This article is a re-post of the July 2020 Insight, from NZIER. It is here with permission.

Covid-19 has changed the trade game that New Zealand plays. With the structure of the New Zealand economy based on our exports the stakes are high.1 Now that New Zealand has shifted through the lockdown levels and arrived at Alert Level 1, it is a good time to ask why our land-based exports have been so resilient? Why are we not staring into the trade and trade policy abyss?

This is particularly startling given the rise of protectionism during the initial Covid-19 phase. The United States (US) and European Union (EU) have been quick to support farmers further in ways that will have medium to long term negative impacts on agricultural trade. While the protectionist credentials of the US and EU are well established, big unknowns will be the reaction of India and China to further protectionist moves. None of this is helped by the freeze in place on appointments to the WTO Appellate Body which will make it difficult to wind back any new subsidies.

The nature of New Zealand’s trade, China, and strong institutions have combined to minimise Covid-19 uncertainty

The Covid-19 crisis has shown the benefit of ‘keeping-on-keeping-on’. Whatever Covid-19 has done to other parts of world trade, it has reinforced the underlying strength and importance of New Zealand’s land-based industries. While it may be a surprise to some, land-based industries have been the stalwarts of the New Zealand economy that have seen us through the continuing Covid-19 crisis. Land-based industries have survived and are coping with a number of uniquely New Zealand based strengths and other factors beyond our control. Some of these are built into how New Zealand approaches trade and trade policy game and therefore are not replicable by other countries.

The rise of China and the parallel rise in third country demand on the back of their own trade growth with China has had a major impact on New Zealand. We have played our trade policy cards well in this game since we have recognised and welcomed China into the world economy. This has been important to China since New Zealand is a small but ‘industrialised nation’. It showed other industrialised nations that China can connect, and do civilised business with industrialised nations.

The steady growth in demand for land-based products from China and other Asian nations has been fundamental. It has been enough for New Zealand to shake off and overcome the biggest destabilising impact on world temperate-zone land-based trade: the subsidy regimes generated in the EU and the US that flood world markets with large volumes of product at disposal prices.

New Zealand product quality and consistency is trusted. This didn’t happen overnight. There have been hard yards of institution building that are now shining through in an era of increasing global interconnectivity. Governments and people around the world continue to ‘buy New Zealand’ based on trust in our product integrity.

Of particular importance is the nature of the land-based products we trade. Commodity trading goes hand in hand with flexible supply chain access. Not only are we flexible about what countries we can trade with but we are also flexible about the product range offered. This allows us to maximise the returns subject to the Covid-19 constraints and reduces the amount of investment required in the market. Underpinning this demand has been the general growth in demand for food and fibre in Asia.

Below we look at each of the factors that have reinforced our commodity trading status. We also review the various sectors that are heavily dependent on trade and how they are coping with the continued Covid-19 crisis.

China has arrived – get used to it

Who is buying is always the key to understanding strength of sales and profitability. NZIER first realised the dramatic impact that China would have on New Zealand in the late 1990s and early 2000s (NZIER 2005). The International Food Policy Research Institute (IFPRI) (2002) built a world trade model at this time to demonstrate the likely impact on commodity prices of China’s entry on to world markets. Tellingly, the reason for building the model in the first place was that the Chicago Board of Trade had realised that world prices for selected agricultural commodities were no longer being set by the United States.2

The IFPRI forecasts weren’t overly dramatic in any shape or form. They predicted essentially stable prices out to 2020. However, the world price stability that China’s entry on to world markets brought in agricultural commodities was dramatic for New Zealand. Prior to 2000, the real price of our agricultural products had been falling year on year.

The spectre of stable/increasing prices of butter and the falling prices of flat screen televisions was totally unexpected.3 Not only have we found a large and growing market for agricultural products, we also had cheaper imports: the so called ‘double dividend’. New Zealand was also in one of the ‘first free trade agreement (FTA) cabs off the rank’ since we were flexible enough to develop a FTA with China that suited both our needs: it helped China demonstrate it could put together a FTA with a developed nation and it gave greater access to the Chinese market for New Zealand goods – particularly agricultural goods.

