This Top 5 comes from interest.co.nz's Gareth Vaughan.

As always, we welcome your additions in the comments below or via email to david.chaston@interest.co.nz. And if you're interested in contributing the occasional Top 5 yourself, contact gareth.vaughan@interest.co.nz.

— mike luckovich (@mluckovichajc) August 11, 2022

1) Spoofing, gold secrets & gasping jurors.

I love a good probe into the inner workings of the world's biggest investment banks and that's certainly what you get from this series of Bloomberg stories. They cover a court case involving senior figures from JPMorgan's precious metals operations.

As Bloomberg's Eddie Spence and Jack Farchy put it:

The trial of JPMorgan Chase & Co.’s former head of precious metals has offered unprecedented insights into the trading desk that dominates the global gold market.

The story is about the Chicago trial of Michael Nowak, who headed up precious metals trading at JPMorgan for more than a decade, and his colleagues Gregg Smith and Jeffrey Ruffo, for allegedly conspiring to manipulate gold and silver markets. Notably the court was shown internal figures detailing JPMorgan's annual profits from precious metals, which according to Bloomberg, is the first time such detailed information has been made public.

JPMorgan is the biggest player among a small group of “bullion banks” that dominate the precious metals markets, and internal documents presented by prosecutors provided a glimpse of just how dominant a role the bank has played.

In 2010, for example, 40% of all transactions in the gold market were cleared by JPMorgan.

Big Bonuses

JPMorgan’s top precious metals employees on the desk were remunerated handsomely, and some jurors audibly gasped when the court was told how much the defendants had earned.

Ruffo, the bank’s hedge fund salesman, was paid $10.5 million from 2008 to 2016. Smith, the top gold trader, got $9.9 million. Nowak, their boss, made the most of all: $23.7 million over the same period.

Their pay was linked to the profits they made for the bank. FBI agent Marc Troiano, citing internal JPMorgan data, told the court that the total profit allocated to Ruffo from 2008 to 2016 was $70.3 million. Smith generated about $117 million over the same period, while Nowak made the bank $186 million, including $44 million in 2016.

Christian Trunz, an ex-trader, who testified against his former bosses, reportedly referred to Ruffo, a salesman on the bank's precious-metals desk, as the best salesman on Wall Street. Meanwhile, at least 10 central banks held their metal in JPMorgan vaults as of 2010. And we also hear about the hedge fund clients.

In a follow-up story Bloomberg reports Nowak and Smith were found guilty on charges they manipulated markets for years. Ruffo was acquitted of charges he participated in the conspiracy. Spoofing, by the way, refers to large orders intended to manipulate prices that were quickly canceled.

The case was the biggest yet in a crackdown by the US Justice Department. Nowak, the managing director in charge of the desk, and Smith, its top trader, were convicted of fraud, spoofing, market manipulation. The government alleged the precious-metals business at JPMorgan was run as a criminal enterprise, though the jury acquitted all three men of a separate racketeering charge.

“They had the power to move the market, the power to manipulate the worldwide price of gold,” prosecutor Avi Perry said during closing arguments.

US District Court Judge Edmond Chang said Nowak and Smith will be sentenced next year. Each faces decades in prison, though it may be far less. Two Deutsche Bank AG traders convicted of spoofing in 2020 were each sentenced to a year in prison.

Smith, Bloomberg reports; "clicked his computer mouse so rapidly to place and cancel bogus gold and silver orders for BearStearns Cos. and later JPMorgan Chase & Co that his colleagues would joke that he needed to put ice on his fingers to cool them down afterward, or that he must be double-jointed."

Weather and climate issues have very much been in the news of late given recent weather extremes experienced both here in New Zealand and overseas, and the release of the Government's climate adaptation plan. Newsroom's David Williams has an interesting article on letting South Island rivers roam as an alternative to building higher flood banks.

The Canterbury Plains were created by high-energy, braided rivers blasting down slopes between the Southern Alps and the coast, hopping between ancient channels and new ones, forming huge, gravel fans.

Colonised New Zealand has gone to great lengths to try and tame nature, impounding rivers behind banks so floodplains can be developed. Not that it always worked. As former Prime Minister Geoffrey Palmer famously said, Aotearoa is an “irreducibly pluvial nation”.

Human-induced climate change makes extreme weather events more likely, but the way we manage rivers is making matters worse.

