Auckland house price expectations have turned negative for the first time in about 10 years according to ASB's latest Housing Confidence Survey.

The decline in sentiment of Aucklanders - to the extent that a net 12% of survey respondents now expect prices to decline over the next year - follows recent softening of prices in the region.

An important caveat though is that the latest ASB survey (for the three months to April) was in large part carried out prior to the Government's decision last month to torpedo any Capital Gains Tax.

Anecdotally the prospect of a CGT was weighing on house market sentiment.

To that end it will be interesting to see if subsequent surveys, and indeed house sales figures, show any positive reaction from the move to ditch any CGT.

ASB chief economist Nick Tuffley and senior economist Jane Turner said the results in the latest quarterly survey implied that "most respondents expected a capital gains tax on residential

investment property would have a fairly material impact on the housing market".

They said the net 12% of respondents expecting house prices to fall in Auckland, compared with a net 8% that expected higher house prices to rise just one quarter ago. "The results became increasingly pessimistic over the three-month survey period."

Tuffley and Turner said the weak result in Auckland was unsurprising, given the Auckland housing market "clearly softened over these months and with the media drawing much attention to weak Auckland housing statistics".

"Furthermore, since late last year many media commentators have drawn parallels between the Auckland and Australia’s housing markets, highlighting the sharp house price declines in Australia and implying declines can be expected in Auckland.

"Nonetheless, we are surprised by the extent of the weak results from the ASB survey. The Auckland housing market has softened, but the balance of indicators suggest the Auckland housing market is not (yet) in dire straits. The number of houses listed for sale in Auckland is only around historic average levels. Meanwhile, Auckland’s housing market is fundamentally undersupplied; a contrast to Sydney’s housing market."

Tuffley and Turner said the other surprise from the survey results was that the fall in house price expectations was broad-based across New Zealand.

"House price expectations in the North Island excluding Auckland moderated to a net 25% expecting an increase (down from a net 32% in the previous survey). Meanwhile, South Island house price expectations moderated to just net 18% expecting a house price increase, down from a net 29%. This is despite most regional housing markets (with a few exceptions) being very tight and recording strong house price growth during the months the survey was conducted."

For the country as a whole, a net 11% of survey respondents, down from 23% in the previous survey, expected house prices to rise in the next year.

Tuffley and Turner say they will be "keenly watching" the next quarter’s housing confidence survey to see how much (if any) of the fall in house price expectations is reversed following the Government's decision to ditch any CGT.

The latest survey found that respondents were "broadly balanced" on whether now is a good time to buy, with sentiment continuing to gradually improve from recent years when respondents perceived it to be a bad time to buy a house.

Housing confidence

Select chart tabs

92 Comments

Don't see the CGT decision making the slightest bit of difference.

Why?

Because people buy investments predominately on price expectations. Price expectation in Auckland is a slow decline hence the CGT decision is irrelevant. Why would you buy with the trend and expectation of a falling Auckland market ?

Also, most investors would have know that if there was a CGT introduced, it was proposed to be introduced in 2021 and only applied to purchases made after that time. so why hold back on buying now?

It wasn't as if the CGT was going to be potentially introduced this year, or retrospectively.

Still there might have been a *little* bit of psychological 'fear impact', and a minority of investors may not have been aware of the above.

CGT would’ve applied to the capital gain on all investment properties from April 2021, regardless of when the property was purchased. If you purchased an investment property in 2020 and sold it in 2027 you would pay CGT on any capital gain accrued from April 2021 to the sale date in 2027.

You are right, I misinterpreted.

So given that, I think the impact may be more significant than I thought.

But I don't think it would be major. The international evidence suggests CGTs have minimal impact on deterring investors.

Bullish investors would back themselves, even if SOME of their future gain was to be taxed.

The primary reason that someone would invest in Auckland is that they think prices are going to rise in the long run. Something like one in five sales go to investors - they aren't buying because they think they are going to make a loss. Don't you think that not having to pay a decent percentage of expected profit in tax will put upward pressure on prices? Crockers found that of all the issues facing residential property, CGT was the most significant factor for property investors.

https://www.crockers.co.nz/knowledge-hub/auckland-property-insight/2019…

https://www.crockers.co.nz/media/62938/graphs-web_significant-factors.p…

{kind=link}

Investment decisions are made by rational investors ~ at least in theory (there isn't an assumption built in about money laundering but I digress).

