By Simon Jensen*

There has been much written in the past few weeks about the unintended (or perhaps ignored) consequences of changes to New Zealand's responsible lending rules under the Credit Contracts Legislative Amendment Act 2019. However, the problems which have emerged with the implementation of the new responsible lending rules raise wider issues about how financial regulation is developed and implemented in New Zealand.

The bigger questions are:

- how did we get this so badly wrong;

- what else have we got wrong; and

- how do we stop it from happening again?

As with many failures, a confluence of factors were in play. This article looks at three key issues in the legislative process of: problem identification and preference for a particular “command and control” solution, the select committee process which didn’t provide the checks and balances it should have, and a concerning trend to delegate too much of what is properly a legislative function to regulation and to regulators.

Poor problem definition and alternatives evaluation

The issues with the responsible lending rules start with the combination of a weak problem identification and a desire to solve problems by imposing prescriptive compliance requirements that focus on prohibiting conduct and ultimately substituting the judgment of regulators for the judgment of lenders.

In this case, the aim of protecting vulnerable borrowers from predatory lending would have been better achieved by:

- allocating resources towards supporting the people at risk, perhaps by providing more financial assistance to budgeting agencies and social lenders like the Salvation Army, and

- focussing on enforcement of misconduct in the car lending industry which had been identified as a significant part of the problem and on whether additional resources or enforcement tools were needed to do this.

Instead, broad-brushed and overly prescriptive regulation was adopted. This has negatively impacted thousands of New Zealanders wanting to borrow from mainstream lenders. It is hard to believe that the main problem was ever with mainstream lenders, who were operating with very low levels of bad debts at the time and largely addressed any conduct issues that could have led to irresponsible lending. Mainstream lenders simply have no incentive to lend to people who can’t pay them back.

Select committee effectiveness

These problems also raise the question of whether the select committee process is really fulfilling its function of enabling genuine, as opposed to token, consultation. Numerous written and oral submissions were made to the Finance and Expenditure Select Committee warning it about the potential overreach of the responsible lending changes and its consequences for people seeking loans from mainstream lenders.

My understanding is that one select committee member has subsequently stated that they thought the proposed changes to the responsible lending rules only applied to "loan sharks" and not to banks – notwithstanding the written and oral submissions made to the select committee by the New Zealand Bankers' Association and at least two banks.

Financial services regulation is complex and while it can have significant impacts on society, it is often not politically interesting. This poses significant challenges in getting it right and getting politicians to care. That was perhaps best illustrated a number of years ago with the select committee considering changes to New Zealand laws relating to swaps and other derivatives. A committee member offered to bake a cake for any select committee member who had actually read the Bill. My recollection was that the member did bake that cake – which was at least some reassurance for those who had taken the time to submit on it.

In my experience, select committees often receive very good submissions on financial services regulation, not just from interested industry bodies and affected parties, but also often from professional firms and academics who are making submissions out a sense of public duty. In many cases these people have significantly more experience and expertise than officials producing the legislation. In general, they can get a good hearing from at least some of the select committee members who are prepared to take the time to understand the subject matter. However, far too often these submissions seem to be ignored or significantly discounted by the time the Bill is presented for a second reading, even when they have been well received by select committee members at the time.

This is often because the same officials that draft the legislation go on to advise the select committee at the end of the hearings and then report back to the select committee on how it should treat the submissions received. The attitude of officials on these occasions often reflects a confirmation bias that looks for reasons to reject changes suggested in submissions as opposed to a more open-minded approach of "why shouldn't we make the changes suggested in submissions."

Officials preparing the report back is then an exercise which is tantamount to them marking their own homework and, I believe, is where the process often falls down. The issue of enabling more meaningful consultation at select committee could potentially be fixed if independent experts were retained and reported back to the select committee. This could certainly fix the more egregious examples, such as where reasons given for rejecting submissions are factually wrong – but then dismissed by officials when this is pointed out as not mattering anyway, because the select committee had "already made up its mind."

In addition, I suspect that very few stakeholders ever read the report back to select committee post-submissions. As a consequence, there seems very little accountability for officials in relation to the contents of that report. In the present case, the report back on the Credit Contracts Legislative Amendment Act was 242 pages long (so unlikely to be read by select committee members, at least in full) and while it identified concerns in submissions about excessively conservative lending practices and excessive verification of income and expenses in the summary of key themes, neither of these were directly addressed by the report. To the extent verification was, lenders concerns were simply dismissed as "overstated" – with no explanation for that conclusion.