“You’d now call it mismanagement,” says Gary Brierley, a Professor of environment at University of Auckland.

Essentially many of our rivers have been strangled, disconnected from their historic channels and confined to smaller areas by engineered flood defences. This has led many riverbeds to build up, or aggrade, considering the huge volume of gravel and sediment being transported from the mountains to the sea.

It has also given people hope, falsely in some cases, that they’ll be safe, pushing development closer to rivers, and within their historical range. Should the worst happen, then, the repair bill for damaged infrastructure and developed property rises, not to mention the risks to lives.

“We are manufacturing future disasters,” Brierley says. “We have created the circumstances by which this is happening.”

3) Isabella Weber on price shocks, inflation & more

Isabella Weber, Assistant Professor of Economics at the University of Massachusetts Amherst, has apparently already effectively been labeled a heretic by some of her fellow economists for calling for price controls on oil and gas late last year as a emergency response to the energy crisis.

Now she has told El Pais that neither monetarist nor new Keynesian views on how the economy works are especially helpful in dealing with the current high inflation. Weber also shares some thoughts on supply chain woes and deglobalisation. It's a Northern Hemisphere focused article, but still of relevance to us in NZ.

I think that to understand the current inflationary situation we need to overcome monetarist understandings of how the economy works, which lay excessive emphasis on the quantity of money and aggregate demand, without paying sufficient attention to the given structures of the real economy and the role of basic inputs such as oil and gas that cannot easily be replaced in the short run. This is something that also the New Keynesian paradigm does not fully account for. It suggest that until you do not reach full capacity utilization in employment and capital, you do not get significant inflation. But that overlooks shortages of basic materials. If you have bottlenecks in inputs that are essential to production across sectors you can reach capacity limits long before you reach aggregate capacity utilisation. Most people looking at inflation thought that this would be transitory and we didn’t need to worry. But this underestimated the importance of such essential materials and input/output relationships and the far-ranging cascading effects that shocks to essentials unleash. It also overlooks the fact that even if inflation was to go away again on its own after some time, price spikes in essentials like food and fuel hit households in the lower parts of the income distribution extremely hard. Some sectors need more redundancy, more buffer stocks to absorb the shocks avoid the shortages that we are currently experiencing.

In a deglobalizing world we risk dealing with enormous price shocks and dominant economic theory is not preparing us to deal with this. Deglobalisation can be an inflationary force especially if it happens in a chaotic manner. We have an extremely interconnected global economy in which many countries are dependent on monocultural exports. If trade is disrupted this can lead to supply issues, rising prices due to rising costs or simply reflecting temporary scarcities and pricing power. On top of that we need to consider the long-term impact of climate change. Because of high temperatures we can have negative effects on basic infrastructure, such as roads melting, and there are all sorts of industrial processes that need to happen within a certain temperature band. Climate change and extreme weather events can cause or exacerbate supply chain issues. Before the current multifaceted crisis, globalisation was dominated by just-in-time production networks. If demand went up, supply could easily follow and prices were remarkably stable. But now you have the opposite situation. If supply networks are not operating just in time anymore, when supplies stop flowing prices rise. In face of sector wide supply disruptions, the dynamic of competition switches from competition for market shares, to a dynamic of competition which prioritises charging higher prices for available inventories and this can be a further inflationary factor.

4) Shock, horror, NZ port reform sought

Back in May I wrote about a Ministry of Transport issues paper on government plans for New Zealand's first ever comprehensive freight and supply chain strategy.

I followed this up in an episode of our Of Interest podcast with Tava Olsen, Professor of Operations and Supply Chain Management and Director of the Centre for Supply Chain Management at the University of Auckland Business School. Olsen said that while the issues paper does an excellent job of outlining the background and all the issues, a national supply chain strategy doesn't make much sense.

Now the Ministry of Transport has released the bulk of the 83 submissions it received and a summary of them as it moves on with a draft strategy.

Not surprisingly given the issue is something of a long-term festering sore, the Ministry says there was strong interest in port reform. Although given significant local government ownership, some submitters might be over optimistic if they think the market will solve their problems.

Many submitters desired some sort of review or reform of the current port system. Ideas included: reviewing the ownership model, competition settings, and moving towards a hub and spoke model for our ports. Some submitters felt that the shift towards the optimal port model would happen naturally through the market over time, others felt that a national port plan and regulatory reform was needed to achieve change.

