This article is a re-post of Westpac's Meat Matters, and is here with permission.

– Improved meat processing capacity, falling shipping costs and the weak New Zealand dollar all should boost farmgate meat prices over coming months.

– However, the global meat market outlook for the season overall has become less clear and the range of possible prices has widened.

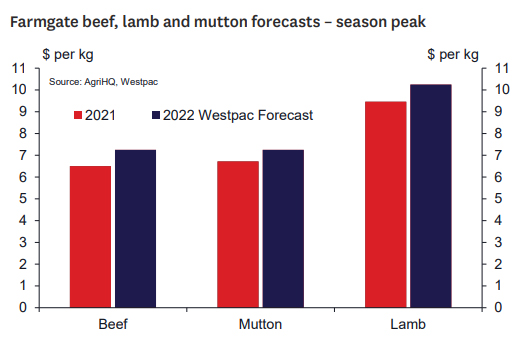

– Nonetheless, our best estimate is still for farmgate beef and mutton prices to crack $7.00/kg and for the farmgate lamb price to surpass $10.00/kg this season.

Back in April, we stuck our necks out and forecast that this season beef and mutton prices would crack $7.00/kg and that lamb prices would surpass $10.00/kg. All these prices, if achieved, would set record highs. Now, here in July and even with all that’s going on, we are sticking with these forecasts.

But to be fair, the market picture is as complicated as it has ever been. So, the range of possible price outcomes has widened since April. Indeed, it’s early days in the season and a lot can happen between now and when prices usually peak in (late) spring. And of course, the peak slaughter period during next year’s autumn is even further away.

With all that in mind, below we step through the likely drivers of prices over coming months on both sides of the “yeah, nah” equation.

Yeah…

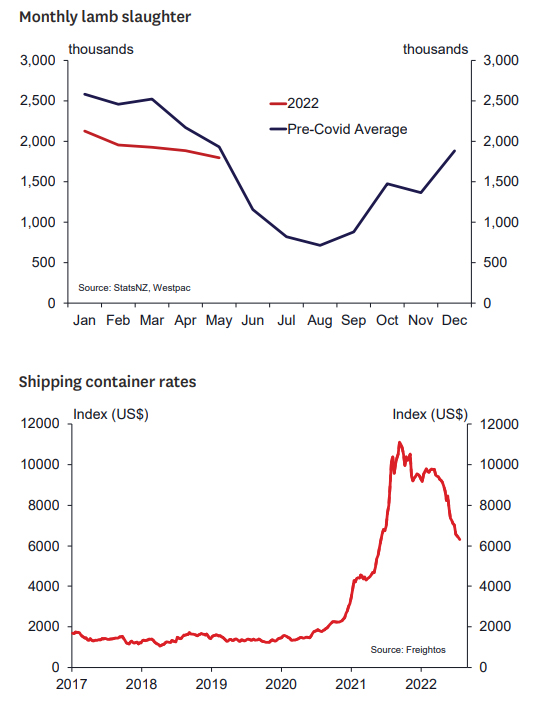

Local meat processing capacity has improved. The number of lambs processed over May was just 7% below the pre-Covid average for May. Whereas between January and April, the number processed was down nearly 19% on the average for same period pre-Covid.

At the same time, shipping costs are also falling. For example, the cost of shipping containers (as measured by the Freightos Baltic Index) has fallen by around a third since mid-March.

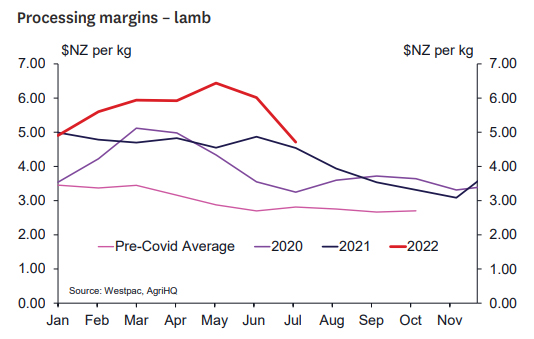

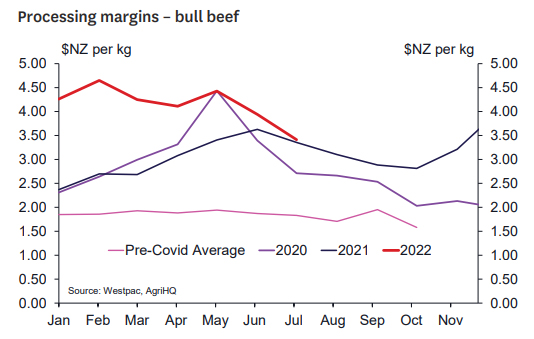

These moves have led to a narrowing of processing margins. Indeed, since the blowout in margins earlier in the year, lamb processing margins have narrowed by over $1.70/kg and are nearing the level that they were back in 2021. Essentially that means that more of the value of a lamb in international markets is making it back to the farmer. It’s a similar picture for beef.