The stronger Chinese connection through the FTA also assisted in broadening the New Zealand economy.4 The doubling of tourist numbers over the past five years (another surprise) in pre Covid-19 times not only made tourism the number 1 export industry but also stimulated demand in the domestic economy for jobs and investment. Trade in education has also been strong.

Raising-of-all-boats impact

Of-course all other nations have experienced a marked increase in trade with China. It’s hard not to; China is now the world’s largest trader by value.5 This has stimulated their economies with various effects on New Zealand depending on their relative economic connections with the Chinese economy. Since trade is not a zero-sum game the broad impact has been positive: ‘a raising-of-all-boats effect’. As countries have improved their economic positions and become more interconnected it has stimulated further demand for New Zealand goods and services. This has been reinforced by a network of trade agreements signed by New Zealand, mainly over the past 20 years.

Without the disruptive force of China’s rise and its positive warping of world agricultural trade, New Zealand’s economic position would be less buoyant and possibly even precarious, given the impact of the Christchurch earthquakes and the current Covid-19 crisis.

The combined impact of China and associated third country demand has lifted demand to such an extent that the subsidy impact of the US and EU has diminished. Not so long-ago New Zealand’s export trade was heavily affected by EU and US subsidies. World prices of dairy products would decline EU subsidies increased and we even tried selling US butter6 on New Zealand markets to reduce the US butter mountain.

Institutions not only count – they are becoming more important

Institutions are becoming more important, particularly in food processing. Institutions7 are about the strength and effectiveness of the rule of law within a country/region and also the strength and effectiveness of informal rules (North 1991). Milgrom et al (1990) infer that strong and effective institutions can act as an “effective bond for honest behaviour in a community”.

A country that exhibits strong and effective institutional behaviour is likely to be able to survive and thrive in a globalised world – even one where chaos abounds – as a trusted supplier.

We are now starting to see food processors specifically locating to New Zealand to benefit from New Zealand’s institutional strength and effectiveness. For example, Blue River Dairy in Invercargill is importing sheep and goat milk from across the world to process in New Zealand as infant formula for the Chinese market. A Japanese company, Sumitomo Corporation has backward integrated into a carrot processing facility in South Canterbury to process carrots into carrot juice for the Japanese market.

In both cases the product quality and consistency are backed up by trust in the strength and effectiveness of New Zealand’s rule of law. This is likely to become more, not less important as global connectedness intensifies (NZIER 2017).

Impact of Covid-19 on land-based agriculture

Steady as we go….

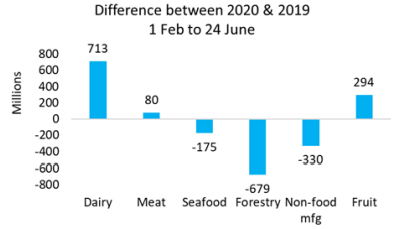

The general picture for exports seems to be of cautious optimism but bracing itself for the coming recession (see Figure 1). The cautious optimism is based around the continued consumption demand for New Zealand farmed products despite Covid-19. This is underpinned by the quality, consistency, as well as our trusted supplier status. Further the ability to move product between categories has also assisted (e.g. moving product out of food services into ingredients and other product categories in dairy).

Figure 1: Major export trade comparisons

Source: Statistics NZ

The continued persistence of Covid-19 particularly in the US and the United Kingdom (UK) is a concern. How this plays out is very uncertain. It may affect US consumption of retail goods which could impact on Asian demand and so incomes. This means that they may have less to spend on New Zealand products and services.

Two factors may be to New Zealand’s advantage:

1. New Zealand has less exposure to the US and Canada because they have, over the years, protected their home markets against New Zealand competition.