Without a mechanism whereby those submitting to the select committee can feel not just heard but genuinely listened to, we run the risk of losing the opportunity for valuable input. New Zealand as a small country has a much smaller pool of people with the expertise to contribute to financial regulation than say Australia. If we do not have a process to genuinely consult with them, we run the risk that they give up and the quality of financial regulation suffers.

The delegation issue

Compounding the problems arising because key submissions were never properly considered in the report back to the select committee was the fact that so much of the substance of the responsible lending obligations were imposed by regulations created under the Act and through the Responsible Lending Code. The Responsible Lending Code was not even a statutory instrument because it was technically not legally binding and so did not even need to go through the cabinet process. However, in practice it would be a brave lender that consciously did not comply with the Responsible Lending Code and Commerce Commission guidance.

This reflects what for me has been a worrying trend in financial regulation – namely that an increasing number of decisions that are rightly policy decisions that should be reflected in primary law end up being delegated to officials and regulators. This is even though the governments Legislative Guidelines say "in general, matters of significant policy and principle should be included in an Act". In the words of one politician "this is where officials get their revenge and put all the stuff taken out during the committee stage [back in]".

The fact that the annual budgets of our key financial regulators have all significantly increased over the last few years could perhaps be an indicator that more and more of what should be parliamentary functions are being pushed down to officials and regulators and more and more resources are being given to them to do it.

This has led to a tsunami of financial regulation in the past two years which shows no sign of abating [see table attached – noting this was during a pandemic with a six month hiatus]:

In fact, the situation has reached a point where the chief executive of one smaller financial institution told me recently that he receives twice as many emails from regulators as he does from customers. If this is not an indication that things have got out of control, I don’t know what is.

The Council of Financial Regulators who are supposed to be co-ordinating financial regulation in New Zealand could perhaps take a leaf out of Marie Kondo's book and ask themselves each time something is being introduced:

- What can be thrown out to make way for it?

- Does this really give me joy? But really – is it really needed to further New Zealand's 10-year strategic vision for the financial sector – something we do not seem to have unlike, say, the Australians.

Regulators will assure you that they will regulate only to the extent necessary. However, that inevitably creeps and never seems to reduce. Regulatory creep is a well-known phenomenon, a phenomenon which certainly seems to be in ascendancy in New Zealand at the moment. This is perhaps a reaction to a period of under regulation – but has ended up as a significant overcorrection.

Furthermore, consultation with regulators and officials is often even more challenging than doing it though the political process. While the legal test requires officials to "keep an open mind and be ready to change and even start afresh" in practice there is often a significant confirmation bias with officials and regulators and therefore reluctance to change anything unless demonstrably necessary (eg a clear error), much less start again.

In the case of the changes to responsible lending guidelines, the most significant issues were in the Responsible Lending Code which had been delegated to MBIE and the Commerce Commission guidance. That was where all of the prescriptive detail on what verification needed to be done and how lenders should assess whether the loan was affordable (notwithstanding that most mainstream lenders had been doing that successfully for their entire history). Given the consumer protection mandate of the Commerce Commission, it was always going to take a conservative approach to the interpretation of the law in its guidelines and education programmes. It is little wonder we are where we are.

The problem of delegating significant powers to regulators is far from unique to this case. It also seems to be the approach being taken with the current exposure draft of the Deposit Takers Bill – where, in an unusual step, the regulator seems to have been given the pen to write a draft law that establishes its own regulatory powers – effectively doing its own delegation from parliament.

We should be asking ourselves whether too many political decisions are now being delegated to regulators – and whether by doing so we are enabling ministers to increasingly rely on the infamous "plausible deniability" excuse to avoid responsibility for decisions and the unintended or ignored consequences of them. There are potential solutions to facilitate more genuine consultation with regulators at least.

For example, the Commerce Commission and FMA have boards made up of respected professionals drawn from the market who understand regulation and could potentially set up sub- committees to act as an appeal body. This could be a relatively simple solution although likely to require some culture change for the board members who would need to be more independent of management/officials than is normal. They would also need access to independent advice and support in reviewing the decisions of the regulators they supervise.