Relatedly submitters also suggest international and coastal shipping faces significant changes. Maybe this could force changes on our ports?

International shipping to New Zealand is expected to develop into more of a hub and spoke model, although perspectives on the degree to which ports and volumes would consolidate, and the speed with which it would occur differed dramatically. There were some concerns about New Zealand’s coastal shipping sector only recently having begun to grow again after decades of decline meaning that there may not be the domestic capacity to meet the required or desired mode shift.

5) China's village bank collapses explained

You've probably seen the recent stories of Chinese bank depositors clashing with police. Writing for Foreign Policy Magazine, Zongyuan Zoe Liu provides an overview of what ha been going on through the wave of bank runs in China. Frozen deposits in online accounts have reached 40 billion yuan and affected some 400,000 depositors. China, the article argues, is fighting a war on multiple fronts against financial insecurity, from dubious online investment schemes to an ongoing property crisis.

Featured are what are described as small and medium-sized banks (SMBs), and village and town banks (VTBs).

The recent bank runs started from three rural village and town banks (VTBs) in Henan province. Three more runs on VTBs happened within a month, including two in neighboring Anhui province. Five of the six troubled VTBs have the same major shareholder bank, Xuchang Rural Commercial Bank. Not being able to withdraw their life savings has led to protests by depositors, triggered panic over the solvency of small banks, and increased the nationwide risk of runs on small banks.

VTBs comprise 84 percent of China’s banking institutions but held just 13 percent of the total assets in the banking sector by the end of 2021. Chinese policymakers envisioned these banks as a pillar of microfinance supporting farmers and small businesses in rural China, and in 2006 they proposed pilot projects in six rural areas. Fifteen years of policy experiment has left the Chinese financial system with 1,651 VTBs that are now the most numerous entities in the banking system but individually are both small and very weak at risk management. The People’s Bank of China (PBOC), the central bank, has rated 186 rural cooperatives and 103 VTBs as the riskiest among all Chinese banking institutions. In other words, close to 7.5 percent of Chinese rural banking financial institutions are already at the highest level of risk—and the problems may go even deeper than that.

A key problem for the smaller banks is a lack of capital. This has led them to alliances with unregulated online deposit platforms. Problems have followed.

SMBs have become the most fragile part of the Chinese banking system. One of the key structural issues is the lack of capital replenishment channels for SMBs. They have low profitability, which makes them unable to generate replenishment capital internally. They are also unable to raise funds through external channels such as initial public offerings due to their small scale and poor credit ratings. But small banks found a natural ally as they competed with their peers for survival: online deposit platforms provided by fintech firms that were not licensed banks and thus unregulated.

These platforms, many of which made exaggerated claims about returns and some of which have turned out to be outright frauds, brought a steady stream of funds to small banks over a short period by listing deposit products online and selling them to their nationwide users. By the end of 2020, 89 Chinese commercial banks (84 SMBs) had attracted 550 billion yuan ($81 billion) worth of online deposits through such platforms, an increase of 127 percent compared with 2019. In some cases, online deposits sold to nationwide depositors even replaced interbank financing as the primary source of funds. The PBOC found that some high-risk small banks amassed 70 percent of deposits from nonlocal online deposit products sold by third-party platforms, whereas interbank financing as a percentage of total liabilities dropped from 30 percent to 3.2 percent.

In January 2021, Chinese regulators banned commercial banks from selling deposit products through third-party online platforms in a notice jointly issued by the CBIRC [China Banking and Insurance Regulatory Commission] and the PBOC, citing concerns of increased hidden risks and the potential for financial contagion. The crackdown on online deposit products removed the life support for many SMBs with limited alternative capital replenishment sources. At that time, online deposits had reached an estimated amount of 1 trillion to 2 trillion yuan.