If price expectations in the short and medium term are for this asset class to fall then a rational investor pops his money in the bank, takes the interest and then buys when the market turns.

Hence the relevance of the imposition (or lack thereof) of a CGT is limited to circumstances where investors see an upward trajectory in an asset class. For now that isn't the case for Auckland property.

Crockers are a property management and real estate agency. Not really an independent body conducting a survey.

Smart investors take a long term view as opposed to trying to time the market. Investors are buying in Auckland primarily because of long-term price growth prospects. Investors are still buying in Auckland, and the absence of CGT will make property investment more appealing. Are you saying that everyone investing in Auckland is either a money launderer or irrational?

How is the survey biased/misleading? They simply asked investors which factor is most important to them. It is based on a questionnaire, not the opinion of someone that works at Crockers. Westpac's Chief Economist believes taking CGT off the table will stimulate house prices - I'm guessing he is also biased?

"Smart investors"

An oxymoron when talking about people who only 'invest' in residential real estate.

They are 100% concentrated in a single, low yielding asset class and reliant upon leverage.

Nothing smart about that.

Smarter than braving the traffic with the rest of the herd 10 times a week, exchanging your time for a wage and then paying full tax on that wage, wouldn't you say?

The smartness or dumbness of the leveraged investment is a function of the capital gain.

I haven't followed Westpacs economics teams forecasts but I would venture to suggest they did not call the 10 year NZ govt bond yields to trade with a 1.70 handle in Q2 2019.

What does this mean ? Not everything a banks economics team predicts is actually going to happen ;)

The same chief economist who said in late 2018 that the relaxation of LVR rules would see price rises in Auckland? He seems to be infallible and clearly has no vested interest in tempting people to take out more and more of those ever-so-profitable mortgages.

What comments are you referring to?

"We have been arguing since August that the housing market

is going to experience a temporary and modest pickup,

due to a sudden drop in fixed mortgage rates and the

RBNZ loosening its LVR mortgage lending restrictions. We

expected the pickup to be most apparent in Auckland, with

prices in that city anticipated to go from slowly falling to

slowly rising."

https://www.westpac.co.nz/assets/Business/Economic-Updates/2018/Bulleti…

obviously quite wrong.

Will likely be minimal. There is no change in CGT, it's the same as it was. Plus it seems more people are coming around to thinking there'll not be any capital gains for the next few years in the property market. This could be a reason the govt decided not to implement CGT, apart from Winston. The property market is just such a big part of the NZ economy (which is not a great thing). No CGT and lower rates could help the market not drop so dramatically, but seems unlikely to give it much in the way of capital gains right now.

Here's a conundrum for everyone.

In April there were 5800 REINZ sales recorded nationally.

RBNZ lending data suggests that there were 22,000 new loans for mortgages.

RBNZ data also suggests that 2300 'loans' were made to First Home buyers at an average of $419,000

First home buyer 'loans' represented 17% of the total new borrowing at just over 950 million NZ dollars but were only just a little over 10% of the total new loans.

If they took on 2300 loans and there were 5800 transactions then either.

a) First home buyers were able to buy 39.6% of all the property sold in April with about 17% of the total 'value' of new loans written at an average mortgage of $419,000, sounds unlikely to me, or

b) The RBNZ have no idea about how big the mortgages that people are taking really are and have misunderstood (like APRA in OZ) that the banks have been splitting mortgages into separate loans to overcome the 'loan' to value restrictions.

It's a conundrum that I don't understand..... what's the answer? a or b?

How about c) the RBNZ have deliberately turned a blind eye to maintain plausible deniability while hoping against hope that the credit injected into the market can offset enough of the exiting investors leaving the market to avoid a catastrophic collapse...?

"12% of respondents expecting house prices to fall in Auckland" *Raises hand as one of them*.