However, this is not the case with the Reserve Bank where the government expressly rejected submissions to follow a model closer to Australia and the UK and have a separate board responsible for prudential regulation (in much the same way we have for monetary policy). It does not seem likely under the current setting that we will end up with a board well positioned to independently oversee prudential regulation – in which case there seems to be a good case for an Administrative Review Tribunal similar to that which exists in Australia to review decisions from the Reserve Bank on their merits.

While there are technically other mechanisms to hold officials to account, such as judicial review, the Regulation Review Committee and the auditor general, these are all nuclear options that have very high thresholds before they can be exercised, tend to be limited to reviewing process not substance and, in the case of judicial review, is very expensive. Even in circumstances where they can be used, the attitude of regulated financial institutions is often – understandably – even if there is a clear case where officials/regulators have got it wrong, and they have advice a judicial review it is likely to succeed, "the regulators will just end up getting them back in the end so it is not worth it". We therefore need some practical solutions well short of more confrontational legal options.

The blame game

Finally, it is disappointing given concerns that have been expressed about the new responsible lending rules that an opportunity has not been taken to do a more comprehensive review of what went wrong.

Instead based on public statements, the Minister seems to have decided that the problem is the way in which the banks have interpreted the law. The Minister has also then referred the matter to the Council of Financial Regulators, a council made up entirely of government agencies, with no independent member, to review. The lead agency for that review is the Ministry of Business, Innovation & Employment – the very agency responsible for the development and implementation of the regime in the first place.

That seems destined for a finding of "not our fault – the banks got it wrong".

That, of course, is very unlikely to be the real answer. It would be a shame if we cannot learn from this example to make meaningful and positive change to the way in which we approach financial regulation in New Zealand.

TABLE

Financial Regulation 1 January 2020 to 9 December 2021

Acts

Financial Sector (Climate-related Disclosures and Other Matters) Amendment Act 2021

Counter-Terrorism Legislation Act 2021

Reserve Bank of New Zealand Act 2021

Financial Market Infrastructures Act 2021

Infrastructure Funding and Financing Act 2020

Secondary legislation/Legislative instruments

Financial Markets Conduct (Recognised Exchanges) Exemption Notice 2021 SL 2021/360

Financial Markets Conduct (Incidental Offers) Exemption Notice 2021 SL 2021/359

Financial Markets Conduct (Property Schemes—Custody of Assets) Exemption Notice 2021 SL 2021/349

Takeovers Code (Voting Agreements for Schemes of Arrangement) Exemption Amendment Notice 2021 SL 2021/348

Financial Markets Conduct (Forestry Schemes) Exemption Notice 2021 SL 2021/347

Financial Markets Conduct (Small Co-operatives) Exemption Notice 2021 SL 2021/343

Financial Markets Conduct (Overseas Registered Banks and Licensed Insurers) Exemption Notice 2021 LI 2021/324

Financial Markets Conduct (Overseas FMC Reporting Entities) Exemption Notice 2021 LI 2021/323

Financial Markets Conduct (Equine Bloodstock) Exemption Notice 2021 LI 2021/319

Tax Administration (Extension of Due Dates) Order 2021 LI 2021/318

Financial Markets Conduct (Overseas Banks Offering Simple Debt Products) Exemption Notice 2021 LI 2021/312

Financial Reporting (Inflation Adjustments) Regulations 2021 LI 2021/307

KiwiSaver (Reallocation and Transfer of Default Members) Regulations 2021 LI 2021/283

Financial Service Providers (End of Transitional Period) Order 2021 LI 2021/282

Credit Contracts and Consumer Finance Amendment Regulations 2020 Amendment Regulations 2021 LI 2021/281

Credit Contracts Legislation Amendment Act Commencement Amendment Order 2021 LI 2021/258

Insolvency (Maximum Priority Amount) Order 2021 LI 2021/257

Companies (Maximum Priority Amount) Order 2021 LI 2021/256

Financial Markets Conduct (Communal Facilities in Real Property Developments) Exemption Notice 2021 LI 2021/224

Financial Markets Conduct (Overseas Subsidiary Balance Date Alignment) Exemption Notice 2021 LI 2021/205

Takeovers Code (Catalist Public Market Issuers) Exemption Notice 2021 LI 2021/160

Financial Markets Conduct (Employee Share Purchase Schemes) Exemption Notice 2021 LI 2021/150