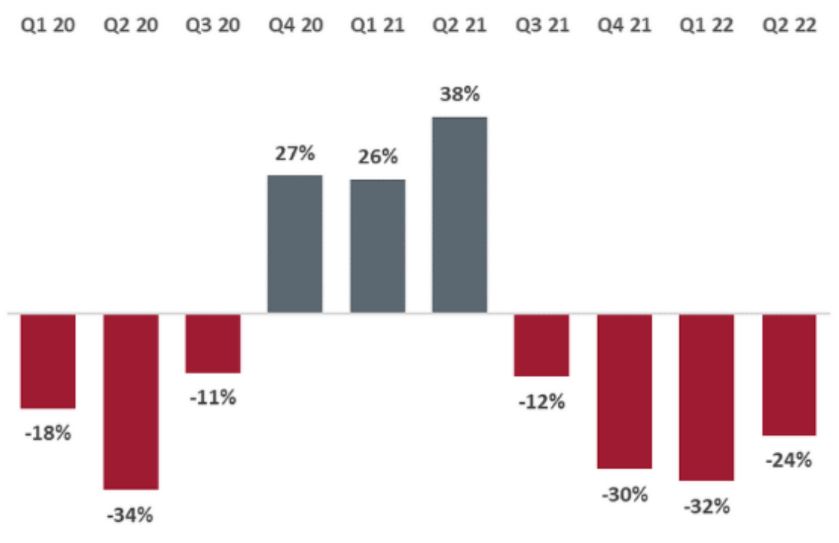

NZ consumer credit demand index, year-on-year changes (%). Source: Equifax.

25 Comments

23 mil over 8 years doesn’t seem that amazing for the best salesman on Wall Street. NZ banks pay their CEOs more don’t they, and I doubt they need to be particularly special.

All markets have been stuffed by rentier speculation and rigging,

https://www.project-syndicate.org/commentary/financial-traders-commodit…

Isabella Weber was absolutely savaged for an article last year that diagnosed the causes of inflation accurately and advocated for supply side solutions to inflation, including price controls. The pile on from the establishment economists / monetarists was disgraceful.

She was absolutely right of course, and since then, the tide has turned and her stock and reputation has risen considerably. Isabella will be one of the few economists that come out well from this whole episode - and we will need sensible voices like hers to help us navigate the next few years.

Lord knows we will be lost if politicians listen to Summers, Sachs, or NZ's own dollar-shop Furman - Crampton.

Price controls? Sounds like a dumb idea to me. Didn’t we try all that in the 70s before working out that monetary policy is actually the best way to control inflation.

Back in Muldoon days, price controls came with side orders of wage & rent controls. A complete unmitigated disaster.

Muldoon should have floated the NZ Dollar instead of operating on a fixed exchange rate which was a hangover from the gold standard days.

Nope.

Price controls has been tried many times throughout history and across different political, social and economic systems. No attempt has ever worked, and usually has resulted in disaster.

Yes we could do something unconventional like Turkey or Venezuela, but I reckon it won’t work very well.

What like borrowing billions of US dollars? Or following the advice of the IMF and ending up being milked by foreign capital? That would be stupid.

Incorrect. There is a whole body of work on this and many countries still operate successful price controls. Did you know that rents for tens of thousands of rentals are controlled in the UK for example? Or that France sets the price of energy? Or that NZ sets the price of the minimum wage, and controls the price of carbon, and credit?

And let's not forget that we have controls on the Price of Debt - % rates, yet that seems to be a-ok.

If we want a truly free market, then allowing interest rates to find their own natural level should be part of the process.

Controlling only part of our economies and not others has led us to where we are today.

I'd like to see no controls (especially Price of Money) and no bailouts, but I don't think we'll be rid of big govts doing stuff like that, not until Mad Max is out there chasing down barbarians. It's just too lucrative for those nearest the money spigots.

Fortunr - that is the received wisdom from most economists, but it is not actually correct. What is needed is an understanding of what is driving the price increases and what the controls are intended to achieve. Price controls and other measures like rationing can help a country manage big supply shocks and ensure equitable access to goods. For example, price controls and similar measures like rationing during and immediately after WW2 worked quite well.

"calling for price controls on oil and gas late last year as a emergency response to the energy crisis."

Wasn't it President Bush jnr who used the term voodoo economics. Look no further than Sleepy Joe for this and his disastrous cut back of oil and gas exploration and putting a halt to the Canadian oil pipeline amongst other measures. Throw in one or two states with some detrimental legislation on fossil fuels and you have a recipe for price increases.

Voodoo economics was used by Bush Senior about Reagan. https://www.investopedia.com/terms/v/voodooeconomics.asp

Thanks. I'll now include Isabella Weber amongst the voodoo economists.

Isabella Weber appears to have her head screwed on the right way....almost guarantees she wont be heeded.