"The fall in house price expectations was broad-based across New Zealand." Not surprised, as the rest of the country will very likely follow Auckland down; later to rise, later to fall.

"Auckland’s housing market is fundamentally undersupplied; a contrast to Sydney’s housing market". I remain unconvinced of this, given the questionable data and the building boom going on, and with new places not rushing off the shelves at all. If there's such an undersupply, why the slowdown?

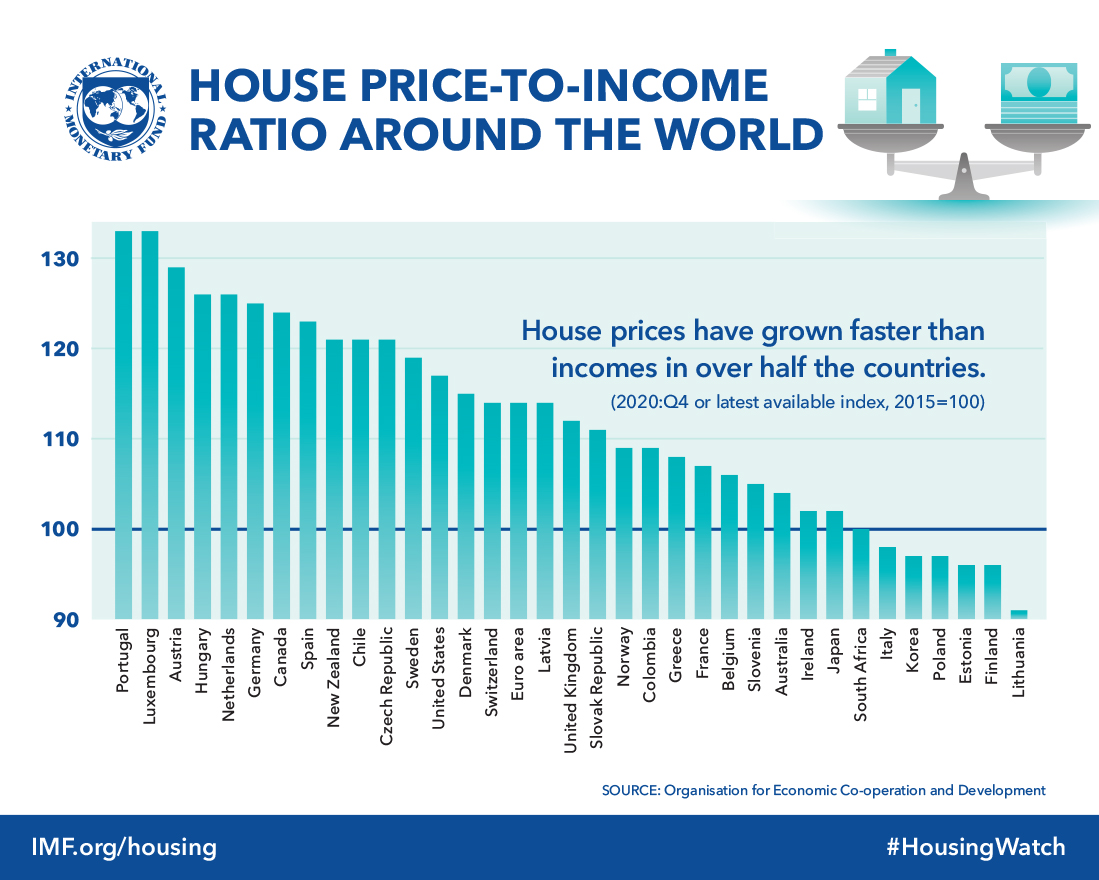

Also, let's remind ourselves once again that NZ price-to-income ratios are still VERY high. According to latest IMF Global House Price Index, NZ is now 3rd highest, ahead of Australia. Interestingly, Ireland is back in 2nd after their housing crash a a decade ago. Canada is highest, with signs of a downturn there as well. Anyone fancy buying a place in Italy, because that looks fairly reasonable, if you don't mind an economy on the brink. https://www.imf.org/external/research/housing/images/pricetoincome_lg.j…

{kind=link}

Under supplied at prices people are willing to pay.