Financial Markets Conduct (Catalist Public Market) Exemption Notice 2021 LI 2021/149

Anti-Money Laundering and Countering Financing of Terrorism (Exemptions) Amendment Regulations 2021 LI 2021/146

Anti-Money Laundering and Countering Financing of Terrorism (Definitions) Amendment Regulations 2021 LI 2021/145

Financial Markets Conduct (Approval of Catalist Electronic Transfer System) Order 2021 LI 2021/113

Financial Markets Conduct (Catalist Public Market) Regulations 2021 LI 2021/112

Financial Service Providers (Registration) Amendment Regulations 2021 LI 2021/89

Credit Contracts and Consumer Finance (Certification) Amendment Regulations 2021 LI 2021/88

Financial Markets Conduct (US Futures Commission Merchants) Exemption Notice 2021 LI 2021/47

Anti-Money Laundering and Countering Financing of Terrorism (Class Exemptions) Amendment Notice 2021 LI 2021/38

Reserve Bank of New Zealand (Designated Settlement System—NZCDC) Amendment Order 2021 LI 2021/34

Financial Markets Conduct (Shares in Investment Companies) Designation Amendment Notice 2020 LI 2020/334

Financial Markets Conduct (Overseas Banks Offering Simple Debt Products) Exemption Amendment Notice 2020 LI 2020/333

Financial Markets Conduct (Overseas Providers of Custodial Services—Assurance Engagement) Exemption Notice 2020 LI 2020/326

Financial Markets Conduct (Australian Licensees) Exemption Notice 2020 LI 2020/325

Financial Markets Conduct (Fees) Amendment Regulations 2020 LI 2020/320

Financial Markets Conduct (Licensing of Administrators of Financial Benchmarks) Amendment Regulations 2020 LI 2020/319

Financial Markets Authority (Levies) Amendment Regulations (No 2) 2020 LI 2020/318

Financial Service Providers (Exemptions) Amendment Regulations 2020 LI 2020/317

Financial Service Providers (Registration) Regulations 2020 LI 2020/316

Financial Markets Conduct Amendment Regulations 2020 LI 2020/315

Financial Markets (Derivatives Margin and Benchmarking) Reform Amendment Act Commencement Order 2020 LI 2020/314

Electronic Identity Verification Amendment Regulations 2020 LI 2020/313

Anti-Money Laundering and Countering Financing of Terrorism (Definitions) Amendment Regulations 2020 LI 2020/311

Non-bank Deposit Takers (Declared-out Entities) Amendment Regulations 2020 LI 2020/303

Financial Markets Conduct (Recognised Exchanges) Exemption Amendment Notice 2020 LI 2020/274

Reserve Bank of New Zealand (Designated Settlement System—ASXCF) Order 2020 LI 2020/207

Credit Contracts and Consumer Finance Amendment Regulations 2020 LI 2020/205

Credit Contracts Legislation Amendment Act Commencement Order 2020 LI 2020/204

Financial Markets Conduct (Regulated Financial Advice Disclosure) Amendment Regulations 2020 LI 2020/132

Anti-Money Laundering and Countering Financing of Terrorism (Exemptions) Amendment Regulations 2020 LI 2020/91

Credit Contracts and Consumer Finance (Exemptions for COVID-19) Amendment Regulations (No 2) 2020 LI 2020/83

Financial Markets Conduct (Financial Reporting—DIMS Licensees) Exemption Notice 2020 LI 2020/81

Financial Markets Conduct (Overseas Registered Banks and Licensed Insurers) Exemption Notice 2020 LI 2020/80

Financial Markets Conduct (Financial Reporting and Other Relief—COVID-19) Exemption Notice 2020 LI 2020/71

Credit Contracts and Consumer Finance (Exemptions for COVID-19) Amendment Regulations 2020 LI 2020/55

Financial Markets Conduct (Restricted Schemes—Custodian Assurance Engagement) Exemption Notice 2020 LI 2020/45

Bills (with current status)

Financial Markets (Conduct of Institutions) Amendment Bill 2019 No 203-2 (second reading to be completed (was interrupted 10 June 2021))

Commerce Amendment Bill 2021 No 9-1

Financial Professional Services Trading Advice Transparency Bill 2021 No 88-1 (a Member's Bill, drawn from the ballot and introduced 21 October 2021)