2. Recessions do not impact on commodity products relative to other ‘nice to have’ products.

Countries don’t have friends they have interests

The ‘America first’ approach and the behaviour of an inward-looking EU have been the realities of post-World War II trade. Agricultural trade, particularly in milk and meat products has continually been destabilised by the domestic-focused policies of these two over producers.

Currently, there are concerns that the EU and US are increasing supplies of milk that may flow onto world markets forcing international prices down. Although because they are subsidy-driven (and not market-driven) they tend to be leaden footed about product selection, e.g. EU milk tends to be converted into cheese rather than other products irrespective of demand. Therefore, there are opportunities for market-led New Zealand players.

Some perspective required on the China relationship…

Every country is grappling with the China question: Are we too dependent on bilateral trade with China? Ideally New Zealand aims to be traders with the world. We want to diversify our risk to ensure that we do not get confined or locked into relationships that could preclude trading with other nations, or fall foul of a specific market shock.

We do face some choices at the margin, but we do need to keep things in perspective:

1. As much as we are dependent on China now, we are nowhere near as dependant as we were on the UK. Trafford8 compares the reliance on the British and Chinese market in Table 1. We note that New Zealand’s dependence on a small number of products in the British market left us wide open to a larger risk factor relative to the much broader connection we have with China.

2. The US has had an eclectic approach to trade agreements. Donald Trump withdrawing the US from the Trans-Pacific Partnership (TPP) was just the latest of a long line of US disappointments which stretch back to 1955 when they introduced an agricultural waiver9 into the GATT (Nixon and Yeabsley, 2002).

3. China can be single-minded about specific internal, trade, and foreign policy issues. Just as single-minded as the United States. In this area no country can claim the moral high ground.

4. If New Zealand did want to divert trade from China: How would we do it? How much trade should we divert? Are we prepared to accept a lower standard of living? Would New Zealand trade be more or less resilient?

Table 1 Dependence comparison between China and the United Kingdom

Source: Trafford 2020

The current Covid-19 crisis

What we have always known about New Zealand trade is that the fine details of the specific markets need to be understood to fully understand how well New Zealand products will perform, e.g. in some markets we face nontariff barriers, in others, such as horticultural products we face strong competition from Chile, and in yet other markets we have ‘windows of opportunity’ to sell our products.

Further, small changes either positive or negative to other supplying nations’ product mix can have a huge impact on New Zealand, e.g. a pig disease (African swine fever) in China in the latter part of 2019/20 resulted in half the Chinese pig herd being slaughtered.10 This increased world prices for exported protein (including sheep meat from New Zealand) in 2019/20 and prices are still elevated.

What has helped the competitiveness of New Zealand products has been the flight to the US dollar. In times of crisis the US dollar has been a safe haven for investors and the Covid-19 crisis is no exception. It has assisted by lowering the New Zealand dollar in relation to the US dollar. Unfortunately, this phenomenon has been brief and the New Zealand dollar is now tracking upwards – potentially a sign of faith in the New Zealand economy.

Transport hurdles (airfreight) have mainly been confined to time-finite goods travelling by airfreight. Typically, 80% of airfreighted products have travelled in the holds of passenger aircraft. With borders closing and international passenger flights curtailed, the ability to move products has been restricted. This has mainly hit seafood (e.g. lobsters) and horticultural products. The Government has subsidised freight transport to important markets, which has helped alleviate the problems.

Another challenge is employment, particularly in horticulture and forestry. Apples, kiwifruit, and wine have survived the current picking season despite what seem to be significant labour market rigidities. Horticulture and forestry do rely heavily on the Pacific recognised seasonal employer scheme and non-New Zealand pickers on working holidays. Employment challenges in the future will be highly dependent on how long the border is closed for, which is a major uncertainty.

A longer term concern is investment. Certainly, investment has become ‘tighter’ with Covid-19. Will the fall in investment flows have a medium term impact on the land-based sector if Covid-19 continues? Government has responded with an investment strategy and ‘shovel ready’ projects but this is still and an area of uncertainty.

