Benign Economy Supports Low Arrears

We expect mortgage performance to remain stable with 90+ days arrears of about 0.5% in 2019 reflecting Fitch’s forecast of stable employment and wage growth. Mortgage rates will remain at low levels with Fitch forecasting a 0.25% increase in 2019 and a further 0.25% increase in 2020.

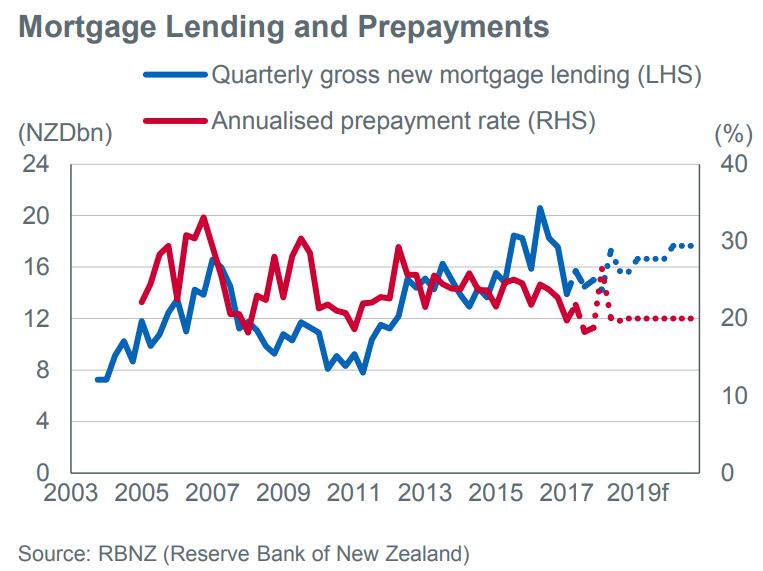

Stable Mortgage Lending Growth

Fitch expects mortgage credit growth to remain stable at 6% as the RBNZ is likely to continue to relax LTV restrictions that were introduced in 2013. From 1 January 2019, banks cannot underwrite more than 20% of new mortgage lending to owner occupied borrowers with LTVs of over 80% (with the former limits 15% in January 2018 and 10% in October 2016) nor can they disburse more than 5% of new loans to investors where LTVs are over 70% (increased from a limit of 65% in January 2018 and 60% in October 2016). The previous limits have resulted in the share of mortgages with an LTV greater than 80% falling by half in three years to less than 7% in September 2018.

22 Comments

Looks like they employed a lot of grey matter in extrapolating those graphs and coming to that conclusion.

It's what we have come to expect from these agencies.

Zero credibility.

Biggest take out for me there is that they believe home price to per capita income will flatline going forward. Kind of like the "post-GFC-QE-driven-global-asset-price-orgy-new-normal."

Right on. After the GFC they had all manner of excuses for why they missed it.

With price fall likely....

LIKELY.. .. In Auckland have already fallen by 10% to 15%,...Likely to fall further FURTHER... by how much will have to wait and see.

I’m in the market for my first property, do you mind letting me know where they’ve droppped 10-15% in Auckland? You must know all the secret fishing spots too? /s

In his dreams.

Well the cost of building or renovating is going ever higher but land value is sinking. So bargains will be oldish standalone houses on good sized sections. If they have not been renovated for decades then you might get a bargain. So long as you can live with a very old fashioned kitchen and a less than modern bathroom you might do well. I would avoid apartments until the builders begin to go bankrupt (in 2009 bought mine new at half price).

If there are more sellers than buyers there must be bargains. Don't be embarrassed making low offers. Good luck.

Check pakuranga, sunnyhills and nearound area where prperties which would have been in million plus are going near around 900 so are many other area.

Probably he means that some properties that sold for silly prices at the peak of the market in 2016 may have changed hands against then for perhaps 10%+ less. My guess is that these are probably the exception rather than the rule.

As far as you as a first home buyer goes, I used to monitor prices in Glenfield because it's where I grew up and where, until recently, my parents lived. Prices there peaked in 2016 and have come off just a tad since then, maybe 2 or 3%. In other words, in that particular suburb prices seem to have basically flat-lined.

Told to me that a Torbay house bought by Asians for $1.25m was sold to my acquaintance recently for $970k.

What road in Torbay ?

Dp

I'm interested to know what they said right before Sydney dropped 10%, because most analysts were forecasting a lot less of a drop or a gain, and they are based in Sydney.

As per the article - “So what specifically does the group expect from Australia’s housing market this year? In one word, stability.”

Why do so many “professionals” get it wrong? Vested interests? Wishful thinking? Too much emphasis on the wrong factors?

Guess it shows the benefit of being a heterodoxical thinker.

Its because they ignore the fact that a large part of the "demand" for housing is in fact just demand for Tax free capital gains. And when the capital gains dry up, that additional demand dry's up (and turns negative).

Also, vested interests. So much of the "professional" commentary we get around housing comes from Real Estate industry and the Banking industry. Both have a vested interest in rising prices.

What a surprise, they got it way wrong. So this Auckland forecast isn't worth a damn, either. Nobody has lost their job over getting things so wrong of course, such is the economics profession. They usually say everybody got it wrong (like not seeing the GFC coming). No, some did see it coming and did forecast the Sydney decline. These are the people we should be listening to.

The loss(?) of 3% foreign buyer interest takes no account of the inability of existing foreign owned property to be on-sold outside NZ to foreigners. Those owners are either stuck or have to market their property within the NZ system.

A current example (admittedly requiring OIO approval) is the German owned island near Nelson originally acquired for under $2m and now on market for $12m. As with many if not most of these earlier approved buyers , they failed to meet their obligations and as usual the OIO failed to follow up.

However what NZ resident is going to get conned into paying anywhere near the asking price?

What a shame. Oh well.

Hey Fitch you got any of those tripple A, double plus good rated bonds. My bitcoins got "hacked" yesterday and I'm thinking of trying something a little safer when the police find the floppy disk wallet with all my coins on it. I think I remember Goldboy sachs used to sell them about 10 years ago.

From the gospel of Tom Petty

Free fallin', now I'm free fallin'

Now I'm Free fallin', now I'm free fallin'

When it becomes so blindingly obvious we are in for a major housing correction, these industry spruikers have to start saying something - only so they don't look completely stupid by failing to call it.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.