Retail Payment System Bill 2021 No 80-1 (Introduced 11 October 2021. Submissions closed 25 November, with the Select committee report due 3 March 2022)

Companies (Directors Duties) Amendment Bill (a Member's Bill, drawn from the ballot and introduced 23 September 2021)

Incorporated Societies Bill 2021 (Second reading 17 November 2021. Awaiting Committee of the House stage)

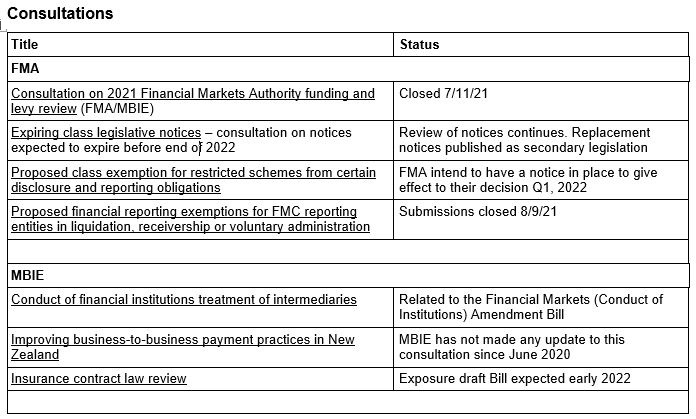

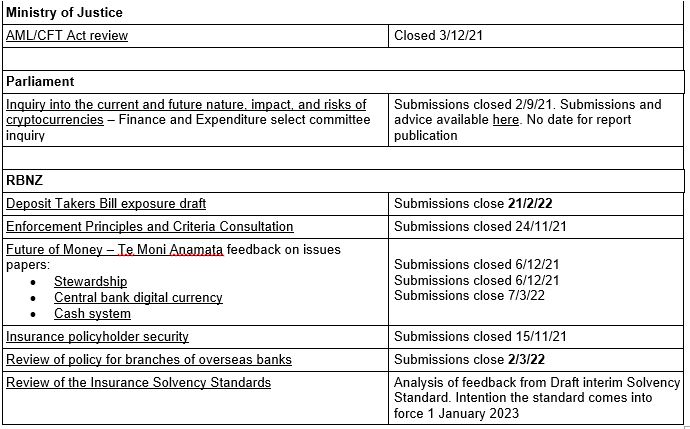

Consultations

*Simon Jensen is a consultant at law firm Buddle Findlay. However, this article is written in a personal capacity. The views in the article do not represent those of the firm he consults to, or of any clients he acts for.

27 Comments

I am not an expert but have lived in democracy for all my life. I do believe last few years has been full dictatorship of bureaucracy with support of politicians.

The only reason for that is the people have lost interest to actively participate in the process and politicians are just not intelligent enough to understand what bureaucrats are getting done.

Total legal failure of democracy.

Since when did your local MP represented you in the parliament?

One has to be blind not to see a minority population being over represented in the parliament while a substantial population has almost none.

That to me is not a democracy.

NZ would be best described as popular dictatorship with tribal and socialist characteristics.

I believe the current narrative uses the wording "Captain's Call".

(This comment is off topic and has been deleted along with responses from other commenters, Ed. Please stick to the issues aired in the story you are commenting on. More general commenting opportunities are available on interest.co.nz via the comment thread on the morning briefing and what happened today articles. Thank you).

Given that no matter how the people vote at elections the country carries on being managed the same way with the same problems unsolved, it is clear that our elected representatives are totally powerless in the face of the government machine. It does not help if you have a party comprised of people who have barely ever managed anything in their lives - lambs to the slaughter.

Drain the swamp.

Great article.

Act's David Seymour who has also been vocal about the CCCFA changes sat on the Select Committee himself!

What a joke.

I find it fascinating that everyone has already decided the CCCFA was a “mistake” with no one providing actual evidence or figures to show that:

1. The pre CCCFA expense calculations by banks were fundamentally sound

2. The post CCCFA expense calculations are somehow defective

3. Whether it is the legislative rules causing a problem or the banks implementation of those rules

Surely everyone remembers that the Royal Commission in Australia found that all of the big four there were using expense models that grossly underestimated actual expenses, yet the RBNZ failed to validate whether the same behaviour was going on in their NZ subsidiaries.

I can't help but suspect that deciding CCCFA is a mistake has something to do with house prices dropping.