"willing to pay"

You spelt borrow wrong.

or 'able to pay'

Totally with you on all these points.

I'm also unconvinced on the 'undersupply' issue. I'm not sure if the economists realise that many of the students who contribute significantly to our immigration numbers live in hostels or homestays, or in quite crowded flats. Which mitigates their influence on demand for new housing.

Hi Fritz,

Have a look at house prices in Auckland's inner-city suburbs.......

The reasons why Auckland inner-city house prices are relatively high is because there's a huge demand for them - but not too many listings. That means there's a shortage of houses there.

By the way, a net 12% of respondents to the survey expecting Auckland house prices to fall is a relatively small percentage. And remember that expectations-type surveys are notoriously volatile.......

Further, the "net 12%" figure says nothing about the magnitude of any house price fall. In fact, Auckland house prices may rise.

TTP

I was talking about the market as a whole in Auckland. Obviously different areas have different characteristics.

That was a net 12%, in otherwords 12% more than were expecting them to rise I guess.

All of these "Doom and Gloomers" in Auckland, ruining the capital gains, gravy train momentum... how dare they, with their common sense views...!

Yep guess most people have finally figured out just how much money laundering was going on in Auckland and have also figured that FTB's can not be expected to make up the difference to afford a home in our massively over inflated multi million dollar central suburbs.

According to our Justice system; Each year about $1.35 billion from the proceeds of fraud and illegal drugs is laundered through everyday New Zealand businesses and most of that would have going in to our property market. So yes property prices need to drop.

https://www.justice.govt.nz/justice-sector-policy/key-initiatives/aml-c…

A P-fueled property bubble has quite a hint of irony.

Are they taking the piss?

“Meanwhile, Auckland’s housing market is fundamentally undersupplied; a contrast to Sydney’s housing market."

They are confusing a market adjustment with population pressure. It’s only relative to price that Sydney is oversupplied.

It amuses me how many commentators point to Sydney’s over supply... but ignore the fact that Melbourne didn’t have the same levels of building (rents are rising) yet still underwent a similar sized correction.

Victoria has maintained a higher rate of building than NSW for most of the last decade.

https://www.abc.net.au/news/2019-01-09/building-approvals-plunge-novemb…

@Hardly: Have you been living under a rock? Auckland's prices are still falling but a bit more gradually than Sydney. Auckland was just a bit too late to the property binge building game (Mostly due to lack of space and NIMBY's). Where as Sydney thought that the overseas money tap could never be switched off. But oh dear, all of a sudden those big spenders in both markets disappeared in late 2017 and now prices are rolling back to more affordable levels for local wage earners and rational investors.

Suggest you do a bit of research, here's a recent article for you from Bloomberg: Chinese Buyers Helped Boost Australian Home Prices. Now They're Leaving. https://www.bloomberg.com/news/articles/2019-03-07/how-a-chinese-exodus…

Quote: "As real-estate agent Adam Wong works through Australia’s worst property downturn in decades, he’s also found himself at the mercy of China’s slowing economy".

"The Chinese didn’t just favor Australia. Investors embarked on a shopping spree that helped inflate asset prices around the world, snapping up everything from luxury condominiums in Canada to resorts in Hawaii and skyscrapers in London.

Things got tougher for Chinese buyers when Beijing imposed capital controls to help stabilize its currency, limiting the amount companies and individuals could move abroad".

'ASB chief economist Nick Tuffley and senior economist Jane Turner said the results in the latest quarterly survey implied that "most respondents expected a capital gains tax on residential

investment property would have a fairly material impact on the housing market".'

How the heck do they make that call, if there are no specific questions on the CGT in the survey.

That's simply a hunch at best, a total guess at worst.

Lousy

They 'know' this because their paychecks depend on it being true.

any while you're at it

A negative outlook by none other than Tony Alexander.......

https://www.landlords.co.nz/article/976514877/don-t-count-on-a-market-u…

Ouch.. the spruikers' spruiker is going bearish. That can't be a good sign.

ha ha, yeah.

Although he didn't say prices will DROP.

The moment he brings himself to say that (if ever?) we really know things are on the way down.