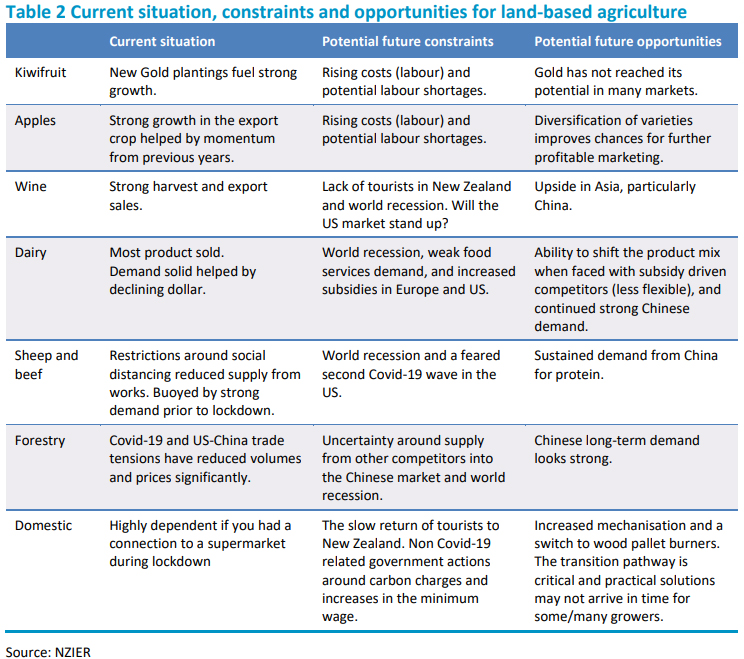

Table 2 sets out the portfolio of New Zealand’s major land-based industries. A strength is the diversity of the group. While individual trades may experience short term fluctuations – to shocks like Covid-19 – as a whole the trades are solid performers. Nothing is likely to dramatically change as long as we stick to product quality and consistency, maintenance of strong institutions, and effective trade policy strategies and tactics.

The golden trade policy age may be over…but there are some silver linings…

At the end of the Uruguay Round in 1994 three things were clear:

1. Markets would become more open over time.

2. Rules were enforceable and most nations self enforced those rules.

3. The social licence for trade in New Zealand was solid and there was positive political bipartisanship.

None of these things can be taken for granted any more. The golden age is over but as you can see from the commentary above the outlook is more like weather in Auckland than Wellington.

Notes:

1 Even though most people are employed in the services sector, the structure of the New Zealand economy relies on export returns. The impact of curtailing any exports has a dramatic impact on the services sector.

2 They were being set by Chinese demand, conversation with Chris Delgado, IFPRI.

3 This was contrary to the earlier pessimism associated with the Prebisch-Myrdal view of the world: that manufactured goods would be income elastic while agricultural commodities’ prices were fated to decline in real terms. See A R Puntigliano and O Appelqvist (2011)

4 FTAs are designed to attempt to create new opportunities for exporters or level the playing field. FTAs with the US and EU may also add to market diversification and mitigate against further dependency on one market if the opportunities present themselves.

5 Exporting US$2.499 trillion worth of goods in 2019.

6 Branded ‘Twin Flags’ to try and use both nation’s national symbols.

7 To the point that the Ministry for Primary Industries realise it is part of the food marketing chain. See for example https://www.mpi.govt.nz/processing/

8 https://www.interest.co.nz/rural-news/105302/guy-traffordpoints-out-our…

9 The waiver exempted US agriculture from GATT disciplines. It was only with the signing of the Uruguay Round (held up by United States agricultural interests for two years) that agriculture came fully into the World Trade system.

References:

Delgado C (2002) The Livestock Revolution in Developing Countries: Issues and Implications. Presentation to NZIER 26th April 2002. International Food Policy Research Institute (IFPRI).