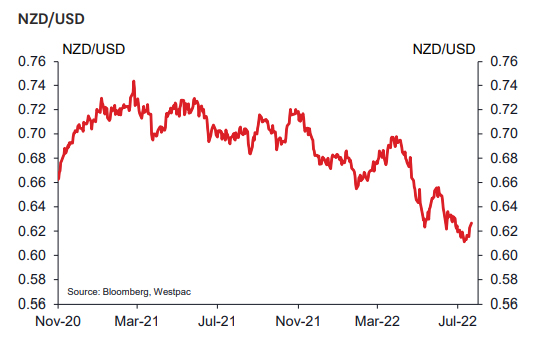

Meanwhile, the NZ dollar is also very supportive of farmgate meat prices. Since March, the NZD/USD has fallen from around US$0.70 to as low as US$0.61 at one stage. The nine-cent fall equates to a circa 13% drop, although the dollar has since rebounded back to the US$0.62 range.

On the global meat supply side, corn and other feed prices remain very high. This fact is putting the squeeze on farmer margins. In the case of Chinese pork, the margin above feed costs is barely above breakeven. In turn, this is forcing Chinese farmers to reduce their pork herd, notably with the number of sows dropping over the past year or so. Lower numbers of sows are translating into lower Chinese pork production and lifting Chinese pork prices. As pork has become more expensive, some Chinese consumers are shifting to other meats like beef, lamb and mutton and this is underpinning prices for our meat exports.

… nah…

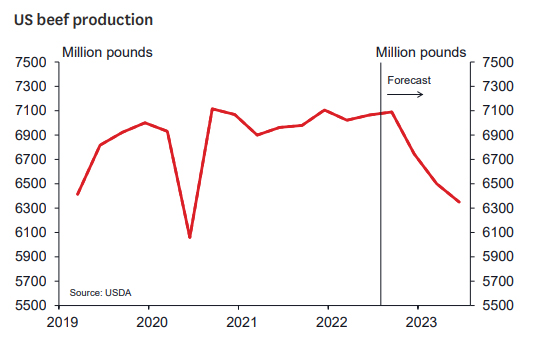

On the “nah” side of the price equation is a major destocking that is taking place in the US beef industry. US beef producers are slaughtering some of their breeding stock and this is leading to a lift in beef production and putting downward pressure on US and global beef prices. The catalyst for the destocking is very low returns off the back of very high feed costs.

However, this downward pressure on prices should prove temporary. A smaller breeding stock will lead to less beef production down the track as fewer beef cattle calves are born. For example, the US Department of Agriculture expects US beef production to peak in the September quarter (i.e. now) and to fall by 10% by June quarter of next year. And as production falls, prices should recover.

We also expect global meat demand to slow this year. Indeed, we expect the global economy to slow from 6.1% growth over 2021 to around 3.4% over 2022. As a result, we also expect lower demand to add downward pressure on global meat prices.

Meanwhile, the impact of the Covid outbreak in China is also a source of uncertainty for global meat prices. The Chinese economy grew by a miserly 0.4% over the June quarter compared to the same quarter a year ago. And while we expect the economy and meat demand to rebound over the second half of the year as Covid restrictions ease and government stimulus takes hold, the Covid outbreak could still curtail that view.

Covid could do similar damage here. For example, we have seen processing capacity improve lately, but Covid could re-emerge and when combined with a flu outbreak, worker absenteeism could spike again. As we have become all too aware, nothing is certain these days.

… yeah.

So, there’s a lot going on and there are risks aplenty. However, on balance, “yeah” we are sticking with the farmgate price forecasts that we set back in April. That means we still expect lamb prices to hit $10.00/kg this spring. At the same time, we also expect beef and mutton prices to lift to $7.00/kg.

This article is a re-post of Westpac's Meat Matters, and is here with permission.

Lamb: 9.12/kg, +4.3% (monthly change), +7.3% (annual change)

Y Lamb

Select chart tabs

Mutton: 6.08/kg, +3.7% (monthly change), -4.5% (annual change)

Beef (P2 steer): 6.11/kg, +1.6% (monthly change), +5.8% (annual change)

P2 Steer

Select chart tabs

M2 Bull

Select chart tabs

2 Comments

Well at least something's going to go right in the next 6 months. This is an informative report, a bit like the log report. But no comments. I guess because it's not about houses?

As a venison producer its like there's an awesome party next door but I'm not Invited. Maybe we need a marketing campaign to explain to the world that deer are made of meat too.

We welcome your comments below. If you are not already registered, please register to comment

Remember we welcome robust, respectful and insightful debate. We don't welcome abusive or defamatory comments and will de-register those repeatedly making such comments. Our current comment policy is here.