Inland Revenue has released a paper for consultation under the dry title Proposed Legislative Changes for Intermediaries. This doesn’t sound terribly exciting for the general public, but it’s actually quite important, because it looks at the role of tax agents and other intermediaries.

The expanding role of tax intermediaries

This has not been a very heavily regulated area and understandably, there's been quite a lot of changes in the dynamic over the past 30 years since the Tax Administration Act was passed in 1994. That act specifically referenced tax agents, but other intermediaries have popped up in this space, such as those dealing with PAYE and tax pooling companies.

The purpose of the paper is to recognise that all these intermediaries have a crucial role in the tax system. And part of it is to set out clear rules as to who can be a tax agent or tax intermediary and how they will be regulated. This is crucial as tax agents and other intermediaries are given access to vital information.

Why register with a tax agent?

Now, the main intermediaries discussed in the paper are tax agents. Currently, there are around 5,000 tax agents registered with Inland Revenue. If you're registered with a tax agent, apart from them having direct access to your information provided by Inland Revenue, a taxpayer also gets what we call extension of time arrangements.

This usually means that if you've registered with a tax agent, then the due date for filing a 2026 tax return is extended from 7th July 2026 to 31st March 2027. (And yes, many tax agents will see clients coming in on the 30th or 31st of March 2027 asking for their 2026 tax returns to be done.)

And the other benefit, and arguably much more important, in terms of cash flow, is that you get an extra two months to pay your terminal tax. Generally, terminal tax payments for the 31st March 2026 tax year will usually be due on 7th February 2027. But if you have a tax agent, that's extended until 7th April 2027.

In addition, tax agents can communicate directly with Inland Revenue on behalf of clients and as part of this are given access to taxpayers' personal details. However, it’s presently pretty easy to become a tax agent. Currently, you can apply to be a tax agent if you have 10 or more clients for whom tax returns are required to be filed. Now in this paper, Inland Revenue acknowledged it had been a bit uneasy about that particular rule because it's quite possible that a person may be able to find 10 family members or friends as clients and then apply to be a tax agent. Coupled with the ability to access sensitive information, the opportunity for a tax agent to commit fraud is obviously a risk

Christchurch’s Andy Dufresne

One of the more memorable cases of gaming the system involved Carl Peterson, a sort of lesser Andy Dufresne from The Shawshank Redemption. Way back in the early 2010s, Peterson was in Christchurch prison and began helping other inmates with filing their tax returns and obtaining legitimate tax refunds.

Peterson realised he was onto a good thing, so he successfully registered as a tax agent whilst still in prison. He went on to make fraudulent claims for non-existent taxpayers totalling $50,000. Anyway, it rebounded on him because, apparently, gang members within the prison found out and put him under pressure. Finally, these frauds were discovered, and he got another year added to the 11-year sentence he was then serving.

The point is that the system still remains loose around who could be a tax agent. Peterson was caught and sentenced in 2013, so Inland Revenue has obviously had some concerns for some time, but it's now finally taking action.

Tightening the rules

The paper proposes a number of changes. There will be three new categories of intermediaries: digital services providers, data consumers and a category of bookkeepers. The Commissioner of Inland Revenue will be given more discretion to disallow someone from being a nominated personal tax intermediary. The current 10-client rule for becoming a tax agent or a bookkeeper will be replaced with a requirement to be a member of an approved professional body.

Currently Inland Revenue recognises some professional bodies as “Approved Advisor Groups” on the grounds that their members must:

- have a significant function of giving advice on the operation and effect of tax laws

- be subject to a professional code of conduct in giving the advice, and

- be subject to a disciplinary process that enforces compliance with the code of conduct.

The organisations that currently have Approved Advisor Group status are:

- Accountants and Tax Agents Institute of New Zealand

- CPA Australia

- Chartered Accountants Australia and New Zealand

- Institute of Certified New Zealand Bookkeepers

- New Zealand Qualified Bookkeepers Association.

The plan is that any future tax agents after the relevant legislation is passed should be a member of one of these groups. Although this initiative is mostly of administrative interest, aimed at improving the running of the tax system, it is one which should have benefits for the wider tax community.

Trusts and United Kingdom resident beneficiaries

An area in which I am increasingly involved, and ironically takes me back to my UK roots, is in relation to distributions made by New Zealand trusts to UK resident beneficiaries. A common theme is that these trusts were established for asset protection purposes 20 to 30 years ago when the settlors were in business. The settlors are now either retired or winding down their activity.

One of the things about New Zealand is that we have a very fluid population, with significant numbers moving emigrating, immigrating or returning from their OE. (More on that below.)

For many doing their OE, the assumption is they will return to New Zealand, but people decide to stay, change their plans etc. For example, I initially arrived here on holiday and basically never left. And the same happens to people who go to Australia or the UK. They meet someone or land an extremely good job, their career takes off and the next thing you know, they've been overseas for some time.

The great wealth transfer

At the same time, we have the Baby Boomers and Generation X, the two richest generations in history, who are now starting to shuffle off this mortal coil. This means there's a great transfer of wealth involving trillions of dollars happening. We referenced this in our last episode when discussing the EU and its paper on wealth taxes.

Obviously, with children and grandchildren overseas, grandparents and parents want to make distributions to those descendants. And this is where they hit a major hurdle, which is often exacerbated because New Zealand does not have a capital gains tax.

The UK would classify the typical New Zealand trust as a non-resident trust for UK tax purposes. Any distribution of income (as calculated for UK purposes) will be taxed at the beneficiary's marginal tax rate (potentially 45%). This is relatively uncontroversial. Helpfully, distributions of accumulated income to other beneficiaries, including those not UK tax resident can be taken into account when determining what proportion of a distribution represents income for UK tax purposes.