Milgrom P, North D, and Weingast B (1990) The Role of Institutions in the Revival of Trade: The Law Merchant, Private Judges, and Champagne Fairs. Economics and Politics. 2(1) pp.1-23. https://doi.org/10.1111/j.1468- 0343.1990.tb00020.x

Nixon C and Yeabsley J (2002) New Zealand’s Trade Policy Odyssey: Ottawa via Marrakech, and on. Research Monograph No 68.

North D (1991) Institutions. Journal of Economic Perspectives Vol 5 No 1, Winter 1991.

NZIER (2005) Economic Trends and China’s impact on world trade. Report to the Ministry of Economic Development. November 2005.

NZIER (2017) Is peak globalisation upon us? NZIER public discussion paper. 2017/1, July 2017.

Puntigliano, AR and O Appelqvist (2011) Prebisch and Myrdal: Development economics in the core and on the periphery, Journal of Global History. 6, pp. 29–52.

This article is a re-post of the July 2020 Insight, from NZIER. It is here with permission.

20 Comments

Need more content of this quality and much, much less of the kind posted by Brooke rat-a-tat-tat van Velden yesterday. Vacuous nonsense. Go, you good farmers!

Pietro,

My view too. Well argued and balanced.

a wonderful and rational piece.

the author should be invited to the coming BRI conference.

We don't seem to hear as much about the BRI after the Covid nightmare.

It would act as a super-highway for the next virus out of China.

not sure if you keep up with any actual news or just stick with your Voice of America radio nowadays, I am sure everyone knows which country has successfully contained the COVID19.

And successfully exported it too.

Excellent brief thank you. As a result of Covid and investors better understanding the risks of other assets including property its highly likely we will see the smart money move into farm land as its such a safe long term hold that will always have a value.

"highly likely we will see the smart money move into farm land"

An enduring problem for me on this site is separating genuine opinion and sarcasm.

Wilco - thats a genuine opinion not sarcasm

It is interesting to see how farmers are diversifing their base products into multiple product types. Last Sunday's episode of County Calendar was a great example. How you go about investing in this aspect might be challenging.

What % of NZ GDP is constituted by exports to China and elsewhere?

China, Germany and NZ are highly reliant on exports income

Thus, if the countries we 3 want to export to have lower GDP, they will import less from us all else being equal.

China has put most of its eggs in export basket. Lately we see that Japan's imports from China are 30% lower than this time last year, so China's professed figs re exports and GDP are highly questionable in Q2.

The economic impact of CV19 will be seen in Q3 and Q4 and thereafter, in terms of lost production, consumer demand and jobs, plus government ballooning debt and cratering revenues. At the moment we remain in the dark on how bad things will be

This article would get my vote for the 'Interest.co Top Prize of the year for Informative Journalism': a masterpiece of informative and comprehensible writing.

Of particular importance is the nature of the land-based products we trade.

Agreed. We import phosphate (a finite rsource)

We import fossilised sunlight (we call it fossil fuel - also a finite resource.

We import 'palm kernel' (calling it a by-product, but it really represents the clearance of - finite, you guessed it) land elsewhere.

We used some of #2, to extract water that was already doing something else.

All of which says what we're doing is un-maintainable. So why, exactly, are we lauding it (in present form)?

“Modern agriculture is the use of land to convert petroleum into food”- Albert Bartlett

Because it maintains our current standard of living which allows you to pontificate

Not that I support the clear felling of native forest, I'll note two things.

1) we did it already, so it's a bit rich complaing about others.

2) the resulting palm crop is a renewable resource, not finite.

pdk,

The present farming model-as practiced by most- is indeed unsustainable. Some things will change due to the potential loss of social licence, palm kernel certainly and phosphate, some things will change as more evidence emerges on regenerative farming, somethings will change as plant based food gains ground and some things will change as climate change intensifies.

“ importing sheep and goat milk from across the world to process in New Zealand as infant formula for the Chinese market”

It doesn’t seem kosher to me but I guess it is common practice...

Good stuff David & co. More of these please.

Excellent article, good to see quality analysis like this. Makes subscribing to Interest well worthwhile & shows up how poor some of the MSM articles are.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.