Prices will not DORP! We must HODL!

The notion of 'independent' bank economists has to be one of the most amusing notions around.

Tony Alexander is a doom and gloomer. Find someone less depressing who will say that property only ever goes up in price, despite evidence to the contrary.

Hi theglc.

I wonder if we’ll see class action suits by investors that were listening to Mr Alexander’s speeches in 2017 and remortgaged the family home to jump in... this one from the Tony Alexander archives is a ‘doozy’ - a masterclass in debt salesmanship! Published in July 2017.

Alexander then (in that vid - shot in 2016?): "I can’t see anything other than Auckland house prices continuing to rise at an unpredictable pace over the next few years"

Alexander now: “This cycle did its dash in Auckland two years ago and will, this coming year, peter out eventually in the regions.”

Is anyone surprised?

Should mean more cuts in the OCR and still lower interest rates to come : )

You property investors are glass half full types aren't you!

No quite, I'm glass fully full : )

"Meanwhile, Auckland’s housing market is fundamentally undersupplied; a contrast to Sydney’s housing market."

Remember that there are two levels of supply and demand

1) Level 1 - fundamental supply and demand

2) Level 2 - effective supply and demand

Market prices are determined by level 2, whilst many economists will talk about level 1.

In each property market there are two types of demand:

1) underlying housing demand

2) effective housing demand

1) Underlying housing demand

‘Underlying demand’ refers to the number of houses needed to accommodate households in the population. Population increase in the age range of 20–40 (which is when people tend to form independent households) leads to smaller household sizes and more single-person households. Further, positive net migration increases underlying demand for housing. A ‘household’ means either one person who usually lives alone, or two or more people who usually live together and share facilities in a private dwelling.

Natural population growth rates, internal migration, housing preferences and household formation rates all tend to change relatively slowly, and therefore changes in underlying demand caused by these factors are reasonably predictable. By contrast, the level of external migration depends on policy rules and incentives, as well as on wider domestic and international economic conditions, and it therefore tends to have a more volatile, less predictable impact on underlying housing demand

2) Effective housing demand

Effective housing demand is the combined effect of both 1) the desire to rent or buy a house, and 2) the financial ability to rent or buy a house. This aspect of demand is what shows up in the housing market statistics for sales, prices and construction. It also largely accounts for the changes in housing and tenure choices over time.

The New Zealand housing market has not only experienced increased underlying demand from population growth and higher net immigration; it has also (until the recent global financial crisis) experienced an increase in effective demand as a result of higher incomes, lower unemployment, cheaper and easier access to credit, and the preference of New Zealanders, for various reasons, to invest in housing over other forms of investment.

The difference between underlying and effective demand is a function of:

• buyer wealth and income

• the cost and availability of finance

• the state of the economy

• individual consumer preferences (for example, location, or between renting and owning)

• the attractiveness of housing as an investment good.

Source: https://www.mbie.govt.nz/publications-research/research/housing-and-prop...

Notice the variables that have impacted effective demand for housing that have not impacted fundamental demand that the economists have not accounted for:

1) the attractiveness of housing as an investment good - driven by property investor price expectations

2) the availability of finance - as driven by the stress test interest rates on bank loan applications, and lower LVR's since 2016

Very good , interesting read thanks.

Demand from buyers is falling, according to this criteria you give. Especially above 1.2m.

As you say, demand has many facets.

Unfortunately economists in housing market tend to only look at immigration and interest rates.

These are not the primary determinants of demand

Auckland median still $175k too high and must revert to mean.

Sales below 2013 and 2011 and will go lower as people was for them to do just that

Yep. It's all coming back to the fact that prices are simply too high.

They are too high for many potential FHBs (both in terms of deposit requirements, and repayments).

And they are too high for many investors, in terms of deposit requirements and yield.

The banks are being more cautious, and interest rates can't drop much more.

The Ponzi has simply run out of steam.

The only think that could restart it would be if mortgage rates dropped below 2.75% - unlikely.