I think the real issue is that when they wrote the rules they didn't realise quite how much debt is considered normal.

It's not just housing... anything that required Finance/credit has been hit. Vehicle sales, Consumer electronics, appliances, Furniture, Utilities.

Then you have all the Credit/quasi credit cards, payment plans, BNPL, and micro/payday loans.

The whole system is grinding to a halt.

Yeah definitely lots of pressure from vested interest, it will be interesting to see how it turns out, I guess this also can bring up the discussion of democracy and benign dictatorship...

The evidence should work the other way: don't regulate unless you can prove there is a problem to be fixed. Can you provide us that evidence?

It was meant to be a solution to loan sharks not banks!

Yes...does seem like that, doesn't it? They should retain the personal responsibility for directors element of the law and remove other specific problems if they can be suitably pointed out.

Interesting article.

I have a career in banking/finance and I work inside/with these regulations on a Daily basis.

Personally I think regulation frameworks in nz is well balanced. I'm currently engaged with one of The regulators mentioned on a piece of organisational change and I have huge respect for the individuals. Pragmatic and professional.

I don't understand the anti cccfa knee jerk though. It really just comes back to the MMT question. Either we keep printing money and pretend inflation is not a thing, or at some point the credit tap needs to stop. It's not rocket science. The ccfa etc is just the money tap starting to squeeze.

Lots of examples of benign dictatorship.

For example, the RMA changes the government introduced last year that will mean cities like Auckland have to zone most of it's urban area for high density development, with very limited legal means for council and residents to oppose it in most cases.

Just see the uproar when the council consults on the required changes in April.... And watch Labour's support in the polls sink further...

The RMA changes that National and Labour worked together to introduce?

The ones that were bought in because councils were trying to water down the Urban Design Statement from 2020 that required uncorking heights along rapid transit routes to allow for more intensification? They got caught playing silly buggers and Govt went over their heads.

This is the kind of regulation I do agree with. There was a problem, the government kept telling the councils to free up more development, the councils kept taking the piss, so the government went over their heads.

With the CCCFA I am not sure there was a serious problem with the banks giving loans to those who can't afford it, and if there was I am not sure the banks were given a chance to rectify it themselves. Regulation should be a last resort not a "hey why not".

Perhaps any CCCFA problems that may exist could be well resolved by simply retaining the personal responsibility clause for directors of lenders. A little personal responsibility is a good thing and ensures that risk is well managed within their organisations. If that results in lower lending, it simply suggests they weren't managing risk adequately before and were counting on the taxpayer as the ultimate backstop.

Housemouse

Time for Labour Govt to go

Like Wellington Protesters, if they won't go peacefully they should be pushed

It's a bizarre take to equate the freeing up of zoning from too much authoritarian restriction on building with "dictatorship".

Surely a bit of cognitive dissonance. How can one claim that giving people more freedom to build on their own freehold land is dictatorship? It's liberalisation!

We need to resist the authoritarian dictatorship of NIMBYism that seeks to rule over what others may do on their own land.

The entire review leading to CCCFA was based on a submission by 2 Whanau Ora sub-providers who did a survey on 74 Maori Housing New Zealand tenants.

To sum up CCCFA in 1 short sentence,

"It's a solution seeking a problem."

You got it in one

The problem of delegating significant powers to regulators is far from unique to this case. It also seems to be the approach being taken with the current exposure draft of the Deposit Takers Bill – where, in an unusual step, the regulator seems to have been given the pen to write a draft law that establishes its own regulatory powers – effectively doing its own delegation from parliament.

Banks don't take deposits and they never lend money. They are in the business of purchasing securities. When one gets a bank loan, the loan contract is a promissory note. The bank purchases that contract from the borrower. Now the bank owes the borrower money and it creates a record of the money it owes, which we call deposits - source.

I owe you + you owe me + magic banking laws = Money out of thin air.

The wealth component is the cash flows (interest) accruing to the banks and depositors, the capital component is extinguished upon liquidation (payment) of the loan.

CCCFA this is how stupid it is! A colleague of mine was recently turned down for a mortgage because his life, medical and car insurance premiums are to high🤣

I like this article very much. Matches my experience in a few areas.

The answer is clearly to let Buddle Findlay write the policy and the regs. For a fee, of course. What do those hapless officials think they’re doing. Dear me.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.