As the risks from climate change advance across the globe and affect all countries to a greater or lesser degree I would like to know how well set up our country is to survive these extremes. How secure are our water, electricity, transport and communication systems for each and every dwelling? If we had to survive on our own as a country where would the vulnerabilities be? The covid border closures were only for people. What if our ability to import food from offshore was restricted? Maybe these questions have been answered somewhere. If anyone could point me in the right direction to that report I would be grateful.

Our plan for future climate collapse goes something like, grab a shovel, dig a hole, place head in hole and then back fill the hole using scooping motions with arms.

Love it!

'Essentially many of our rivers have been strangled, disconnected from their historic channels and confined to smaller areas by engineered flood defences. This has led many riverbeds to build up, or aggrade, considering the huge volume of gravel and sediment being transported from the mountains to the sea.

It has also given people hope, falsely in some cases, that they’ll be safe, pushing development closer to rivers, and within their historical range. Should the worst happen, then, the repair bill for damaged infrastructure and developed property rises, not to mention the risks to lives.

“We are manufacturing future disasters,” Brierley says. “We have created the circumstances by which this is happening.”

And these are the nuances we are missing with climate change.

If my house floods and I put the blame generically on Climate change, then tax everyone to 'solve' this problem, it would pay to check whether the flooding was due to extraordinary rainfall (by whatever reason either Human-induced or natural cycles) OR I had just had the washing machine overflow.

But hey, if I can get the whole country to pay every time my washing machine overflows, am I going to look too closely to see if the real reason was all my fault?

Supply side disruption is an interesting topic all of a sudden. What was allowed to happen over the past 30 years was fine when we all got along. Or even, when we thought we all got along. However that season seems to be over for a variety of reasons.

Our ability to relate to someone unlike ourselves is an interesting study on its own, & one I had to learn early in my time away. What i learnt was that we (the west) were not the most popular people on the planet & never were from most accounts. There were moments (in Pakistan & Morocco) I can remember thinking I need to get out of here, and quickly. Doubtless there would me many more if I had ventured that far. Some of the stories we heard from our fellow travelers about places like Indonesia, Laos, China, Russia, Bolgaria, Mozambique, Ceylon, Lebanon, Iraq, Yugoslavia, Colombia, Peru, Brazil & many other places still stick in my mind. Egypt, Ethiopia & the Sudan were others. [You can gather this was some 40 years ago.]

My point being that the world is a dangerous place in a lot of places, that we conveniently never hear about through our usual means. We had rocks thrown at our bus in Isfahan in Iran, but it was still a cool place to visit. However, my other point is this: Do not believe everything you hear, listen to or read about through your limited channels of learning or listening. Most of what we are told is biased or told from a specific perspective or with a specific end in mind. Everyone has bills to pay & at the end of the day, they don't really care enough to tell you exactly what the real situation is, if it doesn't fit their narrative. Sadly, it is getting worse.

A lot of what we are told is BS. And every side does it. It is very hard to imagine what the reality is out there for 3 out of every 4 people on the planet (even today) unless you've been in it. I can still here my mother telling me ''The world is your oyster boy." Well, it was nearly the death of me in a few places.

So, what has all this got to do with the falling/failing of some regional banks in China you might ask?

Simply this. Nothing is certain. The only certainty is uncertainty. This is a good lesson to understand, even for here in NZ. What seems to be happening may not be happening the way you choose to see it happening. There are always many agendas. Trust very few people. It is safer that way. Believe even fewer. It is probably mostly BS anyway. Love your family & your friends. Lots. Be grateful for each & every day, for you know not what will be here tomorrow.

What is happening there, will probably happen here at some point. We are not smart enough you know any different. Sigh. Indeed, we have let ourselves down from the first day at school right up to now, in so many ways too many mention here.

We are human therefore, we are fallible. And it will be what it will be. And, if my experiences are anything to go by, it may get ugly. Take care.

All University Economics degrees should include Engineering and Agriculture 101 courses in the first year.

Absolutely no engineer would be surprised that if the cost of energy increased faster than energy intensive processes can be engineered out then the cost of a product will rise. There's a reason that cars now are "plastic fantastic", it costs far less to injection moulded GRP than stamping out welded steel parts.

Similarly farming, if input costs rise faster than yields or production efficiencies can be found then prices will rise.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.