Or another unlikely kick-starter - bigger hand outs from the government for FHBs (I wouldn't put it past them though. They are pretty daft. And with Kiwiflop they need to regain some political capital with fHBs). Is this a potential Budget bolter?

Although difficult to quantify effective demand has also fallen due to:

1) foreign buyer ban restrictions

2) anti money laundering rule implementation

3) property prices in Auckland have stopped increasing - this has reduced the amount of buying from property investors using equity release / deposit recycling financing techniques (i.e buy house, add value, get it revalued upwards, extract equity to max out LVR on higher asset valuation via borrowings, use these borrowings for equity deposit on next house purchase). It looks like this financing technique is still being used in other locations around New Zealand where property prices are rising and attracting property investors.

There are probably a few other contributing factors.

1. Capital controls in China have strengthened meaning its harder to get your cash out of the country and invest here even if you are a mainland resident in NZ.

2. The falls in the Aussie market will have had a wealth effect reducing the demand from Aussie investors. These folks aren't subject to the FBB.

3. National have imploded and domestically that gives us a higher chance of further more left leaning domestic policy in the coming four+ years

4. The global economy is slowing down and that means less tourist spending in our economy.

Given the affordability ratios as they are I can't see a single reason for prices to rise as the lower rates don't impact prices until they become a more reasonable multiple of domestic earnings.

How you can have a housing shortage and a fall in property prices at the same time.

The calculation of underlying demand is used for the purposes of long term town planning, and infrastructure needs (such as sewerage, parks, roads, schools, etc) due to an increasing population. Underlying demand is not useful for estimating future property market prices.

For example, the housing shortage number calculated for underlying demand would remain unchanged in the following 2 extreme situations, (assuming current household incomes, current population, current population growth & the number of residents per dwelling of 3.0).

1) if the current median house price in Auckland was $10,000. In this case there would likely be a huge increase in the number of active property buyers which would increase effective demand (and would be above underlying demand). People who were not owner occupiers would buy at this price. A large number of people who are already owner occupiers would also become active buyers and buy at this price - buy a house for their children, grandchildren, parents, holiday homes for out of towners, etc as they are cheap. People who could afford it from all over New Zealand and abroad (such as Australians and Singaporeans who are exempt from the foreign buying rules, and New Zealanders living overseas), are likely to become active buyers in the market. The underlying demand calculation does not incorporate this.

2) if the current median house price in Auckland was $10,000,000. In this case, there would likely be fewer active property buyers in the market. The number of effective demand would be fewer than that for underlying demand. The underlying demand as calculated above would remain unchanged - after all there is no change to population estimates or the assumption of the number of people living in each house. There would still be a "housing shortage" as calculated by economists using the population numbers, but in reality there would be few buyers active in the market if the median house price in Auckland was $10,000,000. Very few would have the deposit necessary to buy, and very few would meet the bank lending criteria particularly on debt servicing.

This is the reason why the underlying housing shortage is a misleading number (as calculated by economists, etc, and quoted by mainstream media, politicians, property market commentators, etc) as a justification for future house prices to continue rising. It is used as a convenient justification by those in the real estate industry to persuade those to enter the residential real estate market.

Economists in their calculations of the underlying housing shortage, and talking about future property market prices, have failed to incorporate the fact that:

1) as prices rise, effective demand falls

2) as prices fall, effective demand rises.

This is introductory economics and the basics of demand. Underlying demand is unchanged, yet effective demand changes. This is how there can be a housing shortage (due to underlying demand), yet property prices fall (due to an imbalance between effective supply and effective demand).

So when talking about a housing shortage, there are two numbers to understand for their own specific purposes:

1) Level one supply and demand - this is underlying supply and demand - this is the most commonly referred to and discussed by most property market commentators, media, politicians, etc. This is useful for long term town planning purposes for local councils to determine infrastructure needs.

2) Level two supply and demand - this is effective supply and demand - and this is the key determinant of property market prices - and this is how property markets can go from being a buyers market to a sellers market (and vice versa).

You need to factor in the supply side as non-constant. The underlying land supply in Auckland almost doubled from 2017 onward, because the long term planning changed dramatically.

Kept supply constant to illustrate the difference between underlying demand and effective demand, and how underlying demand can remain unchanged whilst effective demand can change.