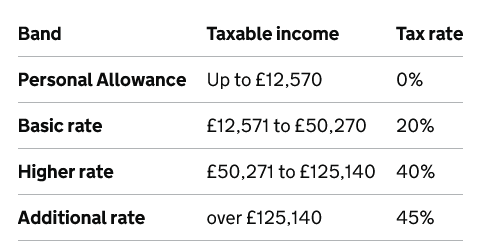

UK income tax rates

It's in relation to distributions of capital gains (as calculated for UK capital gains tax purposes) that matters get really problematic. Unlike distributions of income, the total historic gains of New Zealand discretionary trusts are taken into account when calculating what proportion of a distribution to UK resident beneficiaries is taxable.

Take for example, a New Zealand trust which has, since its settlement, realised one million dollars of (non-taxable) capital gains. These gains have been distributed in full to New Zealand resident beneficiaries.

The trustees now wish to make a distribution to the UK resident beneficiary. The hope is that with all the income and gains of the trust distributed to New Zealand resident beneficiaries, the distribution to the UK resident beneficiary would be tax free for UK tax purposes. Unfortunately for the UK beneficiary, that will not be the case.

Are those capital gains really tax free?

Firstly, the fact that the capital gains are tax-free for New Zealand is ignored. These were capital gains that would have been taxable in the UK. Furthermore, any capital gains that may have been distributed to any non-UK tax resident beneficiaries are ignored for UK tax purposes.

Consequently, any distribution of the trust’s million dollars of capital gains to the extent it wasn't income that year would not be treated as tax-free capital, but as a distribution of capital gains, probably taxable at up to 24%.

This is an increasingly common scenario I’m encountering. In one case, the trust in question was settled in 1972. Just to compound matters, if the capital gains (for UK purposes) can’t be identified, the distribution will most likely be deemed to be income and therefore taxable at up to 45%.

This scenario should prompt the advisors for the baby boomer generation in particular, who have reached retirement age, to think carefully about the role of the family trust for them. In particular, what they want to do about overseas-based beneficiaries. Because in essence, they could be passing tax liabilities down the line.

Beware the “hotchpot clause”

Now you might say, well, that's the overseas beneficiaries' problem. They’ve made their bed; they lie in it. One Jersey court has basically said the same thing. But there may be some issues if the trust deed includes a “Hotchpot clause”, which basically tries to equalise things between beneficiaries. In this case the overseas beneficiaries' tax bill becomes a big problem for the trustees.

It’s an issue for careful consideration. But it's also an example of the golden rule - if there's a cross-border transaction (and the size of the transaction doesn't really matter), you need to seek advice. It’s likely you’re probably walking into a minefield either for the trustees or for the beneficiary.

Immigration and tax

The issue of immigration has hit the headlines after ACT proposed some tougher restrictions around migrants, including a $6 per day infrastructure charge for migrants who come in on short-term work visas. One of the things that stands out about New Zealand is the extraordinarily high proportion of the population who, like myself, were born overseas. According to the 2023 Census for the whole country it's 28.8% and a quite astonishing 42.9% in Auckland where I'm based.

Now we immigrants are an increasingly important part of the economy not least because we pay a lot of tax. Just how much in proportion to our population base is something that hasn't been generally considered until Treasury prepared a couple of Analytical Notes as part of its 2025 Long-term Fiscal Statement He Tirohanga Mokopuna. The first Analytical Note, AN 25/10 Transnationalism over the Life Course of New Zealand Birth Citizens, was published last October. The second Analytical Note AN 26/02 Transnationalism and tax payments among the foreign-born, was released in late March. This is an extremely interesting paper which examines the tax paid on personal income, primarily through PAYE.

"Foreign-born people increasingly pay more tax than their population share would suggest"

Analytical Note 26/02 reveals how the income tax paid by foreign-born persons has risen faster than their population share. In 2000 foreign-born people represented 24% of the population which matched their share of individual income tax on market income. However, by the tax year ending March 2024, the foreign-born made up 32% of the population but now paid 38% of the tax.

As the Executive Summary noted “The central finding of this paper is the simplest. In aggregate, the foreign-born are becoming increasingly important for the country’s tax base.”

This conclusion should perhaps give all the politicians happy to raise immigration for short-term electoral gains pause for thought. They might well be literally biting the hand that feeds some of their would-be voters.

The two Analytical Notes are worth reading for their insights into our economy and should be part of any reasoned debate about migration and a long-term population strategy. I’m not confident we will see such a debate during this year’s Election campaign.

On that note, that's it for this week. I'm Terry Baucher and thank you for listening. Please send me your feedback and tell you and requests for topics or guests. Until next time, kia pai to rā. Have a great day.

[This is the transcript of the episode recorded on Monday 4th May – it has been edited for brevity and clarity]

2 Comments

Analytical Note 26/02 reveals how the income tax paid by foreign-born persons has risen faster than their population share.

Interesting.

Does this insinuate that NZ born citizens are more clued in with the tax system and how to minimise tax payments legally? for example the likes of residential property investment (long heralded as the core way to set one's self up for retirement and build wealth) is more prevalently used by NZ born citizens to minimise tax.

As always, great article Terry.

I'd guess it's simply that migrants are more likely to be of working age, and perhaps also slightly higher earners on average. Our immigration system is pretty good at filtering for the most productive immigrants which is probably one reason that immigration is not as unpopular here as elsewhere, despite being very high.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.