There is also underlying supply of housing and effective supply of housing. The underlying land supply for housing has increased (due to rezoning, etc), but may not impact effective supply of housing. (E.g rezoned land is held by land speculators to be sold to developers, but developers are not buying land due to financing issues, so there are no new houses built)

The highest rate of Auckland building consents in the current cycle has occurred 2 years after the market price peak. There are lots more houses being built, because the cost of land has fallen developers are more able to finance construction.

So underlying supply of houses is increasing.

The effective supply of houses / residential dwellings listed for sale in Auckland as at April 2019 is at the highest level in 9 years when looking at the effective supply levels for the month of April in prior years.

"How you can have a housing shortage and a fall in property prices at the same time". Simple. Availability of credit.

Your MBIE link appears to be broken?

link to PDF report - https://www.mbie.govt.nz/dmsdocument/1087-nz-housing-report-2009-2010-s…

Read Chapter 2: Demand

2.2: Underlying demand

2.3: Effective demand

Thanks

Usual repeated mistake: "market is under-supplied"

ACCORDING to what demand assessment and what is criteria for it?

Market , where extensive building has been done in past 6 years, is NOT over-supplied but in glut.

ie in Rodney, Silverdale and Orewa especially, also Hobsonville.

Property sold over 1m in Auckland 2016-19: down 22%

In Orewa, Red Beach, Silverdale? Up 29%.

People really should stop generalising on the "market" and stick to specifics.

Buyers now have a deflationary mindset.

Oh and that classic about most markers are not bad????

Sales at 2007-08 levels when stock up and demand supposedly steaming??

It is so obvious: over-priced, wrong place, too small, less land

Plus median disposable income in Auckland down on a decade ago.

Er: AML and overseas buyer ban? Little bit more influential than putative CGT.

Bank forecasts and paper written on.....

Albany Ward sales last 4m, cf 2018? Down 42% above 1.2m bracket.

Other bands down to $800k: down 15-18%

Under 650k? Down 33%

No a buyers market: buyers aint buying, esp at top end.

What was that Herald article in 2015 saying 50% of $1m plus houses bought by people with foreign names?

Remarkable then, is it not, that sales in the bracket should, just coincidentally, collapse directly after AML and OBB?

Please follow me on LinkedIn for more non-usual perspective from a person doing real estate in the real market...

In 1998 we had a population of 3,815,000 and 1,440,000 private dwellings according to Stats NZ (377 dwellings per 1000 people)

In 2018 we had a population of 4,758,000 and 1,885,000 private dwellings according to Stats NZ (396 dwellings per 1000 people)

Somebody must be hoarding the houses? If we were to apply a 377 dwellings to 1000 people ratio to today's population, then there's a surplus of 85,000 private dwellings.

More than 33,000 Auckland dwellings officially classified empty

https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11…

Yes that's why we need the results of our 2018 census, to show how many empty home there are out there. I'm pretty sure it will be a lot more that 33,000 empty homes for Auckland which was taken for the 2013 census not even at the height of the Overseas Investor spending spree that went on until late 2017. Wouldn't be surprised if it was at least 50,000+ empty homes now.

Trouble is, is when you do the census, Air BnB houses will not be counted as empty if they are occupied on the night of it.

Nah not practical, too much to organize and maintain. Remember these are Speculative Non-resident Investors so they would have bought wanting to keep the property in pristine condition to be sold to the next greater fool for more profit.

Yep, in Hong Kong and Singapore it's the same ~ mainland buyers don't tend to rent out their vacant property. If you look at the newer blocks in the CBD its certainly the case that the majority of units are not occupied.

Two words - Air BnB

Do you have some numbers on Air BnB? I found the following which suggests there were 19,000 Air BnB listings in New Zealand 2017 & 988,960 guest nights, that's an average of 2709 per day. Even if we divided the total number of guest nights by 3 months (peak season), and for illustrative purposes assumed each property only received one guest night then that would mean there are 11,000 Air BnB properties.

http://www.infometrics.co.nz/390000-airbnb-guest-nights-auckland-180000…

Yes I would agree with you. Even looking at the Auckland waterfront CBD area and other expensive places such as Remuera on Airbnb there's not that many being rented out in those parts that are apartments. Plus it's a lot to organize when you're in another country maintaining rooms for guests etc..

It's exhausting even if you have a fully managed service with a Rental Agency looking after your property and your in another country. I should know I've been a Landlord with an overseas property. So I can fully understand why a speculative Non-resident Investor would just want to keep there apartment in pristine condition by not renting it out.

"House price expectations in the North Island excluding Auckland moderated to a net 25% expecting an increase (down from a net 32% in the previous survey). Meanwhile, South Island house price expectations moderated to just net 18%"

.... the regions keep trucking on ....

As Spruiker in Chief TA said, the regions will soon follow Auckland down....

I would be worried .... if you weren't so utterly wrong. TA did not say that prices in the regions will be down hahaha

The regions didn't get the memo, still flying down in Tauranga with asking and selling prices all above RV. I guess its going to take another 6 months for the flow on effect to bite. Still plenty of people trying to sell in Auckland and move down there.

Clearance rates for auctions are still below 25% in Tauranga. They have been for a while. Listings are down from 1366 houses at the beginning of April to 1219 end of May. Many more high end houses for sale at the moment than in the previous months and before christmas. With a high number of premium properties selling in a low sales volume period, it tends to distort what's really happening. The selling cycle of *auction - price by neg - sale price - sale price reduced* is in full swing as people try to offload less desirable properties while real estate agents cling to the final month or two that they're able to tell people "everything is fine" before the data matches reality. Expect mass job losses for BoP agents in the coming months, the sales numbers are falling and they'll have to go back to working for a living.

Real fall is about to come.

Till now market has had a soft landing before...........................

Housing market just does not crash overnight, it take a while and now the next fall will be meaningfull as will will fall even at lower end of housing market and that is when the party begins for the FHB.

Wait and watch.

Yes totally agree with you. I think the biggest falls will hit the higher priced end of the market though, that has been slow to shift due to a lot of it being owned by 'Trust Funds and Shell companies" not sure how pressured they might to sell up, or clean their money? Make of it what you will.

Take a look at www.oneroof.co.nz Suburb info and scroll down, that gives an indication of who owns what.

Example: https://www.oneroof.co.nz/suburb/remuera-auckland-city-1962

Sadly the link doesn't seem to work. Very interested to look at that data though, most interesting.

@ Glitzy: Ahh probably to do with local search history and why it's not connecting for you. You could try going on the main site https://www.oneroof.co.nz/suburb and then search on an expensive area of Auckland in the Suburb tab such as Epsom or Remuera, scroll down and you'll see the who owns what within that area, It's quite an eye opener.

Another interesting one to look at is the barfoots auctions, a day or two before they go up for auction the Particulars and Conditions are posted, and you can see who the seller is. Eg, of the 5 properties listed at tomorrows barfoots 1.30pm city auctions, only one property is held in a trust. You could also take a (very rough) guess as to the ethnicity of the seller by their names.

Auckland has an under supply of housing, but an over supply of land on which to build housing. And we have prices that reflect our pre-2017 under supply of land.

This is an interesting market dynamic.

On the contrary, there's more building consents issues than almost ever and huge developments are happening all around the country many of them being unsold due to unrealistic expectations. There's no under-supply but over-supply of overpriced housing.

I do wonder who's going to buy all these townhouses in far flung locations like Milldale, at 'affordable' price points (of 800K plus).

Seems like a bust waiting to happen:

https://www.trademe.co.nz/property/new-homes/house-land/auction-2164818…

Or we go south, and we see small sections selling for 450. Even if you are building a compact, more affordable dwelling, you are walking away for nearly 800K.

https://www.trademe.co.nz/property/residential/sections-for-sale/auctio…

$1400/m2 in Drury for bare residential land. Crazy.

But less crazy than last year or the year before that.

Wow, the study believes that thinking that prices will drop is "pessimistic". There's nothing that would mean better news for a huge percentage of NZ's population, that shows how biased this study is.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.